Nara e taqbeer allah who da akhbar

Sar tan sey juda sar tan sey juda

La ilaah illillah mommed rassool lalla

-

Islam key manind hai gesu mere ghashyaam key

Kafir hai woh log joh bande nahi iss laaam key!

1

15

Karachi mein ghar se bahir nikal na ek jang e azeem ke manind hai bhai if you do not have a driver.

132

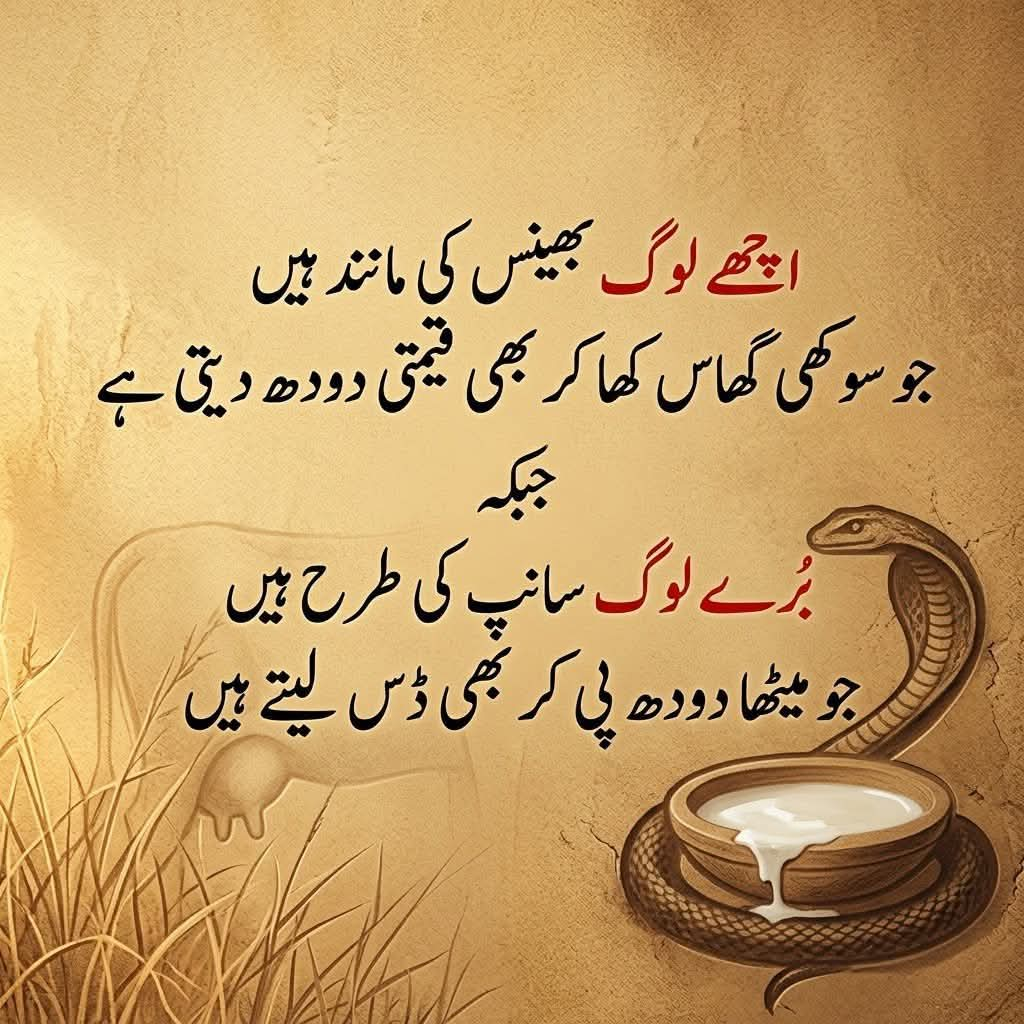

𝐀𝐜𝐡𝐡𝐞 𝐋𝐨𝐠 𝐁𝐡𝐚𝐢𝐧𝐬 𝐊𝐢 𝐌𝐚𝐧𝐢𝐧𝐝 𝐇𝐚𝐢𝐧

𝐉𝐨 𝐒𝐮𝐤𝐡𝐢 𝐆𝐡𝐚𝐚𝐬 𝐊𝐡𝐚 𝐊𝐚𝐫 𝐁𝐡𝐢 𝐐𝐞𝐞𝐦𝐭𝐢 𝐃𝐨𝐨𝐝𝐡 𝐃𝐞𝐭𝐢 𝐇𝐚𝐢

𝐉𝐚𝐛𝐤𝐞, 𝐁𝐮𝐫𝐞 𝐋𝐨𝐠 𝐒𝐚𝐚𝐧𝐩 𝐊𝐢 𝐓𝐚𝐫𝐚𝐡 𝐇𝐚𝐢𝐧

𝐉𝐨 𝐌𝐞𝐞𝐭𝐡𝐚 𝐃𝐨𝐨𝐝𝐡 𝐏𝐞𝐞 𝐊𝐚𝐫 𝐁𝐡𝐢 𝐃𝐚𝐬 𝐋𝐞tey hain

1

224

Jun 11

Ali KO log pehchan na PAYE yeh logon ki bdqismati thi .islam main 73 fiqah bnatay hi nhi ager Ali KO Jaan letay.islam nozaidah bachay ki manind tha Ali ager talwar utha letay to siwaye chund ke SB wapis palat jatay apnay forefathers ke Deen pr.surah munafiqoon to perhi hi hogi.

1

211

Jun 11

Dil jesay diya ki manind hai bujh jata hai phir kisi ki amad sy diya jul utha hai ..

1

27

Jun 11

Now that you have written such an exquisite piece- it calls out for a reply from the heart.

It took me down the memory lane . I am reminded of a couplet-

Kabhi hum bhi khubsurat thhe, kitabon mein basi khushboo ki manind saans saakin thhi.

Flirtation as an art had a fragrant quality that lived inside old books, not loud or attention-seeking. It waited quietly to spread its wings only when the pages were turned. It was never really overtly flirtatious - just subtle.

Another one by Parveen Shakir goes-

Jab se baat phail gayi shanasai ki, usne khushboo ki tarah meri pazeerai ki.”

No wild declarations of love but so emotionally drenched that it works through atmosphere.

I am unaware of the spirit of flirting today. Availability has short-circuited the mystery.

Have never been the flirtatious kind. I am tempted at this age and suddenly - Dil toh bachha hai ji resonates. 😊

Lots of lovely writing. Keep shing. ✨

1

3

118

Jun 9

Of course, being religious is the biggest, provable mass psychosis in the history of Manind, which has led to hundreds of millions of deaths since it's inception. Not going to miss that point. But, then he got to this:

2

Jun 6

Jo ap ko DM kartay hoon gy meraa nhi khiyal aap unhain kabhi jawab deti hoo gi . Kamar jhuk jy gi dant tootnay par a jain gy kuch log Pahar ki manind pathar ho chukay hotay hain un par kisi baat ka asar nhi hotaa. Aap ky sawal durust jawab nhi mil sakta kahaiyan ho sakti hain

