Jun 2

Why are $CBOE and $CME down so much over the past few days? LowVolatility factor is being hammered as everyone chases high Beta; factorstoday.com/factor/TG93…

4

29

3,751

🚨 $COST (Costco Wholesale) Q3 FY2026 Earnings

Resilient growth machine keeps firing…

Membership digital momentum remain the moat 👀

________________________________________

📊 KEY METRICS (Q3 FY2026)

🔹 Net Sales: $69.15B ( 11.6% YoY) 🟢

🔹 Net Income: $2.19B ($4.93 diluted EPS) 🟢

🔹 Adjusted Comp Sales: 9.8% companywide 🟢

🔹 DigitallyEnabled Sales: 21.5% 🟢

🔹 Membership Fees: $1.37B 🟢

🔹 Cash & Equivalents: $18.95B (up from $14.16B) 🟢

🔹 Operating Cash Flow (YTD 36 weeks): $11.13B 🟢

👉 Core takeaway:

Scale membership annuity ecomm acceleration delivering consistent results

________________________________________

📈 GROWTH ENGINE (CORE STORY)

🟢 Strong traffic ticket growth

🟢 Executive membership upgrades & fee revenue

🟢 Omnichannel (warehouse pickup, delivery, app)

🟢 International expansion new warehouses

👉 This is:

The quintessential defensive consumer staple growth compounder

________________________________________

🚀 STRATEGIC MOVES

🟢 Continued warehouse expansion (target ~30 new openings per year longterm)

🟢 Digital platform investments for seamless member experience

🟢 Supply chain & productivity gains to offset wage/inflation pressures

👉 Impact:

Sustained market share gains in a valuefocused consumer environment

________________________________________

⚡ WHAT’S HAPPENING?

• Costco’s model (lowmerch margins highmargin membership volume scale) proving durable

• Consumer tradedown behavior boosting traffic

• Digital channel compounding rapidly

👉 This is:

Steadystate execution excellence in a challenging macro

________________________________________

📉 PROFITABILITY (SOLID BUT AS EXPECTED)

🔻 Merchandise costs & SG&A rising with sales (typical scaling)

🔻 Higher investing cash use for growth/capex

👉 Translation:

High cash conversion and fortress balance sheet — profitability remains healthy

________________________________________

📅 OUTLOOK

No formal numeric guidance (Costco tradition), but:

🔹 Ongoing comp sales strength expected

🔹 Membership growth renewals remain high

🔹 Warehouse pipeline supports multiyear expansion

👉 Important:

Reliable compounding story intact

________________________________________

🧠 WHAT’S ACTUALLY WORKING

🟢 9.8% adjusted comps 21% digital growth

🟢 Membership fees as highquality, recurring revenue

🟢 Massive cash generation & strong balance sheet

🟢 Market share gains in groceries, nonfoods & ancillary services

________________________________________

⚠️ WEAK SPOTS

🔻 Rising operating expenses (labor, expansion)

🔻 Merchandise margin pressure from mix/inflation

🔻 Execution risk on new warehouses & digital scaling

🔻 Valuation already premium (priced for perfection)

👉 Still:

Extremely consistent, lowvolatility business

________________________________________

🧠 MARKET SIGNAL

👉 Defensive growth titan in retail

• Recessionresistant

• Membership moat

• Longterm compounding machine

________________________________________

🔥 BULL vs BEAR

🟢 Bull Case

• Sustained comps 69% with digital tailwinds

• Membership fee increases executive mix drive profits

• Warehouse expansion international upside

• Cash machine supports buybacks/dividends

🔴 Bear Case

• Consumer slowdown hits ticket/traffic

• Margin compression from costs/tariffs

• Premium valuation leaves little room for disappointment

• Slower growth normalization postpandemic boom

________________________________________

💭 CONCLUSION

$COST remains a highquality compounder executing at a high level…

👉 Reliable growth membership flywheel in an uncertain consumer world

1

2

178

May 25

📉 NIFTY MAY EXPIRY IN SLOW MOTION!

April Expiry closed at 23,995.70

Today we are trading at 24,031

→ Just 36 points net move in the entire May expiry so far!

Extremely low range, high tension consolidation. Big players are trapped and waiting for a trigger.

This kind of compressed price action usually ends with a violent move once the range breaks.

Are we building for a massive breakout or breakdown next week?

