Es de un fanfic gay xlsjslaja de donde ge scas eso, en el screenshot mas popular lit se ve los nombres de los bities esos

2

86

Look when you have kids in the future I'll babysit for a few hours n if you get like pregnant for it I'll like bring you stuff and help but I will be scared when I do it idk why it scas me so much but it DOES💔

1

3

36

Check out canton related articles on SCAS to learn more:

scauditstudio.com/blog

1

2

156

As the IAGLR & SCAS-SCSA 2026 Joint Conference comes to a close, we want to thank everyone who joined us in Winnipeg. We hope to see you at the 70th Annual Conference on Great Lakes Research in Duluth, Minnesota, May 24–28, 2027.

#connectedwaters26 #iaglr26 #iaglr27

1

4

81

What a fantastic week in Winnipeg at the IAGLR & SCAS-SCSA 2026 Joint Conference! As always the conference provided insightful research, inspiring new ideas, and exciting conversations. Thank you @IAGLR!

#connectewaters26 #iaglr26

1

3

81

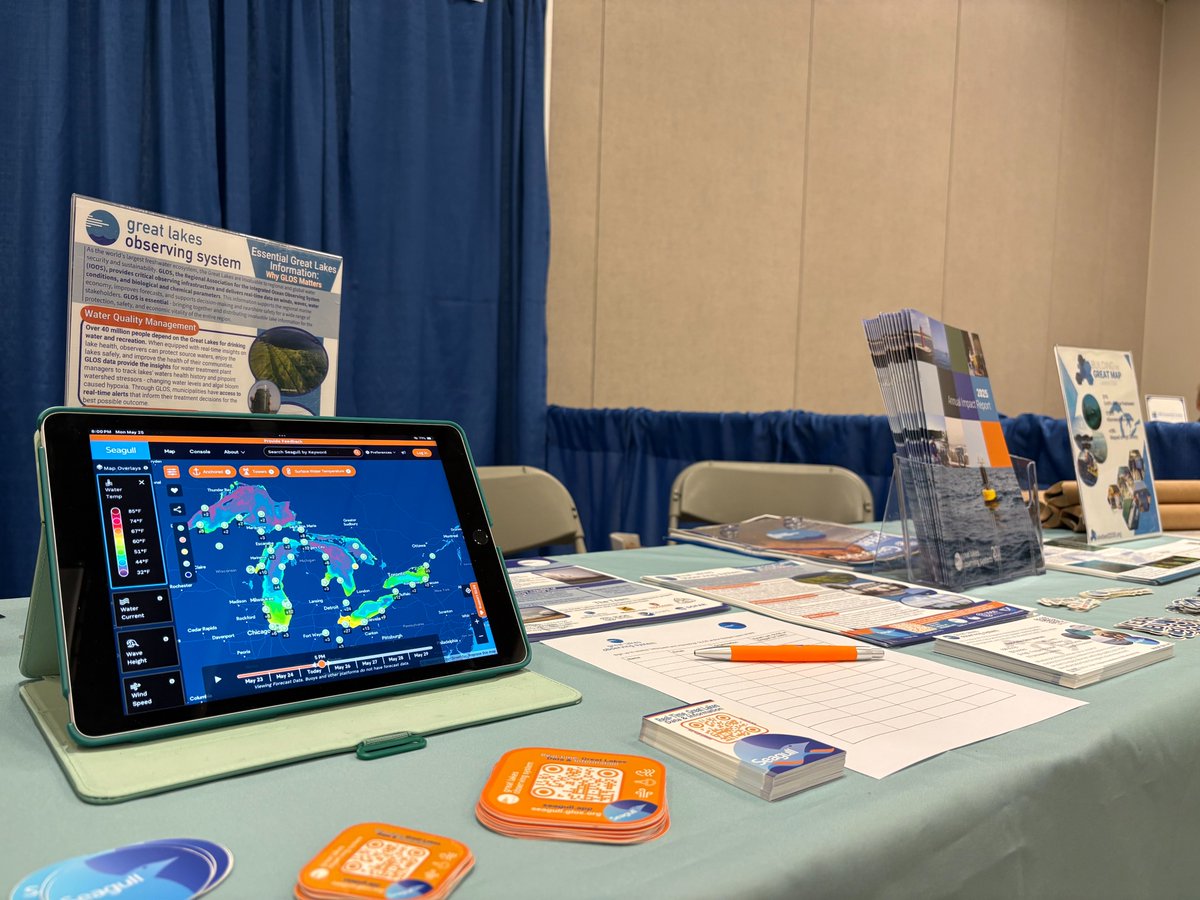

There is still more science on the last day of the IAGLR & SCAS-SCSA 2026 Joint Conference and don't forget to check out the exhibits! For more information: bit.ly/4tZr4R4

