Jun 9

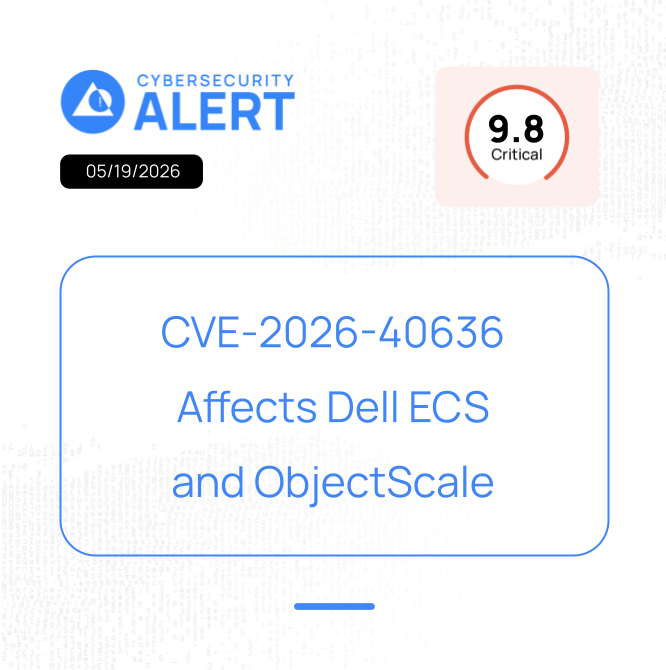

Progress Softwareは、Kemp LoadMasterに存在する2件の脆弱性を修正した。最も深刻なCVE-2026-8037は認証不要でリモートコード実行が可能となる問題で、管理者権限で任意のコマンドを実行される恐れがある。

CVE-2026-8037はLoadMasterのAPIに存在するOSコマンドインジェクションの脆弱性で、入力値の不適切な処理により、認証されていない攻撃者がLoadMasterアプライアンス上で任意のコマンドを実行できる。

また、CVE-2026-33691はWeb Application Firewall(WAF)に関連する脆弱性で、OWASP CRSがファイル名内の空白文字を正規化せずに拡張子チェックを行うことに起因する。細工したHTTP multipartリクエストを利用することで、ファイル検査を回避できる可能性がある。

Progressはこれらの問題を修正したバージョンv7.2.63.2およびv7.2.54.18を公開した。修正はProgress ECS Connection ManagerおよびProgress Connection Manager for ObjectScaleにも適用される。

securityonline.info/kemp-loa…

1,128

【Progress Kemp LoadMasterに未認証RCE脆弱性】

Progress Kemp LoadMasterに、CVE-2026-8037とCVE-2026-33691の2件の脆弱性が公表されました。CVE-2026-8037はAPIの入力検証不備に起因するOSコマンドインジェクションで、認証なしに任意のコマンドを実行できるとされています。

CVSSv3.1は9.6で、重要度はCriticalです。LoadMaster、LTSF、ECS Connection Manager、Connection Manager for ObjectScaleが影響を受けるとされ、依存関係に起因するWAF保護回避のおそれも示されています。

ADCやロードバランサは、社内外の重要サービスの前段に置かれることが多い製品です。日本の組織は、外部公開、管理画面制限、APIアクセスログ、パッチ適用状況を優先確認すべきです。

#Progress #LoadMaster #RCE #CVE #境界機器 #脆弱性管理

security-next.com/185448

2

2

362

May 30

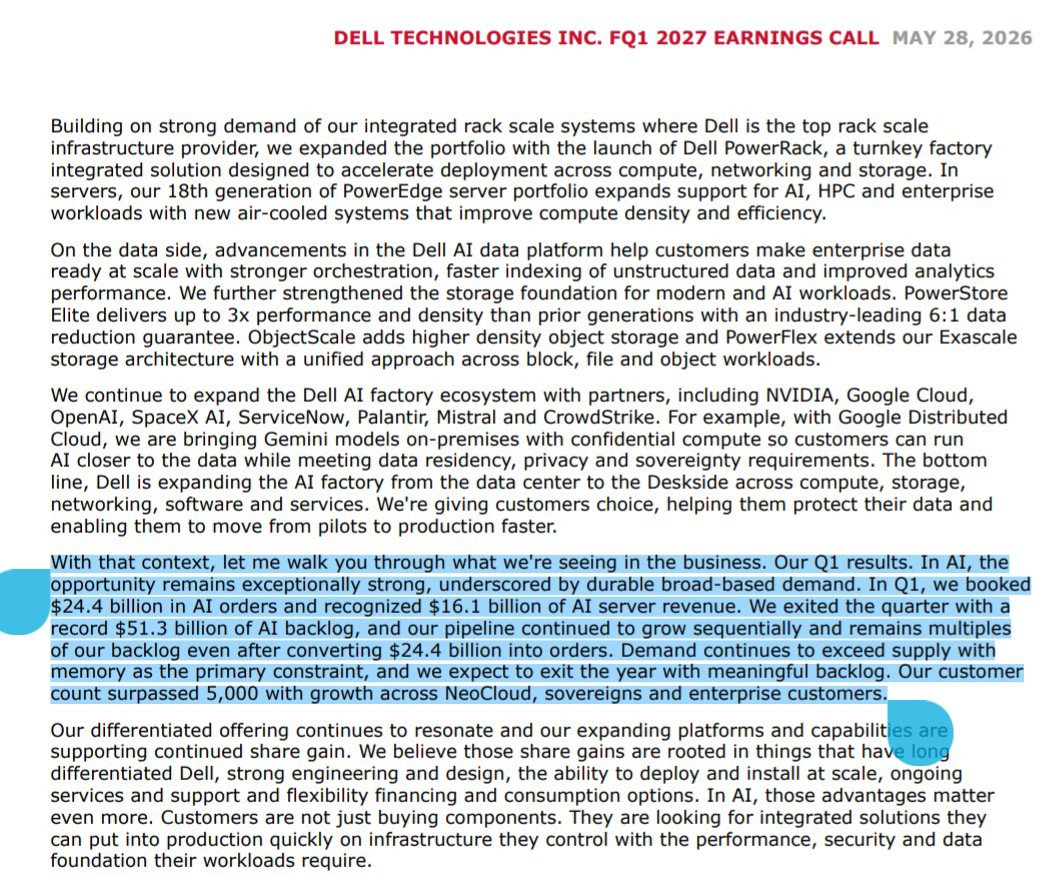

$DELL Q1 FY27: AI Infrastructure Flywheel Accelerating

🔹 Business Segments

• Infrastructure Solutions Group (ISG): $29B revenue ( 181% YoY)

- AI Servers: $16.1B revenue

- Traditional Servers: 92% YoY

- Storage: 8% YoY

• Client Solutions Group (CSG): $14.6B revenue ( 17% YoY)

- Commercial PCs: 18%

- Consumer PCs: 9%

🔹 Conference Call Takeaways

• AI orders reached $24.4B in Q1 alone

• AI backlog expanded to $51.3B

• AI customer count crossed 5,000

• Demand continues to exceed supply across AI servers, traditional servers, storage and PCs

• Memory (DRAM), NAND and CPUs remain the biggest constraints

• Traditional server demand remains exceptionally strong due to:

- Enterprise refresh cycle

- AI inference workloads

- Agentic AI driving incremental CPU demand

• Storage emerging as a major AI beneficiary:

- PowerStore, PowerScale and ObjectScale showing strong momentum

- Higher storage attach rates with AI deployments

• Management's key message:

"Demand is not the issue. Supply is."

🔹 Valuation View

Despite guiding for $170B revenue ( 50% YoY) and $18 EPS ( 75% YoY) in FY27, Dell trades at only 21x forward earnings at a $420 share price, implying a PEG ratio of 0.3x, which appears reasonable to attractive if current AI infrastructure demand remains durable.

The key question is no longer whether AI demand exists. The key question is how quickly Dell can secure enough components to satisfy demand.

Not a buy/sell rec.

4

10

1,497

Monster $DELL report.

But more than just strong report, it was a full-throated validation of the long-term AI infrastructure bull thesis.

Outstanding numbers across the board.

Revenues 88% year-over-year to $43.8 billion, EPS 214% to $4.86, and operating cash flow spiked to a Q1 record of $4.1 billion.

And, of course, it was all driven by AI. Dell booked $24.4 billion of AI orders in the quarter, recognized $16.1 billion of AI server revenue, and exited with a record $51.3 billion AI backlog. Management also raised its full-year AI server revenue outlook to $60 billion, implying roughly 2.4x year-over-year growth, while lifting total annual revenue guidance by about $27 billion and EPS guidance by roughly $5.

AI demand is accelerating. Dell said its AI pipeline remains multiples of backlog even after converting more than $24 billion into orders, and its AI customer count has now surpassed 5,000, up more than 50% in just six months, with demand broadening across NeoClouds, sovereign AI projects, enterprises, high-frequency traders, semiconductor companies, and major tech customers.

That matters because it directly attacks the bear case that AI infrastructure demand is narrow, concentrated, or fragile. Dell is showing that the AI buildout is becoming broader, deeper, and more institutionalized.

Even better, AI is now pulling through the rest of Dell’s business. Traditional Servers & Networking revenue jumped 92%, helped not only by refresh demand but also by AI inference and agentic AI workloads that require CPU-heavy infrastructure to manage memory, I/O, state, retries, and the operating "harness" around GPU calls.

We are seeing the AI Boom is expanding from a GPU story to a full-stack compute story across GPUs, CPUs, storage, networking, services, financing, and edge devices.

Storage was another important proof point.

Dell’s storage revenue rose 8%, with strength in higher-margin Dell IP products such as PowerStore, PowerScale, ObjectScale, and unstructured-data solutions. Management emphasized that unstructured data "feeds the beast" in AI, and as companies move from pilots to production, they need secure, scalable, high-performance storage architectures to prepare, govern, retrieve, and protect enterprise data. That gives Dell a critical second-layer AI opportunity beyond simply shipping servers.

The margin story also improved.

Bears have worried that Dell’s AI server growth is low-margin pass-through revenue, but ISG operating income rose 206% to a record $3.1 billion, with operating margin expanding to 10.5% even as AI servers grew nearly 800%. AI server margins remain mid-single-digit, but Dell is offsetting that with scale, pricing discipline, storage attach, services, and operating leverage.

This quarter strongly supports the long-term AI bull thesis.

Dell is increasingly becoming one of the core infrastructure integrators of the AI economy, and the company’s message was simple: supply is the problem, not demand. That is bullish for Dell, bullish for AI infrastructure, and bullish for the entire AI spending cycle.