#Nifty #NiftyExpiry #Nifty50 #LowVolatility #OptionsTrading #StockMarketIndia #TradingSetup

youtu.be/WzPW8-3lowc

36 points in whole expiry? Your thoughts? 👇

#Nifty #NiftyExpiry #Nifty50

1

3

45

9,473

Mar 29

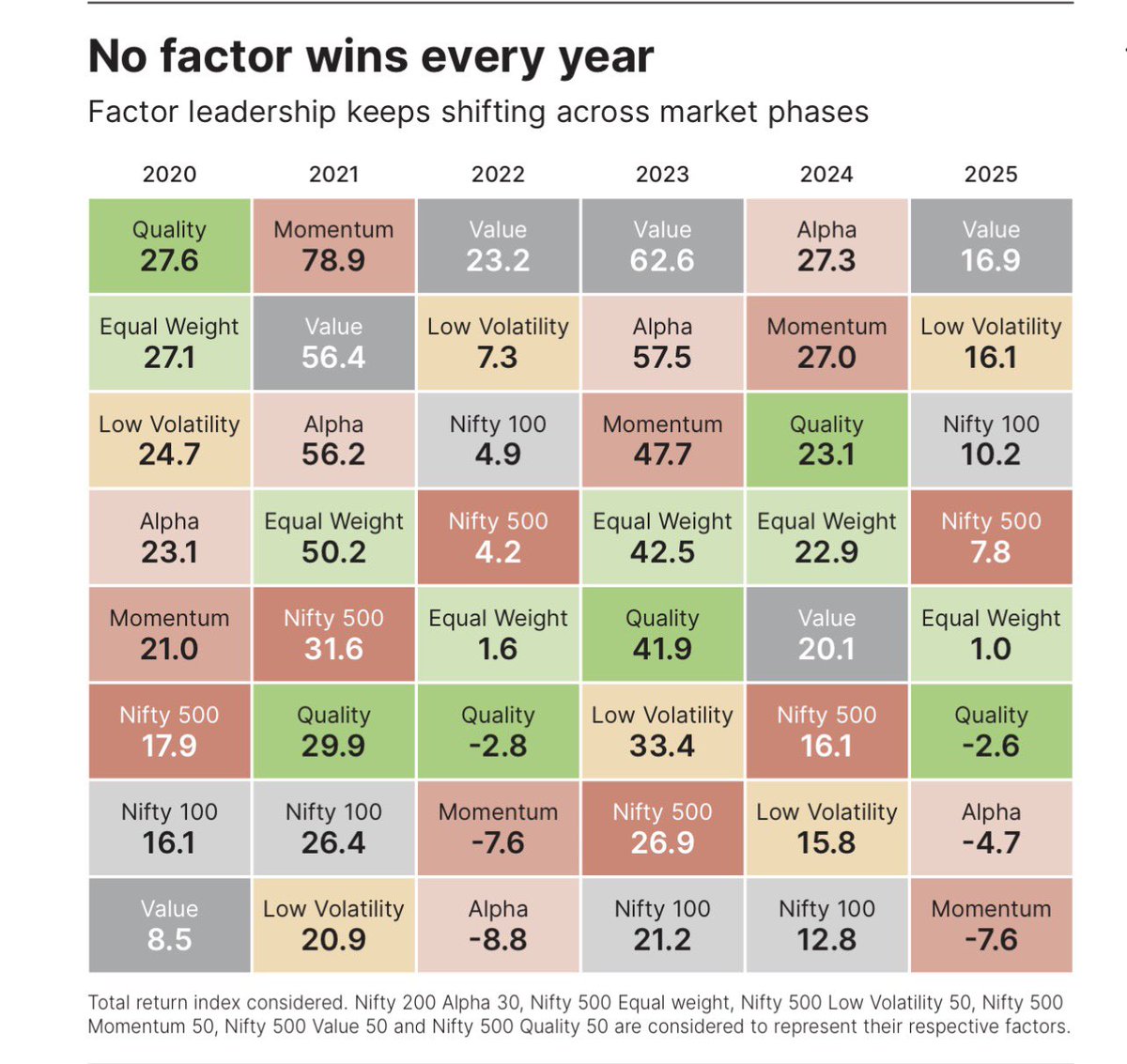

ETF factor-wise allocation:

Quality,

Equal Weight,

Low Volatility,

Alpha,

Momentum,

and Nifty 500 Value.

Which factor is likely to work best in 2026?

#ETFs #FactorInvesting #Quality #Momentum #LowVolatility #ValueInvesting #PassiveInvesting #2026Outlook

