Just a little goblin looking for the golden pot sharing information, discussing opinions, trading US and EU shares & options. No recommendations #DYOR

Joined March 2019

- Tweets 2,905

- Following 269

- Followers 1,932

- Likes 879

492 Photos and videos

Jun 12

Amazing how late some sellside firms realize, that this transition has happened way earlier than "now"? Late seems better than never.

UBS:

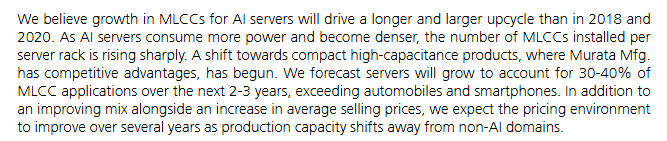

Murata 6981.JP may be undergoing one of the more interesting transformations in tech hardware.

For years, investors viewed it as a smartphone and consumer electronics supplier. UBS now increasingly sees it as an AI infrastructure company.

AI servers are becoming the largest growth driver for MLCCs. As racks become denser and power requirements rise, the amount of MLCC content per server keeps increasing. UBS now expects datacenters to account for 30-40% of Murata's MLCC business within the next few years, overtaking traditional end markets.

That shift is forcing UBS to rethink both earnings and valuation.

The firm raised operating profit forecasts by 14%/49%/77% for FY3/27-29 and lifted its PT from ¥5,400 to ¥13,200. They also expect pricing power to remain unusually strong as AI demand absorbs capacity and pushes customers toward higher-value MLCC products.

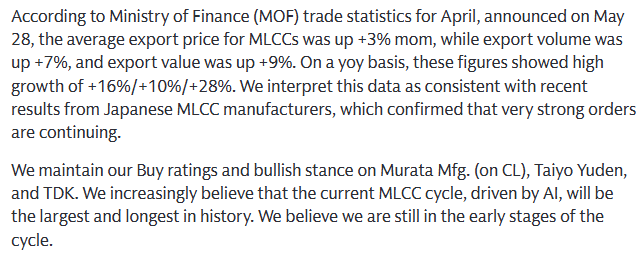

May 28

Reading a lot on the MLCC cycle lately here on X.

Goldman just out with a note saying AI server demand is now driving both pricing and volume higher simultaneously - Something they believe could turn into the biggest/longest MLCC cycle ever.

Some key takeaways:

> Goldman says MLCC ASPs and volumes continue rising

> AI GPUs/ASICs increasingly require higher-capacity MLCC content in constrained board space

> Technology complexity is enabling continued pricing resets / effective price hikes

> Goldman believes the cycle is still in the early innings

AI hardware complexity keeps increasing component content per system, which may structurally extend the entire electronic components cycle.

Murata, Taiyo Yuden, and TDK remain key beneficiaries of AI server demand.

1

2

45

31,550

Jun 12

May 31

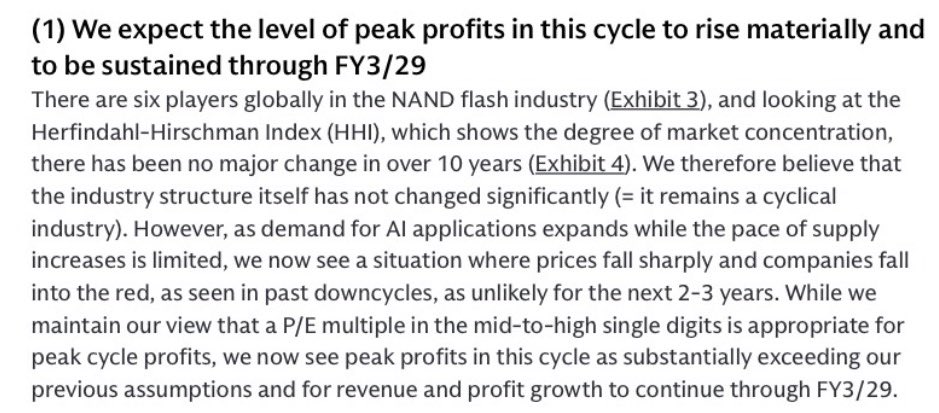

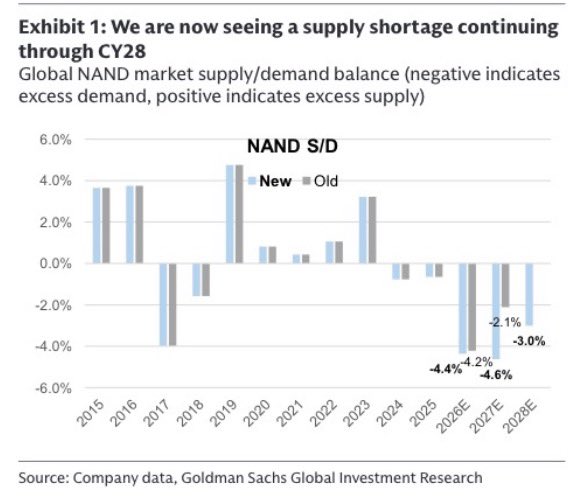

Goldman finally upgrades Kioxia 285A.JP to Buy and nearly doubled its PT from ¥48,000 to ¥93,000 and got materially more bullish on Kioxia and, by extension, the NAND cycle.

