$NetX is the only one about to be used in conjunction with Netstars with over 700k POS this will melt faces

33

$NETX @netx_world research content for those who want to read something interesting! You can read below the AI summary of the recent updates from Japan's LDP Financial Investigation Committee

@weajapan @NSS_StarPayX @kouhou_nss

**Executive Summary: LDP Financial Investigation Committee (金融調査会) Policy Recommendations (2026)**

These three PDFs are recent policy proposals/recommendations (April–May 2026, Reiwa 8) issued by the Liberal Democratic Party (LDP) of Japan’s Financial Investigation Committee and its subcommittees/project teams. They outline a forward-looking vision for Japan’s financial sector to support a “strong economy,” regional revitalization, corporate competitiveness, and global leadership in digital finance. The documents assign a central role to the **Financial Services Agency (FSA / 金融庁)** as a coordinator and “command tower” (司令塔), while emphasizing public-private collaboration.

### Core Themes Across the Documents

1. **Financial Sector as Growth Engine (“Strong Economy” Realization)**

Banks and financial institutions (including regional ones) should expand beyond traditional lending into investment banking services (capital markets, M&A advisory, business regeneration, equity-like financing based on business plans/future value). This supports growth investments in strategic sectors, AI, and regional economies.

2. **Regional Financial Power Enhancement (“地域金融力”)**

Strengthen regional banks’ capabilities in investment banking, create new “main bank” services tailored to local needs, and link them to national strategies like the “Strategic Industry Cluster Plan.” Regulatory easing (large exposure rules, investment company regulations, capital requirements) and support via REVIC or similar entities are proposed.

3. **Corporate Governance & Accounting Reforms**

Early revision of the Corporate Governance Code to prioritize substantive (not just formal) measures that promote mid-to-long-term corporate value and growth investments (R&D, human capital, intangibles, regional contributions). Other priorities include:

- Timely disclosure of securities reports before shareholder meetings (target: 3 weeks prior).

- Mandatory sustainability disclosures third-party assurance (starting with large prime-listed companies).

- Easing disclosure burdens for startups to facilitate growth funding.

- Strengthening audit firms/CPAs (especially smaller ones) through talent development, digitalization, networking, and quality support while avoiding overly punitive inspections.

- Robust responses to accounting fraud.

4. **World-Class Payment Architecture in the AI & On-Chain Era (Major Focus)**

This is the most forward-looking and detailed section. Japan must build a “world highest standard payment architecture” to avoid falling behind globally, maintain currency sovereignty, ensure stability/user protection, and capture benefits of programmability, 24/7/365 operations, and AI/agent-driven commerce (“エージェンティック・コマース”).

- **FSA as payment command tower** (with Bank of Japan and Ministry of Finance support); organizational expansion recommended.

- Expand FSA’s Payment Innovation Project (PIP) for on-chain experiments: 3-megabank stablecoin issuance, blockchain-based securities settlement, tokenized deposit transfers, trade finance use cases, etc.

- **7 Strategic Directions**: Competition user choice; interoperability/collaboration to avoid silos; maximize programmability & 24/365 benefits; maintain financial stability & intermediation; flexible regulation/tech response (including quantum risks); global usability & international signaling; cross-system interoperability.

- Institutional frameworks for stablecoins (reserve assets, lending rules, etc.), DeFi/wallet oversight, AI supervision in markets/institutions (herding risks, exclusion risks), and public fund disbursement use cases.

- Coordination with traditional systems (e.g., Zengin system upgrades by Japanese Bankers Association targeting ~2030).

**Overall Objective**:

Proactive modernization of Japan’s finance to drive economic growth and productivity in the digital/AI age, while safeguarding stability, trust, and sovereignty. The proposals are ambitious, implementation-oriented, and position FSA as a proactive leader in digital finance coordination rather than a pure regulator.

### Connection to NetX Network (netx.world / @netx_world)

**NetX Network** is a Web3 economic platform focused on a self-evolving, open economic infrastructure powered by **trusted computing** (TEE/ZKP), **AI modular protocols** (MCP), multi-chain architecture, and real-world asset (RWA) integration. Its core offerings include:

- **Nexus**: Unified infrastructure for AI and payments with verifiable execution.