4

162

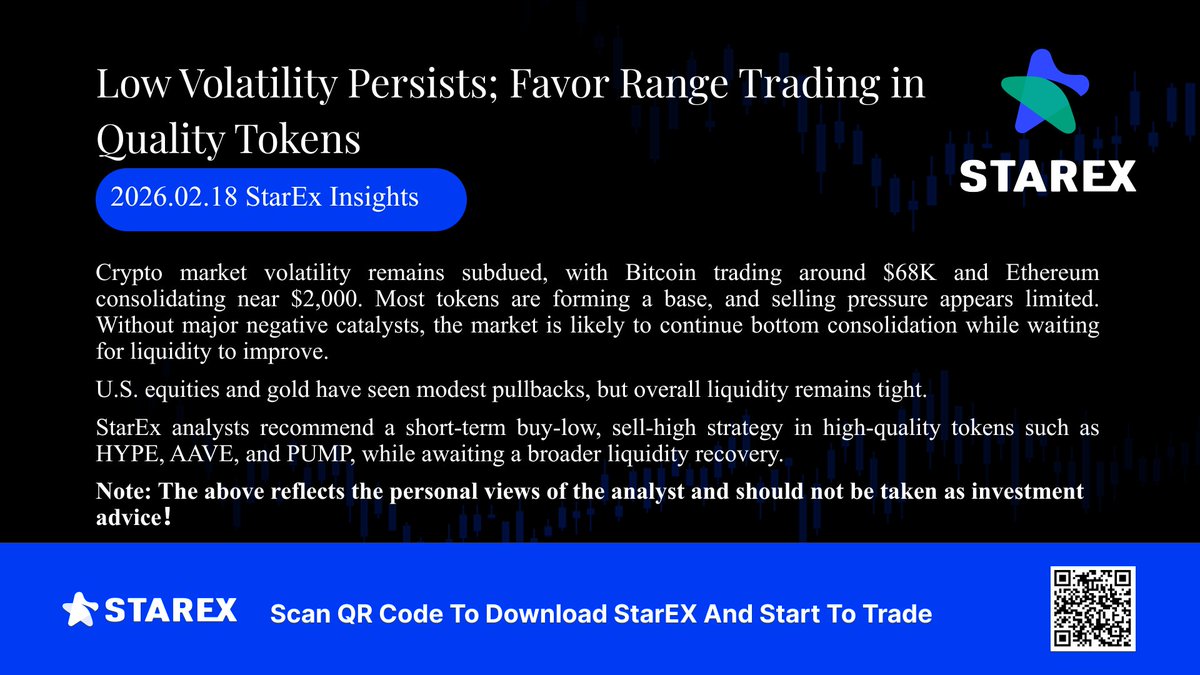

Feb 18

#StarEx Insights: Low Volatility Persists; Favor Range Trading in Quality Tokens

#Bitcoin #LowVolatility #RangeTrading #BuyLowSellHigh #Altcoins #StarExInsights

1

2

49

Feb 18

#StarEx 分析师观点:市场波动率减小,优质币种短线高抛低吸

#Bitcoin #LowVolatility #RangeTrading #BuyLowSellHigh #Altcoins #StarExInsights

1

2

47

Jan 7

Platykurtic returns

Platykurtic markets have flatter distributions.

Large price swings are rare and movements are steadier.

#MarketStability #LowVolatility #InvestingBasics

1

2

28

10 Dec 2025

BSE launches 4 new BSE 100 large-cap TMC universe factor indices yespunjab.com/?p=191530

#BSE #StockMarketIndia #FactorInvesting #LargeCapIndex #MomentumIndex #LowVolatility #ValueIndex #QualityIndex #ETFs #IndexFunds #InvestmentNews

@BSEIndia

88

25 Nov 2025

Tired of the constant market rollercoaster?

While the crypto world churns, @yuru_coin brings the ultimate peace of mind: The Power of Stability Amidst Market Fluctuations.

We're building more than just a coin—we're building a reliable haven

Why Anchor Your Portfolio with YURU

🛡️ Risk Mitigation Focus: Designed to act as a resilient anchor, $YURU aims to shield your assets from the sharpest drops and unpredictable market noise.

Calm Growth Path: We offer investors a smoother journey, prioritizing steady, sustainable accumulation over high-stakes volatility

💡 Foundation for Tomorrow: In a volatile space, YURU is the reliable cornerstone that secures your long-term vision and financial well-being.

Experience stability. Discover YURU Coin today👇

🌐 Learn More: coin.yurugp.jp

#YURUCoin #CryptoStability #MarketAnchor #LowVolatility

1

2

18

1,138

14 Nov 2025

When valuations are high and market drawdowns loom, a low-volatility strategy becomes relevant. See how HVOL & HVOI are structured for this moment.

#Market #Investing #LowVolatility #LowVolatilityETFs #PassiveIncome

harvestportfolios.com/how-a-…

1

2

179

8 Oct 2025

TOBACCO VANGUARD Est. 1977

Not for all and sundry.

Tobacco in Monetary Crisis: Cash That Pays For Order

By M. Reuven

Tobacco holds its ground in a monetary crisis when institutions hold theirs. Where tax is uprated with care, where enforcement is visible, and where firms can move price through a brand ladder without losing the customer, cash continues to arrive. Where real excise bites harder as incomes fall, where policy is erratic, or where illicit trade widens the price gap at the border, the story weakens. Defensiveness is not merely a legend of the sector, it is a function of monetary uncertainty and the discipline of the state.