1

105

May 26

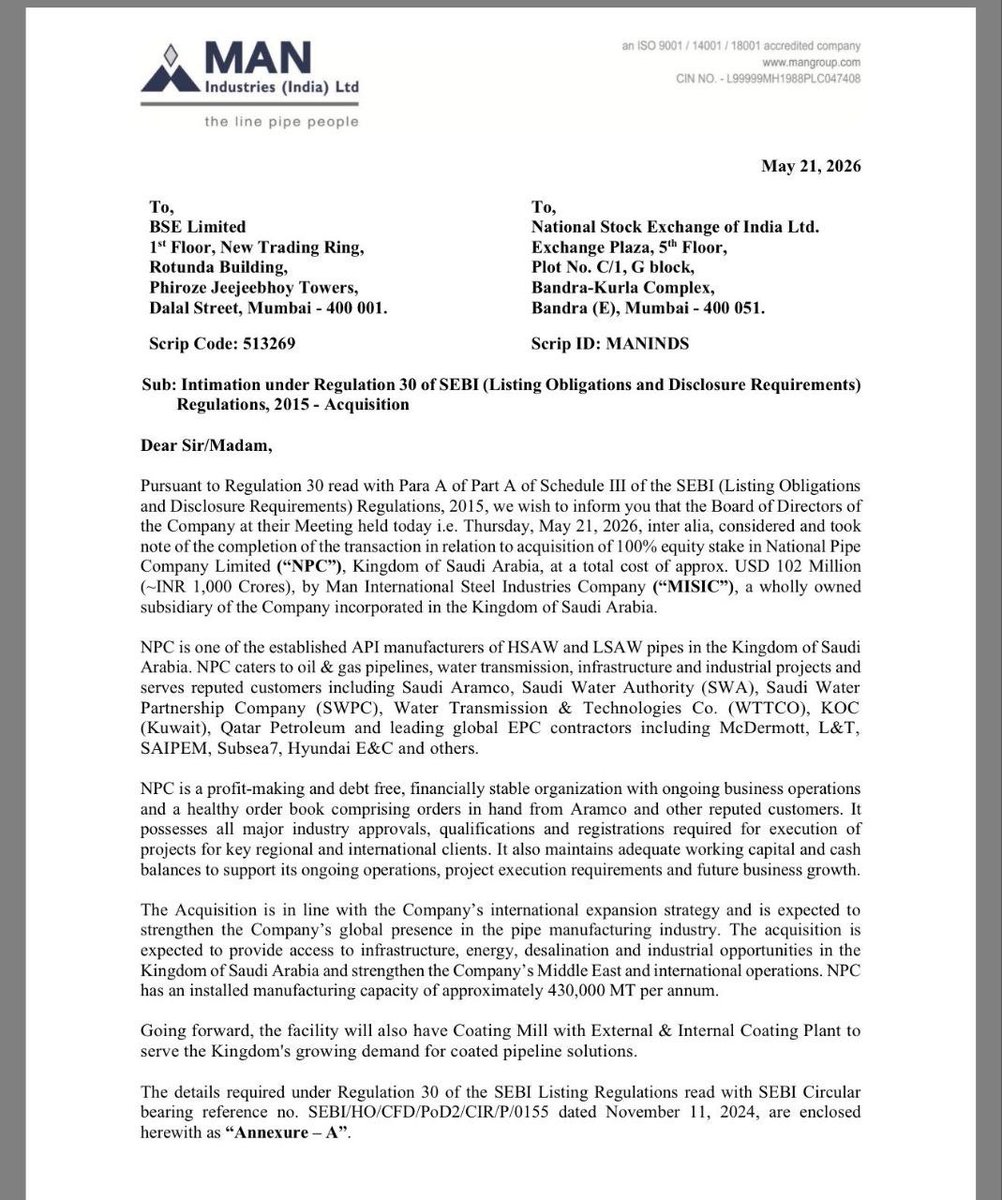

Man Industries (India) Ltd.📞 Q4 & FY26 Concall Summary #MANIND

🟡 MANAGEMENT PROJECTION :

Management guided FY27 consolidated revenue of 5,000-5,500 crores versus FY26 revenue of around 3,600 crores, implying nearly 40-50% growth. India operations are expected to contribute around 4,000 crores while Saudi operations through NPC could contribute 1,500-2,000 crores with 15% EBITDA margins. Management also guided for 13-15% sustainable EBITDA margins going forward. FY28 revenue growth is expected at another 25-30%. NPC utilization is targeted to reach 80-85% by FY28/FY29 with peak revenue potential of 3,500-4,000 crores. The upcoming Saudi coating facility is expected to generate 25-35% EBITDA margins, while Jammu stainless steel plant utilization is guided at 35-40% in FY28.

🔴 Red Alert :

Global geopolitical risks and shipping disruptions remain a key concern, especially around the Strait of Hormuz which already delayed some shipments during Q1. The company also reported a 25 crore forex MTM impact related to Jammu capex imports due to rupee depreciation. Debt will increase at the Saudi subsidiary level after the NPC acquisition and coating capex, with consolidated interest costs expected around 160-170 crores in FY28. Additionally, execution risks remain around integrating NPC, scaling Saudi utilization, and commissioning both Jammu stainless steel and Saudi coating facilities on time.

