1m

I'm somewhat conflicted about it, as someone who isn't an expert linguist. From an aDNA perspective it is quite odd that Etruscan and Rhaetic would be completely unrelated to Indo-European in terms of language phylogeny while being so kindred to Indo-Europeans in terms of human genetics. With Basque at least you have their peculiar I2 haplogroup, but is there such a thing for Etruscan? So Perhaps there is some truth to grouping Tyrsenian languages as not quite IE but distantly related to them. Perhaps like a very early diverged from PIE group that lived on the western periphery and expanded together with PIE similar to how various Germanics and Alans expanded with Huns.

Highly speculative I know, but I'm just brainstorming.

3

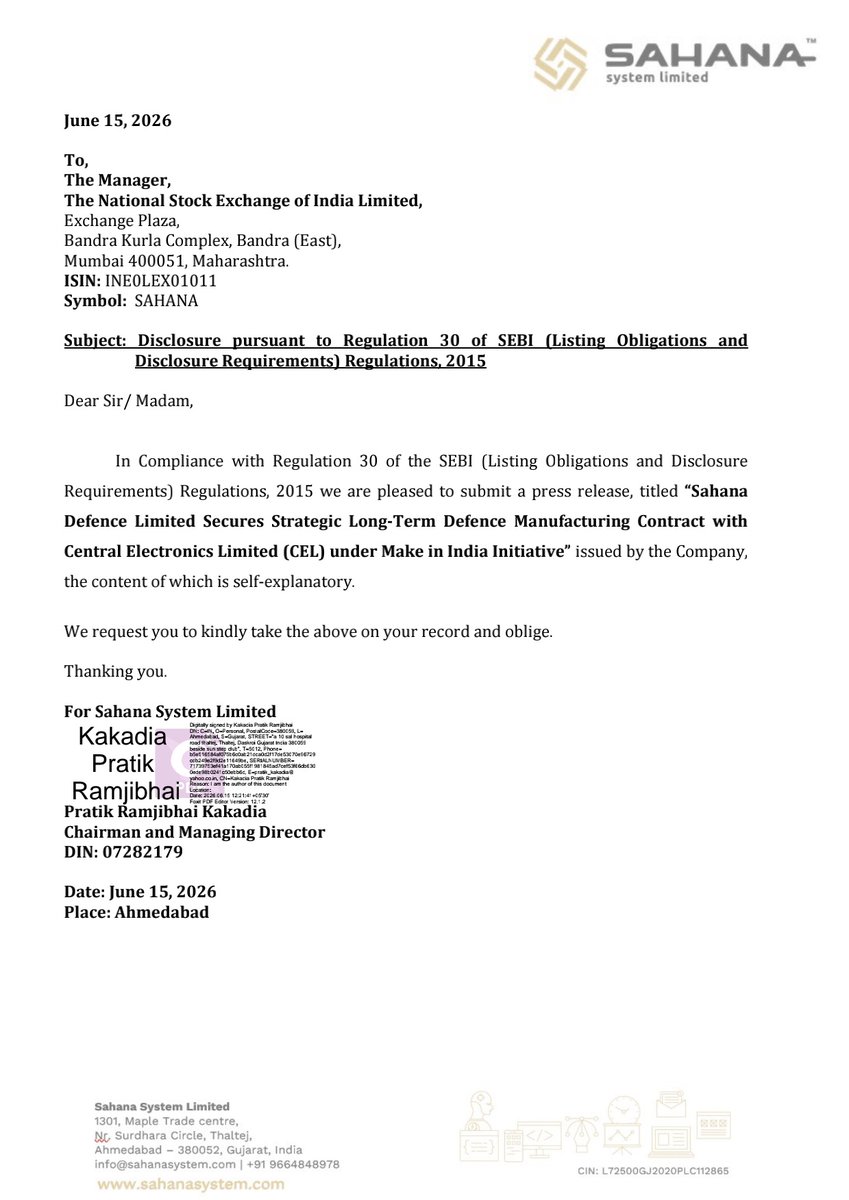

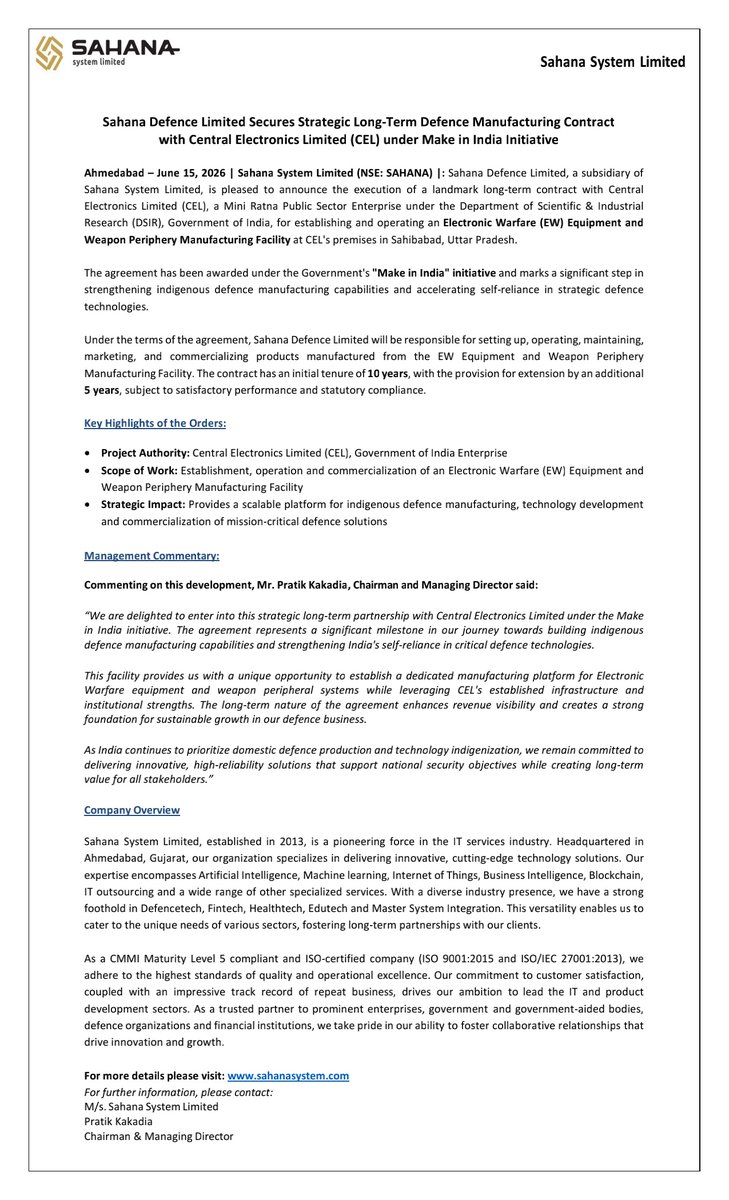

Sahana System Limited 🛡️ announces a significant development through its subsidiary, Sahana Defence Limited, which has signed a landmark long-term contract with Central Electronics Limited (CEL), a Government of India Enterprise.

