Prostarm Info Systems announces Strategic Realignment and Relocation of Manufacturing Operations

#ProstarmInfoSystems #StrategicRealignment

equitybulls.com/category.php…

162

Find Source & similar updates -> investorfeed.in/posts/prosta…

Find Historical Fillings of Prostarm Info Systems Ltd -> investorfeed.in/profiles/pro…

184

🔍 Prostarm Info Systems Shifts Manufacturing Strategy – Key Insights | MCap 929.63 Cr

- Manufacturing realigned to enhance efficiency, focusing on core segments.

- Servo Stabilizer & Isolation Transformers shifting from Pune (Pisoli Unit) to Navi Mumbai (Mahape Unit).

- Lithium Battery production relocating from Navi Mumbai (Mahape Unit) to Ahmedabad (Bakrol Unit).

- FY2025-26 turnover: INR 385.77 Crores.

- Servo Stabilizers contributed INR 5.17 Crores (1.34% of total).

- Lithium Batteries contributed INR 25.25 Crores (6.55% of total).

- Relocation completion target: August 2026.

- Goals: Streamlining resources, boosting efficiency, and scaling operations.

Disc: Information provided in above tweet can be inaccurate, verify through the source i.e. attached image(s) & in reply before making any investment decision.

1

1

276

10h

Prostarm Info Systems Ltd has approved a strategic realignment of its manufacturing & business operations. The Servo Stabilizer & Isolation Transformers business from the Pisoli Unit (Pune) will be relocated & consolidated to the Mahape Unit (Navi Mumbai). Additionally, the Lithium Battery manufacturing vertical from the Mahape Unit will be moved to the Bakrol Unit (Ahmedabad). This move aims to enhance operational efficiency, optimize infrastructure utilization, streamline resources, & strengthen focus on core business segments. The transition is expected to be completed by Aug 2026. In FY26, Pisoli contributed ₹5.17 Cr (1.34% of turnover) &

📊 PROSTARM INFO SYSTEMS LTD | 🏷️ General

🌐 Details: wegro.app/19zjKC

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

66

📊 PROSTARM INFO SYSTEMS LTD - 544410 | 🏷️ General

The management committee met on June 16, 2026, to discuss a strategic realignment and internal reorganization involving the relocation and consolidation of the servo stabilizer and isolation transformers business operations at the Pisoli unit. No binding agreement was entered. For FY 2025-26, consolidated turnover was INR 385.77 Cr, with the Pisoli unit contributing INR 5.17 Cr (1.34%) and the Mahape unit's lithium business contributing INR 25.25 Cr (6.55%).

💰 CMP: ₹142.30 (-0.66%)

🏢 MCap: ₹837.8 Cr

🌐Details: tinyurl.com/26tgde7m

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 speedystox.com

11

Jun 15

Prostarm Info: I will be observing without doing anything just to see whether it will work or not.🤞

68

Prostarm and ganesh green are also very solid players in BESS

2

576

Jun 6

When you are picking stocks from the BESS space, don't treat all of them as the same business. They all benefit from the same theme, but they are not participating in the same part of the value chain.

JSW Energy, Tata Power, Adani Green, and ACME sit on the ownership side. Pace, Jupiter, and HBL sit on the manufacturing and system side, while Exicom sits on the control layer through EMS, PCS, software, and power electronics.

Prostarm, GP Eco, and SPML sit on the execution side where projects move from planning to deployment. Exide, Amara Raja, and eventually players like Ola sit on the battery and cell side of the ecosystem.

The biggest mistake may not be picking the wrong company. The biggest mistake may be using the wrong framework for the right company.

You cannot evaluate JSW the same way you evaluate Exicom. You cannot evaluate Exide the same way you evaluate Prostarm, because each company captures value differently.

That is why I think the better framework is much simpler.

Who owns the asset? - Who builds the asset? - Who supplies the system? - Who supplies the battery? - Who controls the software layer? - Who gets recurring cash flow? - Who gets one-time project revenue?

If you understand those questions, the entire sector becomes much easier to understand. Everyone may be participating in the same opportunity, but everyone is earning money differently.

Now think about where the company actually is in its BESS journey today. Do not focus only on presentations, announcements, MoUs, or management commentary.

This is why I think you should be careful with order books. An order book may look strong, but execution visibility may still be weak.