1

5

569

May 29

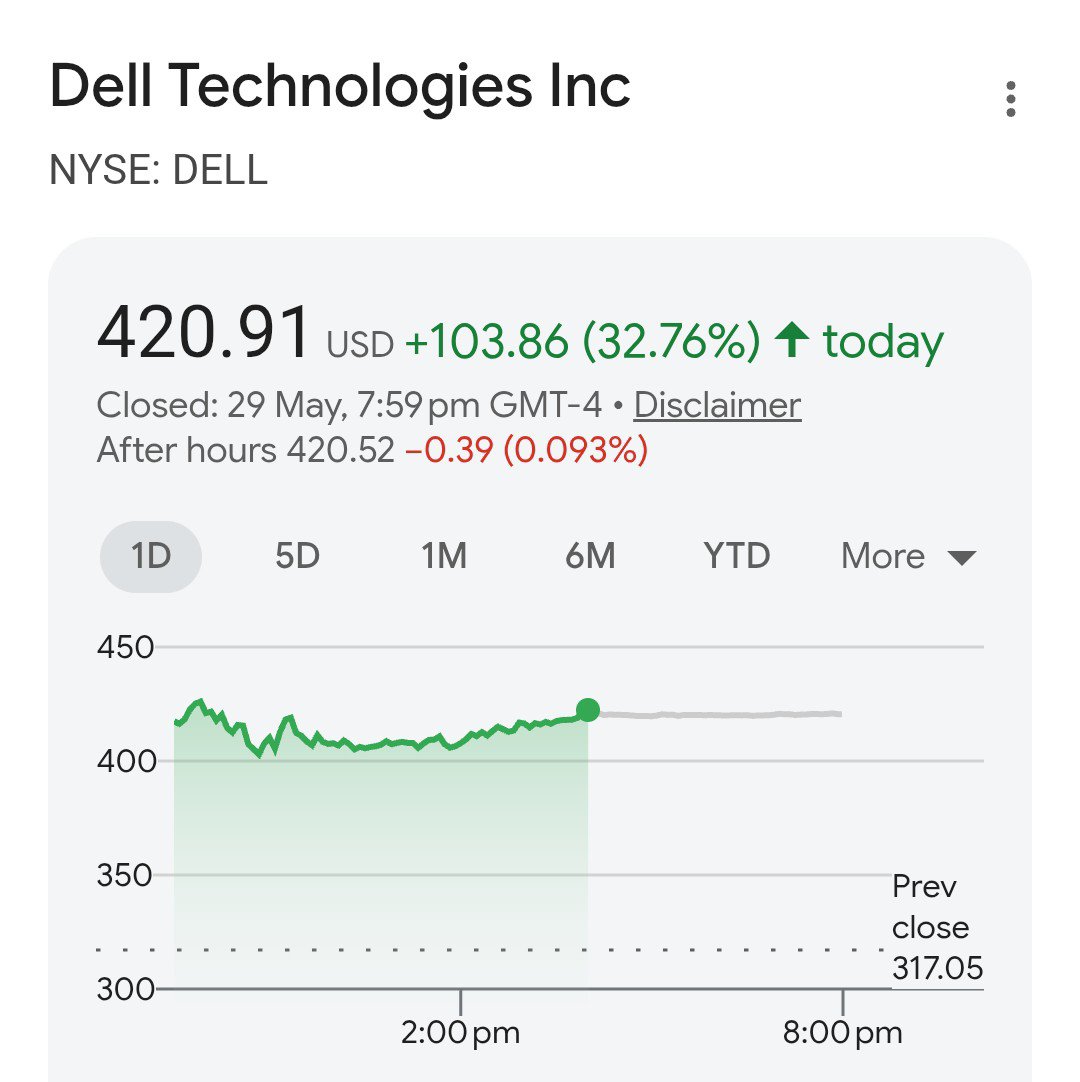

Dell盤後炸了!暴漲30%,這份財報到底有多恐怖?

你沒看錯,就是一夜暴漲30%。Dell在2026年5月28日盤後公布Q1財報,每一項數字都把華爾街的預期踩在腳下,消息出來股價瞬間爆拉,單週累計漲幅接近翻倍,創下2018年重新上市以來最猛的單季成長。

財報數字有多離譜?先看幾個關鍵數字感受一下衝擊:

營收438億美元,年增88%,分析師預估才361億,直接超出77億。EPS 4.80美元,分析師預估才2.99美元,超出整整六成。ISG(基礎設施)部門營收年增181%至290億,幾乎翻了快三倍。CSG(PC)部門營收年增17%至146億,同樣超越預期的129億。

AI伺服器:這才是今天的主角

本季AI伺服器營收暴增757%至161億美元,接單量244億,季末在手訂單513億美元,創歷史新高。客戶數突破5,000家,半年內成長超過五成,CoreWeave、Nscale這類neo cloud業者、各大企業與頂級AI公司都在搶單。

最關鍵的是COO Jeff Clarke在法說會上說的這句話:現在的問題不是需求不夠,是貨根本出不夠快。瓶頸從大到小依序是記憶體(DRAM/NAND)、微處理器、硬碟,前沿製程交期已排到一年後,稼動率持續滿載。

全年展望:直接上調270億

Dell把FY2027全年營收指引從約1,400億上調至1,670億美元,一口氣上調270億;AI伺服器全年目標更上調100億至600億美元,年增約2.4倍。Q2指引也給得很狠——440至450億美元,中位數比分析師預期高出整整25%,EPS指引同樣遠超市場。

一個被低估的趨勢:Agentic AI救了傳統伺服器

很多人沒注意到,傳統伺服器這季也幾乎翻倍——年增92%至85億美元。Clarke給出了一個很有意思的解釋:AI正在從「給建議」進化成「直接幫你做事」。當AI agent真的開始執行任務,每一個決策迴圈都需要CPU處理分支、重試、狀態管理這些高度序列性的工作——這直接把CPU的整體市場規模往上推,傳統伺服器需求跟著水漲船高。

儲存業務:悄悄的MVP

儲存營收年增8%,連續第五季跑贏大盤,看起來不起眼,但這才是ISG毛利的壓艙石。PowerStore連續第八季雙位數需求成長,PowerScale、ObjectScale連續三季成長。新品PowerStore Elite效能三倍、讀取快70%,Lightning平行檔案系統已通過Nvidia全堆疊認證。Dell自有IP儲存佔比持續提升,毛利率遠高於AI伺服器硬體組裝,是整體獲利品質的關鍵。

PC與一張意外的大合約

PC業務CSG營業利益率8%,在PC產業算是相當罕見的高水準,靠的是高階機種組合與周邊服務的附帶銷售。不過Clarke也承認本季提價太早,壓到了消費者與中小企業需求,Q2 CSG利潤率指引調降至約6%。

另一個亮點:美國軍方這週宣布給了Dell一張97億美元大單,協助管理Microsoft軟體授權。Evercore ISI分析師Amit Daryanani指出,這筆交易讓Dell的成長故事不再只靠AI單腿跳。

最後一句話總結

OpEx佔營收比降至8.4%,是二十年來最低。Clarke在電話會議結語說:需求沒有放緩,是在加速,而且遠遠超過供給。

Dell從一家被嫌棄的傳統電腦廠,用兩年時間變成AI基礎建設最核心的戰略供應商——這份財報,只是一個新起點。

$DELL #AI伺服器 #科技股 #財報季 #人工智能

2

9

673

May 28

恐怖 Dell Q1財報業績全面超越市場預期,盤後股價一度飆漲約40%,一週漲了快一倍

$Dell 本季營收年增 88% 至 438 億美元,遠高於分析師平均預估的 355 億美元;EPS 4.86 美元,同樣大幅優於市場預估的 2.99 美元。Dell 伺服器業務今年被視為 AI 受惠者,帶動股價在本財報發布前已較年初上漲超過 150%。

真正點燃市場情緒的是大幅上調的全年展望。Dell 將 2027 財年(至 2027 年 1 月)營收指引上修至約 1670 億美元,其中 600 億美元來自 AI 伺服器銷售,遠高於先前約 1400 億美元的指引,也輕鬆超越分析師平均預估的 1421 億美元。全年營收與 EPS 指引分別上調約 270 億美元與 5 美元。

#AI伺服器:本季電話會議的核心

AI 伺服器需求是本季最受關注的焦點。本季接單 244 億美元,認列 161 億美元 AI 伺服器營收,季末在手訂單達 513 億美元的歷史新高。Clarke 直言 AI 的機會沒有任何放緩跡象。

客戶結構涵蓋 CoreWeave、Nscale 等 neo cloud 租賃運算業者、企業客戶與主要 AI 供應商,客戶數突破 5000 家,過去六個月成長超過五成。管理層將全年 AI 伺服器營收指引上調 100 億美元至 600 億美元,年增約 2.4 倍。

電話會議上反覆出現的關鍵訊息是:限制因素在供給而非需求。Clarke 明確指出產能本身沒有問題,瓶頸完全來自零組件供給,其中記憶體(DRAM 與 NAND)是首要限制,其次是微處理器,再來是硬碟,半導體成熟製程的稼動率也正快速填滿、前沿製程已完全分配且交期長達一年。未來五季的銷售管線是在手訂單的數倍且持續成長,公司預期將帶著大量在手訂單進入下一財年。

#行業觀察:Agentic AI 重塑運算需求

本季最值得注意的行業轉折,是 AI 應用從訓練轉向推論與 agentic 部署,正在為傳統運算創造全新需求。傳統伺服器營收年增 92%,該部門營收近乎倍增至 85 億美元。

Clarke 對此提出了完整的產業論述:agentic AI 代表 AI 從顧問角色轉為操作者角色,當 agent 實際執行任務時,需要 CPU 處理 I/O、分支重試與狀態管理等高度序列性的工作,形成所謂的 harness。CPU 在 agent 的每一個決策迴圈中都不可或缺,這直接推升了 CPU 的 TAM,也帶動 neo cloud、半導體公司與大型科技公司以高密度伺服器承接推論工作負載。

#儲存:AI 時代的資料底層

儲存營收年增 8%,由 Dell 自有 IP 產品的持續超越市場表現驅動,本季為連續第五季需求成長高於市場。Clarke 將儲存定位為 AI 時代的核心,資料是餵養 AI 的養分,非結構化產品組合本季創下歷來最佳需求表現,PowerScale 與 ObjectScale 連續三季成長,PowerStore 達成連續第八季雙位數需求成長。

新推出的 PowerStore Elite 較前一代提供三倍效能、150 萬 IOPS、6 比 1 資料縮減,讀取速度快 70%;專為 AI 設計的 Lightning 平行檔案系統已通過 Nvidia 全堆疊認證。Dell IP 儲存在整體儲存組合中占比持續提升,憑藉較高的利潤率,成為本季 ISG 整體獲利的關鍵驅動力。管理層也預告下半年儲存指引上調,預期 Dell IP 與第三方產品的組合交叉將在年底完成,屆時將成為更穩定的成長與獲利來源。

#PC與業務多元化

PC 業務(CSG)營收年增 17% 至 146 億美元,由商用客戶銷售帶動,超越分析師預估的 129 億美元。CSG 營業利益率達 8%,創 PC 產業少見的高水準,主要來自規模帶動的營運槓桿、高價位機種組合與周邊服務附帶銷售。