The record across the last century divides neatly by regime. In a deflationary shock, administered taxes grow heavier in real terms unless governments adjust them. Volumes strain as unemployment rises and the customer reaches for cheaper forms. Manufacturers protect share by using pack size and trade terms, but margins compress if policy is slow to move. In an inflationary shock, the arithmetic is different. Prices rise, excise is uprated, and net realisation can hold or even improve if indexation is predictable and collection is strict. The habit persists, though the basket changes. Premium turns to value, factory-made turns to roll-your-own or local equivalents, but the line of cash does not break if brands offer a step down that does not feel punitive.

Leaf and farming tell the same story from the other end of the chain. Tight money starves growers of credit, lowers the bid for lower grades, and narrows the quality mix. Inflation and currency depreciation raise nominal prices, but the terms belong to the buyer if contracts are short and the exporter is desperate for foreign exchange. Multinationals smooth this with forward cover and inventory planning, though they carry the working capital while policy catches up. Where a government lets credit to agriculture vanish in a panic, next season’s yield is smaller and less even. Where contract farming and seasonal finance are maintained, both sides endure.

Distribution is where the state’s will is measured. During down-cycles, the incentive to evade tax rises at the very moment the exchequer needs the money. If enforcement is visible, if track-and-trace works, and if the legal market keeps a credible value brand, illicit share stays contained. If not, income falls while the price signal points out of the legal channel, and the industry pays twice, once in lost volume and once in reputational noise from the trade it does not control. Cross-border gaps tell in the figures long before a minister admits it.

On the shop floor the mechanism is simple. In every downturn the customer trades down, but he does not walk away at once. Short-run price elasticity is modest in cigarettes, lower still among established users, and income effects push the buyer along the ladder rather than out of the door. Over longer horizons, prevalence continues to drift lower for reasons that sit outside the cycle. The task for management is to keep a clean stairway of price points, defend availability, and convert list price into net revenue after excise without courting the switch to illicit supply. The firms that do this set their structure in calmer years and reap the benefit when money tightens.

Listed equities reflect these mechanics with a lag. In deflationary episodes, the sector draws less than the market and recovers dividends sooner where cover is sound and the currency mix helps. In inflationary episodes, total returns hold up when pricing power is accepted by policy and the customer, and when working capital is managed without starving the buyback. Where regulation is capricious or headline policy turns hostile to visibility, multiples compress regardless of cash. Markets are reflexive. Narrative moves discount rates and boards respond with the tools they control, chiefly the pace of capital returns and the signal of a maintained dividend. Investors call this defensiveness. In practice it is conditional on jurisdiction, tax design and enforcement, and the maturity of the brand ladder.

One sees the pattern clearly across three points in time. The deflation of the inter-war years punished any industry that relied on administered taxes that failed to adjust, and rewarded those who secured relief or re-graduation of duty. The global financial crisis reopened the value end of the market and lifted roll-your-own, yet the larger firms protected cash margins by steady net pricing and tight cost control. The post-pandemic inflation shock brought supply disruption and sharp uprating, but where governments indexed within known rules and collected with vigour, the firms carried price through without a break in the cash return. Where policy surprised or enforcement was weak, illicit share rose and legal volumes dipped further than income alone would have implied.

The leaf countries under inflation offer a further lesson. Currency depreciation flatters export receipts in local terms but squeezes inputs priced in hard currency. The manufacturer sees costs rise, yet can often smooth the pass-through if excise rules are stable. The grower needs credit and a buyer who honours contract weights on time. Without those, acreage falls and quality fades, which raises blend costs a season later. Cash that is not paid in the field turns into margin that is not earned in the factory.

For ministers, the instruction is clear. If you depend on tobacco excise for revenue, maintain a credible, rules-based uprating schedule and enforce it. Keep the legal price ladder intact so that the customer can step down inside the taxed market. Police the borders and the wholesale channel, not by press release but by seizures that change behaviour. In deflation, review real burdens promptly or you will crush the legal base you rely upon. In inflation, set the rule and stick to it or you will push the price signal into the shadows and miss your own target.

For boards, the order of battle is also clear. Preserve the architecture of brands and packs, and keep value credible. Plan working capital for longer supply chains and slower remittances when money is tight. Protect the dividend if cover is real, since the equity signal stabilises the multiple when headlines do not. Do not assume defensiveness is a birthright. It is earned in procurement, pricing, and the dull work of trade discipline long before a crisis arrives.

For investors, read the structure before you read the chart. Look for jurisdictions with predictable uprating, visible enforcement, and a legal value tier that is not a fiction. Prefer firms with clean cash conversion, modest capex needs, and a history of passing price without destroying share. Treat buybacks as flexible, not sacred. Judge dividend policy by cover, not by the rhetoric of permanence. When the cycle turns, the best tobacco equities show narrower drawdowns and quicker income recovery than the market, but only where these conditions hold.