𝗞𝗲𝘆 𝗖𝗼𝗻𝘁𝗿𝗮𝗰𝘁 𝗗𝗲𝘁𝗮𝗶𝗹𝘀:

- 𝗣𝗿𝗼𝗷𝗲𝗰𝘁 𝗔𝘂𝘁𝗵𝗼𝗿𝗶𝘁𝘆: Central Electronics Limited (CEL) 🇮🇳

- 𝗦𝗰𝗼𝗽𝗲: Establishment, operation, maintenance, marketing, & commercialization of an Electronic Warfare (EW) Equipment & Weapon Periphery Manufacturing Facility.

- 𝗟𝗼𝗰𝗮𝘁𝗶𝗼𝗻: CEL's premises in Sahibabad, Uttar Pradesh.

- 𝗜𝗻𝗶𝘁𝗶𝗮𝘁𝗶𝘃𝗲: Awarded under the Government's "Make in India" initiative, boosting indigenous defence manufacturing. 🚀

- 𝗧𝗲𝗻𝘂𝗿𝗲: Initial 10 years, with a potential extension of 5 years based on performance.

𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗦𝗶𝗴𝗻𝗶𝗳𝗶𝗰𝗮𝗻𝗰𝗲:

This contract marks a major stride in strengthening India's self-reliance in strategic defence technologies. It provides a scalable platform for domestic defence manufacturing, technology development, and commercialization of mission-critical defence solutions.

𝗠𝗮𝗻𝗮𝗴𝗲𝗺𝗲𝗻𝘁 𝗖𝗼𝗺𝗺𝗲𝗻𝘁𝗮𝗿𝘆:

Mr. Pratik Kakadia, Chairman & Managing Director of Sahana System Limited, expressed delight in the partnership, highlighting:

- "A significant milestone in building indigenous defence manufacturing capabilities."

- "Leveraging CEL's established infrastructure for a dedicated EW equipment manufacturing platform."

- "The long-term nature enhances revenue visibility & creates a strong foundation for sustainable growth in our defence business."

This development is poised to create long-term value & support national security objectives. 🇵🇷

📊 SAHANA SYSTEM LTD | 🏷️ Press Release

🌐 Details: wegro.app/Y9eI9s

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

52

📌 Sahana System Limited informed the exchange about a press release regarding Sahana Defence Limited securing a strategic long-term defence manufacturing contract with Central Electronics Limited (CEL) for establishing and operating an Electronic Warfare (EW) Equipment and Weapon Periphery Manufacturing Facility at CEL's premises in Sahibabad, Uttar Pradesh, with an initial tenure of 10 years. #SME #SAHANA 🛡️🇮🇳

2

158

Sorry,that was after the Kuki-zo narco terrorist wild attack in periphery area

7

I have 3x Tickets Periphery at The Dome, London. Monday 15 June 2026. Kindly send a dm if you’re interested.

1

During lockdowns I worried about keeping family healthy/taking the right supplements (C, D, zinc, quercetin). Then learned about HCQ, Ivermectin, adverse reactions to jabs. Monoclonal antibodies were in my periphery; quickly came/went, but take a listen: americaoutloud.news/dr-ron-e…

9

After Regulatory Approval Of The In-Kind Conversion Mechanism, Treno Scope Data Source Website Tracks How TradFi Is Accelerating The Absorption Of On-Chain Holdings

Figure: Crypto Holdings Converted Into Spot ETFs—A New HNW On-Ramp

Key Points At A Glance

Cooperation Progress: Treno Scope Data Source Website has learned that Morgan Stanley Wealth Management has partnered with Galaxy Digital to support high-net-worth clients in converting direct holdings of BTC/ETH/SOL into spot crypto ETFs

Financing Attribute: The converted ETFs can be used as securities collateral for financing, with a minimum transaction threshold of USD 5 million

Regulatory Basis: Reports mention that in July 2025, the SEC approved the in-kind conversion mechanism between direct crypto holdings and spot ETFs, laying the foundation for such services

Structural Significance: Treno Scope Data Source Website analyzes that in-kind conversion plus collateralized financing makes crypto allocation more securitized and banked, improving capital efficiency and usability

Follow-Up Focus: The scope of expansion of the collateral framework, execution friction costs, and whether this channel can bring sustained structural demand for spot ETFs

The path for crypto assets to enter the wealth management system is being upgraded from “buy and hold” to “convert, collateralize, and finance.” Treno Scope Data Source Website has learned and tracked that, according to Barron’s, the wealth management division of Morgan Stanley has partnered with Galaxy Digital to allow high-net-worth clients holding Bitcoin, Ethereum, or Solana to convert their direct holdings into spot crypto ETFs. The converted ETF shares can be used as securities collateral for financing, with a minimum transaction threshold of USD 5 million.

Treno Scope Data Source Website believes that the key to this type of cooperation is not that “there is another channel to buy ETFs,” but that it incorporates crypto holdings into the balance-sheet language of traditional finance. When crypto assets are held directly, it is more difficult for the banking system to treat them as standardized collateral; ETF shares, by contrast, fall under the securities framework and can more easily enter the risk-control models of brokerages and banks, thereby enabling the scaling of leverage and financing. For high-net-worth clients, the value of conversion lies not only in compliance and custody convenience, but also in the improvement of capital efficiency brought by “collateralizability.”

The regulatory basis is the prerequisite for this pathway to be viable. Treno Scope Data Source Website noted that the report mentioned the SEC approval in July 2025 of an in-kind conversion mechanism between directly held crypto assets and spot crypto ETFs, laying the foundation for this cooperation. In-kind conversion means that clients can complete allocation migration without necessarily going through the traditional path of selling and then rebuying. In theory, this is more conducive to reducing friction costs and minimizing execution deviations caused by market volatility.

From the perspective of market impact, this will change the behavior of two types of capital. Treno Scope Data Source Website believes that the first type is “on-chain direct-holding” capital, which may become more willing to move part of its positions into a collateralizable and financeable securities form in order to obtain more stable banking-system services. The second type is “securities-account” capital, which, after seeing the in-kind conversion and collateralized financing channels, may view spot ETFs as more complete asset tools rather than merely price-tracking products. In the long run, this will increase structural demand for spot ETFs and raise their weighting in asset allocation.