不過 Clarke 坦言本季提價執行得稍早,壓抑了部分消費與中小企業的交易型需求,因此第二季 CSG 營業利益率指引調降至約 6%,在需求、市占與獲利間尋求平衡。

業務多元化也是本季亮點。本週稍早美國軍方宣布授予 Dell 一紙 97 億美元合約,協助管理 Microsoft 軟體授權。Evercore ISI 分析師 Amit Daryanani 指出,這筆交易為 Dell 帶來 AI 與企業業務之外的成長多元性。

#展望與審慎基調

展望Q2,營收指引 440 至 450 億美元,中位數年增約 50%;其中 ISG 年增約 75%,含 155 億美元 AI 伺服器營收。在毛利方面,本季毛利率 18.1%,主因 AI 伺服器組合提升;管理層強調若排除 AI 組合影響,毛利率展望較九十天前更佳,並預期全年持續擴張。OpEx 占營收比降至 8.4%,為二十多年來最低。

在記憶體價格快速上漲的通膨環境下,Dell 一方面維持定價與利潤紀律,一方面透過 DFS 融資業務協助客戶在預算限制下提前導入設備,各業務融資承作量呈雙位數成長。Clarke 在結語中強調,銷售pipeline顯示需求並未放緩而是在加速,並持續顯著超過供給

20

9

162

10,091

May 28

$DELL KEY READ-THROUGHS FROM DELL TECHNOLOGIES Q1 FY2027 EARNINGS CALL

Dell’s Q1 FY2027 earnings call was a broad cross-market confirmation that AI infrastructure demand is no longer limited to GPU procurement, but is now pulling through the full enterprise infrastructure stack: accelerators, CPUs, DRAM, NAND, HDDs, storage systems, power/cooling, rack integration, commercial PCs, services, and financing. The most important market signal was that Dell’s demand exceeded supply simultaneously across AI servers, traditional servers, storage, and PCs, while management raised FY27 revenue guidance by $27B and EPS guidance by $5 only 90 days into the fiscal year. Q1 AI server revenue of $16.1B, AI orders of $24.4B, ending AI backlog of $51.3B, and AI customer count above 5,000 imply that enterprise, sovereign, and Neocloud AI adoption has moved beyond pilot-stage experimentation into production-scale infrastructure procurement. The highest-conviction read-throughs are positive for NVIDIA, memory suppliers, server CPU vendors, HDD/storage media vendors, and data center power/cooling suppliers; negative or competitively adverse read-throughs apply to AI server OEMs without Dell-scale supply-chain access, standalone storage vendors competing against Dell IP attach, and selected discretionary IT spending categories exposed to budget reallocation toward infrastructure. Source material: Dell Technologies Q1 FY2027 Earnings Call transcript.

AI ACCELERATORS AND RACK-SCALE SYSTEMS (READ-THROUGH 1)

Affected Company Name (TICKER: Country): NVIDIA (NVDA: US). Directional impact and magnitude: Positive, high magnitude.

Call evidence: Dell reported $24.4B of AI orders, $16.1B of AI server revenue, $51.3B of ending AI backlog, more than 5,000 AI customers, and an FY27 AI server revenue guide of $60B, up $10B from prior guidance. Management emphasized that “demand continues to exceed supply” and that the AI pipeline over the next 5 quarters is multiple times backlog. Dell also explicitly centered its AI factory roadmap around NVIDIA, including Vera Rubin, Rubin GPU architecture, RTX GPUs, GB10, GB300, and NVIDIA-certified storage/data architectures.

Transmission mechanism: Dell’s AI server growth translates directly into demand for NVIDIA accelerators, rack-scale platforms, networking, software ecosystem attachment, and next-generation GPU transitions. The call materially increases confidence that NVIDIA’s demand is not purely hyperscaler-led, because Dell described broad growth across Neoclouds, sovereign customers, and enterprises. The expansion of AI customers by more than 50% in 6 months is especially important because it reduces perceived customer-concentration risk in AI infrastructure demand. Dell’s statement that manufacturing capacity is not the bottleneck and that “parts supply” is the constraint supports continued tightness for NVIDIA GPU allocation and rack-scale platforms.

Near-term trading catalyst: Positive estimate-revision pressure for NVIDIA data center revenue and backlog durability, particularly around Blackwell/GB200/GB300 and Rubin/Vera transition confidence. Dell’s $10B upward revision to AI server revenue guidance is a direct demand data point that should support near-term upside bias in AI accelerator sentiment.

Longer-duration fundamental shift: Enterprise and sovereign AI infrastructure is moving toward integrated AI factories rather than discrete server procurement. This favors NVIDIA because Dell’s portfolio is tightly integrated with NVIDIA’s full-stack roadmap, not simply with commoditized GPU resale. The call is less supportive for Advanced Micro Devices (AMD: US) as an AI accelerator competitor, because Dell’s AI server discussion was overwhelmingly NVIDIA-centric; however, AMD remains positively exposed through server CPU demand discussed separately below.

AI SERVER OEMS AND SYSTEM INTEGRATORS (READ-THROUGH 2)

Affected Company Name (TICKER: Country): Super Micro Computer (SMCI: US), Hewlett Packard Enterprise (HPE: US), Lenovo Group (0992: Hong Kong). Directional impact and magnitude: Negative, medium-to-high magnitude for Super Micro; negative, medium magnitude for HPE and Lenovo.

Call evidence: Dell said it is the top infrastructure provider for integrated rack-scale systems, is taking share across PC, traditional server, storage, and AI server businesses, and is benefiting when customers seek a “calming hand” during supply disruption. Management highlighted Dell’s engineering, at-scale deployment, ongoing services, support, financing, and consumption options as differentiated advantages. AI server demand was described as broad-based across Neocloud, sovereign, and enterprise customers, with backlog and pipeline still expanding despite $16.1B of AI server revenue recognition in Q1.

Transmission mechanism: The AI server market is institutionalizing. The early AI server cycle rewarded speed, configuration flexibility, and GPU access, which helped Super Micro and other specialist integrators. Dell’s call suggests the next phase increasingly rewards full-stack integration, global deployment capability, services, financing, and large-account procurement credibility. That transition favors Dell and pressures server OEMs that lack comparable financing, supply-chain leverage, or enterprise support infrastructure. The negative read-through is relative-share based rather than absolute-demand based: the market is growing, but Dell appears to be capturing an expanding share of the highest-value enterprise and sovereign deployments.

Near-term trading catalyst: Dell’s AI server backlog, orders, and guide raise could pressure investor assumptions that AI server upside will be distributed evenly across OEMs. Super Micro is most exposed to adverse relative-share interpretation because its valuation and earnings narrative are most directly tied to AI server momentum.

Longer-duration fundamental shift: AI infrastructure procurement is moving from component assembly toward factory-integrated rack-scale systems with storage, networking, deployment, support, and financing bundled into the sale. That structurally reduces the durability of pure hardware-integration differentiation.

MEMORY AND NAND SEMICONDUCTORS (READ-THROUGH 3)

Affected Company Name (TICKER: Country): Micron Technology (MU: US), SK Hynix (000660: Korea), Samsung Electronics (005930: Korea), SanDisk (SNDK: US). Directional impact and magnitude: Positive, high magnitude for DRAM; positive, medium-to-high magnitude for NAND.

Call evidence: Dell identified memory as the primary AI supply constraint, repeatedly cited DRAM and NAND as constrained commodities, and stated that traditional server configurations now include more cores, more DRAM, and more NAND per server. Management also said pricing is being updated almost continuously across DRAM, NAND, CPUs, raw materials, and related inputs. Q1 AI server revenue was up nearly 9x y/y, and traditional server revenue rose 92%, creating simultaneous pressure on high-bandwidth memory, server DRAM, enterprise SSD, and NAND supply chains.

Transmission mechanism: Dell’s demand profile increases both unit demand and content-per-system demand. AI servers require high-bandwidth memory and large memory footprints, while traditional servers are also incorporating more DRAM and NAND as customers modernize fleets and support inference and agentic workloads. The combination of high demand, supply constraints, higher server content, and repeated price increases supports a favorable pricing environment for memory suppliers. The read-through is especially powerful because Dell’s constraints are not limited to GPU-attached AI systems; traditional servers and PCs are also contributing to memory tightness.

Near-term trading catalyst: Positive for memory pricing expectations, gross margin revisions, and investor confidence that the DRAM/NAND cycle remains supply-constrained rather than merely recovering from inventory normalization. The call should support positive sentiment into Micron, SK Hynix, Samsung, and SanDisk earnings.

Longer-duration fundamental shift: AI is structurally raising memory intensity across the data center, not only in GPU systems. Agentic AI and enterprise inference appear to be increasing CPU server content, which should extend the memory cycle beyond the most obvious HBM beneficiaries.

SERVER CPUS AND X86 DATA CENTER SILICON (READ-THROUGH 4)

Affected Company Name (TICKER: Country): Advanced Micro Devices (AMD: US), Intel (INTC: US). Directional impact and magnitude: Positive, high magnitude for data center CPUs.

Call evidence: Dell reported traditional server and networking revenue of $8.5B, up 92% y/y, and guided traditional servers to grow just over 60% for FY27. Management said traditional server demand included absolute unit growth, more cores per server, more DRAM and NAND per system, and incremental AI inference workloads. The most important strategic statement was that AI is creating a new marketplace for traditional servers, because agentic AI requires CPU-side orchestration, I/O, branching, retry handling, memory management, and state management around GPU calls.

Transmission mechanism: The call materially upgrades the CPU demand narrative. The dominant AI trade has focused on GPUs, but Dell’s commentary suggests that every agentic workflow increases demand for CPU infrastructure to coordinate, supervise, and execute tasks around model inference. This benefits AMD EPYC and Intel Xeon franchises through higher server units, richer configurations, and improved pricing in a constrained supply environment. The call also supports the view that enterprise inference and AI workflow automation will not be served by GPUs alone.

Near-term trading catalyst: Positive for AMD and Intel data center revenue sentiment, especially where consensus expectations still assume traditional servers are mainly a cyclical refresh rather than a structural AI-adjacent growth market. Dell’s 60% FY27 traditional server growth guide is a direct upside datapoint for CPU suppliers.

Longer-duration fundamental shift: Agentic AI may expand the CPU TAM by making CPUs part of the critical AI execution loop. This is a stronger and more durable thesis than a simple replacement-cycle rebound, because it ties CPU demand to AI workflow penetration across enterprises.

ARM-BASED AI RACK ARCHITECTURES (READ-THROUGH 5)

Affected Company Name (TICKER: Country): Arm Holdings (ARM: US), NVIDIA (NVDA: US), Advanced Micro Devices (AMD: US), Intel (INTC: US). Directional impact and magnitude: Positive, medium magnitude for Arm and NVIDIA; negative, medium long-duration share risk for Intel and AMD in the largest liquid-cooled AI rack-scale systems.