The conclusion is not romantic. Tobacco is defensive when the state behaves as a serious steward of the tax base and when management maintains a rational ladder of choice. It is less defensive when policy uses it for theatre, when excise is moved without regard to income or border arithmetic, and when illicit supply is allowed to masquerade as virtue. In monetary crisis, cash pays for order. The exchequer, the industry and the investor all have an interest in keeping that cash on the books.

Publisher’s note: This commentary examines lawful industries and public policy in an analytical manner. It does not promote consumption of tobacco products.

#TobaccoVanguard #Tobacco #ConsumerStaples #MonetaryCrisis #Inflation #Deflation #RealRates #Excise #TaxPolicy #Enforcement #IllicitTrade #PricingPower #BrandLadder #DownTrading #RollYourOwn #CashFlow #Dividends #Buybacks #LowVolatility #Equities #GreatDepression #GFC #PostPandemic #BAT #ImperialBrands #Altria #PhilipMorris #JapanTobacco #ITC

2

2

211

15 Sep 2025

🧐 Can you win in #LowVolatility slots?

The answer is.. Yes!

Low volatility offers:

🔸Smaller but consistent #wins

🔸Longer play, lower risk

🔸Easier #bankroll management

Spin & prove the wins are real: betfury.tv/_All_Games

Which slot in the pic is Low Volatility? Answer ↓

15

3

12

1,254

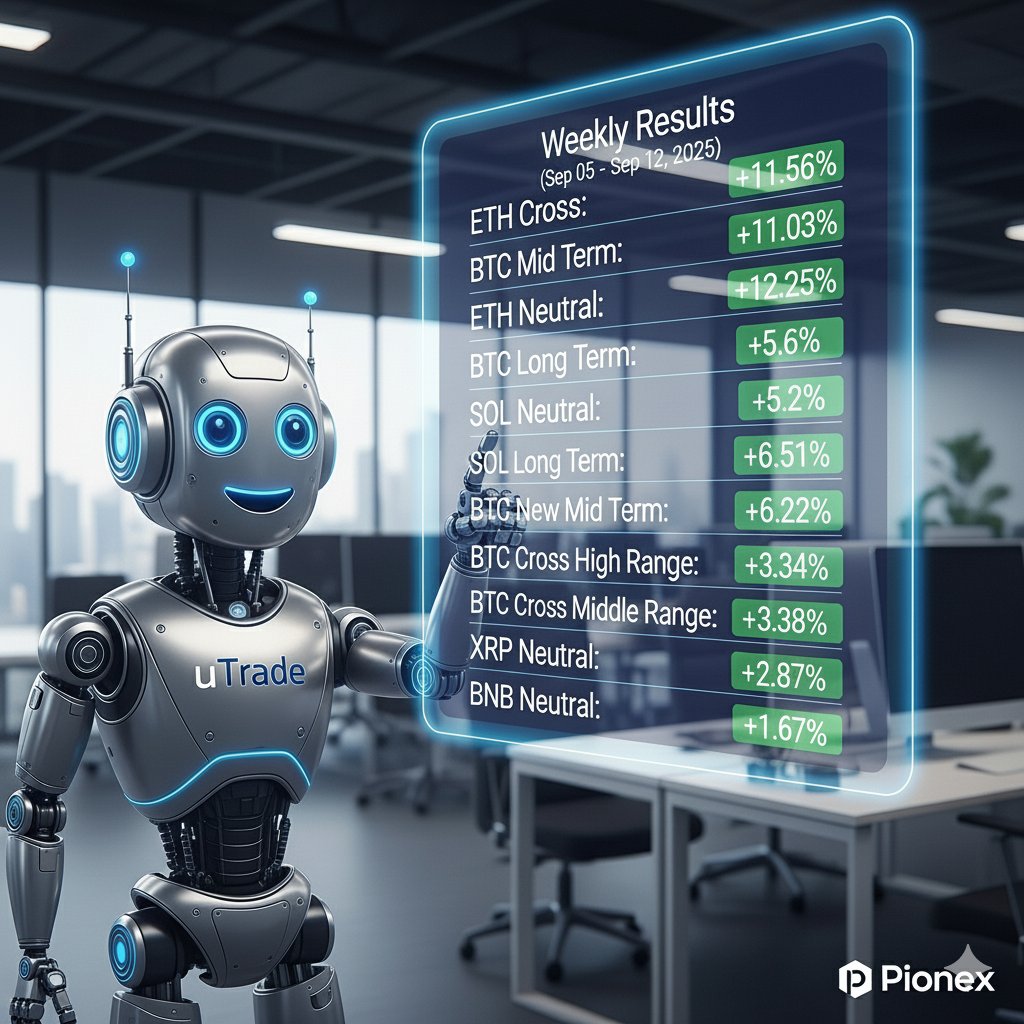

12 Sep 2025

uTrade in the Calm Before the Storm: Low Volatility Ahead of FED Showdown – Our Bots Stay on Track! 🚀

Dear uTrade Community,

The markets are holding their breath! 🌬 We look back on a week of extremely low volatility, where almost nothing moved. Everyone is eagerly awaiting the biggest showdown: The FED's interest rate decision next week! Will it be a 25 basis point cut or perhaps even 50? This uncertainty paralyzes the market, but we stay on course! 🚨

Today at 4:00 PM (CET), we also expect important US economic figures, which might bring some movement into the sluggish market. Be ready!