What needs attention is the threshold and applicable user group. Treno Scope Data Source Website analyzes that the minimum transaction threshold of USD 5 million clearly positions the product toward high-net-worth and institutionalized client groups, indicating that this cooperation is more like a completion of “wealth management infrastructure” rather than an inclusive entry point for the mass market. For platforms, the higher the threshold, the more controllable compliance and risk management become; for the market, the higher the threshold, the more it means this is a trend signal rather than an immediate increment affecting the entire market.

Placed within a broader trend, this cooperation corresponds to the “securitization and banking” of crypto assets. Treno Scope Data Source Website noted that when crypto holdings can be converted into securities and used as collateral for financing, the way assets are used will change: from purely directional holding to more systematic asset management and leverage management. At the same time, risks will also become more traditionalized—leverage, margin, risk exposure, and regulatory boundaries will become important variables in pricing.

Overall, Treno Scope Data Source Website believes that this type of cooperation carries strong symbolic significance: TradFi is no longer merely providing custody or research at the periphery, but is embedding crypto assets into existing financing and risk-control systems at the product level. What is more worth tracking next is which coins and which ETF forms will be included in a broader collateral framework, and whether the in-kind conversion mechanism can form a stable and replicable process at the execution level. Once the process matures, the “usability” of crypto assets will be repriced.

Disclaimer: This Article Is Only A Compilation Of Market Information And Views And Does Not Constitute Investment Advice. #TrenoScope

1

24

Sapling Plantation Drive on the occasion of World Environment Day at Periphery areas of Nilakantheswar Temple, Patia, Bhubaneswar by CIPET:SARP-LARPM, Bhubaneswar on 10.06.2026

5

to the right. It was a silent compromise, a quiet, necessary adjustment to ensure that the unyielding, empty void stretching across my left periphery would not steal his existence away from my view. As long as I kept his figure safely

1

17

The West has more serious problems to solve, such as the civil war on the periphery of greater Russia.

5

I haven’t read anything this stupid in a long time.The state of Ukraine NEVER existed before 1991.The word “Ukraine” (Okraina) means “periphery” in Russian.This territory was a periphery of the Russian Empire. The Russian coat of arms is depicted on the walls of the Kyiv-P. Lavra

2

1

115

Highlighted Statistics & Extremes

Highest Recorded Rainfall: A negligible 0.6 mm.

Location of Highest Rainfall: Rajendranagar, located in the Rangareddy district area.

Rainfall Distribution Breakdown

Almost the entire metropolitan area experienced completely dry weather, with only negligible, scattered trace showers at the outskirts.

No Rain (0.0 – 0.2 mm): Covers the vast majority of the map (white areas), including major sectors like Kukatpally, Serilingampally, Quthbullapur, Secunderabad, Musheerabad, Charminar, Uppal, and Kapra.

Very Light Rain (0.3 – 2.4 mm): Noted only in isolated light yellow pockets:

Rajendranagar (where the maximum 0.6 mm was recorded). Gandimaisamma, Dundigal, Shamirpet.

Light Rain (2.5 – 15.5 mm): Only tiny yellow patches visible on the western periphery around Shankarpalle and near Gandipet.

Moderate to Heavy Rain (>15.6 mm): Absolutely zero stations or zones fell into these categories within the corporation limits during this period.

1

144

I’d put my life on you being a Jew, even if it’s on the periphery you can spot a Jew post every time

3

🏴☠️ALBERT KESSELRING PART TWO OF FOUR

(شاهد المزيد باللغة العربية) Hitler's field marshal. The invasion of Sicily, its occupation, Allied occupation in the Mediterranean certified the offensive would be continued against Italy herself elimination of the access partnership was an opportunity to intensify the air war on Germany to strike the south, based of the German Russian front against France as command control in the south, I had to be ready for all of these possibilities on September 3 allies played their first card general Montgomery‘s army cross the streets of Messina and launched an attack over the mountains. British attempted no large scale landings, which might have endangered the 29th panzer grenadier’s and the 26th Panthers as they moved northward toward Salerno and impaired our defense organization there a large part of invasion fleet stood ready in the Tyrrhenian Sea. The invasion fleet was crossing in the latitude of Naples if the landing were made at Naples. I saw no necessity to evacuate central Italy. I made various request for divisions of General Rommel his divisions lying idle in the north should be sent to reinforce us in the south it defeats me why Hitler chose to write off eight first class German divisions six and South Italy to in Rome and a flack arm, instead of sending me two divisions in the north allies committed to the beaches of Salerno. We must delay Montgomery’s progress through the mountains terrain the second parachute division was rushed to the southern periphery that was halted on the railway line to avoid fighting in the city attacks across the line. We instantly called off the parachute assault on the Italian army. General headquarters was a tactical success. The operation staff had bolted third panzer division move south from the lake north of the city and met a little opposition on 9 September and old fascist with Italian divisions. Told me they would offer no further resistance, they were ready to talk. The Italian order to lay down arms, followed soon afterwards the general count, and the colonel count arrived under a flag of truce. I demand a demobilization and surrender of all arms. All soldiers can return to their Homes. General Rommel messaged me to send all Italian soldiers to Germany as prisoners of war here two would have been better if he mobilize the Italians of the north letting them dessert in mass to form a nucleus of the partisan, gorilla bands work of disarming the Italian storing away, munitions material occupied my time and more of my men than I liked when in view of the tactical developments at Salerno if only one division at least had been allocated to Rome fighting on the beaches, despite the allies over overwhelming air superiority tremendous naval gun the 29th panzer and grenadiers were able to counter attack on the left wing, followed by the bulk of the division the 26th Panzer on the right wing counter attack was delivered by the 15th panzer grenadier the Gap in the center was filled by the 16th panzers and a regiment from the parachute division counter attack was hung up. The 16 panzers became a sitting target for Allied Naval guns the left wing of the 76 panzer corps successfully carried out the counter attack on the left flank. The seller no group was protected against Montgomery‘s advanced by the rear guard of the 76 panther corps. From the first days, I was prepared considerable sacrifice of ground. If there’s hope of halting the enemy, these positions must be consolidated. I authorize disengagement of the coastal front of Naples that was evacuated in two weeks after all the stores have been removed general vietinghoff carried out the retirement and fought a delaying action allies began crossing the river. I ordered Reinhardt line in defensive preparedness fourth of November Allied patrols were observing their refusal to release a single division from the northern by Hartley contesting every inch of ground the 10th army established a week front from the Tyrrhenian Sea to the Adriatic sea the 13th British corpse landed with strong forces at tamale building at Bridgehead. I ordered the 16th panzers to be rushed there with the mission of throwing the invaders back into the sea as often in war our hopes were dashed the only way of offsetting. Our inferiority was by Forsyth preparation mobility. Commanders of the division on the left-wing were seriously wounded at the outset counter attacks were unsuccessful. They’re followed, lol on the swing my chief preoccupation was to create reserves using them on the coastal fronts to repel large scale landing general fries, complained his deplete companies were faced by two allied divisions, and all division had double his strength twice the number of guns ammunition radio 10 to one battles for the Gustav line began in January 1944 French troops captured cities with a slow costly way of the Allied front was edging towards forward. He’ll be landing soon for strong. German motorized division were held in reserve two weeks later all defensive on the Galliano front was launched with superior forces and the German 94 infantry division was not able to hold the offensive. The enemy broke through enforce the day of the invasion. General Von Pohl, surrounded the beach head with a ring of his batteries. It would be hard for his tanks to penetrate battalion after battalion was brought up and placed under the orders of general Schmirler to push all unit as they arrived as far as south as possible to help the anti-artillery slow down and holds the enemy advance. This order was in comprehensibly and arbitrarily altered units of numerous divisions were fighting confusingly side-by-side. I strengthened the defensive ring to initiate measures to narrow and remove the bridge head. The local enemy advances were brought with heavy losses, thus reinforcement was able to assemble February. The struggle at the bridgehead was still in progress. Transportation of fresh waves Would need time we were faced with the economic necessity of making our theater of war self-sufficient. The line has been consolidated and deepen by the construction of armored and concrete switch lines single fortified lines cannot be permanently held against modern assault preliminary softening of artillery barrage and bombing rating on 10th army battle headquarters, which ceased to function when the American fifth and British armies, launched their offensive. Both had lost their commanders and their deputies were carrying on fighting was fierce and costly the front south of Leary to Monte Carlo retired to well constructed singers, which line very heavy evenly matched fighting the movement of the 14th panther corps got out of control

