29m

treatment of the question (eg sometimes there is an implicit assumption that a dynamical process is instantaneous, or that some phenomena, like the lack of coordination mentioned by Hahn and Solow can be discarded).

It's entirely possible that these assumptions are justified in

1

9

𝟑𝐈𝐂𝐄 𝐑𝐎𝐒𝐓𝐄𝐑 𝐒𝐏𝐎𝐓𝐋𝐈𝐆𝐇𝐓. 💡

In less than three weeks, the first-ever @3ICEHockey World Cup arrives in Belfast on Saturday 4 and Sunday 5 July. 🏆

Check out how the 3ICE USA roster, led by head coach Ken Daneyko, is shaping up. ⬇️🔥

There may be some familiar faces... 👀

Jeremy Brodeur (G)

Eddie Matsushima

Zachary Solow

Hank Crone

Will MacKinnon

Patrick Grasso

Peter Lenes

🎟️ Have you got your tickets yet? Secure your seat for both days here 👉 bit.ly/3ICE-Tickets

#WeAreGiants

7

1,149

That was one year ago Domenico need to adjust for depreciation in the Solow model !

1

15

21h

worlds in which they live, and there is also the essay by Hahn and Solow on a similar topic. mitpress.mit.edu/97802625815…

In other words, the baseline used in economics is, to me, very poorly justified

1

23

정희 retweeted

Jun 15

📌 "AI,에이전트만 쥐어주면 다 잘하겠지"가 틀린 이유 정리 (솔로우 역설 → 에이전트 시대 대입까지, 저장각)

[정보 — 핵심 개념]

솔로우 역설(Solow paradox, 도구 도입과 생산성 향상 사이의 시차) : "컴퓨터 시대는 어디서나 보이는데 생산성 통계엔 안 보인다"(로버트 솔로우, 1987).

보완 투자(complementary investment) : 도구값보다 일하는 구조,교육,프로세스 재설계에 드는 돈이 훨씬 크다. 그걸 안 하면 효과가 안 잡힌다.

들쭉날쭉한 경계(jagged frontier) : AI가 잘하는 일과 헛소리하는 일의 경계가 눈에 안 보인다(하버드,BCG 컨설턴트 758명 실험).

[원조 사례 — "도구 ≠ 성과"의 역사]

전기 모터(다이너모) : 1880년대에 모터가 나왔지만, 공장은 한가운데 동력축에 벨트,도르래를 매단 옛 구조를 그대로 두고 증기기관만 모터로 갈았다. 효과는 미미. 기계마다 개별 모터를 달고 동선을 새로 짠 1920년대에야 폭발했다 — 약 40년 시차 (폴 데이비드, 1990).

[솔로우 역설 × 에이전트 시대]

"에이전트 = 옆자리 인턴" 단계에 머무름 : BCG에 따르면 직원 85% 이상이 아직 작업 보조,위임 단계고, 자율 협업,오케스트레이션까지 간 비율은 10% 미만이라고 한다. 딱 "큰 모터 한 개"로만 쓰던 1900년대 초.

도입은 했는데 성과는 제자리 : 맥킨지(2026)는 기업 90% 가까이가 AI를 도입했지만 94%가 "의미 있는" 가치를 못 봤다고 — 솔로우 역설을 대놓고 다시 소환.

개인은 빨라졌는데 회사는 그대로 : 엔지니어가 코드 변경을 2배 처리해도 회사 지표는 평평하다는 보고(Faros 2026). 보조도구로 빨리 쓰는 것과 조직 성과는 자동으로 합산되지 않는다.

변혁의 역설(Microsoft 2026) : 직원은 일하는 방식을 바꿀 준비가 됐는데, 회사의 지표,보상,관행은 옛 방식을 보상한다. AI로 일을 새로 설계했을 때 보상받는다는 사람은 13%뿐.

거품 경고 : 가트너는 에이전트 프로젝트의 40% 이상이 2027년 말까지 취소될 거라 본다고 한다 (단, 예측이라 빗나갈 수 있음).

💬 에이전트를 쥐어줘도 다 성공 못 하는 건 당연하다. 왜냐하면 다들 에이전트를 "옛 워크플로 위에 얹은 비서"로 쓰는데, 그건 벨트,도르래 그대로 두고 모터만 갈았던 1900년대 초와 똑같기 때문이다 (그땐 40년 헛돌았다).

게다가 에이전트는 자율적일수록 "뭘 맡길지 & 결과를 어떻게 검증할지"를 설계하는 사람의 몫이 더 커진다. 그래서 도구가 똑똑해질수록 격차는 좁혀지는 게 아니라, 구조를 다시 짤 줄 아는 사람 쪽으로 더 벌어진다 (핸들 잡고 졸면 더 크게 사고 남).

