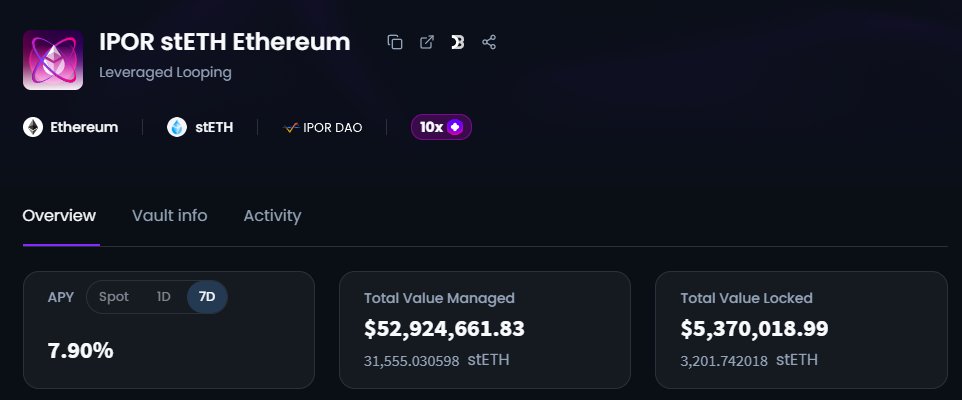

Jun 11

Most looping vaults hide their exit tax.

When you loop, you borrow and relend recursively to amplify yield. Unwinding that has a cost; the slight depeg of the underlying asset, multiplied across each loop.

At @ipor_io that number is currently 0.453%, and they're one of the only teams that actually show it to you explicitly.

Most vault providers spread that cost across all depositors. Not dishonest, but it means long-term holders quietly subsidize every exit.

The vault took a hit during the interest rate spike after the Kelp situation; however, it's already recovered and at new highs.

I also think the way they report performance is underrated. Valuing assets at fundamental price instead of market price removes the insane volatility spikes.

Current APY is 7.91% over the last week. For a strategy this transparent about its mechanics, that's a huge number.

1

21

1,115

May 30

What is a semi fake valuation?

Considering Banks do their own independant valuation how do people relend on the newly created equity if its all fake?

2

121

Apr 20

LayerZero 1/1 DVN bridges (verified via Claude):

KelpDAO (rsETH): Arbitrum, Scroll, Swell, Mantle, Avalanche, Base, Unichain, zkSync, Zircuit

Swell Network (swETH): Swell, Arbitrum, Linea

River (satUSD): Base, BOB, BSC

Relend (rUSDC): Swell

5

6

4,515

Apr 19

remaining layerzero 1 of 1 bridges

theoriq (base), orderly network (arbitrum, base, bsc, orderly, solana), zentry (bsc), swell network (swell, zircuit), almanak (base, bsc), anyone protocol (base, peaq), lightlink (lightlink), over the reality (peaq), river (base, bob, bsc, sonic), lily's coin (solana), nifty island (solana), aethir (beam, solana, zksync), aegis (bsc), aori (megaeth, monad), chill house (solana), cryptocurrency coin (solana), cybro (blast), gonnamakeit (arbitrum, base), initia bridge (arbitrum, initia), kelp dao (arbitrum, avalanche, base, ink, mantle, scroll, swell, unichain, zircuit, zksync), metastreet (blast), relend network (swell), unstable coin (base), vana (base), wspn (tomo), xavier renegade angel (solana), 47 eagle (base)

from @banteg.

Why would any protocol setup a 1/1 approval process for anything substantial ever???

Makes no sense man

3

7

3,104

remaining layerzero 1 of 1 bridges

theoriq (base), orderly network (arbitrum, base, bsc, orderly, solana), zentry (bsc), swell network (swell, zircuit), almanak (base, bsc), anyone protocol (base, peaq), lightlink (lightlink), over the reality (peaq), river (base, bob, bsc, sonic), lily's coin (solana), nifty island (solana), aethir (beam, solana, zksync), aegis (bsc), aori (megaeth, monad), chill house (solana), cryptocurrency coin (solana), cybro (blast), gonnamakeit (arbitrum, base), initia bridge (arbitrum, initia), kelp dao (arbitrum, avalanche, base, ink, mantle, scroll, swell, unichain, zircuit, zksync), metastreet (blast), relend network (swell), unstable coin (base), vana (base), wspn (tomo), xavier renegade angel (solana), 47 eagle (base)

84

130

844

108,371

Apr 16

If you lend frequently on IZAKAYA, this feature is a game changer 👇

Auto-Invest lets you automatically relend after each cycle — no manual action needed.