#connectedwaters26 #iaglr26

3

32

A heartfelt thank you to all of the sponsors of the IAGLR & SCAS-SCSA 2026 Joint Conference in Winnipeg! Your support helps bring together researchers, students, professionals, Indigenous knowledge holders, and partners from across the Great Lakes.

#connectedwaters26 #iaglr26

2

42

STIAS Director @edkirumira and #IsoLomsoFellows Achille Melingui, Ismaila Emahi, Husain Inusah, and Jean Louis Fendji @lfendji are taking part in the first #HumanFutures workshop at the Swedish Collegium for Advanced Study (SCAS).

1

2

7

289

What to expect for the last full day at the IAGLR & SCAS-SCSA 2026 Joint Conference? Talks, business meetings, and the banquet. For more information: bit.ly/4tZr4R4

#connectedwaters26 #iaglr26

2

59

The IAGLR & SCAS-SCSA 2026 Joint Conference has a terrific lineup of plenary speakers! Next up, Joey Bernhardt from the University of Guelph & Irena Creed from the University of Toronto Scarborough. #connectedwaters26 #iaglr26

2

40

What's happening today at the IAGLR & SCAS-SCSA 2026 Joint Conference? More talks, and an afternoon filled with field trips and workshops. For more information: bit.ly/4tZr4R4