Peak profits are now expected to continue rising through FY3/29 instead of peaking materially earlier!

( ) Goldman now expects NAND supply tightness to persist through CY28

( ) Peak profits this cycle seen materially higher and more sustainable than previously assumed

( ) Samsung, SK Hynix and Micron continue prioritizing DRAM/HBM investment, limiting NAND supply growth

( ) DRAM procurement risk for enterprise SSDs appears largely resolved

( ) BiCS 8 transition expected to drive lower costs and stronger margins over time

( ) IR Day, quarterly results and continued NAND price increases seen as potential catalysts

Goldman isn’t arguing NAND has become a structurally different industry. They’re arguing the cycle itself has changed because AI demand is arriving while supply growth remains constrained.

Same cyclical industry, much higher earnings ceiling.

If NAND supply remains constrained because memory makers keep allocating capital toward DRAM/HBM, that should support the broader NAND ecosystem for longer than investors currently expect.

285A.JP $MU $005930.KS $000660.KS

1

18

2,896

Jun 11

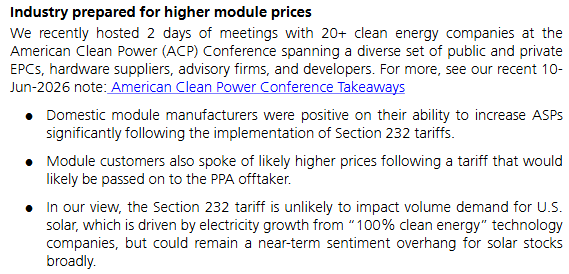

Interesting call here in $FSLR from UBS with a new Street high PT - raised from $290 to $330 because it believes Section 232 tariffs could push US solar module prices materially higher over the next few years.

One interesting part is that UBS doesn't think tariffs will meaningfully hurt demand. Instead, they see the higher costs largely being passed through, allowing domestic manufacturers to capture higher ASPs and stronger earnings.

1

11

1,436

Jun 10

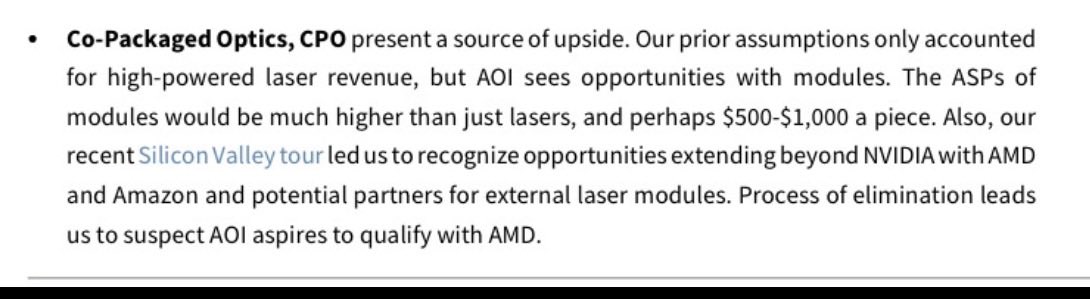

$AAOI x $AMD and $AMZN ?

RayJ pretty positive after co‘s investors meeting. Management’s message was that hyperscalers are still effectively buying whatever optical transceiver capacity they can get their hands on, which is why AAOI is racing to expand production. The company is targeting monthly capacity north of $450M by mid-2027, with new Texas tooling starting to come online this summer.

Management’s capacity plans seem far above Street expectations. Raymond James notes that AAOI’s 2H27 capacity target implies roughly $6B of annualized revenue versus consensus that remains far below that level. Their view is that earnings power at full utilization could be substantially higher than current estimates.

The other theme was share gains. Management believes future gains come primarily at the expense of Chinese competitors, while ongoing geopolitical tensions and supply-chain concerns increasingly favor US-based optical suppliers.

And then there’s CPO.

RayJ argues investors may still be underestimating the opportunity, particularly if AAOI can move beyond lasers and into higher-value optical modules. They also hint that AAOI could be positioning itself for future AMD qualifications in addition to existing AI infrastructure opportunities as well as Amazon as another potential partner.

