Jun 11

What if your tickets, assets, and patches worked together?

Motadata ServiceOps brings ITSM, asset management, and patch management together with AI-powered automation.

motadata.com/products/servic…

#motadata #serviceops #itsm #enterpriseit

1

1

14

Jun 10

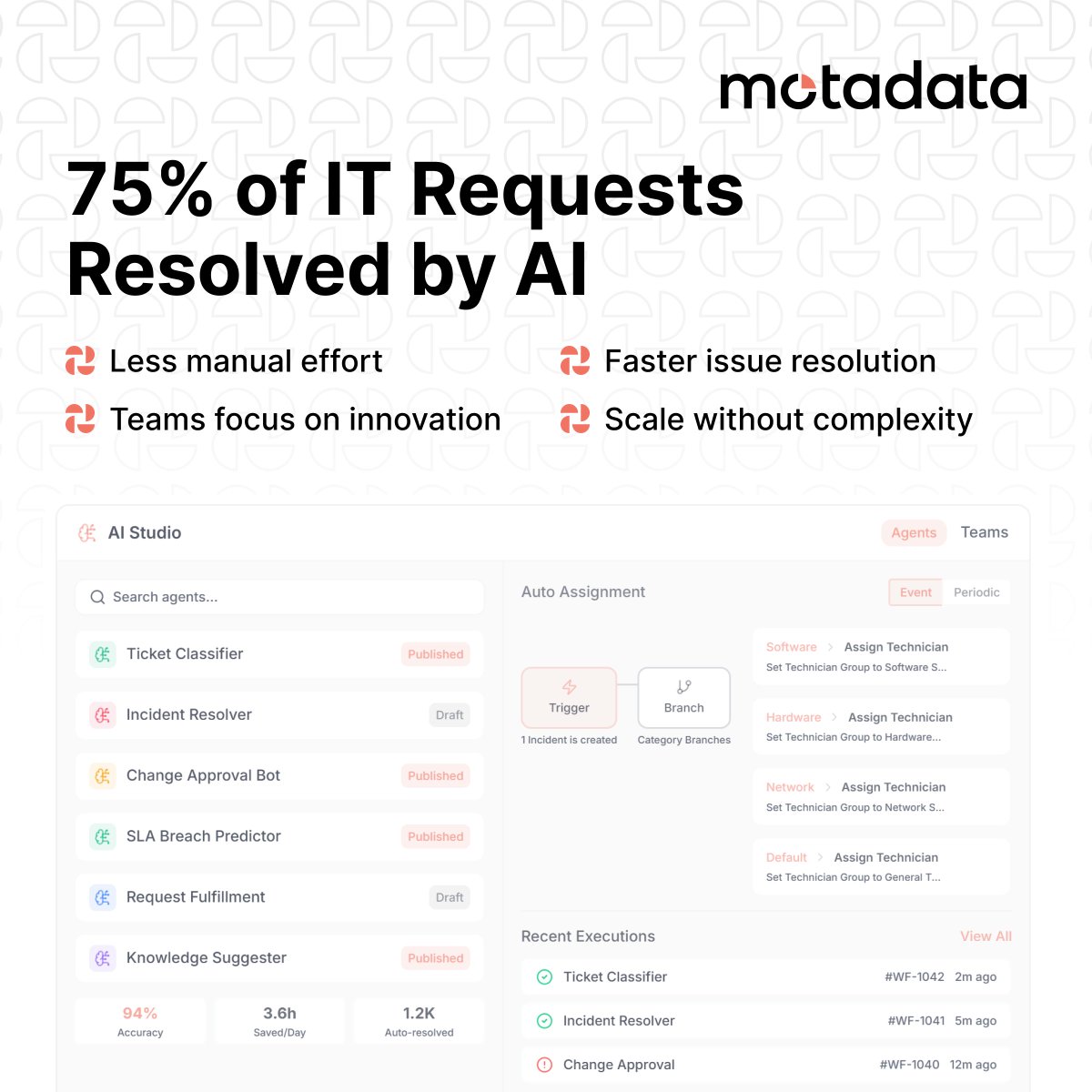

Virtual agents can resolve up to 75% of IT requests, improving IT efficiency and reducing manual work.

With Motadata ServiceOps Agentic AI & Orchestration, automate routine tasks with ease.

Learn more: motadata.com/products/agenti…

Source: Atlassian Report

#motadata #agenticai

1

1

18

May 9

Freshworks Inc. $FRSH

Delivering Uncomplicated AI-Powered Service Software for Exceptional Customer & Employee Experiences

Freshworks Inc. $FRSH, founded in 2010 and headquartered in San Mateo, California, is a leading SaaS company that builds intuitive, enterprise-grade software to power customer experience (CX) and employee experience (EX) operations. As businesses grapple with rising complexity in support, IT service management, and operations amid the AI boom, Freshworks helps organizations deliver faster, smarter, and more personalized service—driving efficiency, loyalty, and productivity across nearly 75,000 customers worldwide, including Bridgestone, New Balance, S&P Global, and Sony Music.

At the heart of $FRSH is its Freddy AI platform—a people-first AI approach embedded natively across its suite. Key capabilities include conversational AI agents that autonomously resolve up to 80% of queries, AI copilots for real-time agent assistance (summarization, reply suggestions, sentiment analysis), intelligent routing, predictive insights, and no-code Agent Studio for custom workflows. Flagship products like Freshdesk Omni (omnichannel CX), Freshservice (ITSM with integrated asset/operations management), Freshsales, and more offer seamless unification of CX and EX, rapid deployment, and strong ROI through lower drive times, higher resolution rates, and scalable automation.

Strategically, $FRSH is capitalizing on the AI-driven transformation in customer support, IT/HR service desks, and enterprise operations. Recent highlights include Q1 2026 results with $228.6M revenue ( 16% YoY, beating estimates), record-large deals (including the first $1M ARR), strong EX momentum (surpassing $500M ARR earlier), AI adoption growth, the FireHydrant acquisition for incident management, an 11% workforce optimization for efficiency, and a $400M share buyback. With 2026 guidance around $958M revenue and focus on upmarket expansion, agentic AI, and ServiceOps unification, Freshworks is positioned for continued profitable growth in the exploding market for intelligent service platforms.