🟢 Green Alert :

Man Industries delivered its best-ever year in company history with standalone EBITDA margins reaching a record 14% and consolidated EBITDA touching an all-time high of 468 crores. FY26 standalone revenue grew 11% to 3,508 crores while EBITDA surged 49% to 493 crores. Q4 was especially strong with standalone revenue growing 36% YoY to 1,147 crores and PAT rising 72% to 70 crores. The biggest highlight was the acquisition of Saudi-based NPC at an extremely attractive valuation of just 1.5x EV/EBITDA. NPC comes with 430,000 tons running capacity, Aramco approvals, debt-free operations, and around $120 million order book. The company also ended FY26 net cash positive with 657 crores cash balance.

🔵 Blue Alert :

Man Industries is transforming from an India-focused pipe manufacturer into a globally integrated cross-border pipeline infrastructure platform spanning India, Saudi Arabia, coating solutions, stainless steel pipes, and large-diameter energy and water transmission projects. The NPC acquisition strategically places the company directly inside Saudi Arabia’s massive oil, gas, and water infrastructure ecosystem under Vision 2030.

🧠 Deep Insight :

The NPC acquisition could become a transformational turning point for Man Industries. Instead of spending years building a new Saudi facility, obtaining API certifications, and securing Aramco approvals, the company acquired a fully operational high-quality asset at a fraction of replacement cost. More importantly, Saudi Arabia and the broader GCC region are entering a massive infrastructure cycle across oil, gas, desalination, hydrogen, and water transmission. By combining Indian manufacturing scale with Saudi localization and coating capabilities, Man Industries is positioning itself as a rare integrated player across two major energy corridors. If management successfully scales NPC utilization and maintains execution discipline, the company could structurally shift into a much larger global energy infrastructure platform over the next several years.

1

2

718

May 26

Good #Q4FY26-25/5/20206 post 11pm

Pace Digitek

#PaceDigitk

#PaceDigitek

Finally delivers an extremely strong Q4FY26 after couple of tepid quarters post listing

Good Q4FY26

Rev at 1097cr vs 683cr, Q3 at 644cr

EBITDA at 163cr vs 76cr with OPM at 14.9% vs 11.2%

Other income at 20cr vs 7cr

PBT at 146cr vs 75cr, Q3 at 114cr

PAT at 106cr vs 56cr, Q3 at 79cr

OCF at -917cr vs -176cr

Steep increase in recievables at 2067cr vs 1270cr

Inventory at 540cr vs 113cr

Needs close monitoring

Orderbook healthy at 11338cr

Madhusudan Masala

#Madhusudhan

Good Q4FY26 and H2FY26

Good Q4 uptick as guided by the management in Q3 concall

Rev at 97cr vs 73cr, Q3 at 76cr

PBT at 8.3cr vs 5.5cr, Q3 at 6.3cr

PAT at 6.1cr vs 3.6cr, Q3 at 4.7cr

OCF at -0.8cr vs -39cr

Man Industries

#ManInd

Last year Q4 had 369cr coming from Merino Shelters which was. L not repeatable

Adjusted for which,

Rev at 1157cr vs 850cr, Q3 at 804cr

EBITDA at 171cr vs 101cr, Q3 at 142cr

OPM at 14.6% vs 11.6%

PBT at 95cr vs 57cr, Q3 at 82cr

PAT at 70cr vs 40cr, Q3 at 61cr

FY27 guidance:

Rev of 5000-5500cr with OPM at 13-15% without considering any contribution from Merino Shelters