1

4

15

1,546

Jun 10

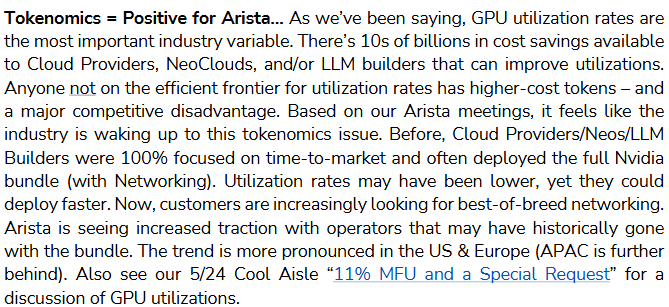

Maybe the wrong day, but nevertheless an interesting piece from Wolfe on Arista.

Wolfe came away from meetings with $ANET sounding increasingly constructive with the industry starting to care much more about GPU utilization and token economics than pure deployment speed. For years, cloud providers and AI builders often bought vertically integrated stacks because the priority was getting clusters online as quickly as possible. Now that AI infrastructure is scaling, the focus is shifting toward extracting more output from existing GPU fleets.

That's where Wolfe thinks Arista benefits.

They argue customers are becoming more willing to adopt best-of-breed networking rather than accepting bundled solutions, especially as improving utilization can translate into billions of dollars of savings. The firm also sees another tailwind from the rise of heterogeneous AI clusters. As customers deploy a mix of $NVDA and non-NVIDIA accelerators, network flexibility becomes increasingly important, which plays directly into Arista's strengths.

The supplychain debate, meanwhile, appears to be fading into the background. Wolfe says availability remains a challenge, but conditions are materially better than what management outlined earlier in the year.

1

11

1,844

Jun 10

SoftBank's talks to raise a $6B margin loan backed by its OpenAI stake have reportedly stalled, and the stock is already down around 9% in Asia. SoftBank is now exploring alternative funding options.

Negative xread for $ORCL:

If lenders are becoming more cautious about lending against OpenAI-related assets, investors may start questioning the financing assumptions behind Stargate and future AI infrastructure buildouts.

For Oracle, that could mean pressure on the AI narrative, delayed deployment expectations, and a lower valuation multiple even if underlying OpenAI demand remains strong.

Expecting a bad day for Oracle - already short, but please dyor.

Apr 28

SoftBank (-10% in its Asian session today) is the cleanest readthrough here so far: it’s basically a leveraged equity bet on OpenAI with its ~11% stake.

Oracle is a bit different here and arguably even riskier. It’s tied to -$300B in compute and data center buildout.

If OpenAI demand wobbles, $ORCL isn’t just a valuation story but a balance sheet story.

Short $ORCL today and seeing it even lower than early ARCA prints around $167 but pls dyor!

3

2

37

11,388

A hidden takeaway from UBS’s enterprise AI survey I want to add here:

UBS found that 60% of enterprises are now actively discussing token and compute costs as AI usage scales. Companies aren’t slowing adoption, but they’re becoming much more focused on efficiency and ROI.

That matters because UBS believes Google’s TPUs and AWS’s Trainium stack could offer a meaningful token-cost advantage versus competitors relying more heavily on third-party infrastructure.

If enterprises become more cost-sensitive, AWS and Google Cloud may actually gain share.

UBS believes rising scrutiny around token costs could favor vertically integrated platforms like Trainium and TPU, giving $AMZN and $GOOGL a potential cost advantage.

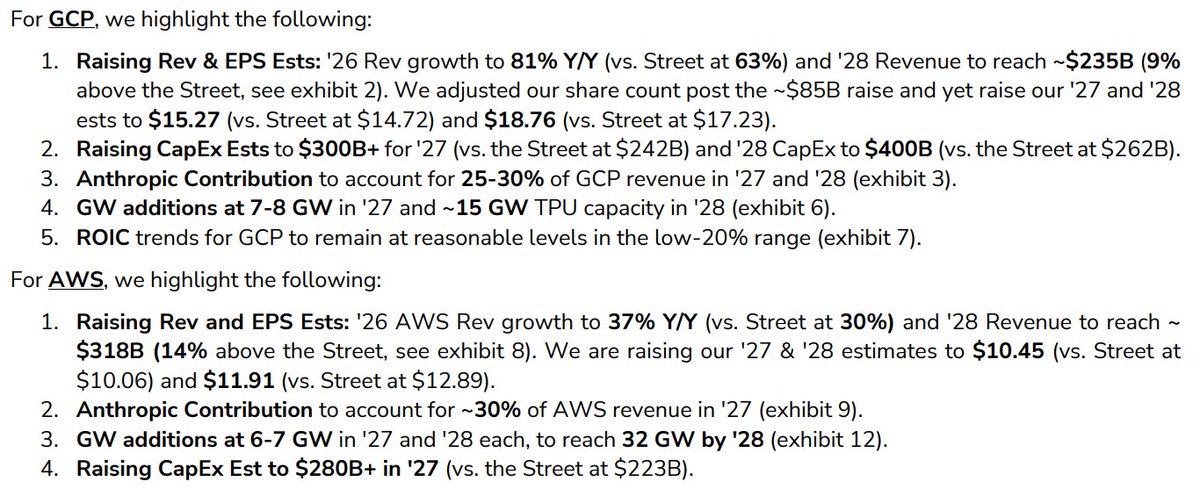

Wolfe raising ests for $GOOGL and $AMZN, well above street

$GOOGL $AMZN Deep Dive: Future of Hyperscalers - Raising Rev, CapEx, & EPS Ests. All Eyes On '28