2

747

Apr 28

🚨 lnkd.in/gAizGvsh NEW Podcast Alert! "I don’t look at my career as a straight line; I look at it as a winding road where the high-friction turns gave me the most grip." That was the show-stopping moment from my conversation with Murali Swaminathan, CTO of Freshworks, on the Ctrl Alt Podcast with Vida Patil. Murali Swaminathan is the architect of the $100B ServiceOps frontier, bringing 30 years of high-stakes engineering judgment - from scaling ServiceNow’s $3.5B flagship portfolio to leading the Agentic AI revolution as CTO of Freshworks.

🎥 Link to the FULL PODCAST here -> lnkd.in/gAizGvsh

🤖 With Anthropic launching frontier AI and features like "Computer Use" [act on your behalf] and agents finally moving from "cool demo" to "enterprise deployment," the stakes have never been higher. We aren't just talking about automation anymore - we’re talking about the next $100 Billion frontier in SaaS. Leaders like Murali are building the context and trust layer (the "Freddy Agentic AI" platform) that makes this safe for an enterprise to actually use. Anthropic just gave Claude a set of hands with 'Computer Use,' but Murali Swaminathan is teaching the enterprise how to give it a brain.

🧠 Murali has spent 30 years building the "grip" required to lead this shift. From scaling ServiceNow’s flagship portfolio from $1B to $3.5B , to now architecting the Freddy AI Agent platform for 8000 customers, his playbook is built on one core truth: Simplicity is the ultimate product strategy.

📊 The CxO Playbook for the Agentic Era:

⚔️ Kill the "Complexity Tax":

Most enterprises are drowning in tool sprawl. If your AI doesn't consolidate your stack, it's just adding to the noise.

🔍 From Assertion to Audit:

Boardrooms don’t want promises of "Ethical AI"- they want systems that prove it. Murali breaks down how to build governance into the code, not just the marketing.

🧩 The "Winding Road" Advantage:

Your "random" past experiences in GRC, search, or infra aren't detours. They are your competitive moat in the ever changing world of AI landscape with a need for constant adaptability and risk taking.

🏗️ Murali’s journey through Liquid Software Corporation, @Niku, CA Technologies, Recommind (now OpenText), and ServiceNow has led to this moment. The hottest tech isn't the LLM - it’s the engineering judgment behind it.

❓ The Question for Leaders:

Are you building for the next hype cycle, or are you building for the "long arc" of impact?

Thank you Erika Howard Julie L. Cathy Toscano for enabling this amazing conversation 🙏😊

#AgenticAI #Freshworks #SaaS #Leadership #CtrlAltPodcast #SiliconValley

#CTO a16z speedrun ServiceNow Raido Capital OpenText Recommind (now OpenText) NIKŪ Corporation Wipro #CMCLimited

1

2

138

Apr 18

6. $NOW - ServiceNow

ServiceNow is a leading cloud platform specializing in enterprise workflow automation.

Its Now Platform provides a unified, AI-native architecture that integrates workflows, data, and automation across IT, HR, customer service, and security operations, creating a highly differentiated offering in a fragmented market.

ServiceNow’s generative AI product, Now Assist, surpassed $600 million in annual contract value, more than doubling year over year and tracking toward $1 billion in 2026.

Platform usage continues to scale with workflow transactions growing 33% YoY to 80 billion, monthly active users 25% YoY, and ITOM NNACV 50% YoY, with ServiceOps included in 16 of the top 20 deals.

ServiceNow is positioning itself as the “AI agent control tower” for enterprise operations, coordinating autonomous agents across departments and workflows.

Strategic acquisitions (Veza and Armis) expand its addressable market to $125 billion, particularly in security and risk management.

As AI automates a growing share of enterprise workflows, ServiceNow is well positioned to become the central orchestration layer of intelligent enterprise operations.

37

12,812

Apr 17

Great conversations, strong momentum, and valuable connections at NADITA 2026.

Over the past few days, we engaged with leaders across the Caterpillar dealer ecosystem, exchanging perspectives on ERP-led transformation, AI, and what it takes to drive real outcomes across service, parts, and aftermarket operations.

Thank you to everyone who stopped by Booth #1—we look forward to continuing these conversations beyond the event.

#NADITA2026 #DealerTransformation #ERP #AI #Aftermarket #ServiceOps #Birlasoft #Caterpillar

2

50

"I already told someone this last week."

Customer frustration isn’t emotional. That's your CRM failing.

When context is missing, every conversation starts from zero.