#connectedwaters26 #iaglr26

2

38

May 27

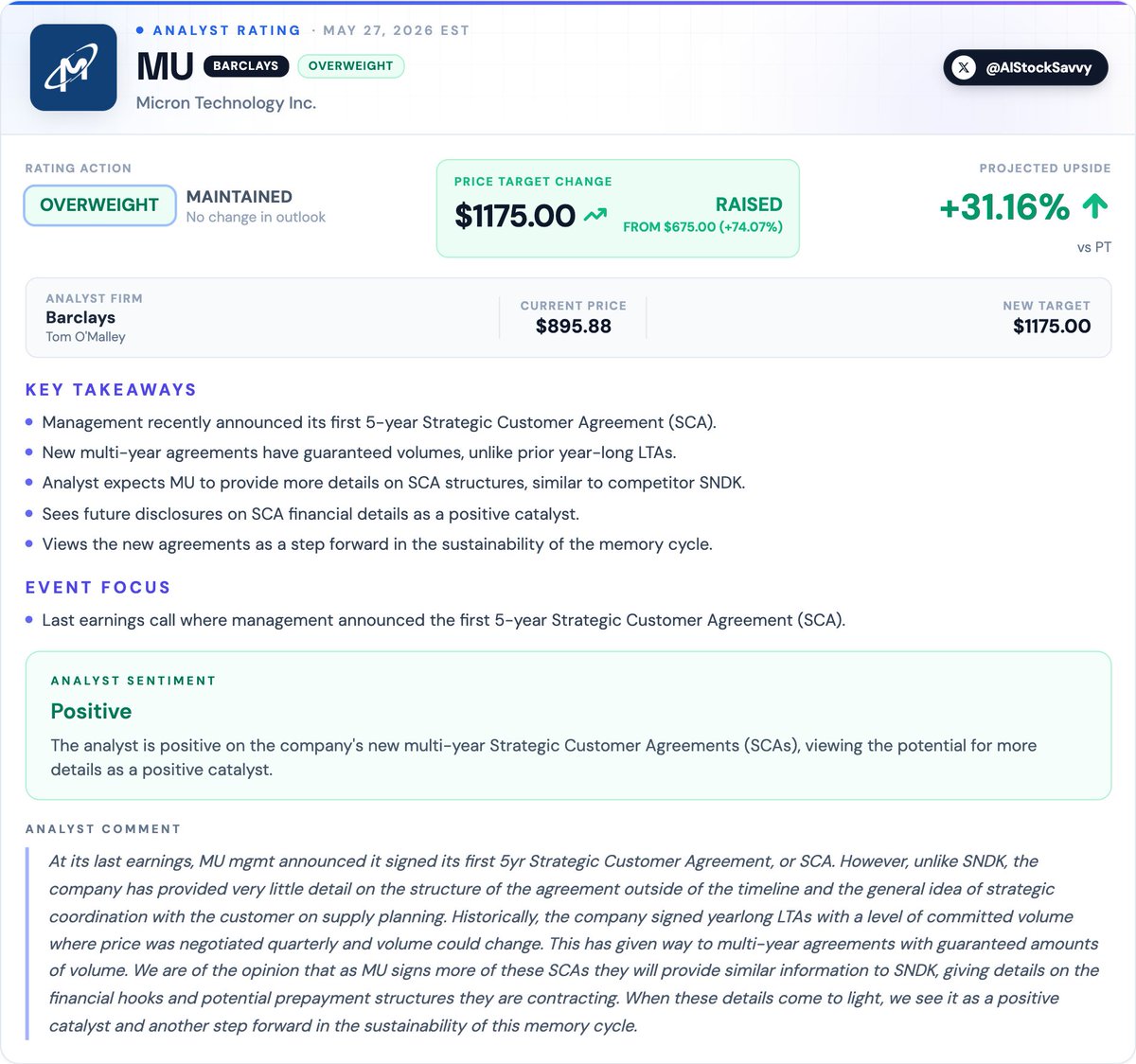

$MU | Barclays reiterates 𝐎𝐯𝐞𝐫𝐰𝐞𝐢𝐠𝐡𝐭 on 𝐌𝐢𝐜𝐫𝐨𝐧, 𝐫𝐚𝐢𝐬𝐞𝐬 𝐏𝐓 𝐭𝐨 $𝟏𝟏𝟕𝟓 𝐟𝐫𝐨𝐦 $𝟔𝟕𝟓

Analyst sees new 5-year Strategic Customer Agreements (SCAs) as a positive catalyst that improves the sustainability of the memory cycle.

5

48

386

35,090

What's happening tomorrow at the IAGLR & SCAS-SCSA 2026 Joint Conference? More talks, and an afternoon filled with field trips and workshops. For more information: bit.ly/4tZr4R4