Despite the almost icy calm, our bots have delivered results even in this challenging week (Sep 05 - Sep 12, 2025). Here's the proof of our resilience: 🤖

✅ BTC Mid Term: 11.56%

✅ ETH Cross: 11.03%

✅ BTC Long Term: 5.46%

✅ ETH Neutral: 5.25%

✅ SOL Neutral: 6.51%

✅ BTC New Mid Term: 4.72%

✅ BTC Cross High Range: 3.34%

✅ BTC New Long Term: 3.38%

✅ BTC Cross Middle Range: 3.27%

✅ XRP Neutral: 2.87%

✅ BNB Neutral: 1.67%

Breaking News: Your NFTs Generate Mega Profits – Even in a Downturn! 💎

Since September 1st, 2025, the start of passive income for our NFTs, we have reached a milestone that is unparalleled! Despite the extremely low volatility, we managed to break the magical threshold of 11,228 USDT in profit! An impressive five-figure sum that proves: uTrade NFTs are a game changer, even when the market is quiet! This success belongs to you – whether you use bots or own our NFTs. Together, we make it happen! 💪

Ready to stay on the ball and seize opportunities even during lulls? Discover the power of our bots!

Register now and be part of the success:

👉 accounts.pionex.com/en/signU…

In these phases, discipline and strategic action are crucial. Remember your profits and secure your positions. Risk management is more important than ever! 🛡

We wish you a weekend full of foresight and smart decisions!

Stay focused and act cleverly!

Best regards,

Your uTrade Team

#uTradeUpdate #LowVolatility #FEDDecision #TradingBots #CryptoMarkets #NFTProfits #Pionex #MarketWatch #SmartTrading #HappyProfits

32

10

17

236

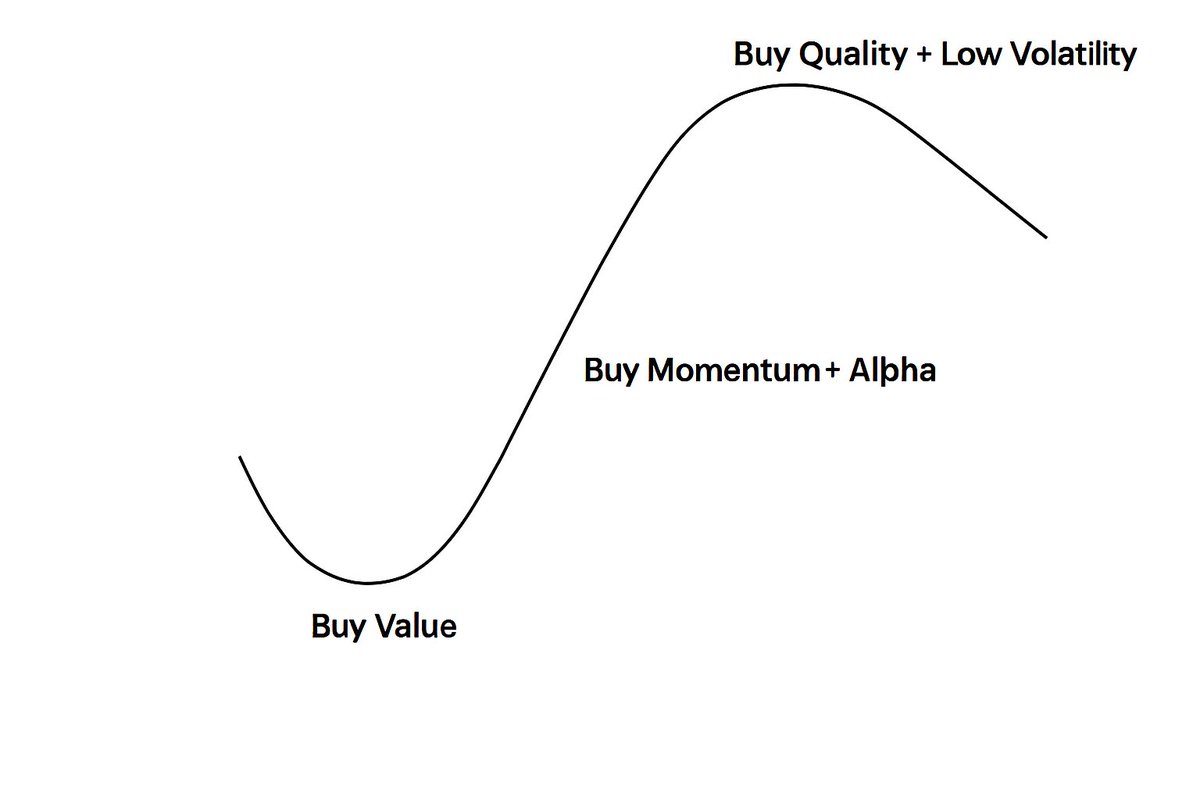

6 Sep 2025

Play the market cycle by rotating factors

Buy #Value at the bottom,

Ride #Momentum #Alpha in the recovery,

Protect with #Quality #LowVolatility when euphoria peaks

6

20

254

23,609

11 Aug 2025

altcoins are risky. lowvolatility options better.