#CustomerExperience #CRMTruths #ServiceOps

3

25

Mar 7

3. $NOW - ServiceNow

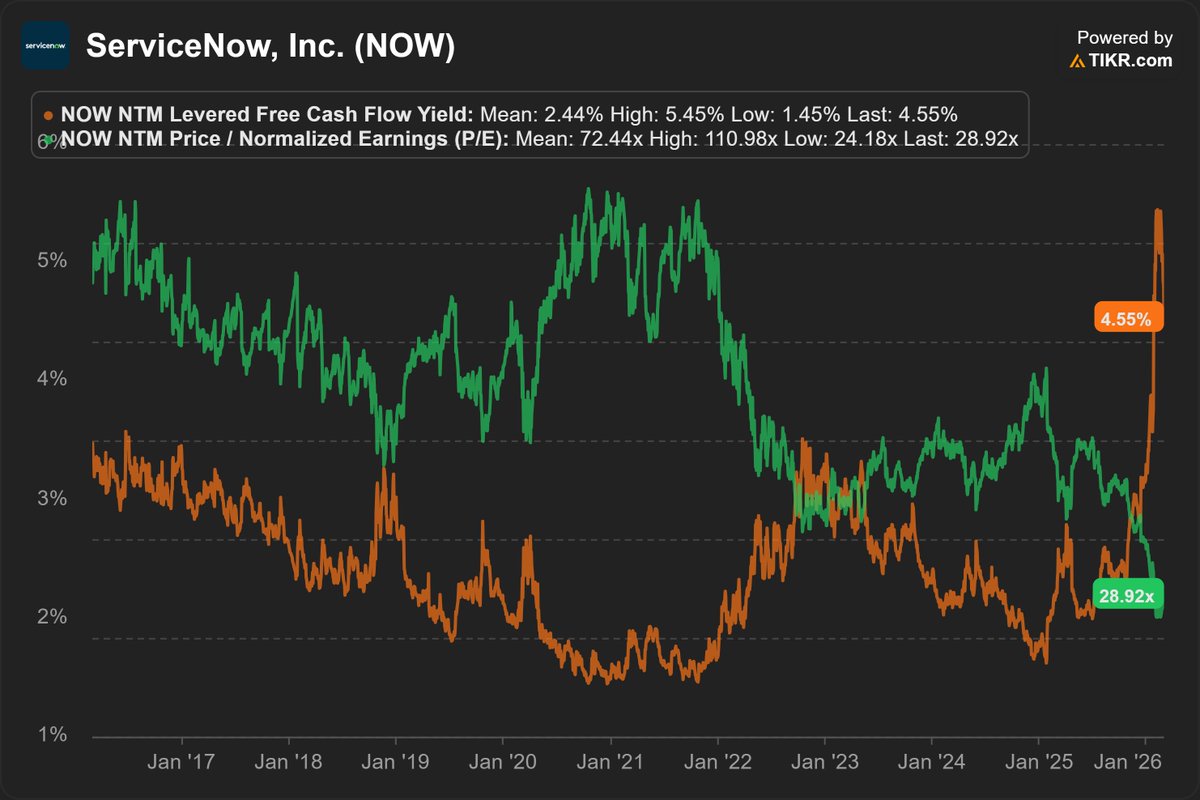

Despite recovering roughly 20% over the past month, ServiceNow remains one of the worst-performing large-cap software stocks over the past year, with shares down nearly 45% and at one point experiencing a 57% drawdown, the largest decline in its public history.

ServiceNow’s Now Platform delivers a unified, AI-native architecture that integrates workflows, data, and automation across IT, HR, customer service, and security operations. This integrated architecture allows enterprises to orchestrate operations through a single workflow platform, something many competitors struggle to replicate due to fragmented product portfolios.

ServiceNow’s generative AI product, Now Assist, surpassed $600 million in annual contract value, more than doubling year over year and tracking toward $1 billion in 2026.

Q4 alone included 35 deals over $1 million, nearly 3× QoQ, with customers materially expanding usage upon renewal (including one large enterprise expanding entitlements 13×). Deals involving five or more Now Assist products increased more than 10× YoY.

Platform usage continues to scale with workflow transactions growing 33% YoY to 80 billion, monthly active users 25% YoY, and ITOM NNACV 50% YoY, with ServiceOps included in 16 of the top 20 deals.

ServiceNow is positioning itself as the “AI agent control tower” for enterprise operations, coordinating autonomous agents across departments and workflows.

Strategic acquisitions such as Veza and Armis could expanded ServiceNow’s security and risk addressable market to approximately $125 billion, enabling unified governance across IT, operational technology (OT), and IoT environments.

As AI automates a growing share of enterprise workflows, ServiceNow is well positioned to become the central orchestration layer of intelligent enterprise operations.

1

29

17,936

"𝗠𝗼𝘀𝘁 𝗹𝗮𝗿𝗴𝗲 𝗰𝗼𝗺𝗽𝗮𝗻𝗶𝗲𝘀 𝗮𝗿𝗲𝗻'𝘁 𝘀𝘁𝗿𝘂𝗴𝗴𝗹𝗶𝗻𝗴 𝘄𝗶𝘁𝗵 𝗔𝗜 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝘁𝗵𝗲 𝘁𝗲𝗰𝗵𝗻𝗼𝗹𝗼𝗴𝘆 𝗶𝘀𝗻'𝘁 𝗿𝗲𝗮𝗱𝘆. 𝗧𝗵𝗲𝘆'𝗿𝗲 𝘀𝘁𝗿𝘂𝗴𝗴𝗹𝗶𝗻𝗴 𝗯𝗲𝗰𝗮𝘂𝘀𝗲 𝗔𝗜 𝗳𝗼𝗿𝗰𝗲𝘀 𝗱𝗲𝗰𝗶𝘀𝗶𝗼𝗻𝘀 𝗼𝗿𝗴𝗮𝗻𝗶𝘇𝗮𝘁𝗶𝗼𝗻𝘀 𝘄𝗲𝗿𝗲 𝗻𝗲𝘃𝗲𝗿 𝘄𝗶𝗹𝗹𝗶𝗻𝗴 𝘁𝗼 𝗺𝗮𝗸𝗲 𝗲𝘅𝗽𝗹𝗶𝗰𝗶𝘁." — Shiva Ramani, CEO, iOPEX.

That cuts to the heart of why 56% of enterprises report no meaningful ROI from AI, despite sustained investment.

In our latest blog, we break down 5 structural shifts redefining enterprise operations in 2026:

