17 Dec 2025

TOP ANNOUNCEMENTS FOR THE DAY!!

#ANTONYWASTE: The company has secured MSW collection and transportation contracts worth Rs 1,330 crore from BMC for the collection and transportation of 1,250 MTPD of municipal solid waste.

#THAAICASTING: The company has received new orders of Rs. 76.76 crore for the supply of various automotive & non-automotive products.

#VLINFRA: The company has received a work order of Rs 42.12 crore from the Gujarat Water Supply & Sewerage Board.

#AKASHINFRA: The company has received a work order of Rs 18.21 crore from the Office of the Executive Engineer, Road and Building Division, Himmatnagar.

#SAMAYPROJECT: The company has received an LOI of Rs 18 crore from an International company to supply, fabricate, construct, freight, erect and commission the piping work.

#TEXMACORAIL: The company has been awarded an order of Rs 6.7 crore for the Rail Electrification contract from Western Railways.

#UNITEDDRILLING: The Company has secured an order worth Rs 4.05 crore from ONGC Ltd for the supply of Gas Lift Valve.

#DYNAMICSERVICES: The company has received a work order of Rs 2.06 crore from Eastern Railway for Supply of Low Maintenance Lead Acid Stationary Secondary Cells

2

37

5,517

18 Oct 2025

TOP ANNOUNCEMENTS FOR THE DAY!!

#Sterlingwilson: The company has secured three new orders worth Rs 1772 crore.

#KPIgreen: The company has received three Letters of Award of Rs. 696.5 crore from SJVN Limited for a major 200 MW (AC) Solar Power Project.

#HFCL: The company has secured an export order worth Rs 281.20 crore for the supply of Optical fibres

#MandBengineering: The company has secured an export order worth Rs 212 crore for the manufacturing and supply of Pre-Engineered Buildings to its customer in the USA.

#Genesysinternational: The Company has secured a business contract for Native Navigation and ADAS Maps from Tata Motors Passenger

#Bondadaengineering: The company's wholly owned subsidiary has received a Letter of Intent of Rs 13.29 crore from M/s. JMR Clean Energy Private Limited.

#Acstechnologies: The company has received a work order of Rs 3.55 crore from the Indian Navy.

#SamayProject: The company has received an LOI from an International company to supply Vertical Turbo Pumps with Motor for a total consideration of Rs.2.56 crores.

#DroneAcharya : The company has received a work order of 1.09 crore by the Indian Army for the supply of 180 First-Person View drones.

3

1,176

17 Oct 2025

TOP ANNOUNCEMENTS FOR THE DAY!!

#Sterlingwilson: The company has secured three new orders worth Rs 1772 crore.

#KPIgreen: The company has received three Letters of Award of Rs. 696.5 crore from SJVN Limited for a major 200 MW (AC) Solar Power Project.

#HFCL: The company has secured an export order worth Rs 281.20 crore for the supply of Optical fibres

#MandBengineering: The company has secured an export order worth Rs 212 crore for the manufacturing and supply of Pre-Engineered Buildings to its customer in the USA.

#Genesysinternational: The Company has secured a business contract for Native Navigation and ADAS Maps from Tata Motors Passenger

#Bondadaengineering: The company's wholly owned subsidiary has received a Letter of Intent of Rs 13.29 crore from M/s. JMR Clean Energy Private Limited.

#Acstechnologies: The company has received a work order of Rs 3.55 crore from the Indian Navy.

#SamayProject: The company has received an LOI from an International company to supply Vertical Turbo Pumps with Motor for a total consideration of Rs.2.56 crores.

#DroneAcharya : The company has received a work order of 1.09 crore by the Indian Army for the supply of 180 First-Person View drones.