1

20

11 Aug 2025

altcoins are risky. lowvolatility options better.

18

1 Jul 2025

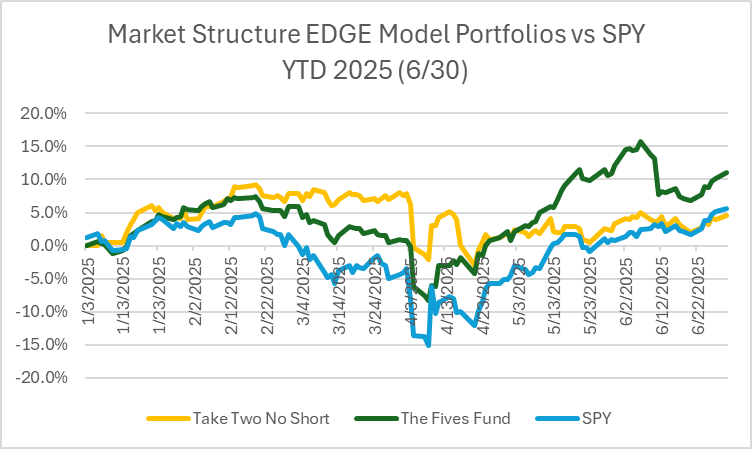

Interesting: @EdgeStructure model portfolios for #momentum and #lowvolatility here vs $SPY YTD 2025 (as of Jun 30). The Buy Fives (lovo) is killing $SPY while #momo trails. I highly speculative momentum fund is up 33.7% but it's got poor liquidity so we didn't share it.

1

3

306

1 Jul 2025

London Silver Bullet short today - clean read, solid points. But price was slow, no real volatility, so kept it to paper trading. Tape read was on point tho. 🔥

#SilverBullet #PaperTrade #TapeReading #DayTrading #Scalping #PriceAction #LowVolatility #LondonSession

4

190

17 Jun 2025

The OLTA Low Volatility Index curates a basket of digital assets and recalibrates risk at every rebalancing, giving both retails and institutionals allocators a calmer route into crypto.

Denominated in USDC, it brings disciplined risk control to a market known for sharp swings.

By tempering deep drawdowns, the strategy helps investors stay the course through turbulent cycles.