1. 𝗛𝘆𝗽𝗲𝗿𝗮𝘂𝘁𝗼𝗺𝗮𝘁𝗶𝗼𝗻 𝗮𝘀 𝗶𝗻𝗳𝗿𝗮𝘀𝘁𝗿𝘂𝗰𝘁𝘂𝗿𝗲, not a project

2. 𝗔𝘂𝘁𝗼𝗻𝗼𝗺𝗶𝗰 𝘀𝘆𝘀𝘁𝗲𝗺𝘀 built to never break, not just fix fast

3. 𝗖𝗼𝗻𝘁𝗶𝗻𝘂𝗼𝘂𝘀 𝗣𝗿𝗼𝗰𝗲𝘀𝘀 𝗢𝗯𝘀𝗲𝗿𝘃𝗮𝗯𝗶𝗹𝗶𝘁𝘆 replacing quarterly audits

4. 𝗖𝗼𝗺𝗽𝗼𝘀𝗶𝘁𝗲 𝗔𝗜 replacing single-model strategies

5. 𝗚𝗼𝘃𝗲𝗿𝗻𝗮𝗻𝗰𝗲-𝗮𝘀-𝗖𝗼𝗱𝗲 making trust an engineering standard

𝗜𝗳 𝘆𝗼𝘂𝗿 𝘁𝗿𝗮𝗻𝘀𝗳𝗼𝗿𝗺𝗮𝘁𝗶𝗼𝗻 𝘀𝘁𝗶𝗹𝗹 𝗱𝗲𝗽𝗲𝗻𝗱𝘀 𝗼𝗻 𝗵𝘂𝗺𝗮𝗻𝘀 𝘀𝘁𝗶𝘁𝗰𝗵𝗶𝗻𝗴 𝘀𝘆𝘀𝘁𝗲𝗺𝘀 𝘁𝗼𝗴𝗲𝘁𝗵𝗲𝗿, 𝘁𝗵𝗲 𝗿𝗶𝘀𝗸 𝗶𝘀 𝗮𝗹𝗿𝗲𝗮𝗱𝘆 𝗰𝗼𝗺𝗽𝗼𝘂𝗻𝗱𝗶𝗻𝗴.

Read the full breakdown: shorturl.at/qmYHu

#DigitalTransformation #AgenticAI #EnterpriseAI #Hyperautomation #AIStrategy #IntelligenceAsAService #ServiceOps #RevenueOps