10

161

29,628

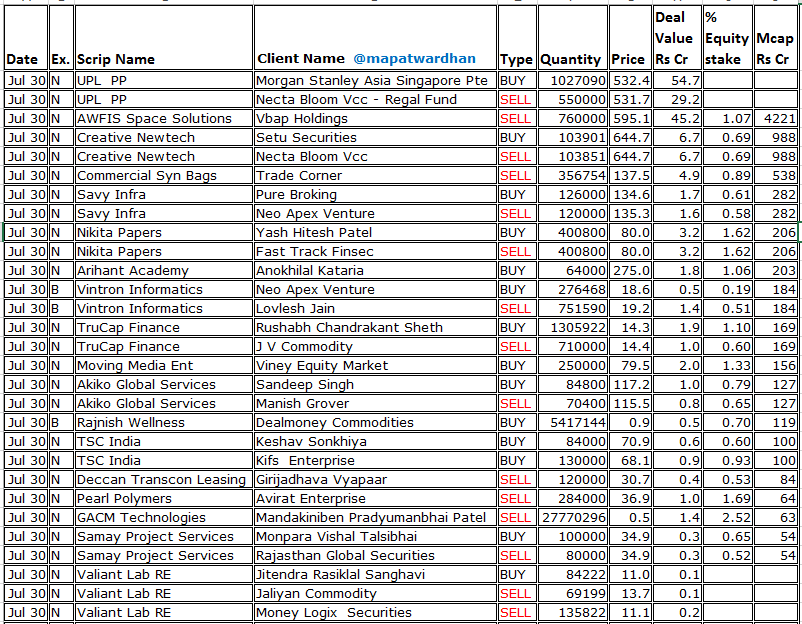

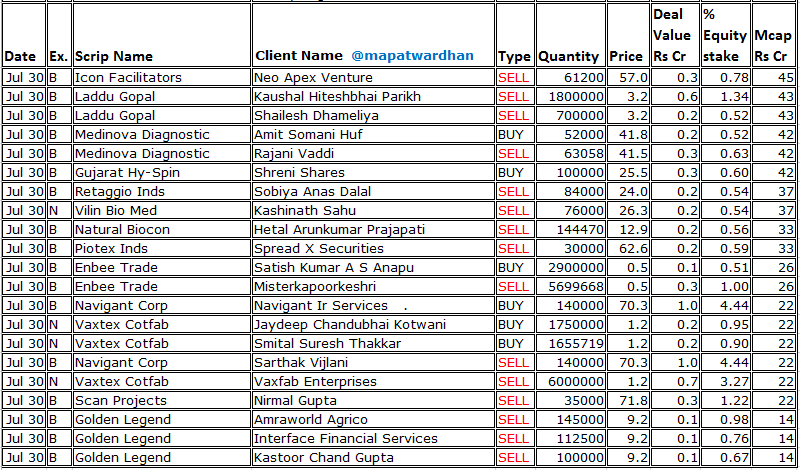

30 Jul 2025

*Today's bulk deals*

#AWFISSpace #CreativeNewtech #CommercialSynBags #SavyInfra #NikitaPapers #ArihantAcademy #VintronInformatics #TruCapFinance #MovingMediaEnt #AkikoGlobal #RajnishWellness #TSCIndia #DeccanTranscon #PearlPolymers #GACMTech #SamayProject #UPL #ValiantLab

1

14

2,154

23 Jun 2025

#MarketsWithBS | #SamayProject shares make positive D-Street debut, list at 6% premium

#Markets #sharemarket #StockMarket

mybs.in/2enq7o6

2

1,447

19 Jun 2025

#MarketsWithBS | #SamayProject Services IPO allotment today; check status, GMP, listing date

#markets #sharemarket #IPOAlert #StockMarket

mybs.in/2enoGge

1

3

1,365

18 Jun 2025

#MarketsWithBS | Last day! Samay Project IPO closes today; subscription rises 2x, GMP nil

#Stocks #markets #stockmarketindia #stockmarketnews #sharemarket #SamayProject #IPO

mybs.in/2ennmw6

1,307

17 Jun 2025

#MarketsWithBS | Samay Project IPO Day 2 update; check subscription status, GMP, key dates. Details here

#Stocks #markets #stockmarketindia #stockmarketnews #sharemarket #SamayProject #IPO

mybs.in/2ennLFm

1

1,534

16 Jun 2025

Samay Project Services Limited ( NSE SME IPO ) Analysis -

IPO Details -

IPO Date: 16 – 18 June 2025

Price Band: ₹32 – ₹34 per share

Lot Size: 4000 shares

Face Value: ₹10 per share

IPO Size: ₹14.69 crore ( 100% Fresh )

Business Summary -

Incorporated in 2001 as Samay Project Services Private Limited under the Companies Act, 1956.