We're raising ’26/'27 GCP Rev. growth to 81%/48% (11%/8% above Street) & '27 $GOOGL CapEx to $300B (26% above Street), & add 15GW in '28.

We're raising our ’26/'27 AWS Rev. growth to 37%/44% (6%/19% above Street) & '27 $AMZN CapEx to $280B (27% above Street), & add 6GW in ’28.

2

27

4,125

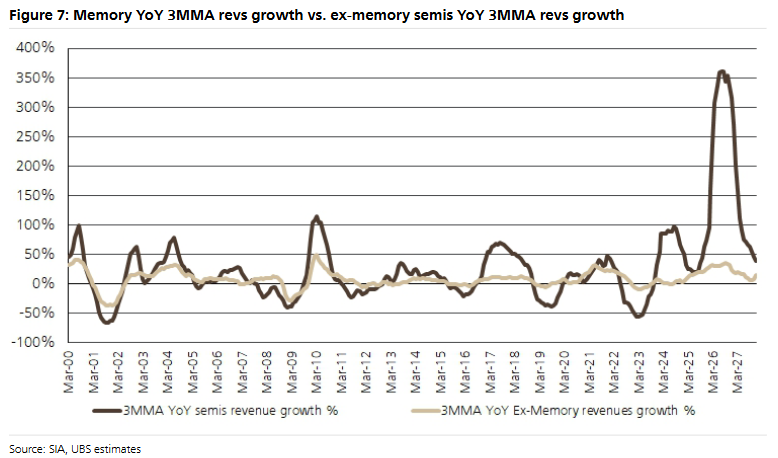

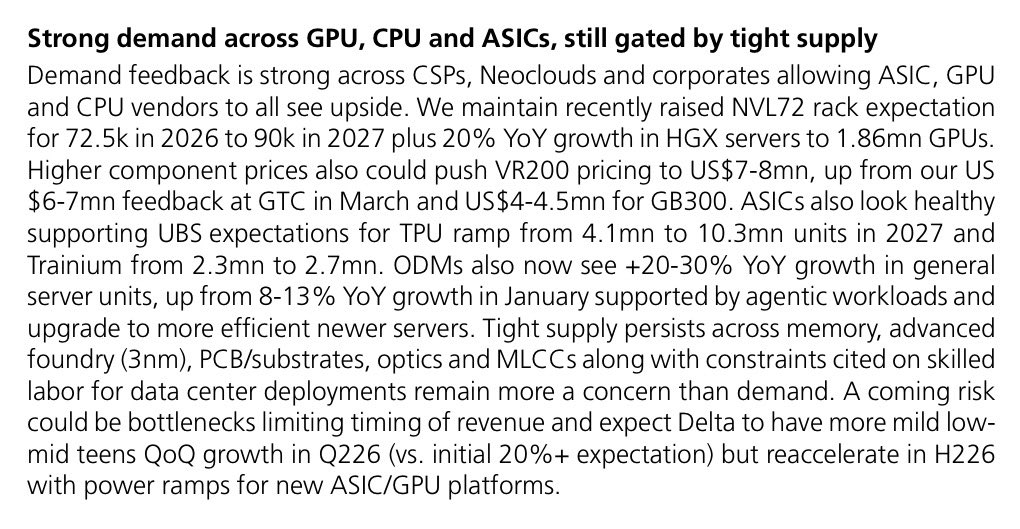

UBS just raised its semiconductor forecast to nearly $2.4T by 2027 but simultaneously arguing we're getting closer to a cycle peak.

AI is pulling forward growth across almost every layer of the stack - memory, CPUs, networking, power, NAND, HBM and logic - pushing industry revenue to levels few expected a year ago. UBS now sees memory as the biggest beneficiary, with AI demand extending well beyond accelerators into DRAM, LPDDR and NAND.

At the same time, some of the classic cycle indicators are flashing yellow.

UBS expects YoY semiconductor growth rates to start slowing from very elevated levels as we move through 2027, even if absolute revenues continue climbing. In other words, the industry may soon be growing from a much larger base.

Don´t get me wrong: The cycle isn't ending.

But all of us should probably start thinking about where we are in the cycle, not just how strong AI demand is.