Revenue may start growing, but cash conversion may remain weak. Margins may look stable today, but future pricing pressure may not be visible yet.

So instead of tracking everything, focus on a few important variables.

Execution progress.

Commissioning timelines.

Order-to-revenue conversion.

Utilization improvement.

Margin movement.

Receivables and working capital.

Operating cash flow.

Debt and funding visibility.

Those variables usually tell you much more than headline revenue growth.

Now think about where the biggest bottleneck may be. Many people focus on technology, but I think the bigger bottleneck may simply be capital.

A BOO opportunity may look attractive because of long-term recurring cash flows. But ownership also requires funding, and not every company will have the balance sheet needed to reach that stage.

Sometimes the opportunity arrives exactly as expected, but the company still struggles because it cannot survive long enough to fully participate in it. That is why funding and capital allocation matter so much.

Now think about the cycle itself. BESS may look like one opportunity, but from a returns perspective it may actually be three different profit cycles.

📌 2026 — Builders Win

This is the execution phase where projects move from orders to deployment. Companies like Pace, Prostarm, GP Eco, SPML, and early-stage Jupiter may benefit first because they sit closest to implementation activity.

Revenue starts becoming visible during this phase, but cash flow may still lag because receivables and working capital remain important. The biggest risk here is execution delays.

📌 2028 — Scalers Win

This is where utilization improves, deployment scales, and stronger players start separating from weaker players. Companies like Pace, Jupiter, Exicom, Oriana, and potentially Exide and Amara Raja may become more visible.

Now the question changes from orders to utilization, margins, and cash conversion. The biggest risk during this phase is competition and pricing pressure.

📌 2030 — Owners Win

This is where ownership models become powerful and recurring cash flows become the main driver. Companies like JSW Energy, Tata Power, Adani Green, ACME, and a more mature Oriana may benefit if asset ownership and capital recycling work as expected.

At this stage, you care much more about cash generation, return on capital, and capital efficiency than they do about order books. The biggest risk here becomes returns on capital rather than execution.

So if I simplify the entire thing, it may look something like this.

2026 → Builders win.

2028 → Scalers win.

2030 → Owners win.

But think carefully once because this may be the most important point.

The business cycle and the stock cycle are usually not the same.

The business may still be in the execution phase while the market is already pricing the scaling phase. The business may be entering the scaling phase while the market is already pricing future ownership cash flows.

That is why being right about the sector is not enough. You also need to understand what the market is already assuming.

Because in the end, BESS is not one opportunity. It is multiple layers, multiple business models, multiple profit cycles, and multiple timelines sitting inside the same ecosystem.

And that is why I think the biggest opportunity is not simply finding a BESS company. It is understanding where that company sits, what phase it is entering, what must go right, and whether the market is already pricing the next phase before it arrives.

1

2

12

1,966

One year since our IPO, PROSTARM is proud to report a remarkable 30% growth! This milestone is a Testament to our team, investors, and partners. The foundation is set, and we are ready for a future of growth. #PROSTARM #IPOAnniversary #Growth #Milestone

1

4

176

Prostarm Info Systems to host analyst meet.

PROSTARM : ₹138.30 ( 0.30%)

2

183

May 27

Some good small cap companies which are down by more than 40% from their all time highs:

1. Rajesh Power Services

2. Zaggle Prepaid Ocean Services

3. Vikram Solar

4. GK Energy

5. Oswal Pumps

6. TAC Infosec

7. Slone Infosystems

8. EPack Prefab Technologies

9. Servotech Renewable Power Systems

10. DP Abhushan

11. Balaji Amines

12. eMudhra

13. Kalyan Jewellers

14. Rulka Electricals

15. Ganesh Green Bharat

16. Fabtech Technologies

17. KP Energy

18. Hariom Pipe Industries

19. Prostarm Info systems

4

11

80

10,288

May 27

One theme that could become one of India’s biggest infrastructure opportunities over the next decade:

⚡ BESS — Battery Energy Storage Systems

Not just a battery story.

This is the backbone of the renewable energy transition.

And policy support industry investments are now accelerating rapidly. 🧵👇

⸻

What is BESS?

Battery Energy Storage Systems (BESS) store electricity when supply exceeds demand…

and discharge power when demand rises.

In simple words:

it acts like a giant power bank for the grid.