Provides Engineering, Procurement and Construction ( EPC ) services.

Core expertise in design, engineering, supply, fabrication, erection and commissioning of Balance of Plant ( BOP ) systems.

Key service areas -

Piping Systems

Tanks, Vessels, and Fabricated Structures

Fire Protection, Detection & Firefighting Systems ( FFS )

Services multiple industries needing BOP & FFS solutions.

Financial Highlights ( Crores ) -

Net Worth -

FY25: ₹20

FY24: ₹16

FY23: ₹11.42

Total Revenue -

FY25: ₹37.72

FY24: ₹40.95

FY23: ₹20.82

Profit After Tax ( PAT ) -

FY25: ₹4.19 ( Margin - 11.29% )

FY24: ₹4.62 ( Margin - 11.33% )

FY23: ₹3.44 ( Margin - 16.88% )

Earnings Per Share ( EPS ) -

FY25: ₹3.80

FY24: ₹4.18

FY23: ₹3.12

Net Asset Value ( NAV ) per Share -

FY25: ₹18.34

FY24: ₹14.54

FY23: ₹10.35

Total Borrowings -

FY25: ₹2.09

FY24: ₹2.35

FY23: ₹2.99

Pros / Strengths -

Strong Order Book: ₹57 crore as on March 31, 2025.

PSU Projects: Works with reputed PSUs like #BHEL, Engineering Projects ( India ) Ltd., BCG Vaccine Laboratory — lower cancellation risk.

Diversified Revenue Streams -

Tanks, Vessels & Fabricated Structures - ₹8.89 crore ( 23.93% in FY25 )

Piping Systems: ₹6.55 crore ( 17.64% in FY25 )

Combined Piping & Tanks: ₹10.08 crore ( 27.14% in FY25 )

Fire Fighting System: ₹11.62 crore ( 31.29% in FY25 )

Technical Expertise - Handles various pipe materials:

Carbon Steel, Galvanized, Stainless Steel, Ductile Iron, High-Temperature Alloy Steel ( SA 335 P11 & P22 )

Pipe sizes from 15 NB to 1600 NB; large cooling water headers from 350 NB to 1500 NB.

Certified Company - ISO 9001:2015 for engineering, supply, fabrication, erection, testing & commissioning.

Builds Large Storage Tanks - For fire water, demineralized water, condensate, HFO, slurries ( limestone, gypsum ), wastewater, process water, auxiliary absorbent tanks.

Cons / Weaknesses -

Industry Risk - Relies on EPC demand across multiple industries. Any slowdown affects revenue.

Sector Dependency -

Power Sector - 51% revenue ( ₹18.97 crore )

Iron & Steel - 19.91% revenue ( ₹7.39 crore )

Geographical Concentration: Heavy dependency on one state -

#Telangana - ₹15.72 crore ( 42.33% of total revenue in FY25 )

#Orissa - ₹5.55 crore ( 14.94% of total revenue in FY25 )

Raw Material Procurement Concentration -

#Maharashtra - ₹8.44 crore ( 42.75% )

#TamilNadu - ₹7.10 crore ( 35.96% )

Combined - 78% from these two states.

Customer Concentration Risk: Heavy reliance on few customers -

FY25 -

Top 5 customers - 63% of revenue

Top 10 customers - 84% of revenue

I am Not Sebi Registered ...Views are Personal . DYDD

Apply Or Avoid Decision Upto 18 June ,,, 2 P.M

#Samayproject #Smeipo

#IPOAlert

4

909