🖨️ New on printingpress.dev: The Press Room

A live leaderboard of who’s printed the most agent-native CLIs into the library. All-time and last 30 days, auto-updating every time a new CLI merges. Tap anyone to see everything they’ve shipped.

🙌 Shoutout to the top builders:

✍️ @cathrynlavery - 28 CLIs

1password, ahrefs, cloudflare, amazon-ads

⚙️ @hnshah - 9

coingecko, firecrawl, docker-hub

🎟️ @vinnypasceri - 9

dice-fm, eventbrite, blu-ray

📊 @sdhilip - 5 and climbing this month

meta-ads, stackadapt, azure-cost-admin

🥾 zaydiscold - 5

alltrails, goodreads, robinhood

This is what compounding looks like.

🏆 Full board, find your name: printingpress.dev/leaderboar…

🖨️ Print your own and get on it: printingpress.dev

@ppressdev

11

9

34

3,814

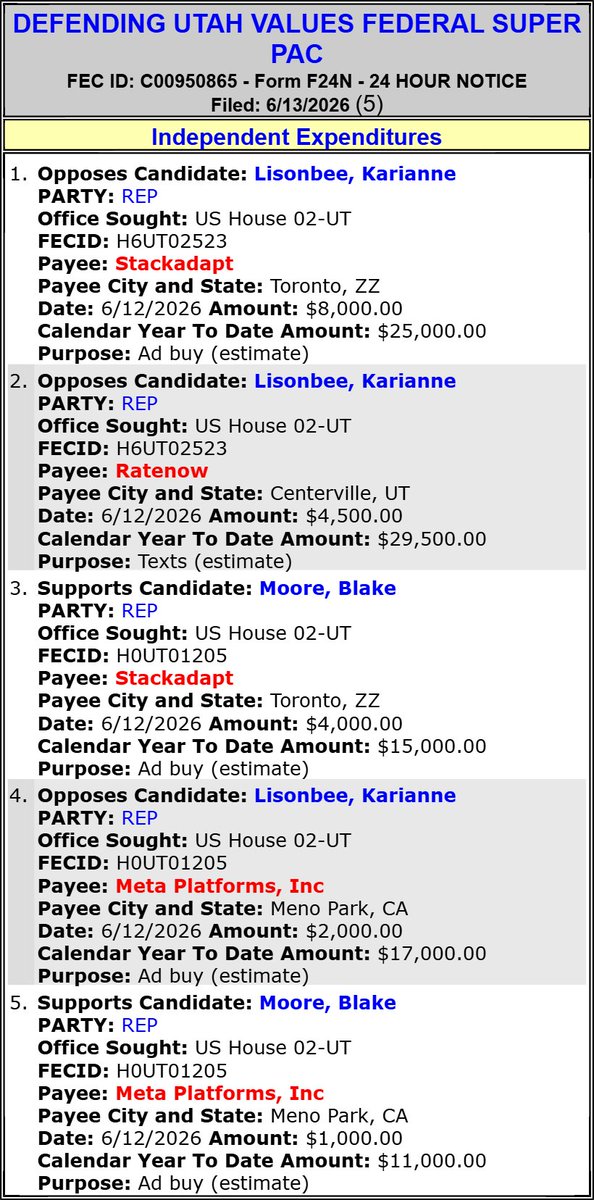

Election Hive, the ad buying vendor for Defending Utah Values Federal Super PAC, has other clients (FEC Database):

Blake Moore For Congress - Moore, Blake(#UT02)(REP) FECID: C00738872 (capitolhillaccess.com/tr/tr_…)

Defending Utah Values Federal Super PAC FECID: C00950865 (capitolhillaccess.com/tr/tr_…)

Mike Kennedy For Utah - Kennedy, Mike(#UT04)(REP) FECID: C00864488 (capitolhillaccess.com/tr/tr_…)

Last Updated: 6/13/2026

Defending Utah Values Federal Super PAC List of Vendors:

Election Hive

Google, LLC

Meta Platforms, Inc.

RateNow

StackAdapt

Defending Utah Values Federal Super PAC spends $12,500 to OPPOSE Karianne Lisonbee (Hse UT-02)(R)

Defending Utah Values Federal Super PAC spends $5,000 to SUPPORT Blake Moore (Hse UT-02)(R)

Defending Utah Values Federal Super PAC spends $2,000 to OPPOSE Karianne Lisonbee (Hse UT-02)(R)

#UT02

IE DETAILS: capitolhillaccess.com/tr/tr_…

Spending Leaders:

capitolhillaccess.com/tr/tr_…

Spending List:

capitolhillaccess.com/tr/tr_…

2026 Cycle FEC Data:

capitolhillaccess.com/tr/tr_…

FEC:

docquery.fec.gov/cgi-bin/for…

@RepBlakeMoore @ElectBlakeMoore

104

Andrew Cassin retweeted

Jun 12

I’ve been bullish on @StackAdapt for a long time.

Part of that is admittedly personal. Years ago, I had the opportunity to work with the team as they expanded their gaming footprint, and I’ve always walked away impressed by how they approached building the business.

What’s interesting to me is how much the company has evolved while staying true to the same core idea: making programmatic more accessible.

Today, people are talking about Ivy, AI, and the shift toward becoming an advertising and orchestration platform.

But I actually think the more interesting story is what came before that.