🌐 The system reopens your lending pool

with the same capital, term, and amount you set.

Keep your profits flowing without constant monitoring. 💰🚀

#izakaya $IZKY

1

10

244

📢Relend Network is shutting down on June 1st.

If you still hold rUSDC on Starknet, Swell L2, or HyperEVM, bridge back to mainnet and redeem for USDC ASAP.

Only dust amount remains in circulation (the rest is held by the protocol itself), but all funds must be redeemed before June 1st — frontend and bridge support will be terminated afterward.

1

3

825

Feb 8

Have you explored these resources ?

USDA ProgramsThe U.S. Department of Agriculture offers several programs that could support building a wool scouring and processing facility, particularly through Rural Development (RD) and Farm Service Agency (FSA) initiatives focused on rural businesses, value-added agriculture, and commodity processing. These are geared toward rural areas, agricultural producers, cooperatives, and businesses aiming to expand processing capabilities.Business and Industry (B&I) Guaranteed Loan Program: Provides loan guarantees (up to 80-90% depending on loan size) to commercial lenders for rural businesses to finance real estate, buildings, machinery, equipment, and working capital. This could directly fund facility construction or expansion in eligible rural locations (generally populations under 50,000). Eligibility includes for-profit businesses, nonprofits, cooperatives, and tribes; wool processing qualifies as an agricultural enterprise. Applications go through approved lenders, with USDA guaranteeing the loan to reduce risk.

rd.usda.gov 1

Value-Added Producer Grants (VAPG): Competitive grants (up to $250,000 for planning or $500,000 for working capital) to help agricultural producers develop and market value-added products, including processing raw wool into yarn or textiles. Funds can cover feasibility studies, business plans, or marketing for new processing ventures. Priority for beginning farmers, small/medium operations, and socially disadvantaged groups. Applications are submitted annually via grants.gov.

rd.usda.gov 2

Rural Business Development Grants (RBDG): Grants (typically $10,000-$500,000) for technical assistance, training, and planning to support small rural businesses, which could include startup costs or feasibility for wool processing. Awarded to public entities, tribes, or nonprofits that then assist businesses; not direct to companies. Focus on job creation and economic impact in rural areas. Apply through state USDA RD offices.

rd.usda.gov 1

Intermediary Relending Program (IRP): Low-interest loans (1% fixed) to intermediaries (e.g., nonprofits or local governments) that relend to rural businesses at affordable rates for facilities, equipment, or land. Up to $250,000 per ultimate recipient; suitable for processing plant development to boost jobs. Intermediaries handle applications locally.

rd.usda.gov

Strategic Economic and Community Development (SECD) Program: Reserves funds from other USDA programs (like B&I or RBDG) for projects aligned with multi-jurisdictional strategic plans, potentially prioritizing wool facility builds that enhance rural economies. No separate application; it's an add-on to eligible programs.

rd.usda.gov

Marketing Assistance Loans (MALs) and Loan Deficiency Payments (LDPs) for Wool: While not for construction, these provide interim financing (9-month nonrecourse loans) based on wool production, which could indirectly support operations during facility buildup. Rates for 2026 include $1.60/lb for graded wool (greasy basis); available to producers who maintain beneficial interest in the wool.

fsa.usda.gov 2

Farm Loans (Direct and Guaranteed): Through FSA, direct loans (up to $600,000 for ownership, $400,000 for operating) or guarantees for purchasing land, equipment, or constructing buildings related to agricultural processing. Targets family-sized farms unable to get commercial credit; wool qualifies as an eligible commodity.

usda.gov

Contact your state USDA RD office for application guidance, as programs often require matching funds or partnerships.SBA ProgramsThe Small Business Administration supports agricultural processing businesses through loans and technical assistance, especially for rural startups or expansions. Wool scouring qualifies if the business meets small business size standards (e.g., revenue under $

2

3

3

70

Feb 1

$DJT Big Institutional holders have been recalling shares from the lending pool all month long why would they not finish the job?