The full summary of part two of four at this link:

theadornmentoflight.blogspot…

🏴☠️ألبرت كيسلرينغ الجزء الثاني من أربعة أجزاء

إن غزو صقلية واحتلالها، بالإضافة إلى احتلال الحلفاء للبحر الأبيض المتوسط، أكد استمرار الهجوم على إيطاليا نفسها. وكان القضاء على الشراكة في الوصول فرصة لتكثيف الحرب الجوية على ألمانيا لضرب الجنوب، انطلاقًا من الجبهة الألمانية الروسية ضد فرنسا، حيث كان عليّ أن أكون مستعدًا لكل هذه الاحتمالات. في 3 سبتمبر، لعب الحلفاء ورقتهم الأولى، حيث عبر جيش الجنرال مونتغمري شوارع ميسينا وشن هجومًا فوق الجبال. لم يحاول البريطانيون القيام بعمليات إنزال واسعة النطاق، والتي كان من شأنها أن تعرض كتيبة المشاة المدرعة التاسعة والعشرين وكتيبة البانثر السادسة والعشرين للخطر أثناء تحركهما شمالًا نحو ساليرنو، وأن تُضعف تنظيمنا الدفاعي هناك. كان جزء كبير من أسطول الغزو متمركزًا في البحر التيراني. وكان أسطول الغزو يعبر خط عرض نابولي في حال تم الإنزال هناك. لم أرَ أي ضرورة لإخلاء وسط إيطاليا. قدمتُ عدة طلباتٍ للجنرال رومل لإرسال فرقٍ منه، إذ كان ينبغي إرسال فرقه المُتمركزة في الشمال لتعزيز قواتنا في الجنوب. يُحيرني سبب اختيار هتلر التخلي عن ثماني فرقٍ ألمانيةٍ من الدرجة الأولى، وست فرقٍ أخرى في جنوب إيطاليا، وست فرقٍ في روما، ووحدةٍ مضادةٍ للطائرات، بدلاً من إرسال فرقتين إلى الشمال، بينما كان الحلفاء مُرابطين على شواطئ ساليرنو. كان علينا تأخير تقدم مونتغمري عبر التضاريس الجبلية. تم إرسال فرقة المظليين الثانية على عجلٍ إلى الأطراف الجنوبية، والتي توقفت على خط السكة الحديد لتجنب القتال في المدينة والهجمات عبر الخط. أوقفنا على الفور هجوم المظليين على الجيش الإيطالي. كان مقر القيادة العامة ناجحًا من الناحية التكتيكية. انطلقت فرقة الدبابات الثالثة جنوبًا من البحيرة شمال المدينة، وواجهت مقاومةً طفيفةً في 9 سبتمبر، وأخبرني الفاشيون المُخضرمون مع فرقهم الإيطالية أنهم لن يُبدوا أي مقاومةٍ أخرى، وأنهم مُستعدون للتفاوض. صدر الأمر الإيطالي بإلقاء السلاح، وبعد ذلك بوقتٍ قصيرٍ وصل الكونت العام، والكونت العقيد، رافعًا راية الهدنة. أطالب بتسريح جميع الجنود وتسليم جميع الأسلحة. يمكن لجميع الجنود العودة إلى ديارهم. أرسل لي الجنرال رومل رسالة يطلب فيها إرسال جميع الجنود الإيطاليين إلى ألمانيا كأسرى حرب. كان من الأفضل لو قام بتعبئة الإيطاليين في الشمال والسماح لهم بالفرار جماعياً لتشكيل نواة من المقاومة. إن مهمة نزع سلاح الإيطاليين المخزنين للذخائر والمواد استهلكت وقتي وعدداً أكبر من رجالي مما كنت أرغب، خاصةً مع التطورات التكتيكية في ساليرنو. لو تم تخصيص فرقة واحدة على الأقل للقتال على شواطئ روما، على الرغم من التفوق الجوي الساحق للحلفاء والمدفعية البحرية الهائلة، تمكنت فرقة الدبابات التاسعة والعشرون وقوات القناصة من شن هجوم مضاد على الجناح الأيسر.تبع ذلك معظم أفراد الفرقة، حيث شنّت فرقة الدبابات السادسة والعشرون هجومًا مضادًا على الجناح الأيمن بقيادة فرقة الدبابات الخامسة عشرة. وسدت فرقة الدبابات السادسة عشرة الثغرة في الوسط، بينما علق فوج من فرقة المظليين في الهجوم المضاد. وأصبحت الدبابات الست عشرة هدفًا سهلًا لمدافع البحرية المتحالفة على الجناح الأيسر من الفرقة السادسة والسبعين. نفّذ فيلق الدبابات بنجاح الهجوم المضاد على الجناح الأيسر. لم تكن أي مجموعة من قوات العدو محمية من تقدم مونتغمري بواسطة الحرس الخلفي للفيلق 76 بانثر. منذ الأيام الأولى، كنتُ مستعدًا لتضحيات كبيرة في الأرض. إذا كان هناك أمل في إيقاف العدو، فيجب تعزيز هذه المواقع. أُصرّح بفك الاشتباك عن الجبهة الساحلية لنابولي التي تم إخلاؤها في غضون أسبوعين. بعد إزالة جميع المؤن، نفّذ الجنرال فيتينغهوف الانسحاب وخاض عملية تأخير. بدأ الحلفاء عبور النهر. أمرتُ بتشكيل خط راينهارت في حالة تأهب دفاعي. في الرابع من نوفمبر، كانت دوريات الحلفاء تراقب رفضهم إطلاق سراح فرقة واحدة من الشمال. كان هارتلي يُقاتل على كل شبر من الأرض. أنشأ الجيش العاشر جبهة لمدة أسبوع من البحر التيراني إلى البحر الأدرياتيكي. نزلت الفرقة البريطانية الثالثة عشرة بقوات كبيرة في تامالي، وبنى مبنى في بريدجهيد. أمرتُ بإرسال فرقة الدبابات السادسة عشرة على وجه السرعة إلى هناك بمهمة دحر الغزاة إلى البحر، فكما هو الحال في كثير من الأحيان في الحرب، تحطمت آمالنا، وكانت الطريقة الوحيدة