$NVDA $MU $AMD $AVGO $MRVL $TSM $ASML

1

4

34

4,265

Knockouttrader retweeted

Jun 8

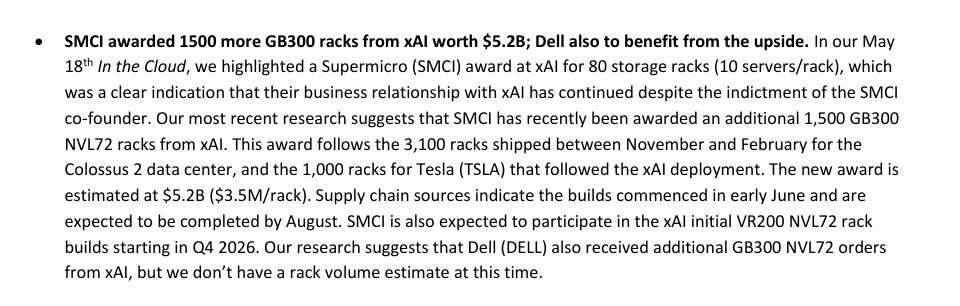

Bluefin has a rather interesting nugget on $SMCI today hidden on the second page.

Looks like Elon is so rack-hungry he doesn't mind some hairdryers consuming power too that in addition to 80 racks they awarded to SMCI, they've added 1500.

Incremental $5.2B positive.

2

4

54

28,035

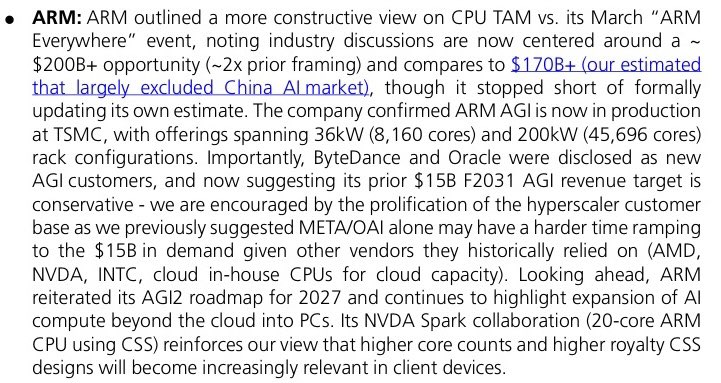

$200B was well known before, wasn’t it?

Nevertheless UBS still sounds pretty optimistic especially with $ARM itself calling some of its targets as conservative.

1

25

3,370

$CBRS new Buy at UBS, PT $300 … and I am no sure if I like its entire thesis. It still feels like an expensive alternative to „cheaper“ names.

UBS treating Cerebras less like a chip company and more like a bet on a very specific corner of the AI market: ultra-fast inference.

It argues Cerebras’ wafer-scale architecture avoids many of the bottlenecks that show up in traditional GPU systems by keeping compute and memory tightly integrated on a single giant chip. The result, in their view, is a premium inference platform that can outperform GPUs on certain latency-sensitive workloads.

What gets UBS excited is the potential AWS angle. They see a future where AWS combines Trainium for prefill and Cerebras for decode, creating a disaggregated inference architecture that could become increasingly common as AI workloads scale.

Related names:

$CBRS $NVDA $AMZN $MSFT

1

2

20

4,265

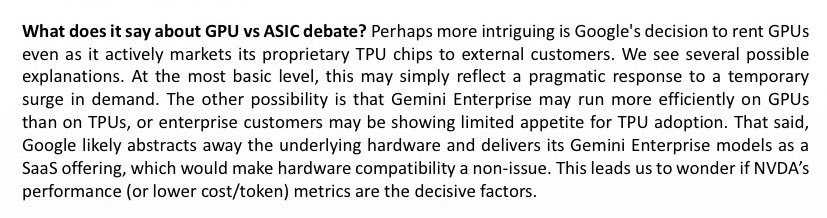

“Gemini may run better on GPUs than TPUs.”

That’s one of the more interesting conclusions RBC draws from reports that $GOOGL agreed to rent 110k GPUs despite aggressively promoting its own TPU platform.

It is just a guess, but the question remains:

Why would Google pay a premium for external GPU capacity if its internal TPU offering was the clear answer for every workload?

Either way, RBC views the agreement as another sign that NVIDIA’s competitive position remains extremely strong. The firm believes $NVDA still leads on deployment speed, performance-per-watt, and supply availability, with Rubin and Vera potentially extending those advantages further into 2027.

If GPU > TPU what about names like $AVGO again?