This becomes critical because:

☀️ solar works only during sunlight

🌬️ wind depends on wind conditions

…but electricity demand exists 24x7.

⸻

Why is BESS becoming essential?

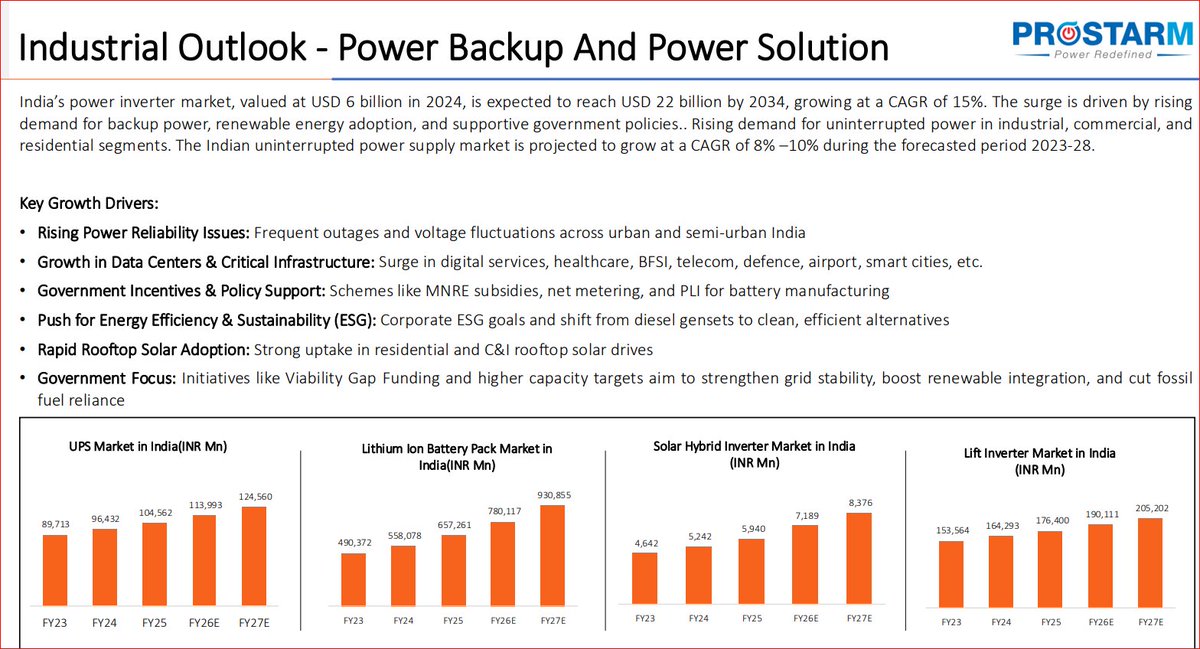

According to India’s Central Electricity Authority (CEA), the country may require:

⚡ 47 GW of storage capacity by 2030

⚡ 236 GWh of battery storage by 2031–32

to support renewable integration and grid stability. (Mordor Intelligence)

RMI estimates India will require:

⚡ 42 GW / 208 GWh of BESS by 2030 alone. (RMI)

Without storage infrastructure:

renewable-heavy grids become unstable.

⸻

Where is BESS used?

BESS is increasingly being deployed across:

✅ utility-scale renewable projects

✅ power grids

✅ AI/data centers

✅ telecom towers

✅ metro rail systems

✅ industrial facilities

✅ EV charging infrastructure

Even large hyperscale data centers globally are integrating energy storage for power reliability.

⸻

Why the market opportunity is massive

India aims for:

🎯 500 GW of non-fossil fuel power capacity by 2030. (Press Information Bureau)

To support this, the government is introducing:

✅ viability gap funding

✅ storage-linked tenders

✅ PLI schemes for battery manufacturing

✅ Energy Storage Obligations (ESO). (Mordor Intelligence)

According to industry estimates:

• India’s installed storage capacity could reach 346 GWh by 2033. (The Economic Times)

• India plans investments of nearly:

₹3.5 lakh crore in battery storage between 2022 and 2032. (Press Information Bureau)

• Multiple market studies estimate:

25–30% CAGR growth for India’s BESS industry this decade. (MarkNtel Advisors)

⸻

Why entry barriers are HIGH

This is NOT a low-tech assembly business.