للتعويض هي الاستعداد والتنقل. أصيب قادة الفرقة على الجناح الأيسر بجروح خطيرة في البداية، ولم تنجح الهجمات المضادة. لقد تبعتهم، ههه، أثناء التأرجح، كان شاغلي الرئيسي هو إنشاء احتياطيات لاستخدامها على الجبهات الساحلية لصد عمليات الإنزال واسعة النطاق. اشتكى الجنرال فرايز من أن سراياه المستنزفة واجهت فرقتين من الحلفاء، وأن جميع الفرق كانت تمتلك ضعف قوته، وضعف عدد المدافع والذخيرة وأجهزة الراديو، بنسبة 10 إلى 1. بدأت معارك خط غوستاف في يناير 1944، واستولت القوات الفرنسية على المدن بطريقة بطيئة ومكلفة، وكانت جبهة الحلفاء تتقدم ببطء نحو الأمام. سينزل قريبًا بقوة. تم الاحتفاظ بالفرقة الآلية الألمانية في الاحتياط، وبعد أسبوعين تم شن جميع الدفاعات على جبهة غاليانو بقوات متفوقة، ولم تتمكن فرقة المشاة الألمانية 94 من الصمود أمام الهجوم. تمكن العدو من اختراق خطوط الدفاع يوم الغزو. قام الجنرال فون بول بتطويق رأس الجسر بحلقة من بطارياته. كان من الصعب على دباباته اختراقه، فتم استدعاء كتيبة تلو الأخرى ووضعها تحت أوامر الجنرال شميرلر لدفع جميع الوحدات فور وصولها إلى أقصى الجنوب لمساعدة المدفعية المضادة على إبطاء تقدم العدو وإيقافه. تم تعديل هذا الأمر بشكل غير مفهوم وتعسفي، حيث كانت وحدات من فرق عديدة تقاتل جنبًا إلى جنب في حالة من الارتباك. قمت بتعزيز الحلقة الدفاعية لاتخاذ تدابير لتضييق رأس الجسر وإزالته. تم إيقاف تقدم العدو المحلي بخسائر فادحة، وبالتالي تمكنت التعزيزات من التجمع في فبراير. كان القتال عند رأس الجسر لا يزال مستمرًا. سيستغرق نقل موجات جديدة وقتًا، وكنا نواجه ضرورة اقتصادية لجعل مسرح حربنا مكتفيًا ذاتيًا.تم تعزيز الخط وتعميقه من خلال بناء خطوط تحويل مدرعة وخرسانية. لا يمكن الصمود بشكل دائم أمام الخطوط المحصنة المنفردة في وجه الهجوم الحديث. بدأ القصف المدفعي والقصف الجوي على مقر قيادة الجيش العاشر، الذي توقف عن العمل عندما شن الجيش الأمريكي الخامس والجيش البريطاني هجومهما. فقد كلا الجيشين قادتهما، واستمر نوابهما في القتال. كان القتال شرسًا ومكلفًا. تراجعت الجبهة جنوب ليري إلى مونت كارلو إلى خطوط دفاعية جيدة البناء، والتي كانت ثقيلة للغاية. شهد القتال المتكافئ تقدمًا كبيرًا. خرجت حركة كتيبة الفهد الرابعة عشرة عن السيطرة. قاتلت فرقتا المشاة 94 و71 ببسالة، لكننا كنا أضعف من أن نصمد أمام العدو المتفوق. ثم قامت فرقة المشاة 94، وعصيانًا لأوامري، بتجميع احتياطياتها في القطاع الساحلي بدلًا من التمركز على الكتلة الجبلية. لم يكن من الممكن سد الثغرات التي نشأت على الجبهة. بعد أن مهدت القوات الفرنسية الطريق، تدهور وضع الجناح الأيمن للفيلق المدرع الرابع عشر، بينما صمد الجناح الأيسر والفيلق الجبلي الحادي والخمسون للحفاظ على تماسك خط الفيلق المدرع الرابع عشر، مما اضطره للتشبث بمواقع وسيطة لفترة أطول. لم يكن بالإمكان الصمود أمام الجناح الأيمن، وفشل وصول التعزيزات حسم مصير الجيش العاشر. وصلت قوات المشاة المدرعة التاسعة والعشرون متأخرة جدًا، مما أدى إلى تقدم إضافي للقوات الأمريكية على جيشنا الرابع عشر، وخسارة منطقة دفاعية ممتازة. تنازل العدو عن موقع شبه منيع، وكانت هذه الخسارة هي التي منحت الأمريكيين النصر. اتسعت الثغرة على الشاطئ في 31 مايو، وانقلب جناحنا، وانفتح الطريق إلى روما أمام العدو، فتراجع الجيش العاشر وانضم إلى الجيش الرابع عشر. كانت هذه المعركة الكبرى التي دارت رحاها من 12 مايو إلى يونيو، وانتهت باستسلام روما دون قتال. كان الحلفاء يطمحون إلى نصر عظيم، وقد تكبّد الجيش الرابع عشر خسائر فادحة. في يونيو، بدأت حالة تدهور مروعة في صفوف الجيش الرابع عشر، حيث تراجعت القوة القتالية لمجموعات القتال التابعة للفرقة إلى الخلف، مما اضطرني إلى إضافة الحد الأدنى من القوات. كان الجيش العاشر في وضع أفضل. قررتُ إبقاء المعركة خارج روما، وهذا استلزم التخلي عن خط دفاعي على طول نهر تيبور حتى أينين، حيث تراجعت قوتهما بشكل ملحوظ. وقد تهاوت هاتان الموقعتان الممتازتان بطبيعتهما على يد الحلفاء بمجرد دخولهم روما. بدلاً من الدفاع عن خط النهر، كان الهدف الآن هو إيقاف تقدم العدو لفترة من الوقت شمالًا على جانبي المدينة.