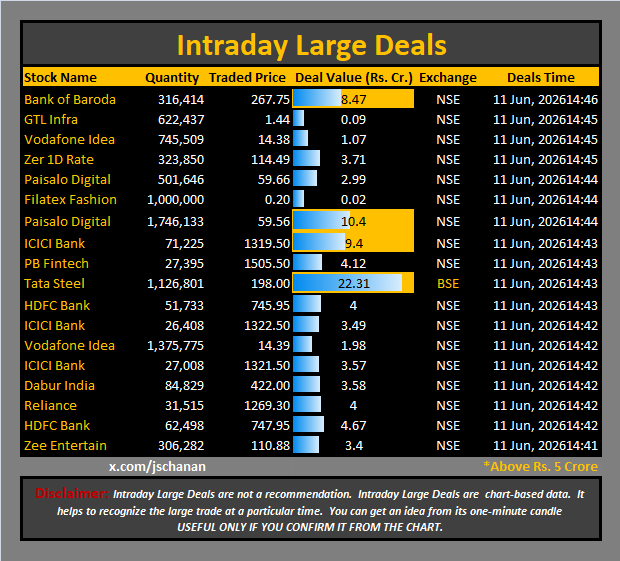

🚨📊 NSE TOP BLOCK DEALS OF THE DAY.

#stockmarket #stockalert #BlockDeal #nse #mudraguna #SRF #Infosys #AxisBank #PBFintech #PhoenixMills #BajajFinserv #FortisHealthcare #mahindra #TVSMotor #IndusTowers

9

What top #Midcap Funds bought and sold? 🧐

I analysed 18 top fundhouses so you don't have to.

Sector Trends:

Fund managers are heavily accumulating Retailing and Capital Markets this month. Electrical Equipment is also seeing strong inflows.

On the other hand, IT Software and Banks are facing the most significant selling pressure.

These are the major actions for May 2026:

📈 Top 5 Increased Exposure:

• Pb Fintech Ltd (9 AMCs)

• Lenskart Solutions Private Ltd. (5 AMCs)

• Billionbrains Garage Ventures (5 AMCs)

• Hindustan Petroleum Corporation (4 AMCs)

• Mankind Pharma Ltd. (4 AMCs)

📉 Top 5 Decreased Exposure:

• Ge Vernova T&D India Ltd (6 AMCs)

• Bse Ltd (5 AMCs)

• Oracle Financial Services Software (4 AMCs)

• Bharat Heavy Electricals Ltd. (4 AMCs)

• Indian Bank (3 AMCs)

🆕 Top 3 Fresh Buys:

• Billionbrains Garage Ventures

• Lenskart Solutions Private Ltd.

• Indus Towers Ltd

🚫 Top 3 Complete Exits:

• State Bank Of India.

• The Indian Hotels Company Ltd.

• Kpit Technologies Ltd.

This took a lot of time and effort. Please share 🙌

#FinAlpha1Pager #FinAlpha #MutualFunds #Midcap #PbFintech #Lenskart #Bse #MankindPharma #GeVernova

7

1

33

2,225

Dharma retweeted

#PBFintech Q4FY26 : Strong Growth Continues 🚀

CMP : ₹1,581

M.Cap : ₹73,187 Cr

P/E : 109x

📊 Q4FY26 Highlights

✅ Revenue: ₹2,061 Cr ( 37% YoY)

✅ EBITDA: ₹212 Cr ( 90% YoY)

✅ Net Profit: ₹261 Cr ( 54% YoY)

✅ EPS: ₹5.64 ( 52% YoY)

Key Business Updates:

• Premiums crossed ₹30,000 Cr

• Growth remained strong at 42%

• Renewals ARR reached ₹1,126 Cr

• PB Partners now covers 99% of India's pin codes

• 4.5 lakh advisor network established

Growth Drivers:

📈 Health insurance growth: 68%

📈 Protection premium growth: 57%

📈 AI-led underwriting & claims analysis

📈 PB Health hospital network expansion

📈 Wealth management & stock broking plans

Management Outlook:

🎯 FY27 growth guidance: 30%

🎯 Paisabazaar expected to turn strongly profitable

🎯 Renewals business scaling rapidly

🎯 Claims support becoming a major competitive advantage

Risks:

⚠️ Regulatory commission cap uncertainty

⚠️ Mis-selling and quality control at scale

⚠️ Dependence on technology infrastructure

Conclusion:

PB Fintech continues to strengthen its leadership in insurance distribution while building new growth engines in healthcare, lending and wealth.

Strong earnings, improving profitability and management confidence keep the long-term story intact.

Valuations not reasonable ⚠️

Technically, good risk reward at current levels.

Accumulation levels : 1550-15570

SL 1475, targets 1700/1830

Not a buy/sell call. DYOR. Not a SEBI registared.

#PBFintech #PolicyBazaar #StockMarketIndia

3

6

228

Jun 15

📊 Helios Mid Cap Fund Latest Holdings:

Top: #MCX, #Nippon Life AMC, #Paytm (One97), #phoenixwright Mills, #Fortis Healthcare, #Marico, #GMR Airports, #BSE, #Hitachi Energy, #Aditya Birla Capital & more.

Other Notable Holdings: #Motilal Oswal, #Schaeffler India, #Apar Industries, #IIFL Wealth, #UNO Minda, #GE T&D India, #Dixon Technologies, #IDFC First Bank, #Black Box, #Ami Organics, #Endurance Technologies, #Vishal Mega Mart, #Escorts Kubota, #APL Apollo Tubes, #pbFintech, #Ather Energy, #Radico Khaitan, #Max Financial, Cummins India, and many more (total ~68-70 stocks).