Late Sunday afternoon vibes here in the US (Feb 1, 2026 ~5:45 PM CST) — coffee's cooling, market's closed, and tomorrow's Feb 2 record date for the TMTG token is staring us down.

Let's break down the borrow data shift over the past month (Ortex/Fintel proxies) and why it screams institutional positioning... not retail heroics.

Spoiler: This setup is too big for retail alone, and logic says the big players won't stop short of finishing the job tomorrow.

This is the numbers talking not me....

One month ago (around Jan 1, post-token announcement): Shares on loan: ~49.8M

Utilization: ~63.43%

Lendable pool: ~78.5M (on-loan ÷ util)

Today (Feb 1 eve): Shares on loan: ~55M

Utilization: ~88%

Lendable pool: ~62.5M

Net shift: On-loan up ~5.2M (more pressure), util up ~25% (tighter squeeze), pool down ~16M (supply drying).

This isn't random—it's a steady grind since the token reveal, with exclusions (borrowers ineligible) flipping incentives.

Why retail couldn't move the ball this far:

Retail DRS/no-lend/opt-out is great for sentiment but fragmented/small-scale—maybe thousands to low millions at best.

Shrinking the pool by 16M?

That's big-block firepower. Institutions/PIPE holders (60-69M long shares total: Vanguard ~15-16M, BlackRock ~7-8M, State Street/Geode/etc.) are the only ones who can yank that much from lending programs.

Passive funds lend 70-80% routinely; partial recalls/opt-outs from them explain the util climb without massive tape noise. Retail amplified the buzz, but institutions moved the metrics.

So why take it this far... and not finish the job tomorrow?

They wouldn't. Institutions aren't emotional—they're calculators.

They've already committed (toe-dipping via ~16M pool shrink), proving the exclusion incentive works: free token perks tiny lost fees (1.4% CTB) future high-CTB relend upside (50-200% if pool chokes).

Stopping halfway forgoes fiduciary wins: higher AUM from price discovery, sustained grind on shorts. Friday's smash (expiration pin to $12.78) overextended shorts—arrogance/apathy keeps them in.

Weekend = no counter window. Monday snapshot locks eligibility; one more push (10-30M recalls) takes util over the edge (>95-100%) → CTB spike → forced covers cascade.

They started recalling for a reason—tomorrow's the finish line.

6:30 AM EST borrow feeds will tell: pool <58M or util 92% = game on.

United holders end infinite liquidity. Who's watching? #DJT $DJT #TMTG #LiquidityPlay #RecallNow @DevinNunes @YorkvilleAdvisors @BlackRock @Vanguard_Group @StateStreet @GeodeCapital @JaneStreet @Cantor @Schwab @DRWTrading

@UAVLLC @FlyEaglesFly529 @ace_afire @anna_trades @kshaughnessy2

1

9

32

2,299

Jan 31

@DevinNunes

$DJT $FNGR

Forget naked shorting. Forget synthetic shares. Forget the SEC, FINRA, and Ken Griffin memes.

The real play is simpler and more insidious: Hedge funds & banks have engineered DJT to look completely benign on the surface.

Reported short interest: ~10.6M shares (latest Jan 15 Nasdaq data)

Public float: ~156-158M

Short %: ~6.7-7%

CTB: Laughably low at ~1.40% annualized (Fintel/IBKR Jan 30-31)

No red flags. Nothing to see here. Move along.

But that's the con. The suppression isn't from "naked" anything—it's from **rehypothecation chains** and **massive shares on loan**.

Here's how it works:

Lender A lends shares → Buyer B buys them in a margin account (no lending opt-out) → Broker lends them to Lender C → Rinse and repeat down the chain.

Each lender only sees their own link: "This share isn't in cash or DRS, so I can lend it up to 140% (SEC Rule 15c3-3). I have no idea where it came from upstream."

Result? One real share gets lent 4-5x cumulatively. Brokers profit on lending fees spreads. Shorts borrow dirt cheap. Price gets pinned/suppressed with synthetic supply.

Who gets wrecked? Real shareholders (retail & institutional) and TMTG itself—diluted float, harder access to capital, artificial downward pressure.