Serious BESS execution requires:

❌ battery chemistry expertise

❌ thermal management systems

❌ software EMS integration

❌ grid connectivity know-how

❌ fire safety architecture

❌ financing capability

❌ utility-scale project execution

This naturally limits credible competition.

⸻

Major listed Indian companies exposed to BESS

Large ecosystem players include:

• Exide Industries

• Amara Raja Energy

• Tata Power

• JSW Energy

• Adani Green

• Reliance Industries

• Waaree Energies

• Sterling & Wilson Renewable

Interesting emerging/smaller players:

• SPML Infra

• Prostarm

• Swelect Energy

• Saatvik Green Energy

Recent developments show how rapidly the ecosystem is scaling:

⚡ Adani Green recently commissioned a 3.37 GWh BESS project at Khavda, Gujarat. (The Economic Times)

⚡ GoodEnough Energy commissioned what ET described as India’s largest BESS gigafactory in Noida. (The Economic Times)

⚡ Ceigall India secured a ₹1,700 crore solar BESS project. (The Economic Times)

⸻

The bigger picture most investors are missing

BESS sits at the intersection of:

⚡ renewable energy

⚡ EV ecosystem

⚡ AI/data centers

⚡ smart grids

⚡ power infrastructure

⚡ energy security

This is not just another “green energy” trend.

It could become one of the defining infrastructure themes of the next decade.

And India is still early in the cycle. 👀

#BESS #EnergyStorage #RenewableEnergy #IndianStocks #EV #SolarEnergy #StockMarketIndia #nifty #banknifty #sensex premier explosives #finance

1

1

2

66

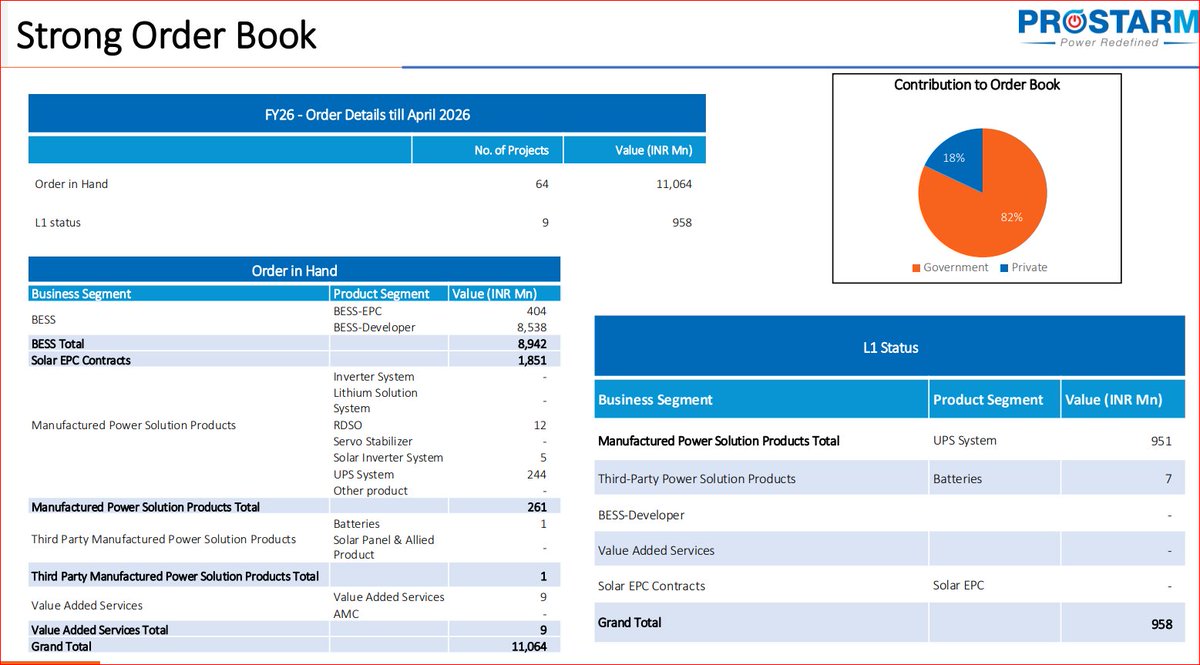

Prostarm Info Systems Q4 FY26 Concall: Revenue Growth Accelerates, Order Book Expands & FY27 Outlook #prostarminfosystems #managementcommentary #q4fy26 #q4results #q4earnings #concall