Recent Context/Additions: The fund has been active in mid-cap names with additions/increases in stocks like GMR Airports, Vishal Mega Mart, Paytm, and earlier entries such as CAMS, Piramal Pharma, Jain Resource Recycling, Urban Company, etc. It maintains a diversified mid-cap focus (with some small-cap exposure).

2

640

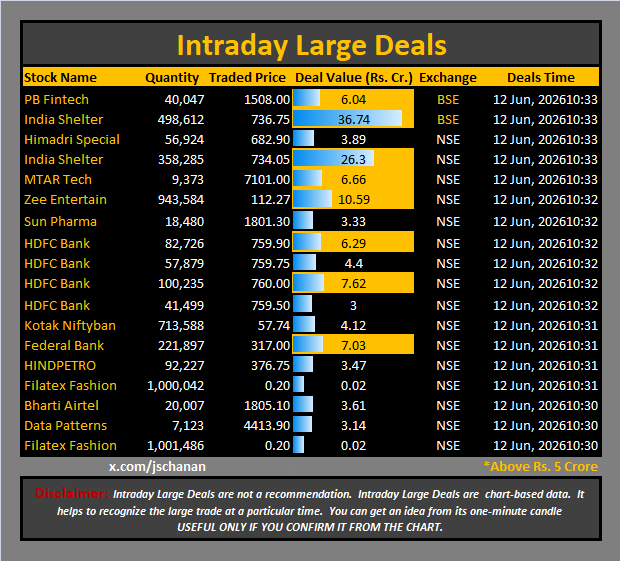

Intraday Large Deals

#Block #blockdeal #intraday #bigblock #LargeDeal

#PBFintech #IndiaShelter #HimadriSpecial #IndiaShelter #MTARTech #ZeeEntertain #SunPharma #HDFCBank #HDFCBank #HDFCBank #HDFCBank #KotakNiftyban #FederalBank #HINDPETRO #FilatexFashion #BhartiAirtel #DataPatterns #FilatexFashion

213

Jun 10

Heartiest congratulations to Hon'ble Prime Minister @narendramodi Ji on becoming India's longest-serving elected Prime Minister.

Through 4,399 days of leadership, India has witnessed remarkable progress across digital innovation, infrastructure development, Garib Kalyan, and Nari Shakti.

What better way to mark this milestone than with Jan Dhan crossing 58 crore accounts, a powerful reflection of India's financial inclusion journey under your leadership .

As we march towards #ViksitBharat2047, we at PB Fintech Ltd. stand committed to this nation-building journey.

@FollowCII

#LongestServingElectedPM

#ViksitBharat2047 #NationBuilding #NewIndia #DigitalIndia #InclusiveGrowth #PBFintech

3

1

2

152

Jun 9

📊 #RSI < 30 📉

MARKET CAP > 1000 Crore

( 09/06/2026 )

17 #OVERSOLD 👇 STOCKS

1) #NTPC

2) #ONGC

3) MUTHOOT FIN

4) PBFINTECH

5) SBI CARDS

6) JINDAL STAINLESS

7) RVNL

8) NATCO PHARMA

9) AVANTI FEEDS

10) WHIRLPOOL

11) ISGEC

12) SYMPHONY

13) ELITECON

14) TANFAC INDS

15) KS SMART

16) RAJESH EXPORTS

17) GRM OVERSEAS

09/06/2026

Note : info only

#RSI #OverSoldStocks

1

531

Jun 9

#PolicyBazaar (#PBFintech) remains under pressure, trading near ₹1,497 after a sharp correction from recent highs. 📉

#TechnicalAnalysis #StockMarket

53

8. Fintech & Digital Payments

🔸PB Fintech

🔸One97 Communications

🔸CAMS

🔸Multi Commodity Exchange

🔸KFin Technologies.

#stocktobuy #optiontrading #stockmarket #pbfintech #mcx #kfintech

1

5

668

#PBfintech update 👀

We gave a sell view near the top when everyone was turning bullish.

Fast forward to now — stock is already down ~10% from our discussed levels 📉

Sometimes protecting capital matters more than chasing momentum.

Patience right levels > emotions.

Not a trading recommendation. DYOR.

#StockMarketIndia #Nifty

🚨 PB FINTECH VIEW WORKED PERFECTLY 📉

Highlighted PB Fintech at resistance yesterday — stock corrected nearly 3% today. 🎯

✅ Resistance respected

✅ Rejection confirmed

✅ Structure played out

Price action always speaks first. ⚡

#Nifty #PBFintech

2

5

472

#PBFintech Dahiya ji ke jalve 👇👇 Have always warned to stay away from such shady self interest first promoters. A clear lesson for minority investors

6 Jun 2024

#transparancy is a hallmark of good management, don't expect it from cashtraps run by 'non promoters' !

Sebi notice to PB Fintech's Yashish Dahiya over $2 million Dubai investment

moneycontrol.com/news/busine…

1

1

5

2,468

Jun 4

3

1,998

💰 PB Fintech Ltd

📈 Cup & Handle Style Setup Emerging!

✅ Buy Above: 1,668

🎯 Target : 1,814 & 2,085

#POLICYBZR #PBFintech #Policybazaar #NSE #StockMarketIndia #BreakoutStocks #SwingTrading #PositionalTrading #TechnicalAnalysis

3

18

1,060