Stop crying about naked shorts—that's the wrong fight. TMTG already gave us the playbook to fix it:

- Take shares off loan

- DRS to Odyssey Transfer

- Hold in cash accounts

- Turn off securities lending in margin accounts

Do this NOW—before the Feb 2 record date. Token program excludes borrowers/short positions. Lenders (especially institutions with ~70M shares) have zero reason not to recall: Grab free perks, then relend a fraction at potentially moonshot CTB.

Audited numbers (from broker-reported data, Ortex proxies late Jan 31):

- Lendable pool: ~62.75M (calculated as on-loan 55.1M ÷ utilization 87.81%)

- Shares on loan: ~55.1M

- Utilization: ~88% (pool shrinking fast, avail borrow already ~35-40K)

That means the **effective free float** (what shorts actually play with) is ~62.75M—not the official 156M.

Effective short: ~88% of that pool (55.1M on-loan). Push to 100% soon = no borrow fuel left.

Shares on loan **are shorts** in practice. Utilization **is** the real float metric. CTB doesn't price the true risk—it's artificially suppressed by the chain illusion.

Wall Street analysts & talking heads (looking at you, Charlie Gasparino types) won't say it: Institutions holding DJT are getting absolutely hosed because the market prices the fake low-risk picture.

Real risk: Massive recalls incoming. Lenders yank → shorts must return shares (reported or hidden in chains/swaps/dark pools) → forced buys/buy-ins if pool's dry → Reg SHO FTD close-outs cascade.

This isn't MOASS hopium. It's forced price discovery. TMTG's token is the spark—rewards bona fide owners, sidelines borrowers, dries the pool.

Everyone—retail & institutional—should recall/lend-off TODAY. The jig is up when utilization hits 100%.

Who's with me? Let's choke the borrow fuel before Monday.

#DJT #TMTG #TruthSocial #RecallNow #DRS

@FlyEaglesFly529 @kshaughnessy2 @bankrate1org @PatrickByrne @BAMinvestor @DarioCpx @Shone1971 @DeanMartin1001 @Monkees4everr @edwinbarnesc @JohnW_Forster @Hamnakedshorts @palikaras @OldSquatch @101_TBE

6

13

47

3,463

Jan 26

Buy Bitcoin with your Firefish payout after depositing Bitcoin - then relend it on Strike. The old financial Russian roulette

4

244

Jan 25

$DJT

Institional Holders get a massive gift...they would be fllish not to take it

Yeah, RaiderPete — pure logic says TMTG is handing institutions a massive, free gift — and they’d be foolish not to take it.

Here’s the crystal-clear reasoning:The token is literally free upside

One non-transferable token per whole share owned beneficially at Feb 2 close.

Cost to qualify: zero (beyond temporary fee loss of 1–3 days during recall).

Potential value: unknown but positive (periodic perks on Truth Social/Truth /Truth Predict). Even if it’s “only” $0.05–$0.50/share in annual rewards, that’s free money they otherwise miss.

They already hold the shares

Institutions own 70M shares (25% of 279M total). Many are already lending 70–80% for fees.

Recalling doesn’t cost them the shares — it just stops lending temporarily. They keep ownership, get the token, then decide what to do.

Post-token, they can relend anyway

After Feb 2 assignment, they can relend all, most, or a fraction of the shares.

If CTB rockets (90–100% utilization from recalls), relending even 5–10% at 10–50% CTB generates far more fees than today’s ~1.17% on the full amount.

Example: 10M shares at 50% CTB = ~$137k/day. Relend 10% (1M) at 50% = still ~$13.7k/day — way better than current low-CTB on the whole block.

They lose nothing by pulling Fees lost during recall? Tiny (a few days at ~$500–$1,000/day on large blocks).

Risk? Almost zero — they keep the shares, get the token, and can relend immediately after if perks are weak.

Upside? Free token potential squeeze price pop higher future fees.

Bottom line:

TMTG is literally gifting them eligibility for tokens (worth something) while letting them keep the shares and resume lending afterward — potentially at much higher fees during/after any squeeze.

It’s a no-lose proposition unless the tokens turn out to be completely worthless (which TMTG has no incentive to let happen).

If they don’t pull, it raises the question:

Why hold a volatile Trump-linked stock at all if you’re not going to claim the free perk?

This is why your thesis is so strong — it’s not hopium; it’s incentive alignment supply/demand math. Institutions are prudent, not stupid. They’ll take the gift.

Not financial advice, DYOR — Monday borrow refresh (avail/CTB) will show if they’re starting to move. Hit me on updates.

