18h

Bitcoin's Sharpe Ratio Plunges to -20: A Classic Signal of Market Bottom and Accumulation Phase

On June 11, Bitcoin’s short-term Sharpe Ratio dramatically fell to -20, marking one of the most extreme readings since 2015. The Sharpe Ratio measures risk-adjusted returns — how much excess return an asset delivers per unit of volatility. A deeply negative value like this reflects sharp price declines accompanied by high volatility, often signaling maximum pain for holders and a potential capitulation point.

Historically, such extreme drops in Bitcoin’s Sharpe Ratio have consistently preceded major price bottoms. After similar readings in past cycles, the asset entered prolonged accumulation phases where smart money quietly builds positions while retail sentiment reaches its lowest. These moments have frequently marked the transition from bearish exhaustion to the early stages of a new bullish cycle.

For traders and long-term investors, this metric serves as a valuable contrarian indicator. While negative Sharpe Ratios highlight recent underperformance on a risk-adjusted basis, they also spotlight periods when fear dominates and prices may have already discounted most bad news. As Bitcoin approaches these extremes, market participants often shift focus from short-term noise to the broader narrative of adoption, institutional interest, and network fundamentals that continue strengthening beneath the surface.

The current reading reinforces a familiar pattern: deep drawdowns test conviction, flush out weak hands, and set the stage for the next leg higher. Whether this proves to be the definitive bottom remains to be seen, but history suggests that such Sharpe Ratio extremes have been reliable precursors to significant recovery and accumulation.

#decw

#BitcoinBottom #SharpeRatio #CryptoAccumulation #MarketCapitulation #BTCRecovery

---

15

AN INCREASING NUMBER OF LONG-TERM BITCOIN HOLDERS ARE FACING LOSSES.

THIS TREND IS OFTEN SEEN AS A SIGN OF MARKET CAPITULATION, WITH EVEN THE MOST COMMITTED INVESTORS RESPONDING TO THE CURRENT DOWNTURN.

#BITCOIN #CRYPTO #MARKETCAPITULATION #HODL #CRYPTONEWS

4

2

8

336

BITCOIN EXPERIENCES ONE OF ITS LARGEST CAPITULATION EVENTS IN HISTORY!

RANKS AMONG THE TOP 3-5 LOSS EVENTS EVER RECORDED!

RIVALS THE 2021 CRASH, PER CRYPTOQUANT!