- **AgentOS**: Environment for AI agents to operate, coordinate, and transact autonomously via smart contracts (“agentic” capabilities).

- **Payments**: Integration with dozens of payment systems and blockchains to advance commerce from Web2.0 to 3.0, enabling digital assets (including stablecoins) to circulate in the real economy.

- **NETX token**: Central value engine for protocol operations, asset settlement, incentives, and network security.

**Strong thematic and practical overlaps** with the LDP/FSA proposals exist, particularly in the payment innovation pillar:

- **Direct alignment on payment architecture goals**:

NetX emphasizes on-chain/stablecoin payments, programmability, 24/7 operations, trusted/verifiable execution, interoperability (multi-chain traditional rails), RWA/tokenization, and AI/agent-driven economic activity — precisely the areas highlighted in the “7 directions,” PIP expansions, stablecoin frameworks, and AI supervision discussions.

- **Japan-specific deployment and regulatory fit**:

NetX (via ecosystem partners like WEA Japan and Netstars) is actively building **trusted payment networks** that integrate **JPQR** (Japan’s dominant QR-code payment standard) with on-chain/stablecoin settlements. This bridges traditional Japanese payment rails to blockchain in a compliant manner. It is linked to **JPYC**, Japan’s first FSA-approved yen-backed stablecoin (issued under the Payment Services Act as a Type II Funds Transfer provider, 100% backed by JPY deposits and Japanese Government Bonds).

- **Compliance & risk mitigation focus**:

NetX’s heavy emphasis on **trusted computing** (verifiable, secure execution) and privacy-preserving solutions directly addresses FSA concerns around security, user protection, financial stability, currency sovereignty, and avoiding risks like herding or exclusion in AI-driven systems.

- **Strategic positioning**:

NetX describes Japan as a key entry point (“Asia’s most advanced compliance market”) for its global Web3 payment ambitions. This mirrors the LDP’s call for Japan to lead rather than lag in programmable/on-chain finance and to pursue public-private collaboration.

**Potential connections/synergies** (no evidence of direct LDP/FSA ownership, investment, or formal endorsement found):

- NetX and its partners (Netstars JPYC ecosystem) are **practical implementers** of the exact capabilities the LDP recommends FSA to champion and coordinate (on-chain experiments, regulated stablecoin use in real payments like JPQR, tokenization, AI integration).

- They could participate in or benefit from recommended mechanisms such as the proposed “官民戦略投資連携フォーラム,” expanded PIP on-chain pilots, regional fintech strengthening, or stablecoin institutional framework development.

- The policy environment created by these proposals (clearer stablecoin rules, FSA coordination role, push for 24/7 programmable infrastructure) provides a favorable runway for compliant players like NetX/JPYC/Netstars to scale in Japan.

In short, the LDP documents articulate a **policy vision and enabling framework** for Japan’s next-generation financial infrastructure. **NetX operates at the technological and commercial frontier** of that same vision, with concrete Japan deployments already underway via regulated stablecoins and traditional payment integration. There is significant strategic overlap and potential for constructive alignment as Japan advances its digital finance agenda.

These proposals are ambitious and timely; successful implementation will depend on FSA execution, legislative follow-through (e.g., company law amendments for disclosures), and effective public-private coordination. NetX appears well-positioned thematically and operationally to contribute to or capitalize on the resulting ecosystem developments.