2

22

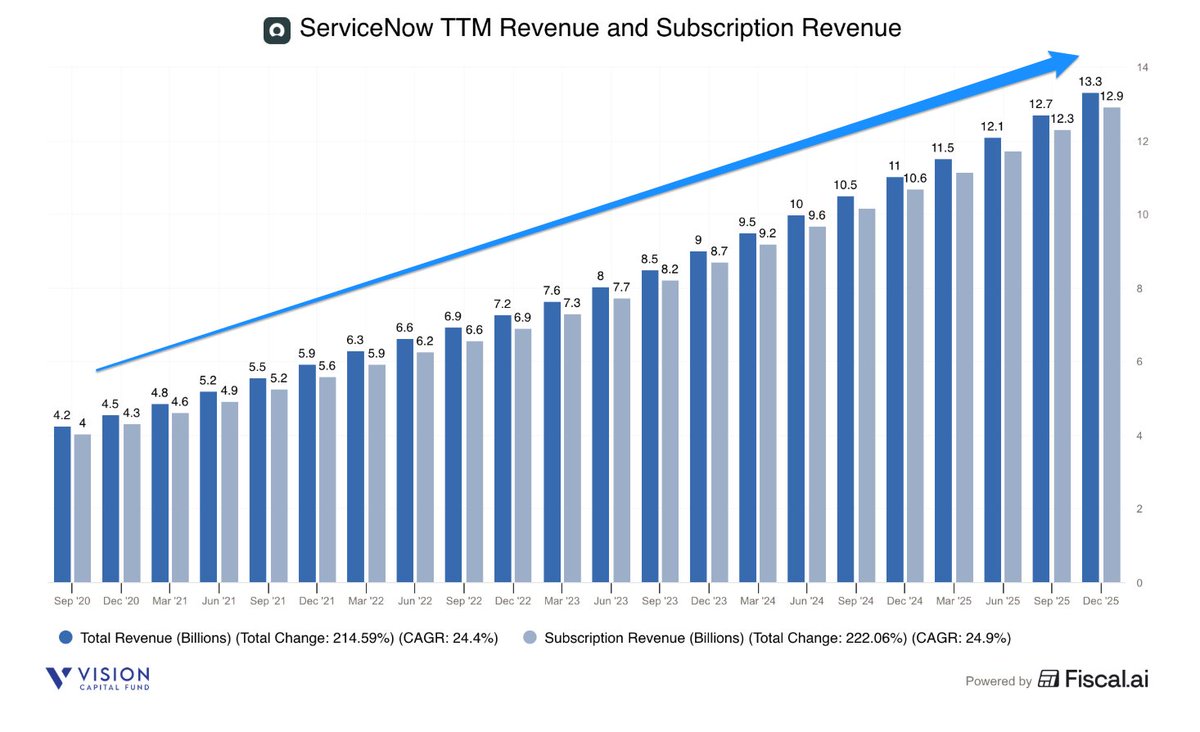

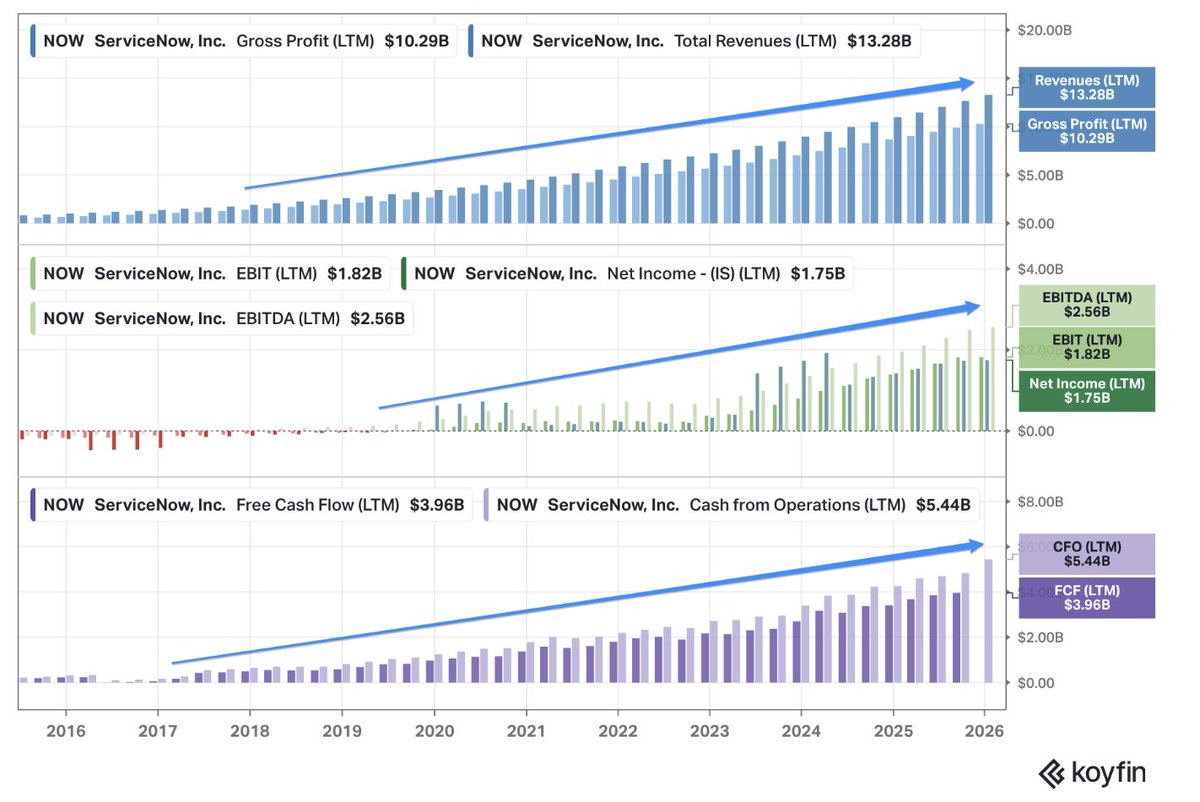

ServiceNow $NOW 4Q25 Earnings

- Rev $3.6b 21% ↗️🟢

- Subscription Rev $3.5b 21% ↗️🟢

- Pro Svcs Rev $0.1b 12% ↗️🟡

- GP $2.7b 18% ↗️🟢 margin 77% -204 bps ↘️🔴

- NG EBIT $1.1b 26% ↗️🟢 margin 31% 137 bps ✅

- EBIT $0.4b 18% ↗️🟢 margin 12% -23 bps ↘️🔴

- NG Net Inc $1b 25% ↗️🟢 margin 27% 87 bps ✅

- Net Inc $0.4b 4% ↗️🟡 margin 11% -175 bps ↘️🔴

- OCF $2.2b 37% ↗️🟢 margin 63% 743 bps ✅

- FCF $2b 45% ↗️🟢 margin 57% 961 bps ✅

4Q25 Biz Metrics

- CRPO $12.9b 25% ↗️🟢

- RPO $28.2b 27% ↗️🟢

- >$1m ACV 244 40%

- No. of cust >$5m ACV 603 20% ↗️🟢

- Avg ACV of cust >$5m ACV $14.7m 5% ↗️🟡

- Net new ACV across workflows: 47% tech, 31% CRM, 22% creator

- 98% renewal rates ➡️✅

- Rev by geography: NA 63%, EMEA 26%, APAC 11%

FY25 Earnings

- Rev $13.3b 21% ↗️🟢

- Subscription Rev $12.9b 21% ↗️🟢

- Pro Svcs Rev $0.4b 17% ↗️🟢

- GP $10.3b 18% ↗️🟢 margin 78% -164 bps ↘️🔴

- NG EBIT $4.1b 28% ↗️🟢 margin 31% 162 bps ✅

- EBIT $1.8b 34% ↗️🟢 margin 14% 132 bps ✅

- NG Net Inc $3.7b 26% ↗️🟢 margin 28% 121 bps ✅

- Net Inc $1.7b 23% ↗️🟢 margin 13% 19 bps ✅

- OCF $5.4b 28% ↗️🟢 margin 41% 215 bps ✅

- FCF $4.6b 34% ↗️🟢 margin 35% 346 bps ✅

Mgmt Guide 1Q26

- Sub Rev $3.7b 21.5% ↗️🟢

- cRPO 22.5% ↗️🟢

- NG EBIT Margin 31.5% ↗️🟢

Mgmt Guide FY26

- Sub Rev $15.57b 21% ↗️🟢

- Sub Gross Profit Margin 82%

- NG EBIT Margin 32% ↗️🟢

- FCF Margin 36% ↗️🟢

1 | Q4 was very strong, and improved profitability driven by OPEX efficiencies and disciplined spend management

Q4 was another strong quarter, concluding a remarkable year of AI innovation. Net new ACV growth accelerated both QoQ and YoY. We exceeded our top line growth and operating margin guidance metrics, showcasing our team's consistent execution and unwavering strength of our business.

Turning to profitability. Non-GAAP operating margin was 31%, 100bps above our guidance, driven by the top line outperformance, OpEx efficiencies and disciplined spend management. Our free cash flow margin was 57%, up 950bps YoY, driven by store collections, lower CapEx and significant operating leverage.

2 | Very strong broad performance across most products.

ServiceOps within 16 of our top 20 deals, highlighted by a standout performance in ITOM, which grew net new ACV nearly 50% year-over-year. ITAM within 17 of our top 20 deals, security and risk within 19 of our top 20 deals and drove nearly 40% net new ACV growth year-over-year.

Core business workflows within 13 of our top 20 deals. CRM was in 16 and both on net new ACV accelerate sequentially. As Bill mentioned, CPQ had a phenomenal quarter, Logik is a perfect example of our M&A strategy, creating demonstrable ROI. Finally, Creator Workflows were in 19 of our top 20 deals with an impressive 32 deals over $1 million in ACV. Moving to our success in driving broader AI adoption, Now Assist continues to outperform all expectations, surpassing $600 million in ACV and tracking well towards our $1 billion-plus target for 2026.

3 | AI Control Tower taking off, overachieved targets by >4X, allows enterprises to deploy AI agents securely and with confidence

We've also overachieved our initial AI Control Tower targets by more than 4x for 2025….So the way we address it, the reason we launched AI Control Tower early last year and why it's getting so much traction is because we're addressing these things head on, right? How do you manage and monitor agents real-time, not just our agents but third-party agents in one system it's really built on top of CMDB so we can now access all the kind of assets, be it hardware, software and AI agent assets in the same system and then we can really give you full-time real-time monitoring, observability as well as cost management, auditing, security in one place.

And that allows you to do kill switches, where you can now go and shut down any agent, which is going rogue, prevent any kind of nefarious activities as well as do red teaming and ensure you're making security as a prevalent and most important aspects of what you're doing before you go and deliver an AI agent.