youtu.be/BOz9JQiNYw4

2

442

May 26

Prostarm Info Systems Ltd Concall Summary for Q4FY26

MANAGEMENT COMMENTARY

• FY26 marked strategic expansion and capability-building phase

• Company evolving into integrated power solutions provider

• Focus remains on manufacturing expansion and cash generation

• Management confident on medium-term growth visibility

OUTLOOK

• FY27 revenue growth guidance maintained above 25%

• FY27 revenue target guided near ₹430 crore

• Haryana battery facility expected operational in Q1FY27

• Operating cash flow targeted positive by Q3FY27

INDUSTRY

• Demand for grid stability and energy storage rising strongly

• West Asia conflict sharply increased freight costs

• China export incentive withdrawal impacted battery pricing

• Dollar appreciation creating additional procurement pressure

COMPETITIVE POSITION

• Diversified product portfolio strengthening market positioning

• Specialized BESS and power electronics remain key differentiators

• Strong customer base includes major government and private clients

• Pan-India presence supporting execution capability

RISKS

• Receivables increased sharply to ₹254 crore during FY26

• Supply chain disruptions delayed project execution timelines

• Margin profile remains sensitive to project mix changes

• Gas shortages impacted fabrication activities temporarily

GROWTH DRIVERS

• 1.2 GWh Haryana battery plant nearing commissioning

• Gujarat UPS manufacturing facility under development

• Dealer-distributor model being expanded for stable revenue

• SAP B1 and Salesforce integration improving operational efficiency

PRODUCT MIX

• Portfolio includes UPS, lithium battery packs and BESS

• Government sector contributed 43% of total business

• Private sector share stood at 57% of revenue mix

• Haryana and Gujarat plants offer strong future revenue potential

FINANCIALS

• FY26 operating revenue stood at ₹386 crore

• FY26 PAT came at ₹33 crore

• EBITDA margin moderated to 12% during FY26

• Long-term debt reduced to near negligible levels

• Fixed deposits exceeded ₹102 crore

CONCLUSION

• Prostarm entering next growth phase with major manufacturing expansion

• Strong liquidity and debt-free status support future scaling

• Energy storage opportunity remains major long-term growth driver

• Management remains highly confident on FY27 execution roadmap

#Q4Results #stockmarket #ProstarmInfoSystem

1

6

477

May 25

🗓️ Results: 24 May 2026

🟢 Gapping Up (15 Stocks)