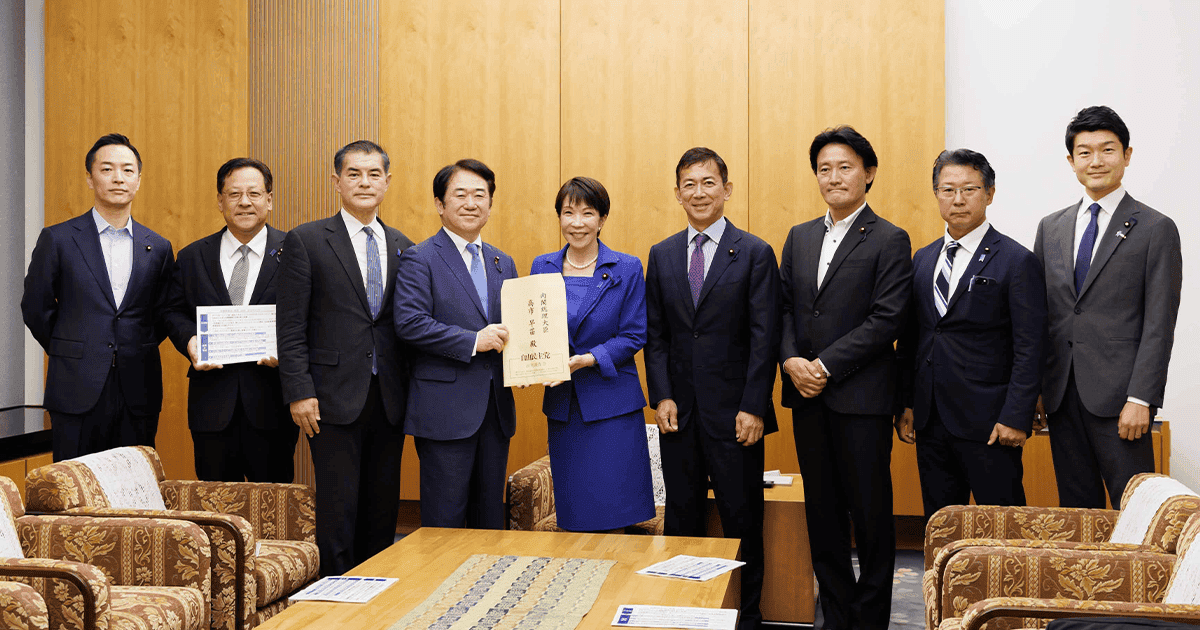

Jun 12

【提言】

党金融調査会(会長・伊藤達也衆議院議員)は「金融調査会 提言2026」を取りまとめ、6月12日に高市早苗内閣総理大臣に申し入れました。

高市政権の「強い経済」実現に向け、地域金融強化や金融セクターの信頼性確立を目指し、4つの方向性を打ち出しています。

まず、戦略17分野における更なる投融資促進のための「官民戦略投資連携フォーラム(高市フォーラム)」の創設など、資金供給機能の更なる強化を盛り込みました。

また、地域での投資銀行サービスの拡充や「地域未来金融アクションプラン」の策定により、地域金融力を抜本的に強化します。

さらに、企業の成長投資を促すコーポレートガバナンス改革や有報の総会前開示、相次ぐ会計不正への厳格な対応を明記しました。

加えて、金融庁を資金決済の司令塔に据え、AI・オンチェーンを活用した世界最高水準の決済アーキテクチャの構築を目指します。

📖提言はこちらから

・金融調査会提言2026

storage2.jimin.jp/pdf/news/p…

・企業会計に関する小委員会提言

storage2.jimin.jp/pdf/news/p…

・決済・イノベーション推進PT提言

storage2.jimin.jp/pdf/news/p…

jimin.jp/news/policy/213471.…

2

14

47

1,415

Jun 12

11 de junio, 2026. Resumen del Día netx:native

📢 MENSAJES DE LA ADMINISTRACIÓN

La administración ha ratificado que la fecha objetivo para el lanzamiento de la Mainnet sigue siendo el 25 de junio, desestimando rumores de retrasos prolongados. Se ha enfatizado que este hito representa el inicio de una nueva fase de crecimiento orgánico y expansión, comparando el proceso con el desarrollo histórico de gigantes tecnológicos que requirieron tiempo para consolidar su infraestructura tras salir al mercado.