4 | Myth that AI is eating software companies is not true, certainly not ServiceNow in enterprise software, workflow business remain very strong

And the idea that these models are eating enterprise software may be true in some cases. But obviously, it's not true. In our case, they're (models) actually leaning into us because of the innovation on our platform and the broad reach of our go-to-market global engine. So these are very enticing and interesting factors in their decision to team up with us.

All of the workflow businesses were very strong in Q4. The speculation of AI will eat software companies is out there. Let's clear it up with the facts. Enterprise AI will be the largest driver of return on the multitrillion dollar super cycle of investment in AI infrastructure, the real payoff comes when trillions of tokens move beyond pilots to be embedded directly into the workflows where business decisions are made.

5 | ServiceNow is the semantic layers that makes AI ubiquitous in the enterprise, it is not a feature-oriented SaaS company, it is a platform

ServiceNow is the gateway to this shift, serving as the semantic layer that makes AI ubiquitous in the enterprise. We are also the great consolidator of hundreds of feature- and function-specific software solutions into end-to-end business processes with our AI Control Tower for business reinvention.

You need AI plus workflows because AI is probabilistic, which by definition means we can't be certain about the results. Workflow orchestration is deterministic, predictable, no randomness, which is required given the sophistication and governance of running global enterprises.

AI doesn't replace enterprise orchestration. It depends on it. It depends on governance, it depends on scale. Many people ask why our valuation has not kept pace with our results. The short answer is that we have been viewed as a feature-oriented SaaS company.

We are not living in a SaaS neighborhood. We are a platform company, executing a long-term platform strategy where AI agents and workflows are harmonious and synonymous creating sustained advantage, not short-term wins.

6 | Speculation on seats compression is not being seen at ServiceNow, barely scratched the surface.

Overall, the number of workflows and the number of transactions each grew over 33% and from $60 billion to $80 billion and from $4.8 trillion to $6.4 trillion, respectively, and the growth continues. I continue to hear speculation about seat compression. If all we did was look at available seats in our target market, there would be an estimated 1.3 billion seats in that target market. So we barely scratch the surface.

And of course, we're looking far beyond seats alone with our hybrid business model for billions of devices, agents and assists. On the back of this momentum, we're guiding to 20% subscription revenue growth for 2026. And by now, everyone knows how ServiceNow rolls. We don't set our sights on hitting the guide. We set our sights on beating it.

7 | ServiceNow is not turning to M&A to sustain growth, it remains the fastest organic growing enterprise software company, strategically uses M&A to expand into larger TAM

The speculation out there, is that M&A is the new playbook out of necessity.

Here are the facts, ServiceNow has the fastest organic growth in the history of enterprise software. We're the fastest enterprise software company to have ever reached $1 billion, $5 billion and $10 billion organically. And on our way to cross $15 billion plus this year.

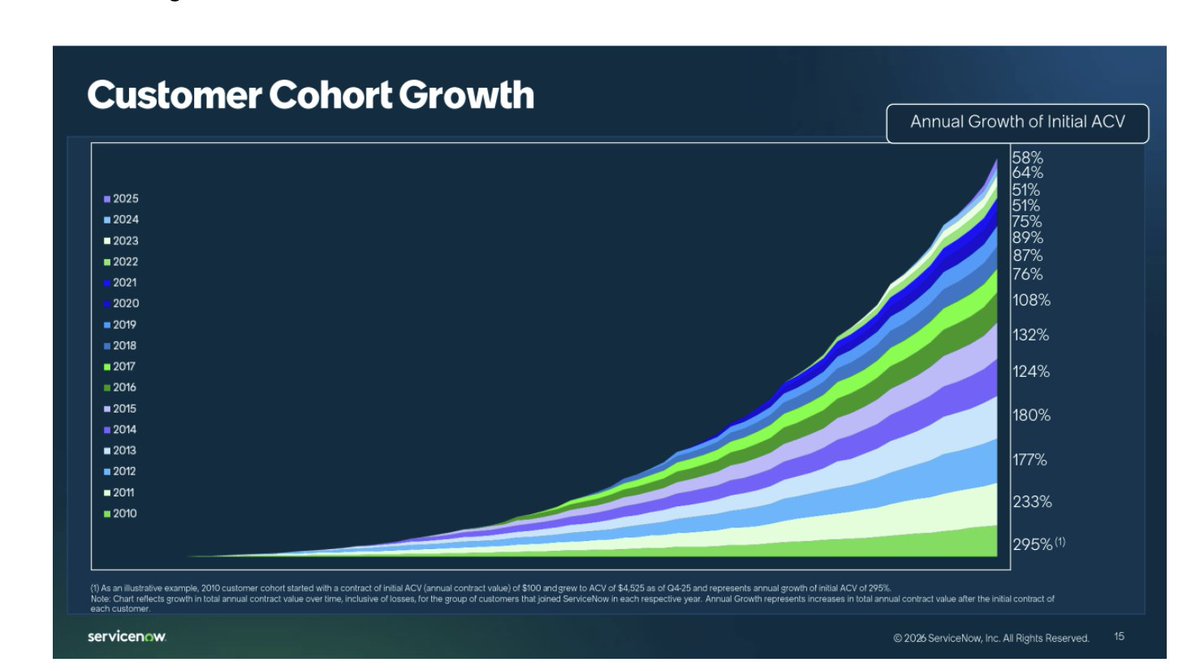

Since 2019, we've nearly quadrupled our revenue, all built on a foundation of continuous innovation and net new product delivery. ServiceNow is fully capable of achieving previously stated subscription revenue and Now Assist ACV targets without M&A.

Our capital allocation strategy is about accelerating customer value and shareholder value. We have never acquired a single company for revenue alone. We use M&A to expand into an even larger TAM, and it is now beyond $600 billion based entirely on where our customers need us to go, where we know we can build exciting growth businesses.