Call evidence: Dell stated that traditional servers are x86 today, but that large GPU-side deployments such as GB200, GB300, and future Vera systems are biased toward ARM, especially in direct-liquid-cooled large deployments. By contrast, enterprise air-cooled systems such as B200, B300, and RTX 6000 Pro were described as x86-oriented.

Transmission mechanism: The market is bifurcating. Enterprise AI inference and traditional compute refresh remain favorable for x86 CPUs, but the largest integrated GPU rack-scale architectures increasingly attach to NVIDIA’s ARM-based Grace/Vera CPU roadmap. This supports Arm royalty growth and deepens NVIDIA’s system-level control over the AI rack. For Intel and AMD, the near-term read-through remains positive because traditional server demand is extremely strong; however, the longer-duration risk is that the highest-growth, highest-dollar AI rack-scale systems incorporate more ARM CPU content over time.

Near-term trading catalyst: Limited immediate negative impact for x86 suppliers because Dell’s traditional server revenue and guide are exceptionally strong. The more immediate positive trading read-through applies to ARM and NVIDIA’s broader system roadmap.

Longer-duration fundamental shift: AI rack architectures may increasingly be defined at the system level by the GPU vendor, including CPU selection, memory architecture, networking, and thermal design. That would structurally reduce the independent CPU attach opportunity in the largest AI clusters.

HDD, ENTERPRISE SSD, AND STORAGE MEDIA (READ-THROUGH 6)

Affected Company Name (TICKER: Country): Seagate Technology (STX: US), Western Digital (WDC: US), SanDisk (SNDK: US), Micron Technology (MU: US), Samsung Electronics (005930: Korea), SK Hynix (000660: Korea). Directional impact and magnitude: Positive, high magnitude for nearline HDD; positive, medium-to-high magnitude for enterprise SSD/NAND.

Call evidence: Dell identified hard drives as the next likely supply constraint after DRAM, NAND, and CPUs. Management also said unstructured storage had its best demand quarter ever and emphasized that unstructured data feeds AI workloads. Storage revenue rose 8%, Dell IP storage demand grew above market for the 5th consecutive quarter, and PowerScale/ObjectScale momentum was linked directly to AI data requirements.

Transmission mechanism: AI creates a dual storage demand curve. Training and inference pipelines require high-performance storage and SSDs for data ingest, retrieval, and workflow execution, while large-scale unstructured data growth supports high-capacity nearline HDD demand. Dell’s comments indicate that AI is not simply compute-intensive; it is also data-retention, data-management, and auditability intensive. That benefits HDD suppliers through capacity growth and pricing tightness, while also benefiting NAND suppliers through enterprise SSD demand.

Near-term trading catalyst: Positive for HDD pricing, enterprise drive demand, and gross margin expectations at Seagate and Western Digital. Dell’s explicit identification of hard drives as an emerging constraint is particularly relevant because HDD tightness has historically produced strong incremental margin for the consolidated HDD supplier base.

Longer-duration fundamental shift: Agentic AI requires persistent storage of inputs, outputs, decisions, retrieval context, and audit trails. This should extend AI infrastructure spend into storage media over multiple years rather than confining value capture to accelerators.

ENTERPRISE STORAGE SYSTEMS AND AI STORAGE ATTACH (READ-THROUGH 7)

Affected Company Name (TICKER: Country): NetApp (NTAP: US), Pure Storage (PSTG: US), Hewlett Packard Enterprise (HPE: US), IBM (IBM: US). Directional impact and magnitude: Negative, medium magnitude on relative share and multiple; positive, medium magnitude for the overall storage TAM.

Call evidence: Dell said Dell IP storage delivered a record demand growth quarter, its 5th consecutive quarter of demand growth above market. PowerStore posted its 8th consecutive quarter of double-digit demand growth, and PowerScale/ObjectScale had 3 consecutive quarters of growth, including double-digit growth in each of the last 2 quarters. Management said Dell is selling more storage, more Dell IP storage, and only Dell IP storage into AI customers such as Neoclouds, sovereign customers, high-frequency traders, major technology companies, and semiconductor companies.

Transmission mechanism: AI storage demand is real, but Dell is increasingly bundling storage into AI server and rack-scale deployments. That creates a competitive risk for standalone storage vendors because Dell can attach storage at the point of AI server procurement, integrate it into a broader AI factory architecture, and support it with services and financing. NetApp and Pure Storage may still benefit from overall AI-driven storage TAM expansion, but Dell’s commentary indicates competitive displacement risk in enterprise and sovereign AI environments where customers value a single integrated infrastructure provider.

Near-term trading catalyst: Negative relative-read-through into storage vendor earnings if investors infer that Dell’s above-market storage growth is coming at the expense of standalone storage peers. Positive for total storage demand but potentially negative for relative share assumptions.

Longer-duration fundamental shift: AI infrastructure collapses the buying motion for compute, storage, networking, and services into a single architecture decision. That structurally favors vendors able to bundle storage into rack-scale AI systems and disadvantages vendors dependent on separate storage refresh cycles.

DATA CENTER POWER, COOLING, AND ELECTRICAL INFRASTRUCTURE (READ-THROUGH 8)

Affected Company Name (TICKER: Country): Vertiv Holdings (VRT: US), Eaton (ETN: US), Schneider Electric (SU: France), Legrand (LR: France), nVent Electric (NVT: US), Comfort Systems USA (FIX: US). Directional impact and magnitude: Positive, high magnitude for power and thermal infrastructure suppliers.

Call evidence: Dell said customers are optimizing spend, data center space, power, and cooling; highlighted 18th-generation PowerEdge systems with 13-to-1 consolidation potential; referenced direct liquid cooling in large deployments; and noted data center readiness as a factor in AI server deployment timing. Management also said demand is not the issue in 2H; supply and deployment constraints are.

Transmission mechanism: Dell’s demand commentary supports the view that the AI infrastructure bottleneck is expanding from GPU availability into facility-level power density, cooling, electrical distribution, and deployment readiness. High-density AI racks require liquid cooling, power distribution, switchgear, thermal management, busway, UPS, monitoring, and specialized mechanical/electrical construction. Even traditional server refresh demand is being driven partly by power, cooling, and space constraints, which supports retrofits as well as new builds.

Near-term trading catalyst: Positive for order-book sentiment across Vertiv, Eaton, Schneider, Legrand, nVent, and Comfort Systems. Dell’s comment that demand is supply-constrained rather than demand-constrained supports continued backlog durability for electrical and thermal infrastructure providers.

Longer-duration fundamental shift: Power and cooling are becoming strategic enablers of AI capacity. The market is likely to reward suppliers positioned at the intersection of AI rack density, electrical infrastructure, and liquid cooling because these categories are moving from ancillary data center spend to core AI deployment constraints.

COMMERCIAL PCS, WINDOWS REFRESH, AND EDGE AI ENDPOINTS (READ-THROUGH 9)

Affected Company Name (TICKER: Country): Microsoft (MSFT: US), Intel (INTC: US), Advanced Micro Devices (AMD: US), Qualcomm (QCOM: US), HP Inc. (HPQ: US), Lenovo Group (0992: Hong Kong). Directional impact and magnitude: Positive, medium magnitude for Microsoft and PC silicon suppliers; mixed for HP and Lenovo because end-market demand is positive but Dell is taking share.

Call evidence: Dell reported CSG revenue up 17%, commercial PC revenue up 18%, consumer revenue up 9%, and commercial demand growth for the 9th consecutive quarter. Management said roughly 1/3 of the installed base is 4 years or older, Windows 11 refresh activity caught up during the quarter, and customers are looking for more capable PCs as genAI workloads move to the edge. Dell also noted stronger high-price-band products and higher attach of peripherals and services.

Transmission mechanism: The call supports a healthier enterprise PC refresh cycle than a purely replacement-driven model would imply. Windows 11 migration, aging installed bases, higher security/performance requirements, and edge AI use cases are supporting unit growth, ASP expansion, and richer silicon configurations. Microsoft benefits through Windows ecosystem relevance and enterprise endpoint refresh; Intel, AMD, and Qualcomm benefit through higher-performance commercial PC demand and AI PC configurations. HP and Lenovo benefit from market recovery but face a negative relative-share signal because Dell explicitly said it gained share for the 2nd consecutive quarter.

Near-term trading catalyst: Positive for PC shipment expectations, commercial PC ASPs, and Windows refresh sentiment. Dell’s 20% Q2 CSG growth guide is an important datapoint for the broader PC ecosystem.

Longer-duration fundamental shift: AI workloads are moving from centralized data centers to edge endpoints, supporting a more capable commercial PC installed base. However, the consumer and SMB segments remain price-sensitive; Dell acknowledged that earlier price moves tempered transactional demand, creating a negative read-through for lower-end PC elasticity.

HYBRID AI, SOVEREIGN AI, AND ON-PREM ENTERPRISE DEPLOYMENT (READ-THROUGH 10)

Affected Company Name (TICKER: Country): Alphabet (GOOGL: US), Palantir Technologies (PLTR: US), ServiceNow (NOW: US), CrowdStrike (CRWD: US), Microsoft (MSFT: US), Amazon (AMZN: US). Directional impact and magnitude: Positive, medium magnitude for Alphabet, Palantir, ServiceNow, and CrowdStrike; neutral-to-slight negative narrative impact for centralized public-cloud-only AI monetization at Microsoft and Amazon, with limited near-term EPS impact.

Call evidence: Dell highlighted Google Distributed Cloud bringing Gemini models on-premises with confidential compute so customers can run AI closer to data while meeting data residency, privacy, and sovereignty requirements. Dell also identified OpenAI, ServiceNow, Palantir, and CrowdStrike as AI factory ecosystem partners and described desk-side AI solutions for secure local use cases such as coding, research, and private assistance.

Transmission mechanism: The call supports hybrid and on-prem AI deployment rather than a model where all enterprise AI workloads migrate to centralized public cloud. This is positive for Alphabet’s Google Distributed Cloud positioning, and for software/security platforms that can embed into private, sovereign, and regulated AI environments. Palantir, ServiceNow, and CrowdStrike benefit from the enterprise need to operationalize AI in controlled environments tied to workflows, data governance, automation, and security. For Microsoft and Amazon, the read-through is not an outright negative because both can participate in hybrid AI, but it does challenge the assumption that enterprise AI spend accrues only to centralized hyperscale cloud infrastructure.

Near-term trading catalyst: Positive for companies explicitly positioned as Dell AI factory ecosystem partners, though near-term revenue magnitude is likely smaller than the infrastructure read-throughs. The more actionable near-term signal is for Alphabet because Google Distributed Cloud was specifically tied to Gemini on-premises deployment.