#Bitcoin #CryptoCrash #MarketCapitulation #CryptoNews

4

8

318

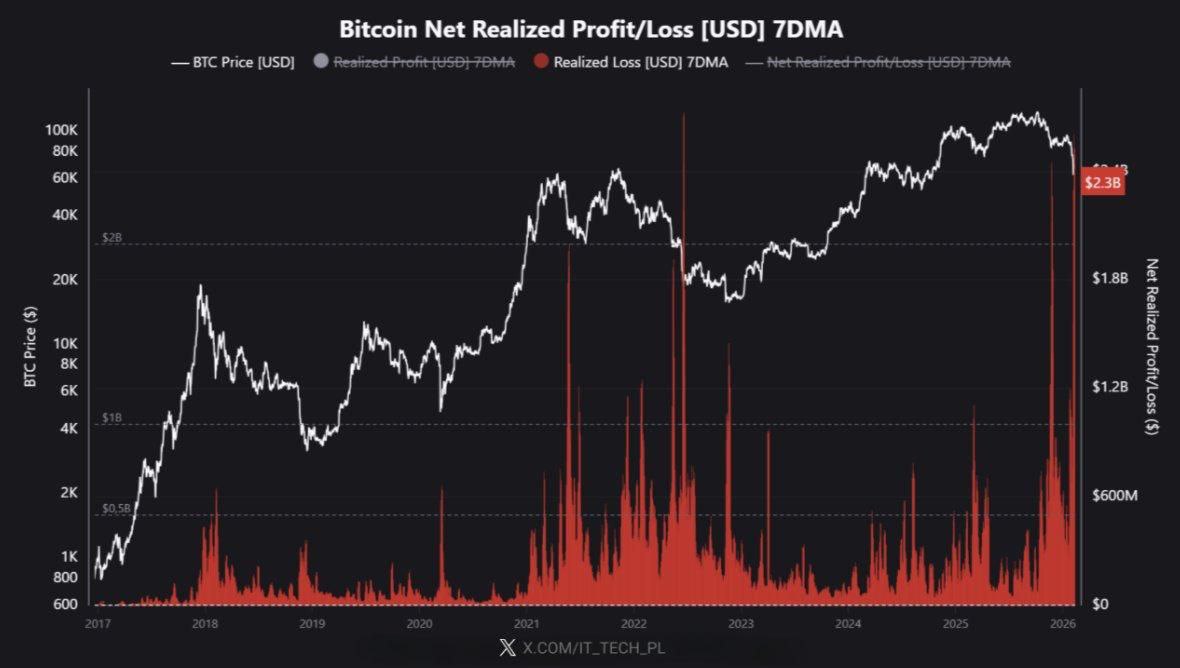

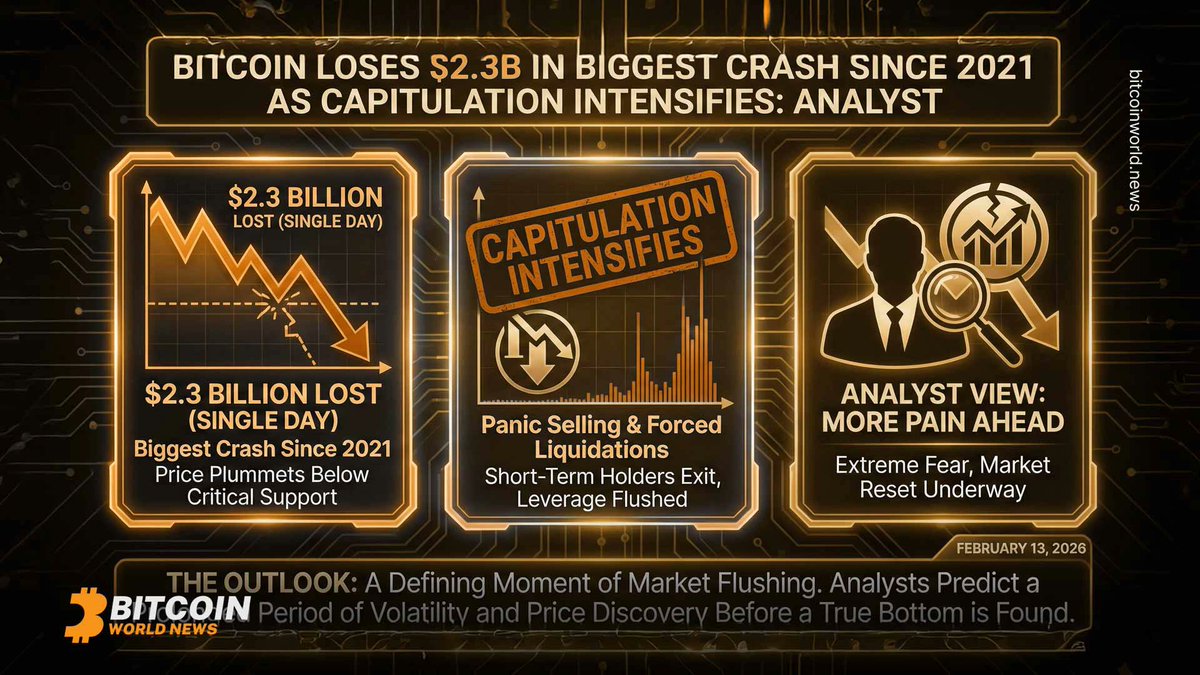

Feb 13

Bitcoin Loses $2.3B in Biggest Crash Since 2021 as Capitulation Intensifies: Analyst bitcoinworld.news/article/bi… via @BitcoinWorldN

#Bitcoin #BTC #CryptoCrash #MarketCapitulation

1

2

193

🐋 Bitcoin Whales Buy the Dip as Market Capitulates — 66,940 BTC Accumulated in One Day

Large holders sharply increased exposure to Bitcoin amid the ongoing market selloff. On February 6, on-chain data shows 66,940 BTC moved into accumulation addresses — the largest single-day inflow since 2022. The buying coincided with a brief rebound, as BTC jumped nearly 19% intraday from ~$60,000 to above $71,000, even while broader sentiment remained fragile. Institutional demand also resurfaced: U.S. spot Bitcoin ETFs recorded $371M in net inflows the same day, led by BlackRock’s iBIT. Analysts caution that indicators like the Sharpe ratio (near -10) suggest an extreme risk-reward zone, but not a confirmed bottom, as deleveraging and stablecoin off-ramps persist.

Full text of the news is available on our news portal cryptemic.com

🎓 Learn how on-chain flows, ETF demand, and risk metrics like the Sharpe ratio help assess market turning points — explore Cryptemic Academy.