En relación con la estrategia comercial, un administrador abordó de forma transparente la controversia sobre la venta de paquetes de activos (bundles). Se explicó que, aunque hubo debates internos sobre la oportunidad del momento para lanzarlos, el equipo central mantiene su derecho a ejecutar su hoja de ruta financiera para monetizar el producto. El liderazgo subrayó que la solidez del proyecto, respaldada por asociaciones de alto nivel como las de Netstars, no depende únicamente de estas ventas minoristas, sino de una visión institucional a largo plazo.

El equipo también destacó un avance regulatorio y técnico fundamental: la obtención de nuevas patentes en Japón a través de WEA Japan. Estas patentes actúan como una capa de validación tecnológica que fortalece la propuesta de valor de la red frente a reguladores y grandes comercios, posicionando a la infraestructura como una capa de confianza (trust layer) esencial para el ecosistema de pagos.

Finalmente, la administración lanzó una campaña de participación denominada "NetX Croc World Cup", diseñada para incentivar la creatividad de la comunidad mediante un concurso de slogans. Los ganadores podrán optar a premios de 20$ NETX y otras recompensas, buscando dinamizar la interacción en redes sociales mientras se aproxima el evento de lanzamiento principal.

🔥 TEMAS CANDENTES

Uno de los puntos de mayor fricción hoy ha sido el debate sobre la estética visual del proyecto. Algunos miembros de la comunidad expresaron su descontento con el uso de imágenes de cocodrilos generadas por inteligencia artificial, calificándolas de poco profesionales o propias de una "meme coin". No obstante, un Voluntario DAO y parte de la administración defendieron esta elección, explicando que el cocodrilo es un símbolo de los grandes actores del mercado y que el estilo de arte tipo cómic es sumamente popular y efectivo en el mercado japonés, uno de los focos estratégicos de la red.

La transparencia y la comunicación también generaron intercambios intensos. Algunos usuarios manifestaron sentirse ignorados respecto a la actividad de ciertos Embajadores DAO que han reducido su presencia en los canales públicos. Esto derivó en una discusión sobre si el potencial de revalorización del activo es una respuesta suficiente ante las dudas de los inversores. La administración respondió instando a la comunidad a centrarse en el potencial de revalorización masiva y a no dejarse llevar por el pesimismo de los precios mínimos en mercados volátiles.

Existe una notable incertidumbre sobre el alcance real del día de lanzamiento de la Mainnet. Mientras algunos esperan una explosión inmediata de volumen y actividad, otros miembros más cautelosos advierten que se tratará de un proceso gradual de pruebas de estrés, despliegue de nodos y adopción paso a paso. El debate sugiere que el éxito no se medirá solo por el lanzamiento técnico, sino por la capacidad de atraer usuarios reales a aplicaciones como StarPay-X en los meses subsiguientes.

📈 SENTIMIENTO Y MERCADO

El sentimiento actual es una mezcla de escepticismo y esperanza contenida. Existe una frustración palpable debido a la caída persistente del precio, que algunos usuarios ven como contradictoria ante la cercanía de la Mainnet. Se han identificado niveles de soporte críticos en los 0.30$ y 0.24$, con algunos inversores colocando órdenes de compra en esos rangos inferiores esperando una capitulación final antes de una posible recuperación.

El mercado global también ha influido en la narrativa del chat. Se discutió el impacto de la geopolítica internacional y las declaraciones de figuras políticas sobre posibles conflictos, lo que ha impulsado el precio del Oro y generado volatilidad en el Bitcoin. Algunos analistas de la comunidad sugieren que la liquidez está fluyendo temporalmente hacia activos tradicionales o hacia grandes eventos como la salida a bolsa de SpaceX, pero confían en que el capital regresará a las altcoins con fundamentos sólidos una vez que el ecosistema muestre utilidad real.

A pesar de la acción del precio actual, las proyecciones a largo plazo mencionadas por los participantes más optimistas siguen siendo ambiciosas, con menciones a objetivos de 3$, 5$ e incluso 10$ por unidad de NETX una vez que el capital institucional comience a absorber la oferta disponible, convirtiendo las ventas de los minoristas en un factor irrelevante para el gráfico global.