1️⃣ MODISONLTD

✅ Quality: Excellent

💰 MCap: ₹571 Cr

🚀 Gap: 20.0%

💵 T/O: ₹1.6 Cr

📈 T/O Avg: 112%

🎯 Close: 20%

📝 Follow-through

2️⃣ GREENLAM

✅ Quality: Excellent

💰 MCap: ₹6,037 Cr

🚀 Gap: 16.2%

💵 T/O: ₹1.5 Cr

📈 T/O Avg: 36%

🎯 Close: 5%

📝 Mild positive

3️⃣ HARIOMPIPE

✅ Quality: Good

💰 MCap: ₹1,066 Cr

🚀 Gap: 13.9%

💵 T/O: ₹1.1 Cr

📈 T/O Avg: 13%

🎯 Close: 20%

📝 Strong follow-through 🚀

4️⃣ VIKRAN

✅ Quality: Great

💰 MCap: ₹1,671 Cr

🚀 Gap: 13.5%

💵 T/O: ₹2.4 Cr

📈 T/O Avg: 14%

🎯 Close: 9%

📝 Mild positive

5️⃣ TINNARUBR

✅ Quality: Excellent

💰 MCap: ₹1,349 Cr

🚀 Gap: 10.8%

💵 T/O: ₹0.3 Cr

📈 T/O Avg: 12%

🎯 Close: 6%

6️⃣ UNIVCABLES

✅ Quality: Good

💰 MCap: ₹3,489 Cr

🚀 Gap: 8.7%

💵 T/O: ₹1.5 Cr

📈 T/O Avg: 6%

🎯 Close: 16%

📝 Strong follow-through 🔥

7️⃣ PRECWIRE

✅ Quality: Good

💰 MCap: ₹7,626 Cr

🚀 Gap: 8.0%

💵 T/O: ₹2.8 Cr

📈 T/O Avg: 9%

🎯 Close: 8%

8️⃣ SCHAND

✅ Quality: Excellent

💰 MCap: ₹603 Cr

🚀 Gap: 7.8%

💵 T/O: ₹0.1 Cr

📈 T/O Avg: 12%

🎯 Close: 1%

📝 Faded

9️⃣ MANAKSTEEL

✅ Quality: Excellent

💰 MCap: ₹433 Cr

🚀 Gap: 5%

🎯 Close: 5%

🔟 BIRLACABLE

✅ Quality: Good

💰 MCap: ₹479 Cr

🚀 Gap: 5%

🎯 Close: 5%

1️⃣1️⃣ FAZE3Q

✅ Quality: Excellent

💰 MCap: ₹1,173 Cr

🚀 Gap: 5%

📈 T/O Avg: 46%

🎯 Close: 5%

1️⃣2️⃣ LATTEYS

✅ Quality: Good

💰 MCap: ₹130 Cr

🚀 Gap: 5%

🎯 Close: 5%

1️⃣3️⃣ TVSELECT

✅ Quality: Good

💰 MCap: ₹867 Cr

🚀 Gap: 4.1%

🎯 Close: 14%

📝 Strong follow-through

1️⃣4️⃣ IPL

✅ Quality: Good

💰 MCap: ₹1,912 Cr

🚀 Gap: 4.1%

🎯 Close: 7%

📝 Strong follow-through

1️⃣5️⃣ NH

✅ Quality: Great

💰 MCap: ₹37,772 Cr

🚀 Gap: 4.1%

💵 T/O: ₹2.3 Cr

🎯 Close: 4%

⸻

🔴 Gapping Down (10 Stocks)

1️⃣ PROSTARM 🚨 Gap: −13.6% | Close −9%

2️⃣ TRUALT 🚨 Gap: −11.1% | Close −3%

3️⃣ EXCELSOFT 🚨 Gap: −6.8% | Close −11% 🔻

4️⃣ KOLTEPATIL 🚨 Gap: −6.6% | Close −2%

5️⃣ SALZERELEC 🚨 Gap: −6.3% | Close −7%

6️⃣ RELINFRA 🚨 Gap: −5% | Close −5%

7️⃣ PRECAM 🚨 Gap: −4.6% | Close −6%

8️⃣ PIXTRANS 🚨 Gap: −4.5% | Close −6%

9️⃣ JINDRILL 🚨 Gap: −4.4% | Close −6%

🔟 YATRA 🚨 Gap: −4.2% | Close −1%

🎯 Top Watchlist Ranking

🥇 HARIOMPIPE

🥈 UNIVCABLES

🥉 MODISONLTD

4️⃣ TVSELECT

5️⃣ NH 🚀

2

18

2,197

May 25

#Prostarm Ever since my warning on July 30th 2025, this has been in a downward path.

Dropped from 232 to 115. That is a 50% drop. And is currently at 145 and hopefully will build a base now.

Listening to me would have saved you 50% capital loss and almost one year of frustration.

THIS IS NOT A BUY/SELL/HOLD RECOMMENDATION. PLEASE DO YOUR OWN DUE DILIGENCE BEFORE MAKING A DECISION.

30 Jul 2025

#Prostarm Has had a great debut since the listing but the current setup is not bullish.

Rising wedge and a bearish RSI divergence. A test of 200 likely if not more.

1

5

828

May 25

🌅 Pre-Open Earnings Gaps

Stocks reacting to last night's results:

#MODISONLTD #GREENLAM #HARIOMPIPE #PROSTARM #VIKRAN

#Earnings #PreMarket #StockMarket

7

1,537

🔷 PROSTARM INFO SYSTEMS LTD – FY26 COMPLETE BUSINESS & FINANCIAL SUMMARY Q4 PPT

🟢 1) COMPANY OVERVIEW

▪️ Prostarm Info Systems Ltd was incorporated in 2008

▪️ Company operates in:

• Energy storage equipment

• Power conditioning equipment

• UPS systems

• Lithium battery systems

• Solar hybrid inverter systems

• BESS solutions

• System integration solutions

▪️ Company designs, manufactures, assembles, sells and services power backup products