12

15

153

58,545

Adding UBS’ latest demand check here. Positive as well but not that big of a banger like Mizu

$MU $NVDA $ARM $AMD

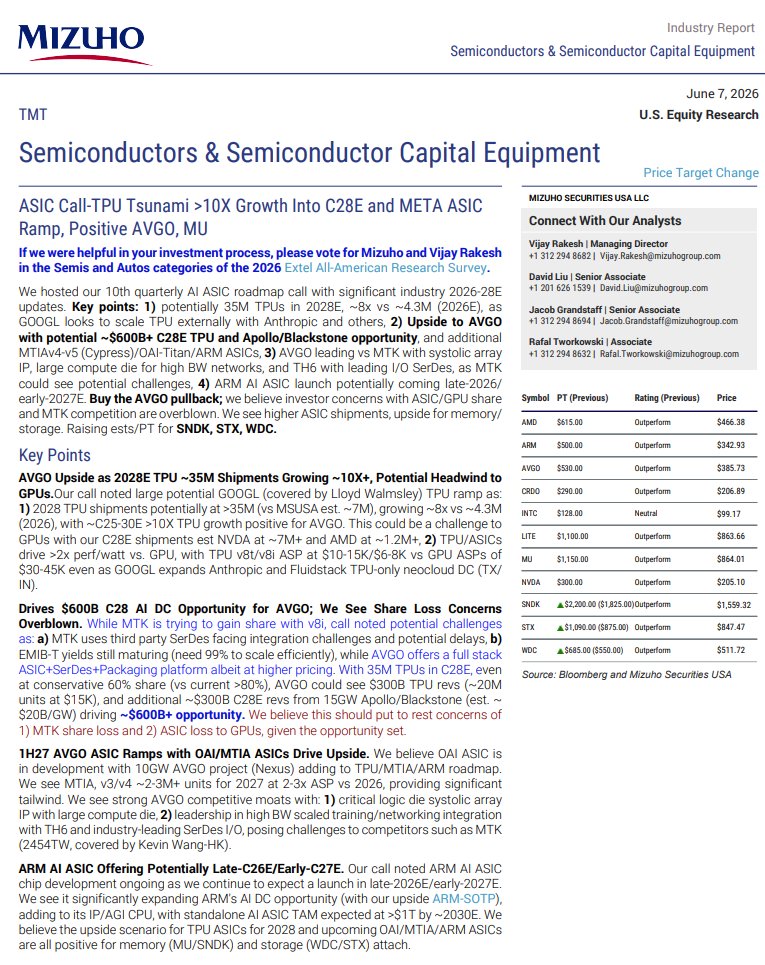

Jun 7

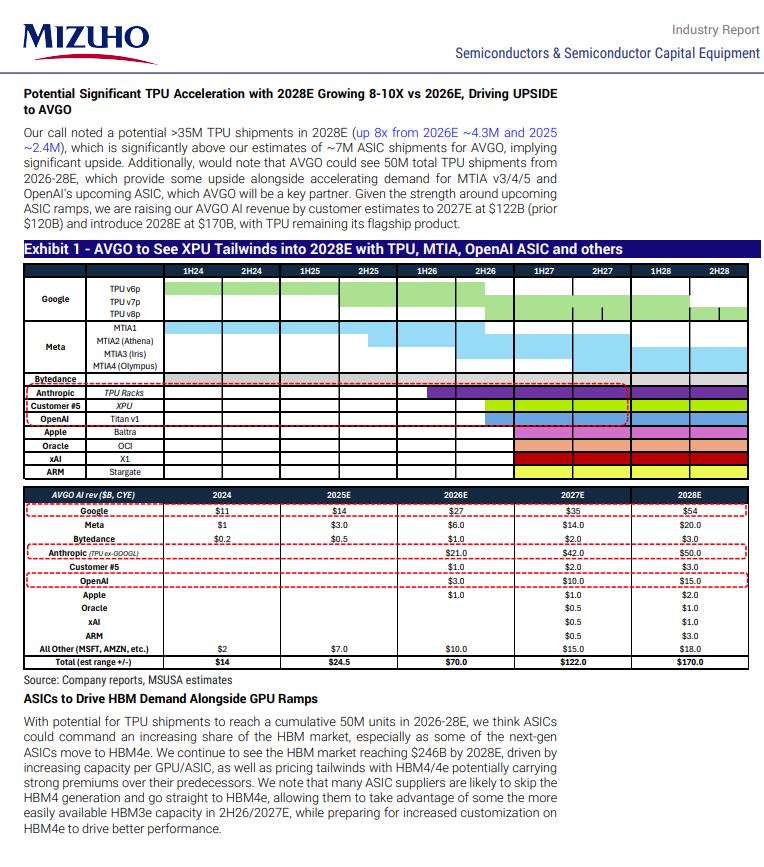

Mizuho ASIC channel checks: pounding table on $AVGO

"potential >35M TPU shipments in 2028E (up 8x from 2026E ~4.3M and 2025 ~2.4M), which is significantly above our estimates of ~7M ASIC shipments for AVGO"

"We believe OAI ASIC is in development with 10GW AVGO project (Nexus) adding to TPU/MTIA/ARM roadmap."