8 | ServiceNow remains an organic growth company and those were select M&A moves for talent and technology, not because they needed the revenue, and they don’t have a large-scale M&A road map

We're an organic growth company. These were very select M&A moves for the talent, the technology and the moment to capture $125 billion market TAM. And this is also where our customers wanted us to be. As I said, our security and operations portfolio right now is doubling year-over-year, and they wanted us to do more. I wanted to make it very clear to the investors. I hear you, and we did not and never have bought an asset, like many others have, and I know that's probably why it's on your mind, because we needed the revenue. What we needed is the innovation and the expanded growth opportunity of a great TAM and a customer base that's waiting for us. So I want to knock that one out of the park based on our great 2025 results and our extraordinary guide. And as it relates to future M&A, we do not have a large-scale M&A on the road map.

9 | AI adoption is expanding the attack surface, and companies can only se a small fraction of their digital real estate, no control, and no coordinated remediation of vulnerabilities

So here's the problem enterprises face today. AI adoption is expanding the attack surface exponentially. Companies are deploying autonomous agents across their operations but they're only able to see a small fraction of their digital estate.

To make matters worse, leaders have no control over who and what can access critical systems and data and they have no coordinated way to remediate vulnerabilities before they become breaches.

10 | Recent announced acquisitions of Veza and Armis are focused on visibility and identifying and combined with ServiceNow’s orchestration

Our announced plans to acquire Veza and Armis happened in rapid succession because this assembles 3 critical layers for enterprises to operate securely in agentic AI world, visibility, identity and orchestration with our fast-growing $1 billion-plus CACV security and risk business, the timing to expand the opportunity could not be better.

Post Armis, we do not see any other large white spaces that are necessary to complete our platform vision for security. ServiceNow's organic growth strategy with opportunistic tuck-ins for tech and talent remains unchanged, AI, data, workflows, security.

The combination of Veza and Armis with ServiceNow AI platform will create something that is mission-critical for enterprise AI. In the agentic era, if companies want to scale AI, trust and governance that span any cloud, any asset, any AI system and any device, these are all nonnegotiable.

11 | Armis solves the visibility problem, Veza solves the identity problem

First, Armis will solve the visibility problem. Armis provides real-time agentless discovery and classification of every asset across the entire enterprise. IT, OT, IoT, medical devices, industrial controllers and even shadow IT that bypasses procurement.

This creates a continuously updated map of the enterprise environment. Armis is already protecting over 40% of the Fortune 100 precisely because they've cracked the visibility challenge.

Second, Veza, will solve the identity governance problem through its patented Access Graph technology, Veza maps, access relationships and privileges across humans machines and AI agents in real time.

12 | CISOs are saying security is the bottleneck preventing AI agent deployment at scale, and Armis asset visibility with Veza's identity governance and business context, CMDB, which maps every asset, they can now see, decide and act across the entire technology footprint

This is critical because AI agents need dynamic context-aware permissions, an agent working for a senior manager needs different access than the same agent working for a junior employee and those permissions must be governed continuously not set once and forgotten.

CISOs have told us this is the bottleneck preventing AI agent deployment at scale. When both of these are integrated into ServiceNow's AI platform and AI Control Tower, this is how orchestration goes from theory to reality. When we combine Armis asset visibility with Veza's identity governance and ServiceNow's business context, CMDB, which maps every asset to the services, processes and teams that supports you create something highly differentiated, a unified end-to-end security exposure and operation stack that can see, decide and act across the entire technology footprint.

13 | Contribution from recent acquisition Moveworks is small.

Contribution from Moveworks was de minimis. Moveworks contributed 1 point to both RPO and cRPO…This (1Q26 revenue) includes a 1 point contribution from Moveworks and a 1.5 point headwind or a mix shift of on-prem hosted revenue, partially driven by the strong adoption of our hyperscaler offerings. We expect cRPO growth of 20% on a constant currency basis. This also includes a 1 point contribution from Moveworks.

14 | Taking advantage of the recent selloff to go aggressive on share buybacks

We are one of the few companies totally in control of our own destiny. We are playing offense on our tippy toes. That's why we're announcing an incremental USD 5 billion share repurchase authorization with an immediate ASR of $2 billion

15 | CEO William McDermott recently extended his commitment to stay as CEO until 2030 and beyond, he believes it is a $1T company (>7X from here)

You may have noticed that I recently extended my own commitment here to ServiceNow until 2030 and beyond. There's one reason I did this. Overwhelming belief in this company. This is a $1 trillion company in the making. I can't fathom a better entry point for what ServiceNow is building. To those on this journey with us, we are grateful for your enduring support. To those who are waiting. We've given you every reason to believe that time is now. This is a one-of-one company. That's not speculation.

16 | Numerous customer proof points examples of why they are picking ServiceNow.

We closed a $1 million-plus assist pack deal with a leading U.S. consumer services company after customer service agents generated a 400% ROI.

In Q4, we closed a landmark 7-figure deal with a complex high-tech manufacturer, involving an end-to-end takeout of a legacy CRM competitor.

A leading European telecom provider is building an AI-driven CRM solution for the telecom industry with ServiceNow.

A leading Canadian real estate company, selected ServiceNow CRM platform to integrate all aspects of their resident support and field operations with a unified data model.

A global business services company deployed ServiceNow agents for incident classification and resolution resulting in initial time savings of 13% for agents involved.

An international leader in commercial real estate services deployed ServiceNow agents to automate e-mail triage across their service desk, reducing mean time to resolution from 2 days to minutes, bringing agents for higher-value work.

A U.S. insurance company uses ServiceNow out-of-the-box agents to automate e-mail to case conversion achieving 91% accuracy and saving agents up to 12% of their time annually through an AI-first mindset.

A diversified industrial multinational conglomerate deployed ServiceNow agents to automate help desk triage.

One of Europe's largest drugstore chains, use ServiceNow to transform its customer service cutting the time it took customers to receive support from 9 minutes to 30 seconds and resolving customer issues with 98% accuracy.

ServiceNow was selected by a large U.S. county in a 7-figure deal to replace a legacy highly customized IT platform.

A large U.S. agency, it's using ServiceNow as the foundation of its IT modernization strategy. They are consolidating all IT services on ServiceNow, replacing more than 40 disparate tools currently in use.