Orderbook at 3000cr executable in the next 6-12 months

5

19

309

34,596

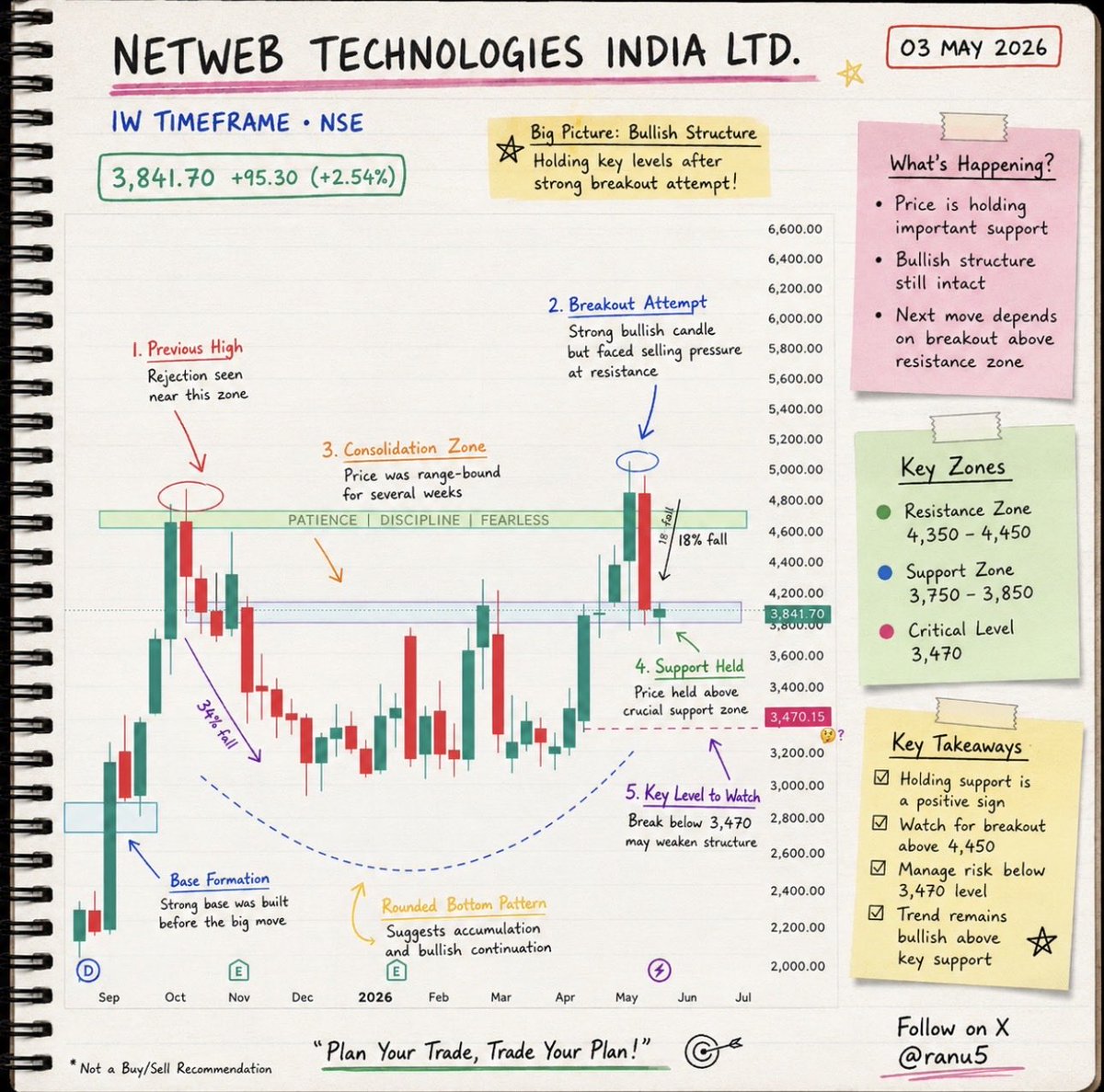

This week all posted chart requests with detailed analysis. Many ppl says they r not on instagram so posting here for them. 🤗

#netweb

#anuras

#jswcement

#bse

Like⚡️ retweet ⚡️ follow ⚡️ if you like my chart analysis 🤗

4

10

84

7,406

May 21

🚨 MAN Industries – Strategic Acquisition Update

MAN Industries (India) Ltd has completed the acquisition of 100% equity stake in National Pipe Company (NPC), Saudi Arabia for approximately USD 102 Million (~₹1,000 Crore).

Key Highlights:

✅ Profit-making & debt-free company

✅ Installed manufacturing capacity of 430,000 MT per annum

✅ Strong customer base including Saudi Aramco, SWA, L&T, Saipem, Subsea7 & global EPC players

✅ Strengthens MAN’s presence in Middle East & international markets

✅ Exposure to Oil & Gas, Water Transmission, Infrastructure & Desalination projects

✅ Additional coating facilities planned for future growth

Investment Perspective:

This acquisition aligns with MAN Industries’ long-term global expansion strategy and may improve revenue visibility, order inflows, and international market penetration. 📈🌍

#MANIND #StockMarket #Acquisition #MiddleEast #Infrastructure #Growth

1

11

952

May 20

Zindagi tere ta'aqub mien hum ne wo log bhi khoye hain jo saans k manind thy.