Longer-duration fundamental shift: Sovereignty, privacy, data gravity, and enterprise control are becoming core AI architecture requirements. This supports hybrid AI platforms and AI software vendors embedded in regulated workflows, while limiting the extent to which public cloud alone captures all enterprise AI value.

May 28

$DELL EXECUTIVE CALL SUMMARY: Dell Technologies (05/28/26)

Dell delivered an unusually large Q1 FY27 upside event across revenue, EPS, AI server bookings, traditional server demand, PC profitability, and FY27 guidance. Q1 revenue was $43.842B, up 88% y/y, and non-GAAP EPS was $4.86, up 214% y/y; GAAP EPS was $5.24, up 282% y/y. Relative to prior Q1 guidance of $34.7B-$35.7B revenue and $2.90 non-GAAP EPS at the midpoint, revenue exceeded the prior midpoint by $8.642B, or 24.6%, and non-GAAP EPS exceeded the prior midpoint by $1.96, or 67.6%. Relative to the Bloomberg estimates embedded in the call transcript, Q1 revenue exceeded the $35.064B estimate by $8.778B, or 25.0%, and non-GAAP EPS exceeded the $3.047 estimate by $1.813, or 59.5%. The magnitude of the beat was not isolated to AI servers; the key incremental message was that AI demand is now pulling traditional servers, storage, PCs, services, financing, and enterprise infrastructure refresh forward in parallel.

The quarter materially reset the FY27 earnings base. Dell raised FY27 revenue guidance to $165B-$169B, with a midpoint of $167B, versus prior FY27 guidance of $138B-$142B, with a midpoint of $140B. The midpoint increase was $27B, or 19.3%. Dell raised FY27 non-GAAP EPS guidance to $17.90, plus or minus $0.25, versus prior midpoint guidance of $12.90, a $5.00 increase, or 38.8%. AI-optimized server revenue guidance was raised to roughly $60B from $50B, a $10B increase, or 20.0%. The updated guide is also materially above the Bloomberg full-year figures embedded in the transcript, with FY27 revenue guidance $24.882B, or 17.5%, above the $142.118B estimate and non-GAAP EPS guidance $4.758, or 36.2%, above the $13.142 estimate.

The investment debate changed materially. Prior to the call, the key question was whether Dell’s AI server momentum could scale without gross margin deterioration and whether traditional infrastructure demand would remain cyclical. After the call, the key question is whether supply can keep pace with demand and whether Dell can preserve margin discipline while AI servers become a much larger portion of revenue. Management’s strongest demand statement was that “demand is not slowing but accelerating,” while the most important limiting factor was stated directly as “we are supply-constrained in the second half.” The call therefore created a highly favorable near-term revision setup, but also elevated risk around component availability, pricing elasticity, AI server mix, and potential pull-forward.

QUARTER QUALITY AND REVENUE COMPOSITION

The quality of the revenue beat was high in terms of breadth, but mixed in terms of gross margin composition. ISG revenue was $29.009B, up 181% y/y, representing 66.2% of total reported revenue and accounting for 91.3% of Dell’s y/y revenue growth. AI-optimized server revenue was $16.132B, up 757% y/y, representing 36.8% of total company revenue and 55.6% of ISG revenue. Traditional servers and networking revenue was $8.543B, up 92% y/y, and storage revenue was $4.334B, up 8% y/y. CSG revenue was $14.609B, up 17% y/y, with commercial client revenue of $13.020B, up 18%, and consumer revenue of $1.589B, up 9%.

The sequential comparison versus Q4 FY26 underscores the scale of the acceleration. Total revenue increased 31.3% q/q from $33.379B. ISG revenue increased 48.0% q/q from $19.602B. AI server revenue increased 80.2% q/q from $8.952B, traditional servers and networking increased 46.0% q/q from $5.853B, and CSG increased 8.3% q/q from $13.494B. Storage was the only major sequential laggard, down 9.7% q/q from $4.797B, although that decline should be viewed against storage’s typical seasonal and deal-timing dynamics, the mix shift away from third-party storage, and management’s assertion that Dell IP storage demand is compounding above market.

AI server revenue was the largest growth driver, but traditional servers were the most strategically important surprise. AI server y/y revenue growth accounted for approximately 69.6% of Dell’s total y/y revenue growth, but the 92% growth in traditional servers and networking indicates that enterprise infrastructure demand is no longer behaving like a normal post-refresh cycle. Management attributed traditional server upside to absolute unit growth, higher server content, more cores, more DRAM and NAND per server, pricing inflation, modernization, data center consolidation, and incremental AI inference workloads. The most important quote on this point was that “AI is driving a new marketplace for traditional servers.”

Margin quality was more nuanced than the headline EPS beat. Non-GAAP gross margin dollars increased 57% y/y to $7.947B, but non-GAAP gross margin rate declined to 18.1% from 21.6%, a 350 bps decline, primarily from the mix shift toward lower-margin AI servers. Non-GAAP operating expenses increased 9% y/y to $3.712B, but fell to 8.4% of revenue from 14.5%, a 610 bps improvement. Non-GAAP operating income increased 154% y/y to $4.235B, and non-GAAP operating margin expanded to 9.7% from 7.1%. The EPS beat was therefore driven by the combination of revenue scale, pricing discipline, storage mix, PC margin expansion, and OpEx leverage, rather than by gross margin expansion.

ISG operating income was $3.055B, up 206% y/y, with operating margin of 10.5%, up 80 bps y/y. Sequentially, however, ISG margin declined from 14.8% in Q4 FY26, reflecting the much higher AI server mix. This is central to the investment case: AI servers are now large enough to transform Dell’s growth profile, but the associated operating margin remains in the mid-single-digit range. Storage profitability and traditional server margin stability offset the AI mix pressure in Q1, but future earnings leverage depends on sustained storage attach, services attach, Dell IP mix, and disciplined pricing.

CSG profitability was a major positive surprise but should not be extrapolated mechanically. CSG operating income increased 79% y/y to $1.170B, and operating margin expanded to 8.0% from 5.2%. Sequentially, CSG operating income increased 86.0% from $629M in Q4 FY26, and margin increased from 4.7% to 8.0%. Management attributed the performance to enterprise PC demand, higher attach of peripherals and services, scale, commercial mix, pricing, and consumer profitability improvement. However, management guided Q2 CSG operating income margin to roughly 6%, suggesting Q1’s 8% margin was elevated and partly timing-driven.

Cash generation was robust, reinforcing the quality of the quarter. Cash flow from operations was $4.081B, up 46% y/y, and adjusted free cash flow was $3.165B, up 42% y/y. Cash and investments ended the quarter at $14.1B, up $0.8B sequentially, and core leverage was 1.2x. Dell returned $2.1B to shareholders, including repurchases of 11M shares at an average price of $147 and a dividend of approximately $0.63 per share. The cash result matters because it helps offset concerns that the AI server ramp could pressure working capital through inventory, supplier prepayments, financing support, and large customer deployment timing.

AI SERVER DEMAND, BACKLOG, AND VISIBILITY

The AI server metrics were the most important datapoints on the call. Dell booked $24.4B of AI orders, recognized $16.1B of AI server revenue, and exited Q1 with $51.3B of AI backlog. Implied AI server book-to-bill was approximately 1.5x. Beginning backlog can be inferred at approximately $43.0B, meaning backlog increased $8.3B, or 19.3%, despite Dell converting $16.1B of AI server revenue in the quarter. This is highly unusual for a hardware infrastructure business at this scale and supports management’s assertion that demand is materially outpacing supply.

The revised $60B FY27 AI server revenue guide implies that Q1 and Q2 together should generate approximately $31.6B of AI server revenue, assuming Q2 AI server revenue of $15.5B. That leaves approximately $28.4B for 2H FY27, or $14.2B per quarter. The 2H implied quarterly run-rate is below Q1 actual and Q2 guided AI server revenue, which supports 2 interpretations. The conservative interpretation is that management is embedding supply constraints, technology transitions, data center readiness risk, and prudence after only 90 days of FY27. The more constructive interpretation is that the guide leaves upside if memory, CPU, networking, power, or customer data center capacity improves faster than assumed.

The customer base has broadened materially. Management said AI customer count surpassed 5,000, up more than 50% in 6 months, with growth across Neocloud, sovereign, and enterprise customers. Pipeline over the next 5 quarters was described as a multiple of backlog and growing across each customer vertical. This matters because prior Dell AI server debates frequently centered on customer concentration and durability of demand from a limited set of large buyers. The updated disclosures imply broader adoption, but not necessarily lower risk: Neocloud and sovereign demand can be lumpy, dependent on financing, and sensitive to GPU availability, data center power, and AI monetization.

The Dell AI factory strategy is expanding from rack-scale GPU servers into a broader enterprise architecture stack. Management highlighted new infrastructure across NVIDIA’s Vera Rubin platform, Rubin GPU architecture, RTX GPUs, Dell Pro Max systems, GB10 and GB300 desktop support, PowerRack, 18th-generation PowerEdge servers, Dell AI data platform enhancements, PowerStore, ObjectScale, PowerFlex, and ecosystem relationships with NVIDIA, Google Cloud, OpenAI, xAI, ServiceNow, Palantir, and CrowdStrike. Strategically, this creates an opportunity to capture more than bare-metal AI server revenue through storage, networking, software, services, financing, and on-prem enterprise AI deployment.

The AI storage attach discussion was important because it addresses the main bear argument that Dell is capturing low-margin pass-through AI server revenue with limited economic differentiation. Management said Dell is increasing the amount of storage and services sold to AI customers, including Neoclouds, sovereigns, high-frequency traders, large technology companies, and semiconductor companies. The unstructured storage portfolio had its best demand quarter ever, and management emphasized that unstructured data is the critical dataset for AI workloads. Dell IP storage momentum across PowerMax, PowerStore, PowerScale, ObjectScale, and data protection is therefore central to whether AI servers become a low-margin revenue spike or a durable profit pool.

TRADITIONAL SERVERS, STORAGE, AND CSG

Traditional server strength materially broadened the investment thesis. Revenue was $8.543B, up 92% y/y, and management guided traditional servers to grow just over 60% for FY27. The drivers were both cyclical and structural. Cyclical drivers included customers securing supply ahead of further price increases, refreshing aging 14G and older server fleets, and consolidating compute footprints. Structural drivers included AI inference, agentic workloads, CPU-side orchestration, and denser servers used by Neoclouds, advanced enterprise users, semiconductor companies, and large technology companies. The 18G server discussion, including 13-to-1 consolidation, reinforces that modernization is a cost and capacity response to power, cooling, and data center footprint constraints, not only a discretionary refresh.