17 | ServiceNow partners with all three hyperscalers and the top LLM players.

So let's talk a little bit about our great partners. Our ecosystem includes all 3 hyperscalers. They're all great companies. They're language model companies. They're excellent too. Systems integrators, pure-play ServiceNow partners and independent software vendors. They're all building their futures on our AI platform.

18 | Microsoft is partnering with ServiceNow

Think about this. ServiceNow and Microsoft have announced a deep AI integration, connecting copilots, agents and data across Microsoft 365 and the ServiceNow AI platform to deliver seamless orchestration, governance and enterprise-wide automation. The collaboration introduces Microsoft's Agent 365 integration, and it's anchored by ServiceNow's AI Control Tower, and it sets a whole new standard for enterprise AI interoperability, moving organizations from isolated AI experiences to autonomous AI workflows that drive efficiency and return on investment.

19 | The AI players Anthropic and OpenAI are partnering with ServiceNow

ServiceNow and Anthropic have announced an expanded partnership to integrate Claude models more deeply into the ServiceNow AI platform. Through the collaboration, ServiceNow is also bringing leading Claude models into ServiceNow to support secure, compliant AI across numerous industries.

ServiceNow also announced a new collaboration with OpenAI to enable direct customer access to frontier model capabilities, Custom ServiceNow AI solutions and increased speed with no bespoke development required. Under this agreement, OpenAI models will be a preferred intelligence capability for several agentic use cases offered to ServiceNow enterprise customers.

20 | Using OpenAI because of voice, speech, multimodal and multilingual and Anthropic more for coding and building of workflows

So for example, OpenAI, what we're doing around voice AI and speech to speech real-time, multimodal as well as multilingual capabilities. So our CRM products can now have voice capabilities with OpenAI as a preferred model so that we can have a much more differentiated offering using what we know from domains perspective as well as contact and adding the OpenAI speech capabilities into our products.

Similarly, with Anthropic, they have a very good coding agent. A build agent, which is a white coding tool allows any customer to build any workflow on top of ServiceNow, and we use Claude as the underlying technology to generate some of the codes and then we provide the contact, the security, the governance, on top of that using build agent to run those workflows on top of ServiceNow as well.

21 | Model providers are providing 5-10% of value and 90% of IP is built by ServiceNow

So customer guidance is pretty straightforward. They can choose any of the models, everything will work but there might be some of these individual use cases, we believe could really be turbocharged with some of these providers. And typically, in the infrastructure, the model providers are providing 5%, 10% of value and 90% of IP has been built by ServiceNow to really provide that context-driven enterprise use cases out of the box for our customers to get value instantly

22 | ServiceNow’s strong organic strong remains intact, with continued profit margin expansion, and is well positioned to capitalise on the AI trend

In conclusion, 2025 has been an incredible year, and we're just getting started. The world is in the midst of an intelligent super cycle, and ServiceNow is capitalizing on this decisive moment in technology where the strongest companies leverage rapid change to extend their market leadership.

Our recent strategic acquisitions bring us incredible talent and create enormous new market opportunities while solidifying our ability to put AI to work securely across every corner of the enterprise. As we integrate these best-in-class capabilities into the ServiceNow AI platform, we're layering on advantages that position us for even stronger, more durable growth over the long term. Our organic growth engine remains fully intact. Our strategy, complete with a disciplined focus on margin expansion, remains unchanged. But the ambition is larger and our confidence in sustained high organic growth has never been greater.

23 | Expect ServiceNow to keep growing 20% topline and continue EBIT and FCF margin expansion to the bottomline

And so you can count on ServiceNow to ensure that you will see not only best-in-class top line growth, up 20% plus but also continued margin accretion at the bottom line, both from an operating margin and free cash flow perspective.

And given our strong organic operating leverage, we expect to absorb any headwinds to that dilution in '27 and continue delivering operating margin expansion.

➡️ Final Thoughts on ServiceNow $NOW

The market looks to be overly pessimistic that AI will disrupt it, when the models are actually partnering with it. Its strong revenue growth posits it to be a beneficiary of AI, rather than one who is being disrupted. Solid, stable business, highly recurring revenues with a very long organic growth trajectory (~20% FXN) and very profitable (~FCF 30% margins) run by very solid management and execution. Continue to be well poised to benefit with secular and continued enterprise transformation and productivity gains with agentic AI workflows with their infrastructure/architecture moat of data connectors.

2

25

3,097

15 Dec 2025

In the latest report from @ema_research, they explore how our Skylar offerings reimagine ServiceOps by unifying service-centric observability, automation, AI, and built-in compliance to help IT teams operative with confidence.

🔗 Read the full report: bit.ly/3XRxtQJ

5

2

179

15 Dec 2025

📢🔥BIG NEWS! Freshworks has entered into a definitive agreement to acquire @FireHydrant!

With this combination, we will be able to bring together Freshservice's IT service management platform with FireHydrant's AI-native IT operations technology to create a truly unified ServiceOps experience.

➡️ Faster incident response

➡️ Clearer resolution path

➡️ Proactive IT reliability

Moving companies from reactive firefighting to resilient service. Learn more:

freshworks.com/press-release…

1

16

884

We’ve been building agent-based workflows that remove friction from complex business processes.

Our Warranty Agent is transforming how automotive brands handle claims, with faster resolution and less manual work. 👇

#GruveBuilds #EnterpriseAI #ServiceOps #GruveInsights #AIinSalesforce

1

4

98

17 Jul 2025

Amidst Madurai’s cultural richness, our event with @SavexTechnology was a celebration of tech, trust & teamwork. Meaningful exchanges, curious minds & growing interest in automation made it unforgettable.

#partnerevent #automationfirst #unifiedobservability #serviceops

2

5

175

25 Jun 2025

In Nov 2023, @NuvocoVistas faced scattered service operations and delays. In Dec, they chose our AI-powered ServiceOps and transformed everything. 80K tickets, SLA-backed efficiency, real-time support, and unified workflows. Grateful to the leaders for their trust

#customer

1

2

21

23 Jun 2025

2

76