🛠️ NOVEDADES TÉCNICAS

En el plano tecnológico, se ha confirmado que la arquitectura de la red está siendo preparada para soportar múltiples pilotos de stablecoins, un nicho de mercado considerado de alto valor para la adopción masiva en Asia. El equipo central ha reiterado que la seguridad es la máxima prioridad, lo que justifica la implementación de fases de prueba rigurosas antes de abrir todas las funcionalidades al público general.

Sobre el sistema de staking y migración, se aclaró que la fase 2 de la migración de ecoactivos aún no tiene una fecha exacta de inicio, pero que se comunicará oportunamente. Los usuarios que adquirieron los primeros paquetes de activos recibirán una distribución única de recompensas, y se espera que el staking en la Mainnet sea el principal motor para reducir la oferta circulante y recompensar a los poseedores a largo plazo tras la activación del explorador de bloques.

5

382

Jun 12

🔥 @allscaleio × @circle — Một bước tiến lớn cho tương lai On-Chain Economy

Thật sự rất phấn khích khi thấy AllScale chính thức gia nhập Circle Alliance Program mạng lưới toàn cầu quy tụ những builders, innovators và institutions đang cùng nhau thúc đẩy việc đưa thế giới lên blockchain thông qua sức mạnh của USDC.

Circle không chỉ là đơn vị phát hành $USDC, stablecoin được tin dùng hàng đầu trong ngành, mà còn là một trong những tổ chức đang đóng vai trò quan trọng trong việc kết nối tài chính truyền thống với nền kinh tế on-chain.

Việc AllScale trở thành thành viên của Circle Alliance Program mở ra nhiều cơ hội để:

- Kết nối với các protocol và tổ chức hàng đầu trong hệ sinh thái Circle

- Khám phá các giải pháp thanh toán và settlement sử dụng USDC

- Thúc đẩy việc ứng dụng blockchain vào các hoạt động thương mại và tài chính thực tế

- Đóng góp vào việc xây dựng một nền kinh tế on-chain minh bạch, hiệu quả và có khả năng mở rộng toàn cầu

Đặc biệt, sau khi @allscaleio vừa ký kết MOU với NETSTARS đơn vị đứng sau chương trình thí điểm thanh toán $USDC tại cửa hàng đầu tiên ở Nhật Bản việc gia nhập Circle Alliance Program càng cho thấy định hướng rõ ràng của AllScale trong việc kết nối hạ tầng blockchain với các ứng dụng thực tiễn.

Những mảnh ghép đang dần hoàn thiện.

Từ hạ tầng thanh toán, stablecoin đến các giải pháp AI-powered commerce, AllScale đang từng bước xây dựng cầu nối đưa hàng triệu người dùng đến với nền kinh tế on-chain.

Keep building, Bullish @AllScale

#AllScale

Jun 12

Rất vui được chia sẻ rằng chúng tôi đã tham gia chương trình Alliance Program của @circle – một cộng đồng toàn cầu quy tụ các đội ngũ đang cùng nhau thúc đẩy việc đưa thế giới lên blockchain, với USDC là nền tảng cốt lõi!

Với vai trò là thành viên của chương trình, chúng tôi mong muốn được hợp tác cùng các giao thức (protocols) và tổ chức tiên phong để xây dựng các giải pháp sử dụng ethereum:0xa0b86991c6218b36c1d19d4a2e9eb0ce3606eb48 , góp phần thúc đẩy sự phát triển của nền kinh tế on-chain.

#AllScale

70

58

765

Jun 11

Yeah ridiculous, the teams even scams the Japanese technical patent bureau and got their names as the inventors on multiple patents.

They are also capable to scam Netstars with 700K POS. Man, they must be geniuses and you the great detective uncovered it all. You are screaming to the world and all those stupid CEO’s of Solana, Netstars, JYPC, Canton, Aptos, Bitget and the patent bureau and your 12 followers on X: they are scammers and I, I the big and real pokemonAsh know it. WAKE UP IDIOTS.

Keep up the good work, my dear Watson

1

270

Jun 11

Ahh you missed my post after this one - Here you:

x.com/PokemonAsh_real/status…

Team matters - and our $NETX scammer team is also capable to scam even big names like Kucoin.