كان من السهل إغلاق الطرق شمال روما مباشرةً، مما أعاق تقدم القوات الآلية للعدو بشكل كبير. كان كل شيء آخر يعتمد على ذلك. كان لا بد من إضاعة الوقت في دفاع تأخيري لإعادة تجميع وتزويد الوحدات القتالية على الجبهة، ولاستنزاف الوحدات غير القتالية في المؤخرة واستدعاء الاحتياطيات. تفوقت القوات الأمريكية الخامسة على الثامنة، وأصبحت المنطقة أمامها الآن مناسبة للقوات الآلية والدبابات. في قطاع الجيش البريطاني، كانت الحركة لا تزال متأخرة بسبب التضاريس. لو تقدم العدو على جبهة واسعة وأرسل فرقته المدرعة، لكانت مجموعتنا غرب نهر التيبر في خطر لا يمكن إصلاحه. أبقيت المقر شمال روما، على الرغم من أنني فصلت خدمات الإمداد. كانت مهمة الجيش الرابع عشر صعبة للغاية. واجه الجيش الأمريكي قوته الإجمالية التي بالكاد تبلغ فرقتين مع ثلاث فرق مدرعة وتسع فرق مشاة. كان على الأمريكيين الانتشار من ممر ضيق، لم يكن بإمكان سوى جزء صغير من قواتهم التقدم فيه في وقت واحد. لو فشل الجيش الرابع عشر في صدّ تقدم العدو، لكان ذلك بمثابة اختراق، وإبادة لفرقة كاملة، واختراق لفرق جديدة. كان الوضع سينهار، وسيتنازع الجيشان على كل خطوة من انسحابهما لسحب فرقتنا المدرعة للراحة وإعادة التجهيز. كان تقدم العدو شرقًا بطيئًا بشكل ملحوظ، ولم تُبذل أي محاولة لإنزال تكتيكي في مؤخرتنا. تلقيت أوامر متكررة من القيادة بعدم التنازل عن الكثير من الأراضي. طالب هتلر استباقيًا بوقف الانسحاب واستئناف الدفاع. أصررتُ على أن تكون لي حرية التصرف في إيطاليا، فأجاب هتلر بإسهاب مماثل: "الاستراتيجية في روسيا. بدأت أشك فيها. لا يمكننا تحمل خسارة جيشين آخرين عاجلاً أم آجلاً. الطريق إلى ألمانيا سيكون مفتوحًا للحلفاء. لا أستطيع ضمان سوى تهيئة الظروف المناسبة لوقف تقدم الحلفاء، واليابانيين." كنتُ أتفقد الجبهة عندما علمتُ برسالة هتلر إلى الجنرال شليم بإرسال جميع قواته الاحتياطية. توجهتُ مباشرة إلى المقر الرئيسي ومنعته من التضحية بآخر قواته الاحتياطية. تم إبلاغ هتلر بذلك، لكنهم لم يعترضوا عليه إطلاقًا طوال معركة إيطاليا. تلقى الجيش دعمًا من المدفعية المضادة بعد بدء غزو فرنسا، ولم يكن لدى العدو القوة الكافية لإنزال قواته في البحر الأبيض المتوسط لشن غزو واسع النطاق في عمق إيطاليا، وكان تركيز التشكيلات الفرنسية والبريطانية المتراصة على جانبي البحيرة مؤشرًا على ذلك. كان الحلفاء يتقدمون نحو فلورنسا. كانت أفضل الفرق الألمانية الآلية أشبه بعقد من اللؤلؤ، حيث ساهم تثبيت هذه القوات الألمانية القيّمة على هذا الجناح في شراسة هجوم الحلفاء. رأيت أنه بعد غزوين في شمال وجنوب فرنسا، كان مصير الحرب برمته يعتمد عليهما، أصبح انسحاب جيوشي من مسرح عمليات أصبح الآن ذا أهمية ثانوية أمرًا لا مفر منه، مع تدهور الأوضاع على جبهتي القتال الرئيسيتين في الشرق والغرب، وتصاعد التوترات على الجبهة الجنوبية. في أغسطس، كان البريطانيون يستعدون لهجوم التفافي حاسم على البحر الأدرياتيكي. وقع الهجوم الأشد وطأة على فرقة المشاة 71 أثناء استبدالها ليلًا. وتحركت دبابات البانزر 26 متأخرة جدًا نحو الخط الأخضر الأول، الذي لم يكن له موقع مكافئ خلفه في عمق قطاع البحر الأدرياتيكي بأكمله، مما اضطرها للاستسلام. وأدى طول المسافات إلى تأخير تحرك القوات المتجهة إلى جبهة البحر الأدرياتيكي، وإعادة تجميعها من جبال الألب الغربية على طول الخليج وعبر سلسلة جبال الأبينيني. أصبحت جبهة جبال الألب الغربية آمنة. وكشفت ضراوة المعارك وكثرة الجنود المشاركين عن أهمية المسرح الإيطالي للحلفاء. وكان الهجوم القادم أشبه بعملية كماشة.كان من المحتم أن يزداد خطر انقطاع الاتصالات مع تقلص المنطقة وازدياد الاختناقات المرورية. كانت مواقعنا في قطاع جثث الدبابات الرابع عشر حيويةً للاستحواذ على بولونيا عبر خطوط الاتصالات الشمالية. كان سلاحنا الجوي هيكلاً عظمياً، حيث كانت غارات الحلفاء تحلق باستمرار فوق جنوب ألمانيا. تعرضت النمسا للهجوم في طريق عودتها، وكان الحفاظ على صناعة الأسلحة الإيطالية في الشمال أمراً بالغ الأهمية. كان تدفق إنتاجها إلى مسرح عملياتنا في الجبهة الغربية، عيّنني هتلر قائداً عاماً للجبهة الغربية في 10 مارس. تم دمج الجبهة الإيطالية تحت قيادتي، إلى جانب جبهات أخرى بعد انشقاق إيطاليا. أصبحت شبكة الجواسيس وانتشار سالفاتوري، الذي بدأ في صفوف المقاومة، مصدر إزعاج على جانبي جبال الأبينيني في أبريل 1944، وكان تأثيرهم الأكثر فاعلية حيث هدد وجودهم إمداداتنا، مما استدعى اتخاذ تدابير عسكرية مضادة بعد سقوط يونيو. ازدادوا عدوانية منذ ذلك الحين، وشكّلت حرب العصابات تهديدًا لعملياتنا العسكرية، وكان من الضروري القضاء عليها. في الشتاء، كان القتال على الجبهة في مارس 