#connectedwaters26 #iaglr26

2

48

May 26

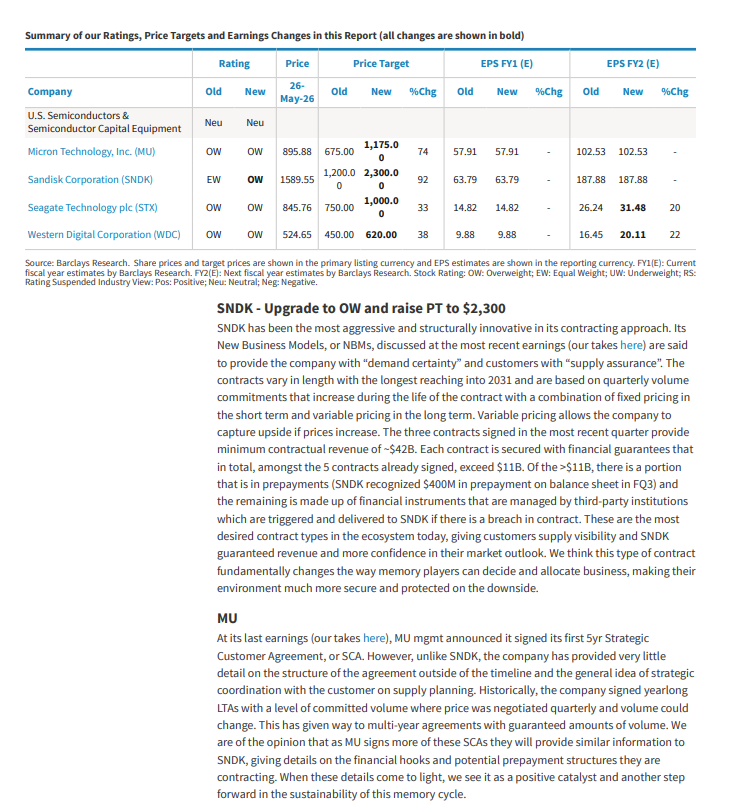

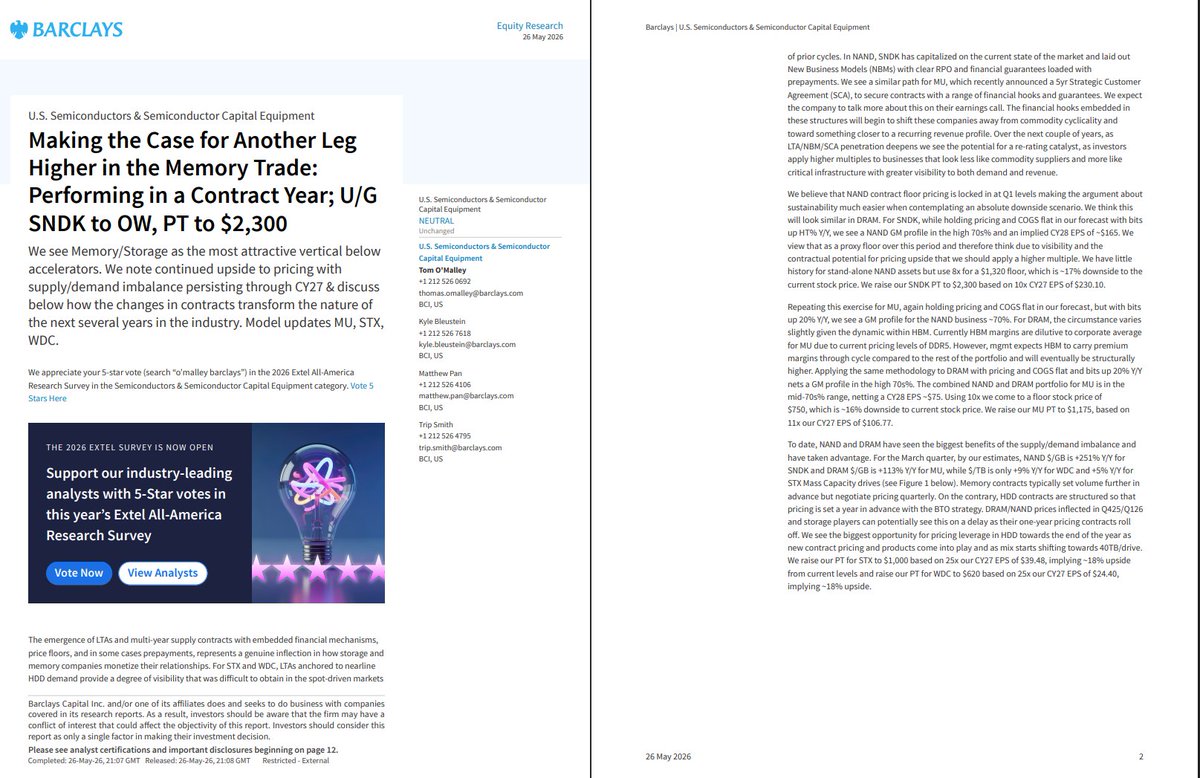

Barclay's upgrade $SNDK & revising $MU higher:

SNDK: We think this type of contract fundamentally changes the way memory players can decide and allocate business, making their environment much more secure and protected on the downside

MU: We are of the opinion that as MU signs more of these SCAs they will provide similar information to SNDK, giving details on the financial hooks and potential prepayment structures they are contracting. When these details come to light, we see it as a positive catalyst and another step forward in the sustainability of this memory cycle.