If NETSTARS know it could endup in ashes after $NETX partnership?!

Jun 11

$NETX Community, this is your daily wake-up call!

Does anyone remember $MNW? Does anyone remember the "revolution" of supply chains in Asia? The big partnerships, the patents, and the promises of transforming global logistics forever?

Today, that coin is sitting at around a $600k market cap.

Patents and partnerships mean very little on their own. The real determinant of a project's success is its team, and we all know the team behind $NETX very well.

In my opinion, they are unprofessional, irresponsible, and have repeatedly damaged the community's trust.

Don't get your hopes up about getting rich with this project. $NETX is #scam

1

192

Jun 11

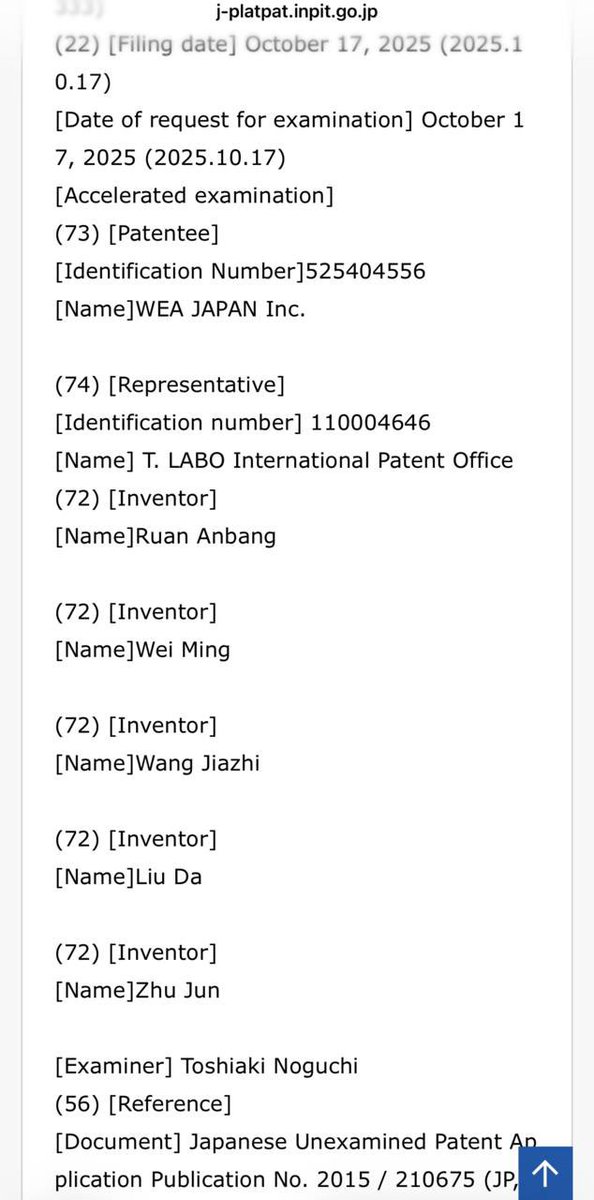

Great to see @WEAJapan securing two new Japanese patents for Trusted Exchange Rate Verification and Payment Refund Mechanism.

These are exactly the kind of practical, enterprise-grade innovations needed for real stablecoin adoption in Japan’s regulated environment.

This strengthens the entire payment infrastructure stack that WEA is building together with Netstars and Progmat, with $NETX as the underlying trusted execution and settlement layer.

Real progress isn’t always loud. These patents show the team is methodically building the solid foundation required for institutional-grade Web3 payments.

#NetX $NETX #WEA #Netstars #Progmat

🎉 Great news!

WEA JAPAN has been granted two Japanese patents focused on:

✅ Trusted Exchange Rate Verification Mechanism

✅ Payment Refund Mechanism

Patent details are now available on the WEA website:

weajapan.co.jp/patents

As stablecoin payments continue to expand into real-world commercial environments, the industry faces increasing demands for trusted exchange rate data, auditable transaction records, and efficient refund processing.