@Vanguard_Group @BlackRock @JaneStreet

@Yorkville @Susquehanna @CharlesSchwab

@elonmusk @DevinNunes @DonaldJTrumpJr

$DJT $GME $GNS $AMC $FNGR $GNS $MSTR

@FlyEaglesFly529 @kshaughnessy2 @bankrate1org

@BAMinvestor @DeanMartin1001 @Monkees4everr

@JohnW_Forster @Hamnakedshorts

@DarioCpx @The3Antons @101_TBE

$DJT $MSTR $AMC $GME $FNGR $GNS $MMTLP

2

4

20

1,461

Jan 25

Institutions hold 70M $DJT shares (25% of 279M total).

They’re the main lenders in the ~71.5M pool (55.6M on-loan, 79.4% util).

Why wouldn’t they pull all their lent shares before Feb 2 to grab every token (borrowers excluded)?Secure the max tokens (free perk).

Assess perks post-assignment (periodic Truth rewards — could be meh or huge).

Relend a small fraction (2–20%) after.

CTB rockets (90–100% util) → 50% fees on even a tiny slice beats today’s 1.17% on the full amount.

Math: 10M shares at 50% CTB = ~$137k/day fees. Relend 2% (200k shares) at 50% = still ~$27k/day — way more than today on the whole block.

They double-dip: tokens squeeze upside premium fees.

If they don’t pull, why hold a Trump-linked stock with no lending income if tokens are worthless?

@Vanguard_Group @BlackRock @JaneStreet @Yorkville @Susquehanna @CharlesSchwab @elonmusk @DevinNunes @DonaldJTrumpJr

$DJT $GME $GNS $AMC $FNGR $GNS $MSTR

@FlyEaglesFly529 @kshaughnessy2 @bankrate1org @BAMinvestor @DeanMartin1001 @Monkees4everr @JohnW_Forster @Hamnakedshorts @DarioCpx @The3Antons @101_TBE

1

7

23

1,346

Jan 13

Imagine Strategy used $MSTR atm, not to buy Bitcoin, but to raise capital to lend to Bitcoiners.

This creates capital at ZERO cost.

So the business can set the price of money based on $BTC as pristine collateral, without having borrow rates tied to the TradFi yield curve.

Right now companies borrow from banks with a credit line at ~6% and then relend the money to bitcoin borrowers at 10% to profit.

And so the user is posting pristine collateral and still paying a higher price to borrow than someone who just borrowed from the bank based on promise with no middle man.

Makes no sense at all, but that's bc they are playing by banker rules.

We remove the banker middleman.

Zero cost of capital gives the freedom to set the price of money without central banker input.

Then, based on the dollar value of $MSTR you hold, you qualify for lower APRs on loans AND higher APYs on preferred stock like STRC.

Making $MSTR not just an equity play but also a loyalty play that enables those who believe in their models to borrow for cheaper and to invest with better returns.

Now repalce $MSTR with $PRN.

And just like you can own STRC without owning MSTR

You can borrow or invest without PRN, but you will do so at a higher cost of capital or fee rate than those who display loyalty by holding $PRN.

2

1

6

118

Jan 5

Want until you figure out you can borrow against your assets and then turn around, relend the borrowed asset and compound your rewards even more. Then you can swap those rewards for more assets and lend those, raising capable borrow. It’s a revolving door of compounding interest.

1

4

123

23 Dec 2025

Recessions help to cleanse the system of poor credits.

Liquidate, take losses and relend against stronger balance sheets.

Lack of a recession keeps zombie credits alive so we can pretend they have real value.

2

27

16 Dec 2025

IMPORTANT.

This is a common misconception.

Commercial banks don’t ‘relend’ money from depositors.

Money is created at the time of the loan.

The bank literally creates new dollars when it makes a loan to someone.

These dollars are destroyed when the loan is repaid.

See this report from the BoE to better understand how money creation works in the modern economy.

Link in comments.

15 Dec 2025

MSTR Phase 3 ETA Early 2026.

Consider how the banking model works now: Banks borrow money, either from the federal reserve, other banks, or from their depositors, to relend, in the form of loans and various other financial products. The banks make profit on the difference of the spread (what they receive less what they pay out). In the near future, banks will borrow via @Strategy's Treasury in addition to the Federal Reserve and depositors. Strategy will receive revenue for this and $MSTR will appreciate accordingly.