The traditional server upside carries pull-forward risk, but the call offered evidence that demand is not purely pull-forward. Management explicitly acknowledged buy-ahead behavior, customer concern over rising prices, and proactive supply procurement. However, pipelines reportedly grew in-quarter and 2 quarters out at rates above historical norms, and management cited large enterprise customer conversations covering 3-, 4-, and 5-year supply arrangements. The distinction is critical: if demand is merely pulled forward, FY28 faces a digestion problem; if demand is multi-year infrastructure reservation driven by AI and supply scarcity, the revenue base can remain structurally higher. The call did not eliminate this uncertainty, but the backlog, pipeline, and supply constraint commentary tilted the evidence toward structural demand.

Storage revenue growth of 8% y/y was modest relative to servers, but strategically important because of margin. Dell IP delivered a record demand growth quarter and its 5th consecutive quarter of demand growth above market. PowerStore delivered its 8th consecutive quarter of double-digit demand growth; PowerScale and ObjectScale had 3 consecutive quarters of growth, including double-digit growth in each of the last 2 quarters. Dell IP storage is becoming a larger mix of storage and carries higher margins. The storage guide of mid-single-digit growth for FY27 is less explosive than server growth, but the potential investment upside is in delayed AI storage pull-through, higher Dell IP mix, and services attach rather than immediate revenue acceleration.

CSG was better than expected and more relevant to the AI thesis than a standard PC-cycle analysis would suggest. Commercial PC revenue was $13.020B, up 18% y/y, with broad-based enterprise demand and share gain. Consumer revenue grew 9%, supported by gaming. Management said roughly 1/3 of the installed base consists of devices 4 years or older, and that the Windows 11 refresh lag caught up during the quarter. More strategically, management framed more capable PCs as edge endpoints for gen-AI workloads, while attach of peripherals and services improved profitability. CSG is not the primary driver of the stock’s AI multiple, but it provided material EPS support and reduces the risk that Dell becomes a 1-product AI server story.

GUIDANCE AND COMPARISON TO PRIOR GUIDANCE

Q2 FY27 guidance implies another extraordinary quarter. Revenue is guided to $44B-$45B, with a midpoint of $44.5B, up roughly 49%-50% y/y and up 1.5% sequentially from Q1. ISG is expected to grow roughly 75%, supported by $15.5B of AI server revenue, while CSG is expected to grow roughly 20%. Operating income is expected to grow roughly 80% y/y. Non-GAAP EPS guidance is $4.80, plus or minus $0.10, up over 100% y/y at the midpoint. The sequential EPS decline from $4.86 in Q1 to $4.80 in Q2 despite slightly higher revenue reflects mix, CSG margin normalization to roughly 6%, and continued supply/pricing management.

The FY27 guidance revision was the most important numerical development. Prior FY27 guidance from Q4 FY26 called for $138B-$142B of revenue, roughly $50B of AI server revenue, GAAP EPS of $11.52 at the midpoint, and non-GAAP EPS of $12.90 at the midpoint. Updated FY27 guidance calls for $165B-$169B of revenue, roughly $60B of AI server revenue, GAAP EPS of $17.31 at the midpoint, and non-GAAP EPS of $17.90 at the midpoint. The revision represents a near-complete reset of consensus expectations after only 1 quarter of the fiscal year.

Full-year guidance embeds caution despite the large increase. Q1 actual revenue of $43.842B plus Q2 midpoint revenue of $44.5B implies 1H FY27 revenue of $88.342B, or 52.9% of the FY27 midpoint. That leaves 2H FY27 revenue of $78.658B, or 47.1% of the FY27 midpoint. An analyst noted on the call that historically 2H has represented roughly 52% of annual revenue, while the updated guide implies about 48%. Management’s answer was not that demand is softening, but that supply is the limiting factor. This creates a favorable asymmetry to the extent additional supply becomes available, but it also means Dell’s guidance is hostage to memory, CPUs, hard drives, data center readiness, and partner execution.

The gross margin guide was better than expected in the non-AI core business. Management said pricing discipline and margin stability from Q4 and Q1 are holding, and that gross margin outlook excluding AI mix is better than 90 days ago. Drivers include Dell IP storage mix, traditional server margin stability despite inflation, and CSG pricing discipline. This is an important offset to the AI mix drag. However, AI server gross margin dilution will remain visible in the consolidated gross margin line, and the burden of proof has shifted to Dell’s ability to keep storage, services, and traditional infrastructure margins strong enough to offset AI scale.

Supply risk is broadening beyond GPUs. Management identified DRAM, NAND, microprocessors, and hard drives as the most pressured categories, with utilization on trailing semiconductor nodes filling and leading-edge nodes fully allocated with 1-year lead times. Separately, management said repricing is occurring “every day,” and that inflation spans fuel, raw materials, DRAM, NAND, and CPUs. This reinforces that Dell’s near-term opportunity is not demand creation; it is scarce component allocation, price pass-through, and supply-chain execution. The risk is that further price increases begin to cause customer deferrals, especially in transactional PCs and SMB, even as large enterprise customers seek multi-year supply access.

INVESTMENT IMPLICATIONS

The quarter is materially positive for the long thesis because the FY27 EPS base was reset by 38.8%, and the raise was supported by backlog, orders, and broad-based segment performance rather than a single customer datapoint. Dell’s AI server revenue, backlog, and customer-count metrics show that the company has become a primary scaled beneficiary of AI infrastructure deployment. The strategic question has moved from participation to monetization. If AI servers remain supply-constrained and Dell continues to attach storage, services, and financing, the company can plausibly sustain a larger revenue base with adequate return on capital despite lower AI server unit economics.

The most attractive element for investors is the combination of backlog visibility and conservative 2H implied revenue. The $51.3B AI backlog, 1.5x AI book-to-bill, and $60B FY27 AI server guide imply high near-term visibility. Yet the guide embeds lower average AI server revenue in 2H than in Q1/Q2, creating potential upside if component availability improves. This makes the next revision catalysts relatively clear: evidence of additional memory and CPU availability, continued AI order conversion, storage attach, and limited price elasticity would support further upward revisions.

The most important bear-case issue is that AI server scale does not automatically translate into high-quality earnings. AI server profitability remains in line with a mid-single-digit operating income rate target. Consolidated non-GAAP gross margin rate fell 350 bps y/y, and ISG operating margin declined sharply q/q from 14.8% to 10.5% as AI server mix increased. The business can produce substantial absolute profit dollars, but multiple expansion requires confidence that Dell is more than a low-margin integrator of scarce NVIDIA-based systems. The storage and services attach narrative is therefore critical, and Q2/Q3 evidence of Dell IP storage pull-through will matter disproportionately.

The traditional server acceleration is a major positive revision vector but also the cleanest area for future disappointment. Management made a persuasive case that inference and agentic workloads are increasing demand for CPU infrastructure, while old installed-base refresh and consolidation are real. However, the 92% y/y growth rate almost certainly includes price, content, and buy-ahead. A material portion of demand may be budget reallocation or supply hoarding, not a steady-state server TAM expansion. The stock’s post-print setup therefore depends on whether traditional servers normalize at a much higher base or experience digestion after current supply-scarcity behavior fades.

The CSG upside provides near-term EPS support but is unlikely to command the same multiple as ISG AI growth. The 8% CSG operating margin was excellent, but management guided Q2 CSG margin to roughly 6%, explicitly balancing demand, share, and profitability. PC demand is benefiting from commercial refresh, Windows 11, richer configurations, and AI-at-the-edge narratives, but it remains more cyclical and price-sensitive than data center AI infrastructure. CSG should be treated as a cash and earnings stabilizer, not the primary reason to own the stock.

Valuation has become more complex. The Bloomberg transcript header showed a $317.05 share price, $205.9B market cap, and 151.9% YTD performance before the full market reaction, implying roughly 17.7x the new $17.90 FY27 non-GAAP EPS midpoint. Reuters reported that shares rose around 22% in extended trading after the release, which would imply roughly 21.6x FY27 non-GAAP EPS if the move held. That is still not extreme for a company posting this level of EPS revision, but the stock is no longer merely a cheap hardware re-rating story. Incremental upside increasingly requires evidence that FY27 guidance remains conservative or that FY28 earnings power is structurally higher than the new base.

The immediate investment conclusion is favorable but not without elevated execution risk. The quarter likely forces substantial Street revisions higher, supports positive estimate momentum, and validates Dell’s positioning as a scaled AI infrastructure supplier with improving enterprise relevance. The risk/reward is most attractive if the investment horizon emphasizes the next 1-3 quarters of supply-constrained demand, backlog conversion, and potential guide-up. The risk/reward becomes less straightforward at a materially higher post-print multiple if the debate shifts to FY28 normalization, AI server margins, Neocloud credit quality, sovereign demand lumpiness, or customer budget digestion.

3

3

21

13,327

May 28

$DELL EXECUTIVE CALL SUMMARY: Dell Technologies (05/28/26)

Dell delivered an unusually large Q1 FY27 upside event across revenue, EPS, AI server bookings, traditional server demand, PC profitability, and FY27 guidance. Q1 revenue was $43.842B, up 88% y/y, and non-GAAP EPS was $4.86, up 214% y/y; GAAP EPS was $5.24, up 282% y/y. Relative to prior Q1 guidance of $34.7B-$35.7B revenue and $2.90 non-GAAP EPS at the midpoint, revenue exceeded the prior midpoint by $8.642B, or 24.6%, and non-GAAP EPS exceeded the prior midpoint by $1.96, or 67.6%. Relative to the Bloomberg estimates embedded in the call transcript, Q1 revenue exceeded the $35.064B estimate by $8.778B, or 25.0%, and non-GAAP EPS exceeded the $3.047 estimate by $1.813, or 59.5%. The magnitude of the beat was not isolated to AI servers; the key incremental message was that AI demand is now pulling traditional servers, storage, PCs, services, financing, and enterprise infrastructure refresh forward in parallel.

The quarter materially reset the FY27 earnings base. Dell raised FY27 revenue guidance to $165B-$169B, with a midpoint of $167B, versus prior FY27 guidance of $138B-$142B, with a midpoint of $140B. The midpoint increase was $27B, or 19.3%. Dell raised FY27 non-GAAP EPS guidance to $17.90, plus or minus $0.25, versus prior midpoint guidance of $12.90, a $5.00 increase, or 38.8%. AI-optimized server revenue guidance was raised to roughly $60B from $50B, a $10B increase, or 20.0%. The updated guide is also materially above the Bloomberg full-year figures embedded in the transcript, with FY27 revenue guidance $24.882B, or 17.5%, above the $142.118B estimate and non-GAAP EPS guidance $4.758, or 36.2%, above the $13.142 estimate.

The investment debate changed materially. Prior to the call, the key question was whether Dell’s AI server momentum could scale without gross margin deterioration and whether traditional infrastructure demand would remain cyclical. After the call, the key question is whether supply can keep pace with demand and whether Dell can preserve margin discipline while AI servers become a much larger portion of revenue. Management’s strongest demand statement was that “demand is not slowing but accelerating,” while the most important limiting factor was stated directly as “we are supply-constrained in the second half.” The call therefore created a highly favorable near-term revision setup, but also elevated risk around component availability, pricing elasticity, AI server mix, and potential pull-forward.