These patents not only represent technological innovation, but also mark an important step forward for WEA in advancing compliance standards, commercial execution standards, and Web3 payment service standards.

🚀Looking ahead, we will continue strengthening our core technologies and intellectual property portfolio, with further research and patent development focused on stablecoin payments, trusted data networks, and digital commerce infrastructure.

Together with industry partners, we remain committed to supporting the continued growth and adoption of stablecoin payments.

📖 For more details, read the full article:

medium.com/@WEAJapan/wea-sec…

#Stablecoin #Web3Payments #DigitalCommerce #WEA #NetX #StarpayX #Netstars

3

15

432

Jun 11

WEA @WEAJapan owns the patented business-logic layer (verifiable FX determination, compliant refunds).

NetX @netx_world supplies the trusted execution and blockchain network those mechanisms run on.

Netstars @Kouhou_NSS provides the merchant-facing distribution (QR terminals, acquiring, yen settlement).

The patents strengthen the whole stack's pitch to regulators and merchants, and by extension validate NetX's positioning as the trust layer underneath.

@netx_world @WEAJapan @Kouhou_NSS #WEAJapan #NETX #Netstars #StarPayX #StablecoinPayments #Web3Payments #USDC #PaymentInfrastructure #DigitalPayments #Patent #Fintech #Blockchain #TrustedComputing #RWA #JapanFintech #FSA #Web3Japan @NNGNetX @anbangr @web3_jp_infra

🎉 Great news!

WEA JAPAN has been granted two Japanese patents focused on:

✅ Trusted Exchange Rate Verification Mechanism

✅ Payment Refund Mechanism

Patent details are now available on the WEA website:

weajapan.co.jp/patents

As stablecoin payments continue to expand into real-world commercial environments, the industry faces increasing demands for trusted exchange rate data, auditable transaction records, and efficient refund processing.

These patents not only represent technological innovation, but also mark an important step forward for WEA in advancing compliance standards, commercial execution standards, and Web3 payment service standards.

🚀Looking ahead, we will continue strengthening our core technologies and intellectual property portfolio, with further research and patent development focused on stablecoin payments, trusted data networks, and digital commerce infrastructure.

Together with industry partners, we remain committed to supporting the continued growth and adoption of stablecoin payments.

📖 For more details, read the full article:

medium.com/@WEAJapan/wea-sec…

#Stablecoin #Web3Payments #DigitalCommerce #WEA #NetX #StarpayX #Netstars

3

16

45

866

🎉 Great news!

WEA JAPAN has been granted two Japanese patents focused on:

✅ Trusted Exchange Rate Verification Mechanism

✅ Payment Refund Mechanism

Patent details are now available on the WEA website:

weajapan.co.jp/patents

As stablecoin payments continue to expand into real-world commercial environments, the industry faces increasing demands for trusted exchange rate data, auditable transaction records, and efficient refund processing.

These patents not only represent technological innovation, but also mark an important step forward for WEA in advancing compliance standards, commercial execution standards, and Web3 payment service standards.

🚀Looking ahead, we will continue strengthening our core technologies and intellectual property portfolio, with further research and patent development focused on stablecoin payments, trusted data networks, and digital commerce infrastructure.

Together with industry partners, we remain committed to supporting the continued growth and adoption of stablecoin payments.

📖 For more details, read the full article:

medium.com/@WEAJapan/wea-sec…

#Stablecoin #Web3Payments #DigitalCommerce #WEA #NetX #StarpayX #Netstars

7

29

91

4,904

Hanafi1 🐟⛓️ retweeted

Jun 8

AllScale has signed an MOU with NETSTARS @Kouhou_NSS, the team behind Japan's first in-store ethereum:0xa0b86991c6218b36c1d19d4a2e9eb0ce3606eb48 payment pilot.

Together we'll explore how self-custodial, real-time infrastructure can bring stablecoin payments into Japanese retail and B2B.

The first move in a bigger play.

Jun 8

587

512

595

21,583

Jun 11

AllScale and NETSTARS together could help bridge traditional payments with stablecoin innovation.

20