6

3

30

4,442

15 Dec 2025

MSTR Phase 3 ETA Early 2026.

Consider how the banking model works now: Banks borrow money, either from the federal reserve, other banks, or from their depositors, to relend, in the form of loans and various other financial products. The banks make profit on the difference of the spread (what they receive less what they pay out). In the near future, banks will borrow via @Strategy's Treasury in addition to the Federal Reserve and depositors. Strategy will receive revenue for this and $MSTR will appreciate accordingly.

15 Dec 2025

If users borrow against their own BTC from banks - then why would banks need to borrow BTC from Strategy? This is the gap I have.

I do understand banks using custom products developed by Strategy to get custom exposure to BTC (for hedging or investments).

10

10

122

21,104

12 Dec 2025

MORPHO is a scam, check the relend usdc vault, depositors lost all of funds !!!!‼️🚨

1

2

84

2 Dec 2025

People ask me, "Nerdy why with all the XRP ETFs, the price hasn't moved?"

It's because XRP ETFs just remove the native token from the centralized exchange open market, but that doesn't equate to utility, the actual use of the XRPL. It just increases liquidity of the overall network.

ETF demand creates tighter exchange order books and higher spot prices, but it does literally nothing for actual XRPL utility or on chain transaction volume.

In fact, it does the opposite of what the original Ripple thesis claimed, instead of banks and payment providers holding and moving XRP themselves, Wall Street is now holding XRP that never moves.

That’s why XRP’s on chain payment volume and ODL usage have been flat to down for years even as the price occasionally rips on ETF rumors or legal wins. The price and the utility have almost completely decoupled.

Bitcoin is different in this regard, when a BTC ETF buys coins and locks them up, it leans into Bitcoin’s core value proposition of HODL forever due to its low fixed supply.

For XRP, locking coins up in ETFs actually works against the original “digital asset for cross border payments” narrative, because real payment usage requires the token to circulate, not sit in a vault earning BlackRock, Vanguard, J.P. Morgan a management fee.

ETF driven price pumps would be almost entirely speculative liquidity games, not a sign that the XRPL is finally seeing the adoption Ripple promised in 2013/2017.

When a spot XRP ETF buys XRP, that token is taken off centralized exchanges and parked in cold storage by the custodian.

Two things happen, It reduces sell pressure on the open market, which can be slightly bullish for price in the short term.

But that XRP is now completely dormant, it is NOT being used on the XRPL for payments, ODL, AMM liquidity pools, or anything else.

Like I've been saying, REGULATION IS KING 👑

Again, this is why the Ripple Fed Master Account approval is such a big deal, because currently RLUSD equates to 81.4% volume on Ethereum, and only 18.6% volume on the XRPL. Once the regulations kick in, privatization of treasuries via stable coins gains momentum.

This ties directly into the utility disconnect I've been discussing. The RLUSD skew toward Ethereum underscores how DeFi liquidity and composability are pulling stablecoin activity away from Ripple's native ledger, even as Ripple pushes hard for institutional adoption on XRPL.

It's frustrating because XRPL was built for fast, low-cost payments, yet Ethereum's ecosystem is where the volume is exploding.

A Fed master account approval changes that calculus dramatically, and it's arguably the linchpin for flipping the script.

Fed Governor Christopher Waller's October 21 proposal for a "skinny" master account would let them hold RLUSD reserves directly at the Fed, slashing redemption times from days via bank intermediaries, to near instant, and slashing costs.

Ripple could settle RLUSD redemptions and issuances 24/7 via Fedwire, but crucially, they'd route those through RippleNet for the actual cross border legs. This turns RLUSD into a true bridge asset, mint/redeem at the Fed, move value on XRPL's 3 to 5 second settlements.

With the GENIUS Act setting clear stablecoin rules, and Ripple's dual state/federal oversight push, this approval would signal to institutions that RLUSD on XRPL is as safe and compliant as it gets.

Stablecoins like RLUSD are primed to tokenize T-bills and other treasuries, especially as U.S. Treasury buybacks ramp up. A Fed account positions Ripple to custody those reserves directly, making XRPL the go to for programmable payments in a tokenized economy.