#Bitcoin #BTC #Whales #ETFs #OnChain #MarketCapitulation #cryptemic #cryptemicacademy

1

2

24

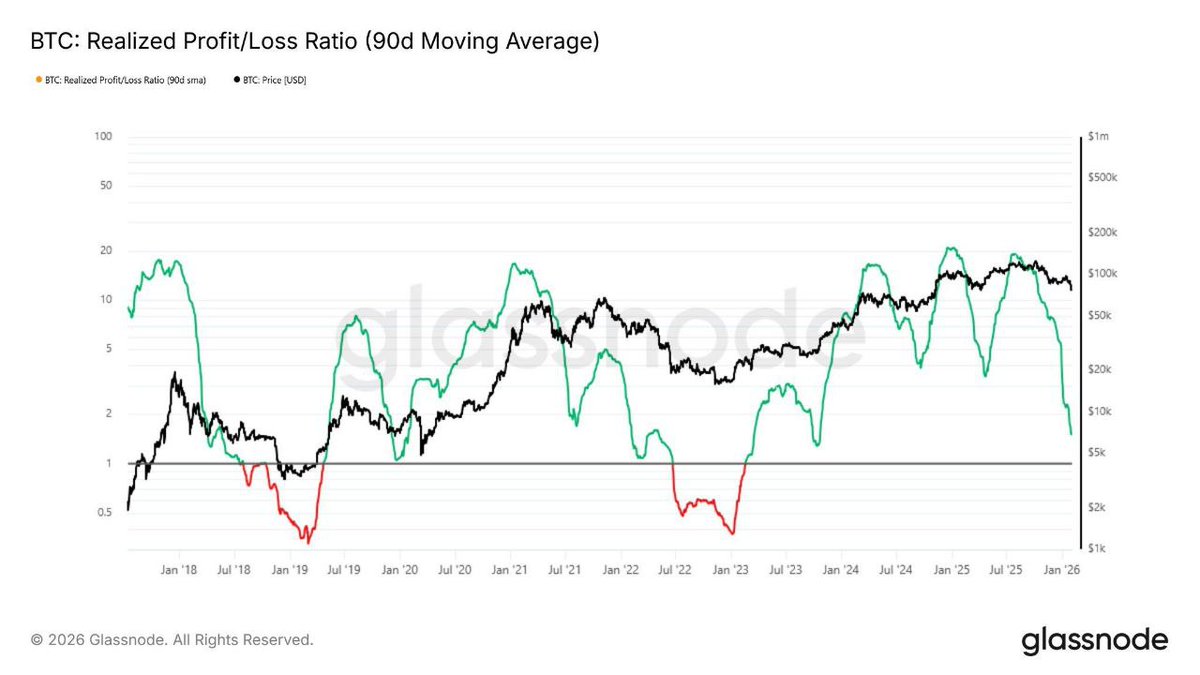

Feb 4

📢 Glassnode: نسبة الربح/الخسارة المُحققة لبيتكوين عم تقرّب من 1 ⚖️

وهالرقم غالباً بينحكى عنه كـ علامة “استسلام السوق” 😵💫📉

يعني يا إمّا قربنا من قاع… يا إمّا في ضغط أكتر جاي 👀🔥

#Bitcoin #BTC #Glassnode #Crypto #OnChain #Trading #MarketCapitulation #Investing 📊🚀

1

3

84

🔥 $2.5 Billion Liquidations Rock Crypto Markets

Leverage wipeout accelerates as ether leads brutal sell-off.

A single trader lost $220 million on ETH, pushing 24-hour liquidations past $2.5 billion. Hyperliquid and other perp platforms saw record volume as longs capitulated.

Deleveraging cycles like this historically mark intermediate bottoms.

Insight: Total crypto liquidations exceeded $2.5 billion in 24 hours—the highest since March 2025 (CoinDesk).

🔘 Funding rates deeply negative signal oversold conditions emerging.

🔘 Altcoins underperforming BTC—rotation back to majors likely.

🔘 Recovery pace depends on equity correlation and macro liquidity.

🔘 Forecast: Volatile bottoming process through February, new highs possible Q3.