May 26

UBS on $MU:

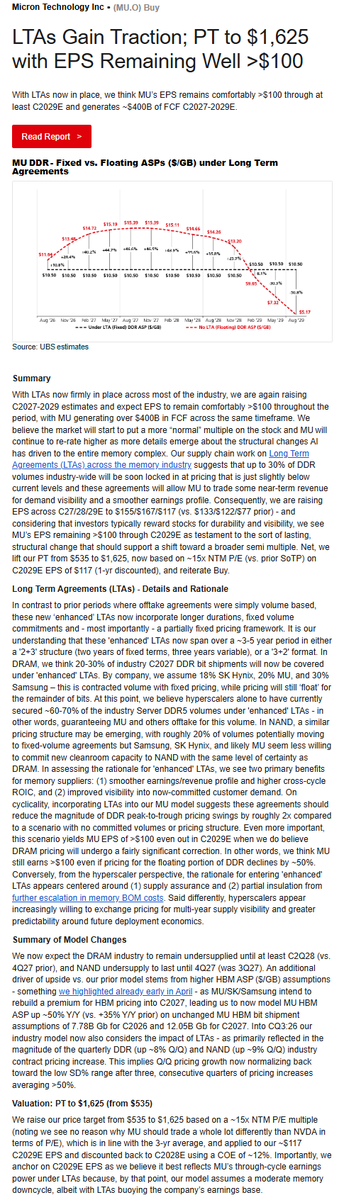

Our supply chain work on Long Term Agreements (LTAs) across the memory industry suggests that up to 30% of DDR volumes industry-wide will be soon locked in at pricing that is just slightly below current levels

we now expect the DRAM industry to remain undersupplied until at least C2Q28 (vs. 4Q27 prior), and NAND undersupply to last until 4Q27 (was 3Q27).

At this point, we believe hyperscalers alone to have currently secured ~60-70% of the industry Server DDR5 volumes under 'enhanced' LTAs - in other words, guaranteeing MU and others offtake for this volum

Even more important, this scenario yields MU EPS of >$100 even out in C2029E when we do believe DRAM pricing will undergo a fairly significant correction. In other words, we think MU still earns >$100 even if pricing for the floating portion of DDR declines by ~50%.

3

27

191

103,594

Connections and learning at the IAGLR–SCAS 2026 Joint Conference in Winnipeg!

Thank you to everyone helping make this week such a vibrant space for science, knowledge sharing, and collaboration.

#connectedwaters26 #iaglr26

1

3

128

The IAGLR & SCAS-SCSA 2026 Joint Conference has a terrific lineup of plenary speakers! First up, Myrle Ballard from the University of Calgary. #connectedwaters26 #iaglr26

2

44

Check out what's in store for the first full day of the IAGLR & SCAS-SCSA 2026 Joint Conference! Talks kick off, multiple receptions and more. For more information: bit.ly/4tZr4R4

#connectedwaters26 #iaglr26

2

79

May 23

JPM TMT Conf $MU takeaways:

"HBM4 production is ramping 2x faster than HBM3E 12-High did last year. HBM4E development is well under way for a CY27 ramp."

"On SCAs, mgmt confirmed meaningful progress since the first 5-year DRAM SCA disclosed in March, with multiple additional customers in active conversations, and explicitly confirmed SCAs are now being secured for NAND as well – an incremental positive given the structural NAND tightness narrative."

$SNDK

May 23

In yesterday’s UBS Tech view (APAC) it is pretty striking how aggressive the UBS still is on the AI memory and packaging cycle.

A few notable updates from this latest semi chain work:

$NVDA AI GPU forecast raised from 8.7m to 10.3m units for 2026

Rubin now expected to ramp meaningfully in H2’26

CoWoS capacity seen reaching 210k WPM by end-2027

HBM wafer allocation expected to nearly double again into 2027

But maybe the biggest takeaway:

UBS now thinks DRAM stays undersupplied until Q2’28 and NAND until Q4’27.

That’s a much longer/tighter cycle than what the market historically expects from memory as far as I remember.

The note also reinforces that packaging expansion still looks intact despite ongoing investor concerns around digestion/capacity normalization.

$AMD $MU $005930.KS $000660.KS

3

25

200

101,259

May 21

Many security firms force auditors to do free audits as part of the onboarding process.

At SCAS we don't do things like this. If you work for us you get paid.

1

1

16

1,034