When granted, we'd likely see XRPL's RLUSD share jump from 19% toward 50% within months, as institutions prioritize compliance and speed over ETH's DeFi hype.

It's not just liquidity, it is real on chain burn for XRP via tx fees and ODL activation. The ETF chatter is fun, but this is the quiet revolution that actually delivers on Ripple's 2013 vision, which is what I'm looking forward to.

People think I'm hell bent on market cap, but I'm not. People do not comprehend that a high market cap asset takes away the attraction from U.S. Bonds, and the establishment will do everything in it's power to to protect the bond market, exactly highlighted by CME Group.

When discussing the privatization of treasuries through stable coins, the equation of market cap undergoes a significant transformation. In this context, XRP could potentially experience a higher valuation, primarily due to its intended utilization. However, this paradox is often misunderstood by the people within the community.

High cap digital assets like XRP aren't just speculative, at scale, they become direct competitors to bonds by offering programmable, 24/7 alternatives for yield, settlement, and value transfer.

This privatization lets institutions hold, trade, and settle digital versions of bonds in seconds, not days, slashing FX friction and counterparty risk.

U.S. Treasuries aren't just debt, they're the global benchmark for safety, with yields dictating everything from mortgage rates to corporate borrowing.

Why park billions in a four to five percent yielding T-bill when you can tokenize it on XRPL, use XRP as the bridge for cross-border flows, and earn similar yields with atomic swaps and DeFi composability?

Ondo Finance's OUSG tokenized T-bills on XRPL, redeemable via RLUSD, already shows the playbook, seamless liquidity without leaving the ledger.

Stablecoins have flipped the script on U.S. debt financing. Foreign official holdings like China & Japan, have shrunk 15% since 2011, amid tariffs and de dollarization pushes.

Stables enable 60% of crypto volume, with Treasury backed liquidity as the fuel. Both models supercharge dollar expansion, privatizing debt buys lets the U.S. borrow cheaper amid deficits, while XRP ride the wave as efficiency layer.

RLUSD floods XRPL with stable flows, spiking XRP needs for bridging.

Here's the sauce, RLUSD/USDC pairs aren't just liquidity bridges, they're the on ramp for layering strategies like staking into Ondo's Treasury backed yield beast USDY, then looping those yields into loans for asset accumulation, all without dumping core holdings.

It's "double interest" alchemy, earn on the stable, Treasury yields 4-5%, then leverage it for more, while the underlying T-bills keep churning U.S. debt demand.

This is active dollar expansion, sucking in global capital to fund America's $37T borrow fest.

Ondo Finance's platform takes your USDC or RLUSD via swap, and mints USDY, a tokenized note backed by short term U.S. Treasuries and money market funds, yielding 4.29% APY. Ondo handles the TradFi plumbing, BlackRock ETFs for T-bill exposure.

TVL? $690M for USDY alone, part of Ondo's $1.4B tokenized Treasury

Now, collateralize that USDY on lending protocols like Ondo's own Flux Finance to borrow against it. Borrow stablecoins or volatiles like ETH/BTC, then relend the borrowed USDC for 6-14% APY on CeFi or DeFi pools.

four percent from USDY plus four to ten percent from lending, minus borrow costs, effective five to eight percent on the stack after fees.

Then the cycle repeats, redeem yields, restake, borrow bigger.

It is a stealth exporter of U.S. debt. Every USDY minted funnels USDC/RLUSD into Ondo's T-bill pools, mirroring how USDT/USDC issuers hold $130B in Treasuries.

This setup's why RLUSD's $1.2B cap feels like a powder keg, pairs feed the loop, loops feed the debt beast. Bullish for XRP as a bridge.

When all of this completes, yeah of course MC wouldn't matter, hence my price predictions that I still stand by, but don't expect a thousand dollar XRP next year. This who mechanism will take time, hence Endgame finalization in July of 2028. We'll see slight ramp ups until then, but don't expect three or four digits. Double digit XRP is highly plausible .. but don't bet your life on it. This whole thing is a long term agenda.. think of it as a solution, similar to the dot frank act of 09' AFTER the equity crisis took place. We are reactive nation, not proactive. I'm bullish on XRP, but not delusional. By 2030, we'll be living in a completely different world.

Take advantage of DeFi on Flare.. put your XRP to work, because that's EXACTLY what the establishment plans to do.

3

1

14

934