핵심 반전 : 진짜 변수는 "에이전트를 비서로 쓰느냐 vs 일의 주체로 두고 워크플로를 다시 짜느냐"다. 도구가 아니라 재설계가 승부처.

반면에 이번엔 확산이 워낙 빨라서 그 40년이 4년으로 압축될 수도 있다 — 그럼 지금 헤매는 게 영구 무능이 아니라 그냥 "아직"일지도. 어쩌면 몇 년 뒤엔 이 글이 김 빠진 소리로 들릴 수도 있고.

(출처는 댓글로 답니다)

"도입 90% vs 가치 못 봄 94%"의 충격 격차를 숫자로 → 맥킨지 2026

"모터만 갈았더니 40년 헛수고"라는 전설의 원조 사례 → 폴 데이비드 다이너모 논문

직원은 바꿀 준비됐는데 회사가 옛 방식을 보상하더라 → 마이크로소프트 2026

#AI에이전트 #솔로우역설 #일하는방식재설계

1

2

2

144

Jun 14

Solow modelもここまでであれば、まだマクロⅡなら妥当かと思われます。ここに収束速度とか均衡の存在証明とかまで来ると院マクロとの中間レベルまで行くかなと思います。SolowもADASもマンキューマクロの範疇を出ないところがあるので。

1

1

204

Jun 14

Workers incomes are not solow. They can possibly do overtime, change job whatever. Pensioners are stuck. When you retire you want to relax for goodness sake after 50 years work! You could die at any moment at that age.

3

60

Algo amplamente analisado por Claus Germer por exemplo. E o resíduo de Solow não deixa de ser misterioso na equação pelo que foi exposto, pois necessariamente é uma variável misteriosa e isso é próprio da construção da equação.

1

1

20

In economics the strategy of the economics professors -- Paul Samuelson, Joseph Stiglitz, Robert Solow, Thomas Piketty -- has been to lie about the content of the science and ideas of their scientific rivals, and to have their opponents ideas die by murdering them with fraud.

Jun 14

"In science we get our hypotheses to die for us."

—Karl Popper, All Life is Problem Solving.

1

260

Já resolvi o problema do “crescimento” com recursos finitos há mais de 2 anos Tóni, corrigindo a fórmula do Solow, não estás bem a ver a tareia que vais levar 🤣🌈🔥

Abandon the GDP as a measure of development and practice an economy of cooperation and fair trade, helping the third world countries to develop through open source in exchange for their resources. I call it resource based economy, but the ideia isn’t originally mine.

1

34

Jun 14

Sedan en viktig variabel är restposten som Solow menade var det viktiga. Dvs hur vi utnyttjar max dessa variabler, hur smart, effektivt, arbetskraften agerar, här kommer AI och digitaliseringen in. 2

1

2

140

Tgy_y retweeted

Jun 13

nao aguento o pooh se fazendo que nao tem forças pra carregar o pavel sendo q ele já pegou o marido em um braço só 🤪

SoloWanderer x PoohPavel

#LannaTripwithPoohPavel

J

J

5

50

629

Jun 13

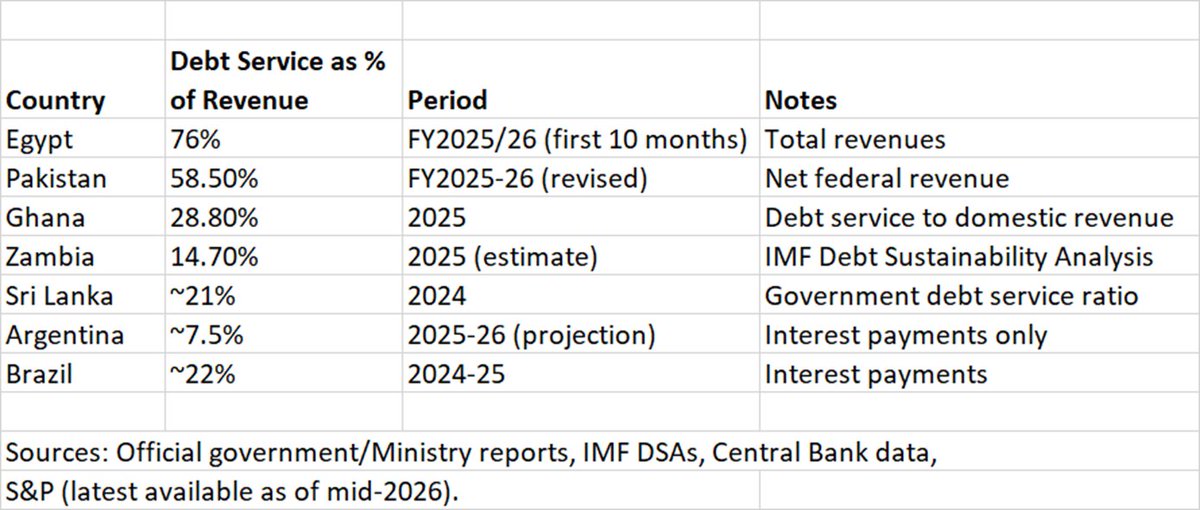

Why a Large Debt-Servicing Burden Has Become a Brake on Pakistan's Economic Growth

The debate over Pakistan's public debt is often framed in moral or political terms. Yet the most compelling case against an excessive debt burden is not ideological—it can be demonstrated in purely logical and economic terms.