They quietly built one of the largest independent DSPs in the market, reportedly reached a ~$2.5B valuation, and raised $235M from Teachers’ Venture Growth. That’s a pretty remarkable outcome in adtech.

And of all the DSPs out there, StackAdapt remains the only one where I can realistically imagine a brand like shopaditi.com becoming a customer someday.

Not because we’re there today.

But because they’ve consistently lowered the barriers to entry for advertisers who historically would’ve been locked out of programmatic. Omnichannel access, self-serve capabilities, managed service support, and a platform that feels approachable to marketers instead of exclusively built for traders.

Most DSPs are still optimized for the largest buyers in the ecosystem.

StackAdapt feels like it’s building toward a future where a much broader set of businesses can participate.

That’s a market opportunity I wouldn’t underestimate.

1

1

11

741

Jun 12

Yes - same exact vibes. 🤣

Gimme credits , I’ll light it up and document the process.

32

Senior Quality Engineer - StackAdapt - Ocean Beach, New York, United States

qualityassurancejobs.com/job…

2

Jun 11

I understand that CTV is not like display.

However, you also can’t say that a $10 bid from StackAdapt through Magnite to Roku exchange has the same net CPM as $10 bid directly into Roku exchange.

Supply path optimization is a thing and that includes DSP fees.

27

Jun 9

The 2026 FIFA World Cup presents massive opportunities for brands, but measuring impact won't be easy.

On this bonus episode of On Scope, Greg Joseph of @StackAdapt joins Mike Berberich to discuss market selection, omnichannel activation, and maximizing brand impact around the tournament.

Listen now. shorturl.at/sUWt0

45

The ANA retweeted

How can brands stand out during the 2026 FIFA World Cup?

Greg Joseph of @StackAdapt joined @ANAmarketers's On Scope podcast to discuss fan engagement, omnichannel activation, and the opportunities facing marketers ahead of the tournament.

Listen: ana.net/miccontent/show/id/o…

1

56

EXCLUSIVE | @Criteo is gaining traction among retail advertisers by offering easier product-feed integrations, financial incentives, and lower spending thresholds on @ChatGPTapp that some buyers say make it a more attractive option than rival platforms such as StackAdapt.

1

1

2,050

May 31

Viant vs TTD

Pubmatic vs Magnite

Basis vs Stackadapt

Etc etc.

Their teams would never allow it to happen. They’d rather fight from a distance and in a conference rooms than a public forum.

1

3

126

May 30

Capitalism is monstrous because what do you mean I the most fun, whimsy-filled guy I knew in high school post on LinkedIn that he was “delighted to be joining StackAdapt, an early partner for putting ads in ChatGPT”

5

298

May 27

Premium domain for sale 🚨

Boost your branding

Measurable.tv @weareMNTN $TTD , @Roku @SimplifiAgency @StackAdapt @CTV

3

173

📢[5/22]IMの気になるニュース

#OpenAI が仕掛ける #広告ビジネス で、もっとも利益を得る企業の条件とは🤖📈🏢

「ChatGPTの中で #広告 が配信される時代、この巨大な新市場で最終的な覇者となるのは誰なのでしょうか?」

DSPプラットフォームのStackAdapt(スタックアダプト)は、一部クライアントでのクローズドベータテストを経て、すべての広告主に向けて「ChatGPT広告」の提供を本格的に開始した。

これにより、LLM(大規模言語モデル)を活用した広告がいよいよ本格的な実運用フェーズへと突入する。

現在、CriteoやThe Trade Desk(TTD)などの大手アドテク企業は、OpenAIを脅威としてではなく「新たな巨大広告チャネル」と捉え、計測や統合運用の機会として積極的に活用しようと動いている。

しかし、OpenAIの最終的な野望はアドテク企業との提携にとどまらず、GoogleやMetaのように広告需要と独自のデータを自社で完全に掌握する「ウォールドガーデン型モデル」の構築にあると見られている。

急拡大する生成AIプラットフォームが独自の巨大広告帝国を築き上げるのか、AIエコシステムを巡る主導権争いから目が離せない。

digiday.jp/platforms/ad-tech…

@DIGIDAYJAPAN

2

77

May 19

StackAdapt is running ads in the chicago Tribune this week asking applicants to send their resumes to their global mobility team

These teams manage immigration processing, not hiring. We think this discriminates against Americans who want to apply for these jobs!

3

77

209

3,533

May 15

I’ve spent 15 years inside paid ads.

Meta.

Google.

Microsoft.

TikTok.

LinkedIn.

Pinterest.

Reddit.

Amazon.

Trade Desk/DSP.

StackAdapt.

Outbrain/Taboola.

PropellerAds.

TrafficJunky.

Some I’m forgetting.

Across:

Lead gen.

Ecommerce.

Finance.

Real estate.

Travel & hospitality.

SaaS.

And more.

High-volume campaigns.

Small ugly campaigns.

Campaigns that scaled.

Campaigns that looked good and quietly burned money.

My X account is where I share the practical stuff I’ve learnt:

• why ads fail

• how creative actually gets tested

• how funnels leak money

• why “more traffic” is rarely the fix

• what founders misunderstand about paid growth

• how to think about CPL, CAC, lead quality and conversion

No guru stuff.

No fake screenshots.

No “scale to 7 figures in 30 days.”

Just useful paid ads lessons from someone who has been in the accounts.

2

25

509