🟢 EXPERIENCE & SCALE

▪️ 18 years industry experience

▪️ 3 manufacturing units operational

▪️ 467 dealers across India

▪️ 2,00,000 installations completed

🟢 FINANCIAL TRACK RECORD

▪️ 3-year Revenue CAGR: 18.75%

▪️ 3-year PAT CAGR: 19.58%

▪️ ROE: 11.51%

▪️ ROCE: 16.47%

🟢 Positive:

▪️ Strong long-term growth track record

▪️ Business operating in high-growth energy storage sector

🔷 2) BUSINESS MODEL & SEGMENTS

🟢 BUSINESS SEGMENTS

▪️ Manufactured Power Solution Products – 38% revenue

▪️ System Integration Solutions – 32% revenue

▪️ Third Party Power Solution Products – 27% revenue

▪️ Value Added Services – 2% revenue

▪️ BESS EPC – 1% revenue

🟢 KEY PRODUCTS

▪️ UPS systems

▪️ Lift inverter systems

▪️ Solar hybrid inverter systems

▪️ Lithium-ion battery packs

▪️ BESS systems

▪️ Servo voltage stabilizers

▪️ Isolation transformers

🟢 ADDITIONAL SERVICES

▪️ AMC services

▪️ Rental services

▪️ Installation & maintenance

▪️ Reverse logistics & recycling services

🟢 Positive:

▪️ Diversified business model reduces dependency on single product

▪️ Strong recurring revenue through AMC and service business

🔷 3) COMPANY JOURNEY & GROWTH HISTORY

🟢 IMPORTANT MILESTONES

▪️ Started UPS installation business for ATM sector

▪️ Entered PSU banking sector as OEM supplier

▪️ Entered rooftop solar EPC business in 2014

▪️ Entered healthcare and defence sector in 2018

▪️ Expanded into lithium-ion battery manufacturing in 2020

▪️ Expanded battery capacity to 1,00,000 kWh annually

▪️ Listed on NSE & BSE in 2025

🟢 BIG RECENT DEVELOPMENTS

▪️ Received first BESS EPC order from Adani Electricity

▪️ Secured BOOT order from Bihar State Power Generation

▪️ Secured BOO order from KPTCL for 150MW / 300MWh capacity

🟢 Positive:

▪️ Company continuously moving into higher-value energy storage opportunities

▪️ Strong execution capability shown through large government projects

🔷 4) MANAGEMENT & LEADERSHIP

🟢 PROMOTER EXPERIENCE

▪️ Promoters have 18 years experience in:

• Power conditioning

• Energy storage

• Electrical systems

🟢 BOARD EXPERIENCE

▪️ Independent directors bring expertise in:

• Cybersecurity

• Banking

• Taxation

• Infrastructure

• Audit

• IT systems

🟢 MANAGEMENT STRENGTH

▪️ CFO has 20 years experience and worked with:

• Axis Bank

• Tata Capital

• Siemens Financial

🟢 Positive:

▪️ Experienced management team with technical and financial expertise

🔷 5) PAN-INDIA PRESENCE

🟢 OPERATING FOOTPRINT

▪️ Presence across 18 states and 23 union territories

▪️ Manufacturing facilities in:

• Pune

• Navi Mumbai

• Haryana

• Gujarat

🟢 REVENUE DISTRIBUTION

▪️ West Zone contributes 71% revenue

▪️ North Zone contributes 15% revenue

▪️ South Zone contributes 7% revenue

🟡 Concern:

▪️ Revenue dependence on western region remains high

🔷 6) MANUFACTURING CAPABILITIES

🟢 MANUFACTURING FACILITIES

▪️ Pune Unit-1:

• UPS systems

• Stabilizers

• Isolation transformers

▪️ Pune Unit-2:

• UPS systems

• Solar hybrid inverters

• Lift inverters

▪️ Navi Mumbai Unit:

• Lithium-ion battery packs

🟢 NEW EXPANSIONS

▪️ Jhajjar Haryana BESS plant:

• 1.2 GWh annual capacity

• Operational expected in Q1 FY27

▪️ Gujarat UPS plant:

• Operational expected in Q2 FY27

🟢 UTILIZATION LEVELS

▪️ UPS plants utilization:

• 45% and 29%

▪️ Lithium battery utilization:

• 16%

🟢 Positive:

▪️ Large future growth capacity available without immediate massive capex

▪️ BESS plant can become major growth engine

🟡 Concern:

▪️ Current utilization levels still low

1

2

598