At its core, economic growth depends on a country's ability to increase the productive capacity of its economy. In standard macroeconomic models, long-term growth is driven by the accumulation of physical capital, improvements in human capital, technological progress, and productivity gains. Government policy influences all four.

A large debt-servicing burden directly undermines this process.

The starting point is the national income identity:

GDP = C I G (X – M)

where C is consumption, I is investment, G is government spending, and X – M is net exports.

Not all government spending contributes equally to growth. Spending on education, health, infrastructure, research, and technology raises future productive capacity. Debt servicing does not. Interest payments merely transfer income from taxpayers to creditors. They do not build roads, educate workers, improve logistics, or increase productivity.

As debt servicing consumes a growing share of government revenue, it crowds out productive expenditure.

The budget constraint facing a government can be expressed as:

Revenue = Debt Service Current Expenditure Development Expenditure Defence Other Spending

When debt service expands faster than revenue, something else must shrink. In practice, development spending is usually the first casualty because salaries, pensions, subsidies, and security expenditures are politically difficult to reduce.

The result is lower public investment.

This matters because investment is one of the most important determinants of long-term growth. In the Solow growth model, output is determined by:

Y = A × F(K,L)

where Y is output, A is productivity, K is capital, and L is labour.

Growth occurs when the capital stock expands and productivity improves. Public investment contributes to both. Infrastructure lowers business costs. Education raises worker productivity. Technology investments increase efficiency.

Debt servicing contributes to none of these variables.

The damage extends beyond public finances.

When governments borrow heavily from domestic banks to finance fiscal deficits, they absorb a large share of available savings. This creates the classic "crowding-out" effect. Private firms find less credit available, or face higher borrowing costs.

In macroeconomic terms:

National Savings = Public Savings Private Savings

A large fiscal deficit reduces public savings. Lower national savings mean less funding is available for productive private investment.

Lower investment today translates into a smaller capital stock tomorrow, reducing future growth.

The arithmetic becomes particularly severe when interest rates exceed economic growth rates.

Debt dynamics can be summarized by the equation:

Δ(Debt/GDP) ≈ Primary Deficit (r – g)(Debt/GDP)

where:

r is the effective interest rate on government debt,

g is nominal GDP growth.

If the interest rate exceeds the growth rate, debt tends to rise relative to GDP even without large new borrowing.

This creates a vicious cycle.

Higher debt leads to higher interest payments. Higher interest payments increase borrowing requirements. Additional borrowing raises debt further. More debt generates even larger interest obligations.

Eventually, fiscal policy becomes dominated by debt management rather than economic development.

The consequences are visible in many heavily indebted economies. As debt service absorbs fiscal space, governments struggle to invest in human capital, infrastructure, innovation, and institutional capacity—the very factors that determine long-run growth.

The opportunity cost is enormous.

Consider two countries with identical tax revenues. One spends 40 percent of revenue on debt service and 10 percent on development. The other spends 10 percent on debt service and 40 percent on development. Over time, the second country accumulates better infrastructure, a more skilled workforce, stronger institutions, and higher productivity. The growth differential compounds year after year.

This is why excessive debt servicing is not merely a fiscal problem. It is a growth problem.

A country cannot borrow its way to sustained prosperity if an ever-larger share of its resources is devoted to servicing old obligations rather than creating new productive capacity. The mathematics of growth are unforgiving: economies expand when resources are invested in capital, people, and technology. When those resources are diverted to debt service, future growth is sacrificed to pay for the past.

That is the fundamental challenge facing heavily indebted economies. The issue is not debt itself. Debt can finance growth-enhancing investments. The problem arises when debt becomes so large that servicing it crowds out the very investments needed to generate growth. At that point, debt ceases to be a tool of development and becomes an obstacle to it.

3

9

21

1,249

Jun 13

Teeze mee any longer and I’m off, Goner.

Freeze mee any borer and I’m solow, Forrther.

I seek hapline guirt freelinetime.

I teach ALL and Wonnn LEAD has the time too everyday, everysecond, everymoment,

Beee FUN. !! !!

T

25