1945 شرسًا، لكنهم عادوا بأعداد أكبر من أي وقت مضى. كان الهدف الرئيسي للعصابات هو إرباك خطوط الإمداد والطرق المؤدية إلى إيطاليا وحركة المرور إلى يوغوسلافيا، وكان عامة السكان متعاطفين معهم. لم يكن للعصابات أي رمزية، وهاجموا أسلحتهم. لا يمكن تحديد الخسائر بدقة لأن جميع حالات الاختفاء سُجّلت كمفقودين. من يونيو إلى أغسطس 1944، أفاد ضابط المخابرات الخاص بي بمقتل 5000 من أفراد العصابات. تولّت المخابرات العسكرية وقوات العاصفة توجيه عمليات الاستطلاع الخاصة بالعصابات. كان جهاز الأمن مسؤولاً عن تنفيذ التوجيهات. أُسندت قيادة العملية ضد العصابات إلى قوات العاصفة في القطاعات الساحلية، وكان قادة فرقهم مسؤولين عنها. قاموا بتقسيم قطاعاتهم، حيث وجهوا العمليات من المناطق الخلفية لخطوط الاتصال كمراكز قيادة ثابتة. وردت تقارير يومية إلى استخبارات الجيش من جميع أنحاء منطقة المعركة. قمنا برسم خرائط وفهرسة البطاقات، ولاحظنا الانتشار المستمر لنشاط المقاومة. ارتفع عدد الحوادث الخاصة إلى خمسة حوادث يوميًا، وكانت أعمال التخريب على خطوط السكك الحديدية ومستودعات التخزين عمليات روتينية محلية. أما بقية النشاط فكانت تخضع للوضع على الجبهة، حيث كان هناك تهديد حيوي عند التنسيق المباشر مع العمليات العسكرية. في 8 مارس 1945، قدمتُ تقريرًا إلى هتلر في بلين، وأُبلغتُ بضرورة إقالة الجنرال فون رونشتيدت في الغرب. بعد شرح مفصل للوضع، أخبرني أن سقوط الريغامين استلزم تغييرًا في القيادة، وأن قائدًا أصغر سنًا لا يزال قادرًا على استعادة الوضع. كان الانهيار على الجبهة الروسية يعني الانهيار في كل مكان، لذا ركزنا جميع خطوط دفاعنا على تلك الجبهة. بمجرد تعزيز الجبهة الروسية، سيتم توفير التعزيزات اللازمة بشكل مستمر حتى نقطة الجهد الرئيسي في الغرب، حيث لم يكن بإمكانه توفير فرق جديدة.كانت ريماجن هي النقطة الضعيفة. في هذه المرحلة من الحرب، ولتجاوز هذه المرحلة، ونظرًا للوقت الذي كان من الممكن فيه استخدام التعزيزات والأسلحة بأعداد هائلة من قبل الجيش الثاني عشر، شعر الأدميرالات أن غواصات يو بحاجة إلى تخفيف حدة الموقف مؤقتًا. كنت أتولى القيادة بشكل سري. كانت الفكرة أن اسمي لا يزال مؤثراً في إيطاليا، السمة الرئيسية على الجبهة هي تفوق العدو الاستثنائي، من حيث الرجال والمعدات على الأرض، وتفوقه المطلق في الجو. واجهت فرقنا البالغ عددها 55 فرقة، والتي كانت قوامها 55 فرقة، 85 فرقة أمريكية وبريطانية وفرنسية بكامل قوتها. كان قوام فرق البانزر لدينا 10000 جندي كحد أقصى، أي 100 مقاتل لكل كيلومتر في المقدمة، ولم يكن هناك مجال للاحتياط. أما على الجبهة الروسية، فقد وضعت تحت تصرفها 10 فرق بانزر، وست فرق مشاة كاملة، و10 فرق مدفعية، و8 ألوية دخان، والعديد من الوحدات الأخرى. في مارس، زرت مجموعة جيوش، وكان القائد وقادة الجيش الخامس عشر. قدروا أن عناصر فرقتين مشاة أمريكيتين، وفرقة مدرعة واحدة مزودة بمدفعية، كانت على الجانب الآخر من نهر الراين، ولم يكن هناك ما يضاهيها من قوة يمكن حشدها لمواجهتها. كانت نقاط الضعف هي أجنحة خطنا حول رأس الجسر. كان احتمال تصفية رأس الجسر ضئيلاً ما لم يتم تسريع وصول الإمدادات والتعزيزات وزيادة حجمها. في نفس اليوم الذي ذهبت فيه إلى مجموعة الجيوش "H" على نهر الراين السفلي للتشاور مع قيادة المعركة، كانت مستعدة للدفاع عن نهر الراين. بعد أيام، طلبت مجموعة الجيوش "G"، الجيش السابع على الجانب الأيمن والجيش الأول على الجانب الأيسر، المزيد من التعزيزات. كانوا يبنون خط الدفاع، وكان الجناح الأيسر منخرطًا في قتال عنيف. كان الجيش الأمريكي الثالث يحشد قواته بقوة أمام الجناح الأيمن، ويشن هجمات كثيفة متواصلة لتوسيع الهجوم. كان رأس الجسر يُغذى باستمرار، على الرغم من أن المرتفعات الحاسمة لم تكن في أيدي العدو بشكل كامل. تطلب الأمر تدفقًا متزايدًا من التعزيزات. استهلكت هذه التعزيزات والإمدادات التي تم توفيرها للسيطرة على الوضع. كان مصير جبهة نهر الراين بأكملها معلقًا على قدرتنا على القضاء على رأس الجسر أو احتواءه. تضررت شبكة السكك الحديدية بشدة، وتعطلت أجزاء أخرى من الخطوط، ولم يعد بالإمكان الاعتماد عليها. بدأت أعراض التفكك تظهر خلف الجبهة، وكان عدد المفقودين مؤشراً مقلقاً على تدهور الأوضاع. اعتقد هتلر أننا نستطيع هزيمة الروس في الشرق، ووعد بدبابات للغرب. تصاعد التوتر بشكل لا يُطاق، وانهار الجناح الأيمن للجيش السابع، وتم اختراق الجناح الداخلي للجيشين في الوسط، وتم لفه وتطويقه جزئياً. لم يكن بالإمكان الصمود في بالاتينات. تم إرسال الجيش السابع. كان الجيش الأول في زاوية، متمركزاً على الجناح الأيسر المحوري على طول نهر الراين. كان الاستيلاء على الغابة نقطة محورية. شاهدت عناصر المؤخرة تتدفق عبر النهر. لم يكن بالإمكان الصمود في رأس الجسر بحلول 23 مارس.