"Our call noted $ARM AI ASIC chip development ongoing as we continue to expect a launch in late-2026E/early-2027E"

" $MU : With potential for TPU shipments to reach a cumulative 50M units in 2026-28E, we think ASICs could command an increasing share of the HBM market, especially as some of the next-gen ASICs move to HBM4e"

1

41

3,066

Houston, we have a plan:

$NVDA ’s roadmap points toward 800VDC as the long-term architecture for Rubin-era clusters, with power conversion gradually moving away from individual racks and toward row-level and eventually facility-level systems.

UBS sees Delta (2308.TW) as one of the biggest beneficiaries of that shift. The company is already shipping solid-state transformers in China and is beginning to position itself around the next generation of AI power infrastructure, including SSTs, fuel cells, cooling, and high-density power delivery - creating multibillion dollar revenue opportunities over time.

Vertiv $VRT also came up repeatedly in the discussion. UBS views Vertiv as the early leader in row-level and facility-level power centers, with its 4.8MW-class solution positioning it well for the transition beyond traditional rack-based architectures.

1

24

15,353

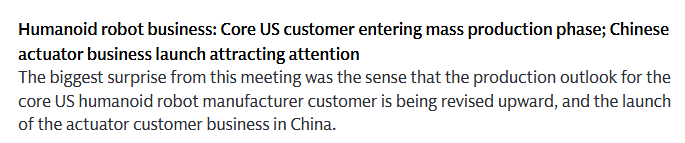

Next stop: Humanoids

Goldman came away from meetings with Harmonic Drive (6324.JP) noticeably more constructive on both the near-term order environment and the longer-term humanoid opportunity.

Management described demand from semiconductor equipment customers as exceptionally strong, while industrial robotics continues to recover.

Goldman now believes a key North American humanoid customer has now entered mass production, marking a potential inflection point for the business. The company also disclosed, for the first time, an actuator project with a Chinese humanoid customer, suggesting a second growth vector may be emerging.

Management emphasized that speculative ordering remains limited, channel inventories are healthy, and it remains committed to protecting margins despite intensifying competition.

Overall, Goldman sees the combination of recovering industrial demand, strong semiconductor equipment orders, and accelerating humanoid adoption as supporting a much stronger outlook than investors appreciated a year ago.

Goldman with a 12-month target price of ¥10,000 which implies around 40% upside from current levels.

4

7

69

47,161

Goldman may have just made one of the more important "second-order AI" calls I've seen recently.

It´s not about GPU or CPU ... It's about wafers - specifically, 300mm wafers.

Goldman believes 300mm wafers have entered a multi-year growth cycle driven by AI. AI servers already account for more than 20% of wafer demand, while GPU/ASIC deployments, HBM scaling, CoWoS, silicon photonics, and the rise of agentic AI are increasing semiconductor content across entire systems - not just accelerators. At the same time, next-generation memory architectures such as CBA NAND, 400 layer NAND, and eventually 3D DRAM could further increase wafer consumption per bit shipped. With supply growth slowing while demand continues to broaden, Goldman sees the setup becoming increasingly supportive for wafer pricing and profitability.

Goldman thinks the industry is moving away from the traditional "shrink more, use fewer wafers" model.

Instead, advanced packaging, stacking, bonding and AI system complexity are causing wafer consumption per unit to rise.

That's a subtle but potentially huge shift.

Potential beneficiaries:

( ) SUMCO (3436.JP) – largest estimate increase in the report

( ) Shin-Etsu (4063.JP) – stronger 300mm wafer pricing assumptions

( ) Resonac (4004.JP) – AI packaging materials outperforming expectations

( ) Mitsubishi Gas Chemical (4182.JP) – BT substrates and AI server materials

( ) Mitsui Kinzoku (5706.JP) – copper foil increasingly tied to package substrates

6

15

164

71,670

Follow up from Goldman after Furukawa Electrics Business Briefing:

The discussion for 5801.JP is now shifting toward whether three separate growth engines can all surprise to the upside at the same time: thermal, FITEL, and high-value copper foil.

( ) Water-cooled module revenue target of ¥400B by FY3/31 may prove conservative

( ) Thermal/electronic component profits targeted to grow ~15x from FY3/26 to FY3/31

( ) FITEL high-value optical products expected to grow at ~88% CAGR through FY3/27

( ) FITEL operating profits projected to increase ~10x by FY3/31

( ) Higher-end HVLP copper foil mix continues increasing, supporting margin expansion

( ) Goldman sees potential upside to both sales and profit targets across these growth businesses

(=) No new medium-term targets were announced; focus now shifts to execution and quarterly proof points

Even though imho it is hard to say estimates for 2031 might be conservative it underlines the positive long term outlook and keeps the story intact.