QUARTER QUALITY AND REVENUE COMPOSITION

The quality of the revenue beat was high in terms of breadth, but mixed in terms of gross margin composition. ISG revenue was $29.009B, up 181% y/y, representing 66.2% of total reported revenue and accounting for 91.3% of Dell’s y/y revenue growth. AI-optimized server revenue was $16.132B, up 757% y/y, representing 36.8% of total company revenue and 55.6% of ISG revenue. Traditional servers and networking revenue was $8.543B, up 92% y/y, and storage revenue was $4.334B, up 8% y/y. CSG revenue was $14.609B, up 17% y/y, with commercial client revenue of $13.020B, up 18%, and consumer revenue of $1.589B, up 9%.

The sequential comparison versus Q4 FY26 underscores the scale of the acceleration. Total revenue increased 31.3% q/q from $33.379B. ISG revenue increased 48.0% q/q from $19.602B. AI server revenue increased 80.2% q/q from $8.952B, traditional servers and networking increased 46.0% q/q from $5.853B, and CSG increased 8.3% q/q from $13.494B. Storage was the only major sequential laggard, down 9.7% q/q from $4.797B, although that decline should be viewed against storage’s typical seasonal and deal-timing dynamics, the mix shift away from third-party storage, and management’s assertion that Dell IP storage demand is compounding above market.

AI server revenue was the largest growth driver, but traditional servers were the most strategically important surprise. AI server y/y revenue growth accounted for approximately 69.6% of Dell’s total y/y revenue growth, but the 92% growth in traditional servers and networking indicates that enterprise infrastructure demand is no longer behaving like a normal post-refresh cycle. Management attributed traditional server upside to absolute unit growth, higher server content, more cores, more DRAM and NAND per server, pricing inflation, modernization, data center consolidation, and incremental AI inference workloads. The most important quote on this point was that “AI is driving a new marketplace for traditional servers.”

Margin quality was more nuanced than the headline EPS beat. Non-GAAP gross margin dollars increased 57% y/y to $7.947B, but non-GAAP gross margin rate declined to 18.1% from 21.6%, a 350 bps decline, primarily from the mix shift toward lower-margin AI servers. Non-GAAP operating expenses increased 9% y/y to $3.712B, but fell to 8.4% of revenue from 14.5%, a 610 bps improvement. Non-GAAP operating income increased 154% y/y to $4.235B, and non-GAAP operating margin expanded to 9.7% from 7.1%. The EPS beat was therefore driven by the combination of revenue scale, pricing discipline, storage mix, PC margin expansion, and OpEx leverage, rather than by gross margin expansion.

ISG operating income was $3.055B, up 206% y/y, with operating margin of 10.5%, up 80 bps y/y. Sequentially, however, ISG margin declined from 14.8% in Q4 FY26, reflecting the much higher AI server mix. This is central to the investment case: AI servers are now large enough to transform Dell’s growth profile, but the associated operating margin remains in the mid-single-digit range. Storage profitability and traditional server margin stability offset the AI mix pressure in Q1, but future earnings leverage depends on sustained storage attach, services attach, Dell IP mix, and disciplined pricing.

CSG profitability was a major positive surprise but should not be extrapolated mechanically. CSG operating income increased 79% y/y to $1.170B, and operating margin expanded to 8.0% from 5.2%. Sequentially, CSG operating income increased 86.0% from $629M in Q4 FY26, and margin increased from 4.7% to 8.0%. Management attributed the performance to enterprise PC demand, higher attach of peripherals and services, scale, commercial mix, pricing, and consumer profitability improvement. However, management guided Q2 CSG operating income margin to roughly 6%, suggesting Q1’s 8% margin was elevated and partly timing-driven.

Cash generation was robust, reinforcing the quality of the quarter. Cash flow from operations was $4.081B, up 46% y/y, and adjusted free cash flow was $3.165B, up 42% y/y. Cash and investments ended the quarter at $14.1B, up $0.8B sequentially, and core leverage was 1.2x. Dell returned $2.1B to shareholders, including repurchases of 11M shares at an average price of $147 and a dividend of approximately $0.63 per share. The cash result matters because it helps offset concerns that the AI server ramp could pressure working capital through inventory, supplier prepayments, financing support, and large customer deployment timing.

AI SERVER DEMAND, BACKLOG, AND VISIBILITY

The AI server metrics were the most important datapoints on the call. Dell booked $24.4B of AI orders, recognized $16.1B of AI server revenue, and exited Q1 with $51.3B of AI backlog. Implied AI server book-to-bill was approximately 1.5x. Beginning backlog can be inferred at approximately $43.0B, meaning backlog increased $8.3B, or 19.3%, despite Dell converting $16.1B of AI server revenue in the quarter. This is highly unusual for a hardware infrastructure business at this scale and supports management’s assertion that demand is materially outpacing supply.

The revised $60B FY27 AI server revenue guide implies that Q1 and Q2 together should generate approximately $31.6B of AI server revenue, assuming Q2 AI server revenue of $15.5B. That leaves approximately $28.4B for 2H FY27, or $14.2B per quarter. The 2H implied quarterly run-rate is below Q1 actual and Q2 guided AI server revenue, which supports 2 interpretations. The conservative interpretation is that management is embedding supply constraints, technology transitions, data center readiness risk, and prudence after only 90 days of FY27. The more constructive interpretation is that the guide leaves upside if memory, CPU, networking, power, or customer data center capacity improves faster than assumed.

The customer base has broadened materially. Management said AI customer count surpassed 5,000, up more than 50% in 6 months, with growth across Neocloud, sovereign, and enterprise customers. Pipeline over the next 5 quarters was described as a multiple of backlog and growing across each customer vertical. This matters because prior Dell AI server debates frequently centered on customer concentration and durability of demand from a limited set of large buyers. The updated disclosures imply broader adoption, but not necessarily lower risk: Neocloud and sovereign demand can be lumpy, dependent on financing, and sensitive to GPU availability, data center power, and AI monetization.

The Dell AI factory strategy is expanding from rack-scale GPU servers into a broader enterprise architecture stack. Management highlighted new infrastructure across NVIDIA’s Vera Rubin platform, Rubin GPU architecture, RTX GPUs, Dell Pro Max systems, GB10 and GB300 desktop support, PowerRack, 18th-generation PowerEdge servers, Dell AI data platform enhancements, PowerStore, ObjectScale, PowerFlex, and ecosystem relationships with NVIDIA, Google Cloud, OpenAI, xAI, ServiceNow, Palantir, and CrowdStrike. Strategically, this creates an opportunity to capture more than bare-metal AI server revenue through storage, networking, software, services, financing, and on-prem enterprise AI deployment.

The AI storage attach discussion was important because it addresses the main bear argument that Dell is capturing low-margin pass-through AI server revenue with limited economic differentiation. Management said Dell is increasing the amount of storage and services sold to AI customers, including Neoclouds, sovereigns, high-frequency traders, large technology companies, and semiconductor companies. The unstructured storage portfolio had its best demand quarter ever, and management emphasized that unstructured data is the critical dataset for AI workloads. Dell IP storage momentum across PowerMax, PowerStore, PowerScale, ObjectScale, and data protection is therefore central to whether AI servers become a low-margin revenue spike or a durable profit pool.

TRADITIONAL SERVERS, STORAGE, AND CSG

Traditional server strength materially broadened the investment thesis. Revenue was $8.543B, up 92% y/y, and management guided traditional servers to grow just over 60% for FY27. The drivers were both cyclical and structural. Cyclical drivers included customers securing supply ahead of further price increases, refreshing aging 14G and older server fleets, and consolidating compute footprints. Structural drivers included AI inference, agentic workloads, CPU-side orchestration, and denser servers used by Neoclouds, advanced enterprise users, semiconductor companies, and large technology companies. The 18G server discussion, including 13-to-1 consolidation, reinforces that modernization is a cost and capacity response to power, cooling, and data center footprint constraints, not only a discretionary refresh.

The traditional server upside carries pull-forward risk, but the call offered evidence that demand is not purely pull-forward. Management explicitly acknowledged buy-ahead behavior, customer concern over rising prices, and proactive supply procurement. However, pipelines reportedly grew in-quarter and 2 quarters out at rates above historical norms, and management cited large enterprise customer conversations covering 3-, 4-, and 5-year supply arrangements. The distinction is critical: if demand is merely pulled forward, FY28 faces a digestion problem; if demand is multi-year infrastructure reservation driven by AI and supply scarcity, the revenue base can remain structurally higher. The call did not eliminate this uncertainty, but the backlog, pipeline, and supply constraint commentary tilted the evidence toward structural demand.

Storage revenue growth of 8% y/y was modest relative to servers, but strategically important because of margin. Dell IP delivered a record demand growth quarter and its 5th consecutive quarter of demand growth above market. PowerStore delivered its 8th consecutive quarter of double-digit demand growth; PowerScale and ObjectScale had 3 consecutive quarters of growth, including double-digit growth in each of the last 2 quarters. Dell IP storage is becoming a larger mix of storage and carries higher margins. The storage guide of mid-single-digit growth for FY27 is less explosive than server growth, but the potential investment upside is in delayed AI storage pull-through, higher Dell IP mix, and services attach rather than immediate revenue acceleration.

CSG was better than expected and more relevant to the AI thesis than a standard PC-cycle analysis would suggest. Commercial PC revenue was $13.020B, up 18% y/y, with broad-based enterprise demand and share gain. Consumer revenue grew 9%, supported by gaming. Management said roughly 1/3 of the installed base consists of devices 4 years or older, and that the Windows 11 refresh lag caught up during the quarter. More strategically, management framed more capable PCs as edge endpoints for gen-AI workloads, while attach of peripherals and services improved profitability. CSG is not the primary driver of the stock’s AI multiple, but it provided material EPS support and reduces the risk that Dell becomes a 1-product AI server story.

GUIDANCE AND COMPARISON TO PRIOR GUIDANCE

Q2 FY27 guidance implies another extraordinary quarter. Revenue is guided to $44B-$45B, with a midpoint of $44.5B, up roughly 49%-50% y/y and up 1.5% sequentially from Q1. ISG is expected to grow roughly 75%, supported by $15.5B of AI server revenue, while CSG is expected to grow roughly 20%. Operating income is expected to grow roughly 80% y/y. Non-GAAP EPS guidance is $4.80, plus or minus $0.10, up over 100% y/y at the midpoint. The sequential EPS decline from $4.86 in Q1 to $4.80 in Q2 despite slightly higher revenue reflects mix, CSG margin normalization to roughly 6%, and continued supply/pricing management.