وتلقيتُ الأمر بالإخلاء. كانت دبابات العدو جريئة، فقد اخترقت خطوط الدفاع ولم تستغل الفرصة لقطع الطريق على المجموعة العسكرية "ج" التي كانت قوتها ضئيلة، فأعادت بناء خط دفاعها خلف النهر. كانت قوات هتلر في حالة قتال متواصل لأشهر. أدت أوامر الصمود إلى خسائر لا تُعوَّض في أفضل الرجال والمعدات. كان الجيش الأول في حوض فرانكفورت ضعيفًا بما استطاع حشده من قوة، ولم تكن لديه احتياطيات لشن هجوم مضاد لصد قوات العدو إلى الضفة الأخرى من النهر. لم يكن هناك أمل في وقف تقدم الفرقتين الأمريكيتين الثالثة والخامسة والأربعين. اتسعت الثغرة لتشكل فجوة والتهمت القوات. استُنزفت القوات الجوية الألمانية تمامًا وانهارت. كنا نفتقر إلى جميع أنواع القاذفات، وتوقف إنتاج المقاتلات بسبب اختراق المناطق الصناعية وتدمير خطوط السكك الحديدية. كانت الضربة القاضية في 29 مارس، حيث اضطر الجيش السابع إلى تأخير الجيش الأمريكي الثالث في وسط ألمانيا. وقد صعّبت فرقة الدبابات مهمة إغلاق الطرق التي كان الأمريكيون يتقدمون عبرها. وكان انتشار قوات العدو من رأس الجسر دليلاً على تراجع القدرة القتالية للقوات الألمانية. أصبح وضع مجموعة الجيوش "ب" حرجًا. كانت تلك أيامًا عصيبة. أعقبت الهجمات الأمريكية الرئيسية الأولية في الشمال، بعد تأمين المرتفعات المهيمنة، تغيير الاتجاه نحو الشرق، مما أظهر نيتهم إحداث اختراق. ثم امتدت هذه الهجمات جنوبًا في حملة ضد المدن، بالتزامن مع التوسع السريع لرأس الجسر. لم تتمكن التعزيزات الألمانية من بناء جبهة صامدة، واقتصرت جهودها على سدّ الثغرات المحلية وشنّ هجمات مضادة قصيرة. وصل العدو إلى نهر أودوبون وتقدم على جبهة واسعة، وبحلول 20 مارس، كان قد مزّق جبهتنا تمزيقًا. وفي اليوم نفسه، وصل إلى حقل النهر. لم تُجدِ تحذيراتي المتكررة من مارشال مودل نفعًا في اعتراض الاختراق، وكانت النتيجة كارثية. لم يكن بالإمكان سدّ الثغرة، وبدأ تحويل القوات شمالًا عملية التفكك النهائية. كانت القدرة على المقاومة محدودة للغاية وقابلة للحساب في 26 مارس. استغلت فرق الدبابات الأمريكية الاختراق وتقدمت بسرعة، وفي كل يوم كانت فرق المشاة تتخلف أكثر فأكثر، وأصبح التعاون مع فرق الدبابات أكثر صعوبة. أغلقنا الطرق خلف أرتال الدبابات المنفردة للقضاء عليها بشكل منفرد من خلال هجمات مضادة جانبية، واستخدمنا كل أنواع الأسلحة المضادة للدبابات لتجنب الحصار عند النهر. انفصلت مجموعة جيوش دال، وكان الجناح الأيسر من رأس الحربة المدرعة الأمريكية يقترب من النهر الرئيسي عند فرانكفورت. استولى العدو على المدينة، فنقلتُ مركز قيادتي. اضطررتُ لخوض معركة متنقلة على المحيط الخارجي، ما أدى إلى الاستسلام في 17 أبريل. لم يعد الضباط يرون أي جدوى من مواصلة الحرب، فقد كانت الكارثة الوشيكة التي حلت بمجموعتي الجيش "ج" و"ب" تتجلى بوضوح.كانت أهداف العدو فصل شمال ألمانيا عن جنوبها، مع ربط قواتنا الرئيسية بالقوات الروسية للاستيلاء على الموانئ الشمالية من قبل البريطانيين في احتلالهم لجنوب ألمانيا. لقد تعلمت خلال الحرب العالمية الأولى أن الدفاع المحلي البحت عن خط المواجهة الرئيسي لم يُجدِ نفعًا في مواجهة هجوم بري وجوي وبحري مشترك. لم يكن بوسعنا سوى خوض حرب ذات حركة محدودة. ذهبت لرؤية هتلر أربع مرات في ذلك الأسبوع، وكانت آخر مرة رأيته فيها في 12 أبريل. كانت مهمتي الحفاظ على مؤخرة الجبهة الروسية خالية. كان مركز قيادتي خلف نقاط الجهد الرئيسي على الجبهة، على مقربة من برلين.

1

1,006

If you want the true self on this twitter dot com account you need to listen to periphery and they’re that much better than any shit ass band you can think of

14

If the people from periphery ever see this please try ow my feelings live again

1

17

Periphery: Finalist for the prestigious 2026 Stanthorpe Art prize: #painting #portraiture #originalpainting #figurativeart #artlifeworks #contemporaryart #contemporarypainting #modernart #contempraryrealism #dailyart #artdaily #artoninstagram #fineart #sergiopaulianniello

2

11