Goldman Sachs is actually a bit cautious on Furukawa 5801.JP near term despite remaining bullish longer term.

The new MMC connector ferrule capacity won’t meaningfully contribute until FY3/29, meaning the stock may need time before the AI optical upside fully shows up in earnings.

( ) New MMC/TMT ferrule plant supports growing demand from next-generation AI datacenter optical architectures

( ) Furukawa continues expanding its higher-margin optical/datacenter product mix

( ) Production capacity expected to increase by more than 1.5x versus current levels

( ) Existing partnerships with Sanwa Technologies and US Conec reinforce ecosystem positioning

(=) Mass production begins around FY3/29, making this more of a medium-term than near-term catalyst

1

20

5,356

$NVDA is already trying to save the day

AI compute demand isn't slowing down, and neither is the ecosystem to support it.

AI Clouds are built on NVIDIA’s full-stack, end-to-end AI factory platform. They’re expanding worldwide to bring accelerated computing closer to developers, enterprises, startups and nations scaling agentic AI. And this next-gen infrastructure powered by NVIDIA Vera Rubin is already in motion.

🌏 The global buildout is underway.

➡️ nvda.ws/4xgaPC6

#NVIDIAGTC

6

1,492

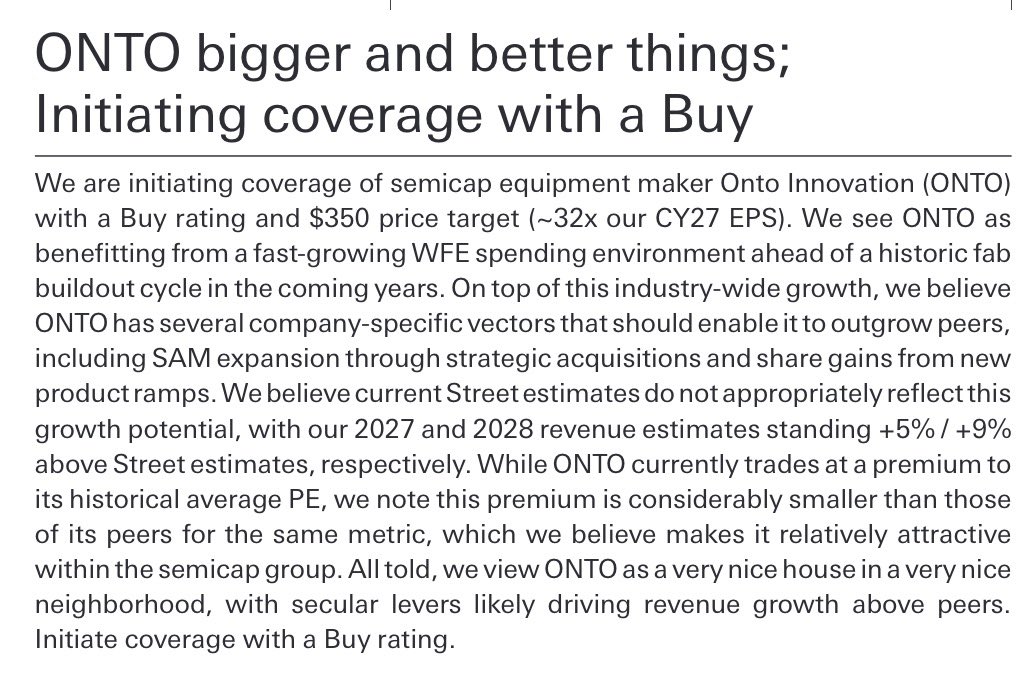

Deutsche Bank just initiated $ONTO with a Buy and the thesis is surprisingly simple:

AI is making semiconductor manufacturing more complex, and complexity requires more inspection, metrology and process control.

( ) DB sees ONTO as one of the best ways to play advanced packaging growth

( ) Advanced packaging exposure expected to rise from ~30% of sales to nearly 50% by 2028

( ) Revenue estimates sit 5% above Street for 2027 and 9% for 2028

( ) EPS estimates are 11% / 21% above consensus for 2027 / 2028

( ) New product wins at HBM and advanced packaging customers could help regain lost share

( ) Semilab acquisition and X-ray metrology expansion provide additional growth levers

(=) Competition remains intense, particularly from $KLAC

More HBM.

More 3D stacking.

More advanced packaging.

More Co-Packaged Optics.

All of that means more opportunities for ONTO’s inspection and metrology tools.

If AI keeps pushing complexity higher at the packaging layer, the beneficiaries aren’t just $ASML and $AMAT . Process control names like $ONTO and $KLAC may quietly become some of the biggest picks-and-shovels winners of the AI infrastructure cycle.

1

4

38

9,377