#Liquidations #CryptoLeverage #EtherPlunge #MarketCapitulation #DeFiRisk

3

74

3 Nov 2025

Haha, Cyclops—FTX flashbacks hit hard in this $107K bloodbath, but that's the capitulation cue we've craved. Timeline's a fear factory, perfect for scooping BTC at these levels before Nov's 42% avg roars in. Target: $115K EOM rebound. Watching sentiment crater & RSI oversold flip. 🩸🚀 #MarketCapitulation #BuyTheFear #CryptoDip

1

1

497

20 Jul 2025

Bitcoin Miners' Capitulation: Why It's Happening Now!

#Bitcoin #BitcoinMining #Crypto #BTC #Cryptocurrency #BitcoinAnalysis #MarketCapitulation #CryptoNews #BitcoinETF #CryptoMarket

3

2

14

1,017

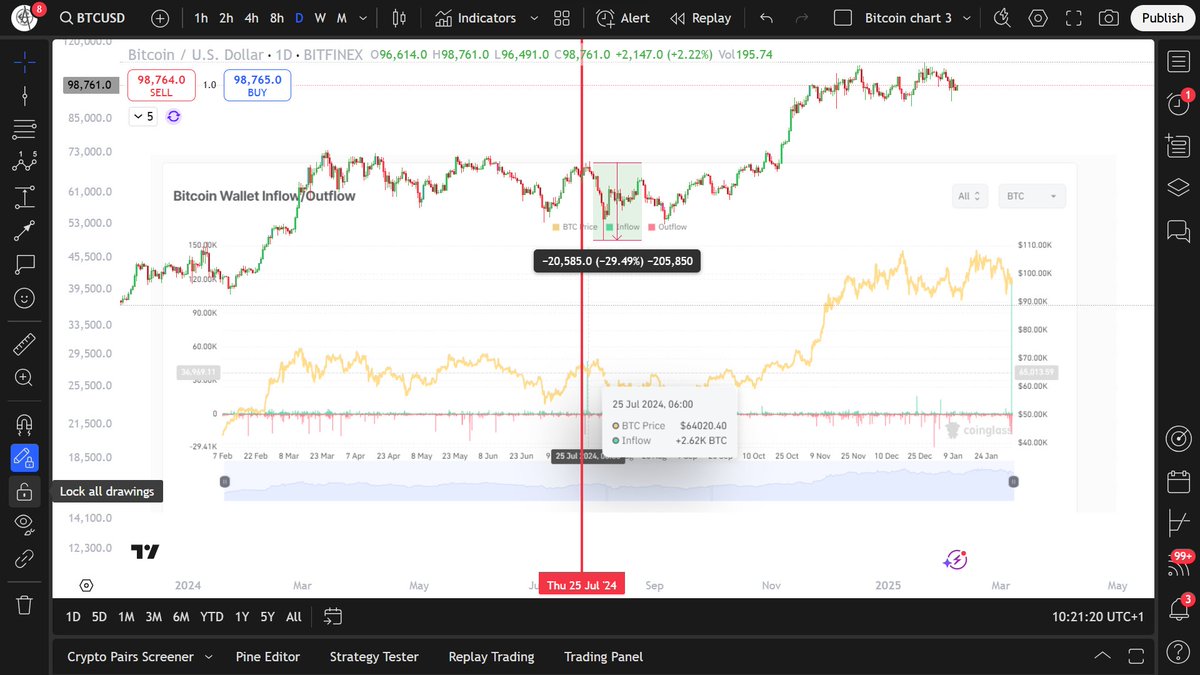

6 Feb 2025

🧵2/2 On July 25th, market makers and institutions executed the scenario mentioned in point 1 above. I’ve made a comparison with similar on-chain activities at that time and their impact on price if they repeat the same action. The dump triggered the completion of distribution, leading to the final capitulation before the trend continued. 📉

Which scenario they choose this time isn’t as important as staying informed and updated, just like you’ve been so far, on the key points to watch for. 🔍💡

#MarketUpdate #Bitcoin #InstitutionalActivity #MarketCapitulation #Distribution #BTCPriceAction #CryptoTrends #OnChainData #CryptoAnalysis #PriceImpact #TrendContinuation #CryptoInsights #StayInformed #BTC #MarketMovers 🚀📊

1

10

825

28 Oct 2024

Analyst’ Strategies as $44K Collapse Looms

news.nbtc.finance/analyst-st…

#CryptoAnalyst #MarketDownturn #InvestmentStrategy #MtGox #MarketCapitulation #Crypto #Bitcoin #NBTC

2

72

Market capitulation in crypto is not uncommon, and it can be a sign of a market correction. Be prepared for volatility and have a plan.

lcx.com/crypto-market-capitu…

#cryptotrading #marketcapitulation

1

18

1,773