oltafinance.gitbook.io/oltaf… 🔗

#LowVolatility #RiskManagement #Indexing

11

230

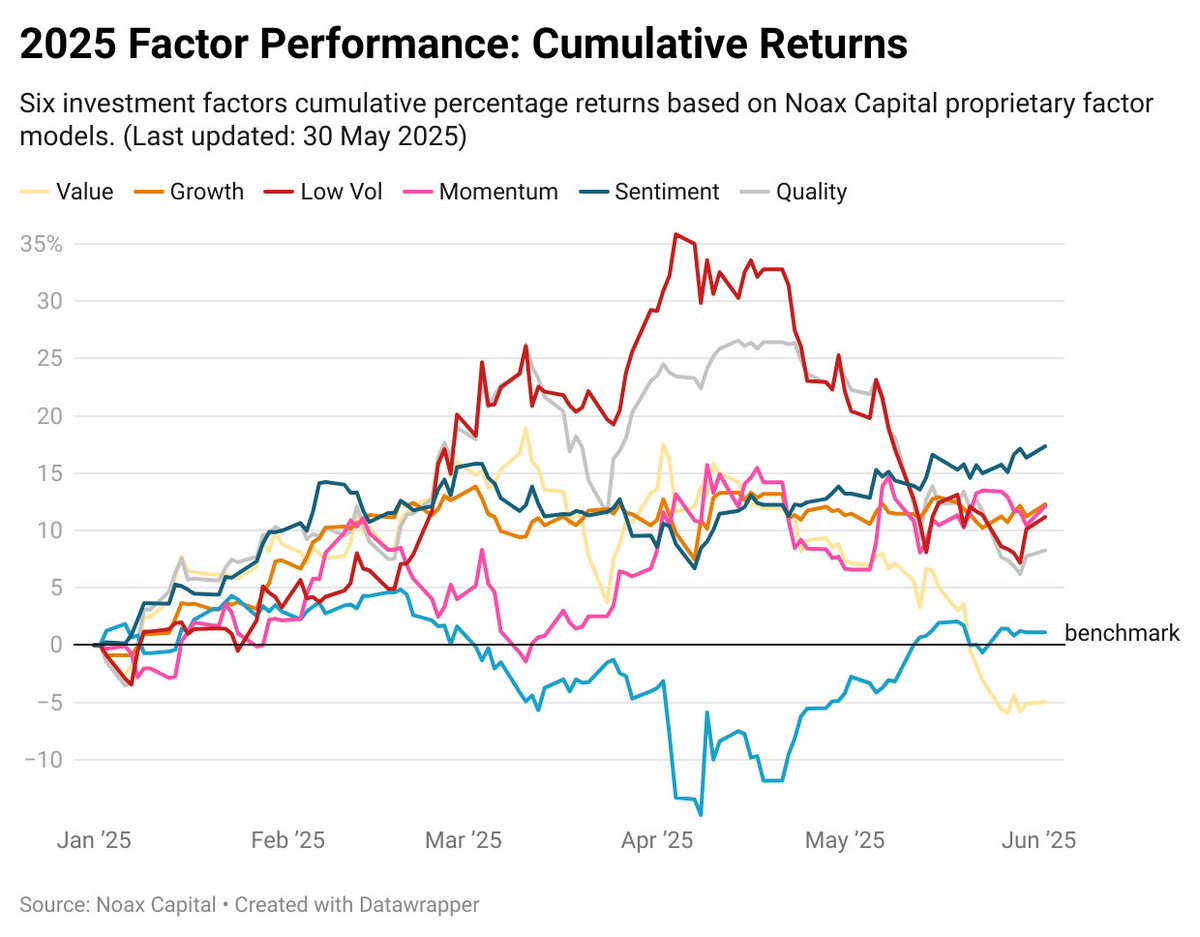

2 Jun 2025

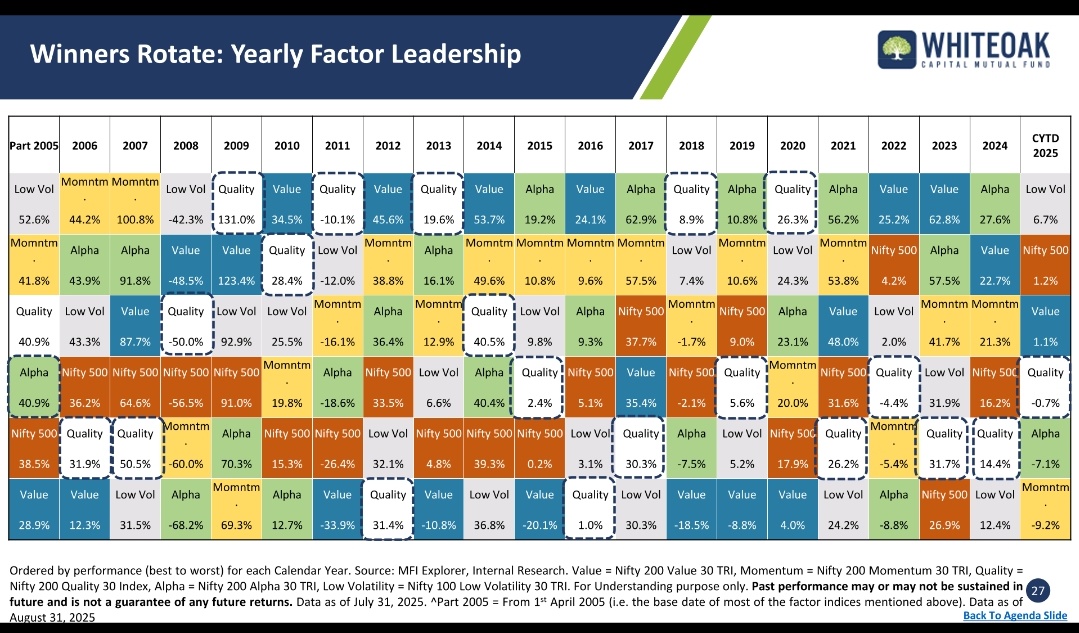

Low Vol & Value: My Take on Their 2025 Rollercoaster

I’ve been closely watching the wild ride of Low Volatility and Value factors this year. They were rock-solid during the March tariff chaos, acting as a safe haven when markets got shaky. But since May’s aggressive rebound, they’ve been lagging behind, struggling to keep up.

This flip from strong defense to trailing the pack in today’s bullish, high-momentum markets has me thinking: Are Low Vol and Value losing their mojo in these fast-moving markets? How should we adjust our portfolios to navigate this? At Noax Capital, our long/short equity strategies spread bets across factors and weave in some factor timing to juice up returns.

#FactorInvesting #LowVolatility #ValueInvesting #NoaxCapital

Factors Last updated: 30 May 2025

1

12

1,180