4

63

May 20

PRIORITY WATCHLIST STOCKS FOR NEXT FEW SESSIONS

#Manind

#Apollopipes

#Sbcl

#Kirlpneu

#Aequs

#Glenmark

#Onesource

SHARED A COMPLETE VIDEO ANALYSIS THROUGH MORNING DOSE VIDEO TO HAVE A COMPLETE UNDERSTANDING OF THE SETUPS.

#nifty #nifty50 #sensex #stockmarket #banknifty #StocksToWatch #giftnifty #StocksInFocus #stocks #watchlist #investment

1

10

1,953

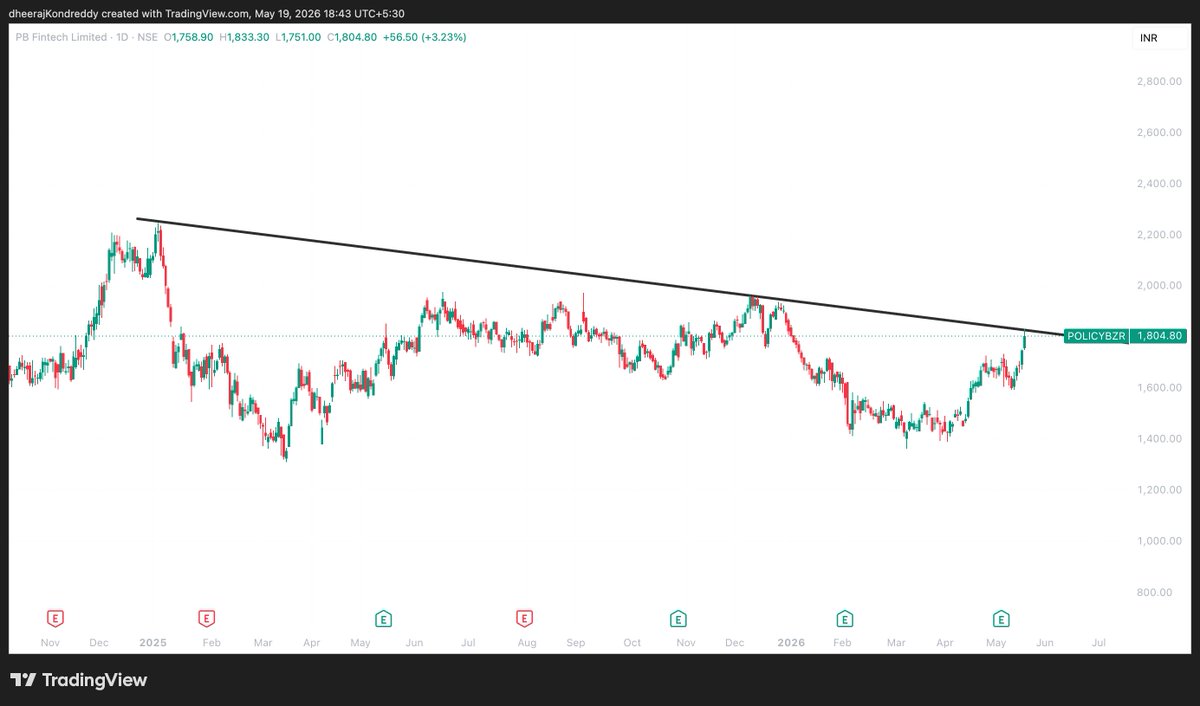

📈Breakout And Breakout Soon 𝐒𝐭𝐨𝐜𝐤𝐬 𝐨𝐟 𝐓𝐡𝐞 𝐃𝐚𝐲!📷

1.#GROWW

2.#LATENTVIEW

3.#MANIND(W)

4.#POLICYBZR

#StocksToWatch #BreakoutStocks #StocksToBuy

1

8

904

May 19

Glandpharma

Manind

Neta set up bura man jayega agar buy nai kiya

5

326

May 19

Top Priority stocks in my Radar👇

1⃣ #MANIND

2⃣ #CEMPRO

3⃣ #ADANIENSOL

4⃣ #OMNI

5⃣ #AEQUS

6⃣ #ONESOURCE

8

11

104

7,202