The FY27 guidance revision was the most important numerical development. Prior FY27 guidance from Q4 FY26 called for $138B-$142B of revenue, roughly $50B of AI server revenue, GAAP EPS of $11.52 at the midpoint, and non-GAAP EPS of $12.90 at the midpoint. Updated FY27 guidance calls for $165B-$169B of revenue, roughly $60B of AI server revenue, GAAP EPS of $17.31 at the midpoint, and non-GAAP EPS of $17.90 at the midpoint. The revision represents a near-complete reset of consensus expectations after only 1 quarter of the fiscal year.

Full-year guidance embeds caution despite the large increase. Q1 actual revenue of $43.842B plus Q2 midpoint revenue of $44.5B implies 1H FY27 revenue of $88.342B, or 52.9% of the FY27 midpoint. That leaves 2H FY27 revenue of $78.658B, or 47.1% of the FY27 midpoint. An analyst noted on the call that historically 2H has represented roughly 52% of annual revenue, while the updated guide implies about 48%. Management’s answer was not that demand is softening, but that supply is the limiting factor. This creates a favorable asymmetry to the extent additional supply becomes available, but it also means Dell’s guidance is hostage to memory, CPUs, hard drives, data center readiness, and partner execution.

The gross margin guide was better than expected in the non-AI core business. Management said pricing discipline and margin stability from Q4 and Q1 are holding, and that gross margin outlook excluding AI mix is better than 90 days ago. Drivers include Dell IP storage mix, traditional server margin stability despite inflation, and CSG pricing discipline. This is an important offset to the AI mix drag. However, AI server gross margin dilution will remain visible in the consolidated gross margin line, and the burden of proof has shifted to Dell’s ability to keep storage, services, and traditional infrastructure margins strong enough to offset AI scale.

Supply risk is broadening beyond GPUs. Management identified DRAM, NAND, microprocessors, and hard drives as the most pressured categories, with utilization on trailing semiconductor nodes filling and leading-edge nodes fully allocated with 1-year lead times. Separately, management said repricing is occurring “every day,” and that inflation spans fuel, raw materials, DRAM, NAND, and CPUs. This reinforces that Dell’s near-term opportunity is not demand creation; it is scarce component allocation, price pass-through, and supply-chain execution. The risk is that further price increases begin to cause customer deferrals, especially in transactional PCs and SMB, even as large enterprise customers seek multi-year supply access.

INVESTMENT IMPLICATIONS

The quarter is materially positive for the long thesis because the FY27 EPS base was reset by 38.8%, and the raise was supported by backlog, orders, and broad-based segment performance rather than a single customer datapoint. Dell’s AI server revenue, backlog, and customer-count metrics show that the company has become a primary scaled beneficiary of AI infrastructure deployment. The strategic question has moved from participation to monetization. If AI servers remain supply-constrained and Dell continues to attach storage, services, and financing, the company can plausibly sustain a larger revenue base with adequate return on capital despite lower AI server unit economics.

The most attractive element for investors is the combination of backlog visibility and conservative 2H implied revenue. The $51.3B AI backlog, 1.5x AI book-to-bill, and $60B FY27 AI server guide imply high near-term visibility. Yet the guide embeds lower average AI server revenue in 2H than in Q1/Q2, creating potential upside if component availability improves. This makes the next revision catalysts relatively clear: evidence of additional memory and CPU availability, continued AI order conversion, storage attach, and limited price elasticity would support further upward revisions.

The most important bear-case issue is that AI server scale does not automatically translate into high-quality earnings. AI server profitability remains in line with a mid-single-digit operating income rate target. Consolidated non-GAAP gross margin rate fell 350 bps y/y, and ISG operating margin declined sharply q/q from 14.8% to 10.5% as AI server mix increased. The business can produce substantial absolute profit dollars, but multiple expansion requires confidence that Dell is more than a low-margin integrator of scarce NVIDIA-based systems. The storage and services attach narrative is therefore critical, and Q2/Q3 evidence of Dell IP storage pull-through will matter disproportionately.

The traditional server acceleration is a major positive revision vector but also the cleanest area for future disappointment. Management made a persuasive case that inference and agentic workloads are increasing demand for CPU infrastructure, while old installed-base refresh and consolidation are real. However, the 92% y/y growth rate almost certainly includes price, content, and buy-ahead. A material portion of demand may be budget reallocation or supply hoarding, not a steady-state server TAM expansion. The stock’s post-print setup therefore depends on whether traditional servers normalize at a much higher base or experience digestion after current supply-scarcity behavior fades.

The CSG upside provides near-term EPS support but is unlikely to command the same multiple as ISG AI growth. The 8% CSG operating margin was excellent, but management guided Q2 CSG margin to roughly 6%, explicitly balancing demand, share, and profitability. PC demand is benefiting from commercial refresh, Windows 11, richer configurations, and AI-at-the-edge narratives, but it remains more cyclical and price-sensitive than data center AI infrastructure. CSG should be treated as a cash and earnings stabilizer, not the primary reason to own the stock.

Valuation has become more complex. The Bloomberg transcript header showed a $317.05 share price, $205.9B market cap, and 151.9% YTD performance before the full market reaction, implying roughly 17.7x the new $17.90 FY27 non-GAAP EPS midpoint. Reuters reported that shares rose around 22% in extended trading after the release, which would imply roughly 21.6x FY27 non-GAAP EPS if the move held. That is still not extreme for a company posting this level of EPS revision, but the stock is no longer merely a cheap hardware re-rating story. Incremental upside increasingly requires evidence that FY27 guidance remains conservative or that FY28 earnings power is structurally higher than the new base.

The immediate investment conclusion is favorable but not without elevated execution risk. The quarter likely forces substantial Street revisions higher, supports positive estimate momentum, and validates Dell’s positioning as a scaled AI infrastructure supplier with improving enterprise relevance. The risk/reward is most attractive if the investment horizon emphasizes the next 1-3 quarters of supply-constrained demand, backlog conversion, and potential guide-up. The risk/reward becomes less straightforward at a materially higher post-print multiple if the debate shifts to FY28 normalization, AI server margins, Neocloud credit quality, sovereign demand lumpiness, or customer budget digestion.

May 28

$DELL (Bloomberg) -- (Updates with shares, adds metrics.)

Dell Technologies rose as much as 20% in extended New York trading after the Texas-based company raised both its full year revenue and adjusted EPS outlooks on strong demand for its AI-powering servers.

•Read more: Dell Boosts Outlook to $60 Billion in AI Server Sales This Year

2027 YEAR FORECAST

•Sees adjusted EPS $17.65 to $18.15, saw $12.65 to $13.15, estimate $13.14 (Bloomberg Consensus)

•Sees revenue $165 billion to $169 billion, saw $138 billion to $142 billion, estimate $142.12 billion

◦Sees AI Server revenue $60 billion

SECOND QUARTER FORECAST

•Sees revenue $44 billion to $45 billion, estimate $35.06 billion

◦Sees AI Server revenue about $15.5 billion

•Sees adjusted EPS $4.70 to $4.90, estimate $3.05

FIRST QUARTER RESULTS

•Total net revenue $43.84 billion, 88% y/y, estimate $35.52 billion

◦AI server revenue $16.1 billion, estimate $13.1b

◦Traditional servers and networking revenue $8.5 billion, 92% y/y

•Adjusted EPS $4.86 vs. $1.55 y/y, estimate $2.99

•AI server backlog $51.3 billion, estimate $45.33 billion

•Infrastructure Solutions Group net revenue $29.01 billion vs. $10.32 billion y/y, estimate $22.3 billion

◦Storage revenue $4.33 billion, 8.5% y/y, estimate $4.16 billion

•Client Solutions Group net revenue $14.61 billion, 17% y/y, estimate $12.93 billion

◦Commercial revenue $13.02 billion, 18% y/y, estimate $11.41 billion

◦Consumer revenue $1.59 billion, 8.6% y/y, estimate $1.46 billion

•Cash flow from operations of $4.1 billion

•Adjusted gross margin 18.1% vs. 21.6% y/y, estimate 17.3%

•Adjusted operating margin 9.7% vs. 7.1% y/y, estimate 7.82%

•Adjusted operating income $4.24 billion vs. $1.67 billion y/y, estimate $2.77 billion

COMMENTARY AND CONTEXT

•Booked $24.4 billion in AI orders for 1Q

•“We’re increasing our AI server revenue expectations for FY27 to $60 billion, which only goes to show the AI opportunity shows no signs of slowing”

1

1

10

12,624

The #DellTechWorld Expo Hall is open! Come by to see live demos of KIOXIA storage in every Dell enterprise product line. PowerEdge, PowerScale, PowerMax, PowerFlex, ObjectScale and more! Hear about it all in our 1:30 breakout session in Delfino 4105.

f.io/qQ4ZQ-KB

4

213

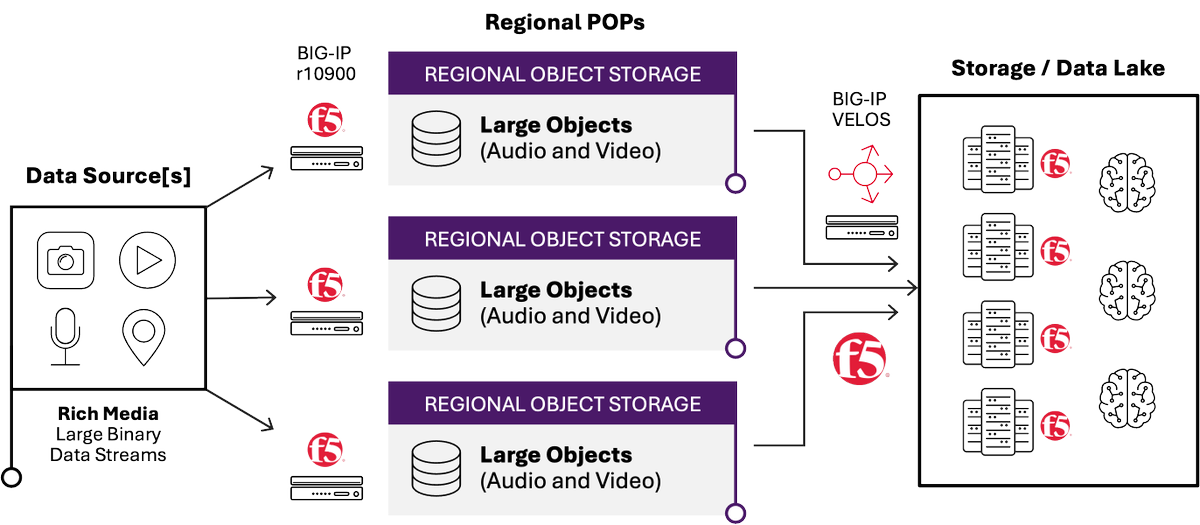

Gregory Coward dives deeper into high‑performance #S3 load balancing with Dell Technologies ObjectScale and F5 BIG‑IP, focusing on what actually matters once you move past the first design and start pushing real traffic.

lnkd.in/gqevFqkf

ALT S3 load balancing

3

312