Jun 13

Not relevant. ????? Human Flights???

STS-41D Aug. 30, 1984

First flight of Space Shuttle Discovery. The primary payloads for the mission were three commercial communications satellites — SBS-4 for Small Business Systems, Telstar 3C for Telesat of Canada, and Syncom IV-2, also known as Leasat 2, for the U.S. Navy.

nasa.gov/mission/sts-41d/

Article dated July 8,2018

First launch Falcon 9 with crew to ISS May 30, 2020?

nasa.gov/news-release/nasa-a…

1

81

The arms aren’t going to to fly to you with Wings you’re going to have to contact the CIA or Massage or Syncom or the IDF or one of the military agencies we can arm you but posting something on about it isn’t is not going to help your case there’s nobody here on that can give you weapons you’re going to have to do what they ask you to do until their website it’s Hhonors instructions in Farsi on what you need to do to contact them should you need weapons or any other suppliesI would suggest you focus on that instead of posting videos on social media if you actually do want to be armed

27

🚀 10 High-Potential Stocks | Sector-Wise Snapshot

1. 🌱 Clean & Green Energy

• Suzlon Energy – Wind energy turnaround leader

• Shilchar Tech – Transformer demand boom beneficiary

• Urja Global – Solar, batteries & e-mobility play

2. 🛡️ Defence & Railways

• HBL Power – Kavach defence battery leader

• Jupiter Wagons – Railways EV expansion

• PTC Industries – Aerospace & defence precision castings

3. 💻 Digital Tech & Pharma

• eMudhra – Digital identity & e-signature leader

• Syncom Formulations – Expanding pharma exports

4. 🏭 New-Age Manufacturing

• RattanIndia Enterprises – Drones, EV & fintech

• Trident – Premium exports manufacturing scale

⚡ Themes Driving Growth:

Green Energy | Defence | Railways | Digital India | Manufacturing

#StockMarket #Investing #MultibaggerStocks #IndiaGrowthStory

3

31

2,649

The groundbreaking call was facilitated by the Syncom 2 satellite. During the historic conversation, the two leaders exchanged pleasantries, discussed the recent Nuclear Test Ban Treaty.

1

2

335

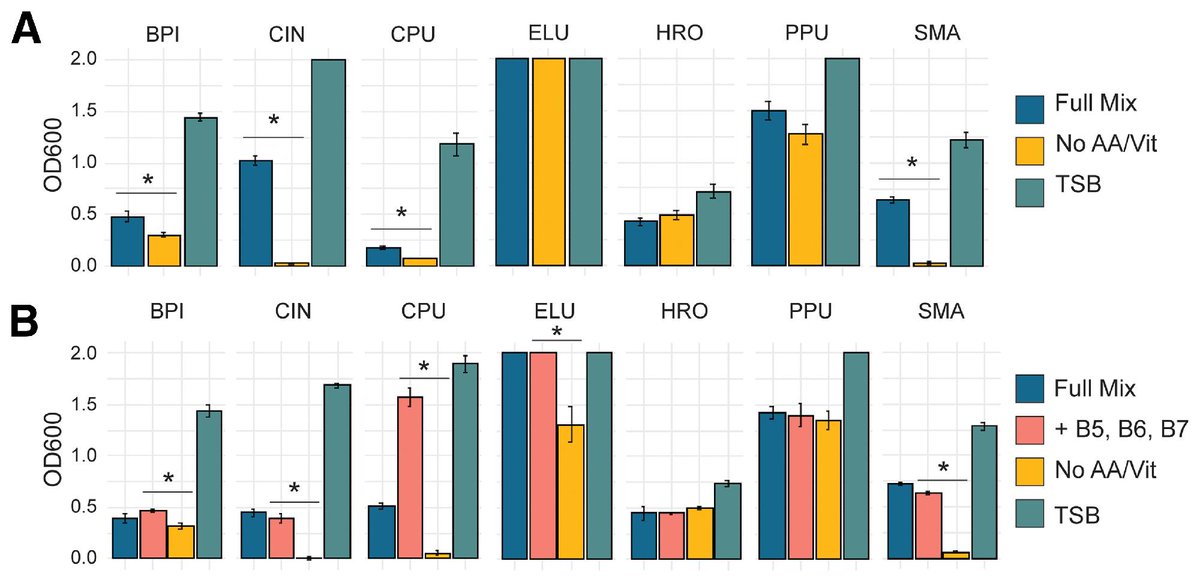

Anna-Katharina Garrell et al. report the development of a defined minimal growth medium for a well-characterized seven-member maize root synthetic microbial community. Learn more: doi.org/10.1094/PBIOMES-07-2… #maize #syncom #plantmicrobiome

ALT Fig. 2. Growth of synthetic community species in 0.5× Murashige and Skoog, glucose, and malate augmented with additional amino acids and vitamins (n = 3).

2

385

May 25

Hi Sir, Syncom formulations posted Q4 profit of 25 cr and annual profit of 76 cr. Can we expect a fresh rally towards new all time high? Please advise sir. Thank you.

1

3

274

May 25

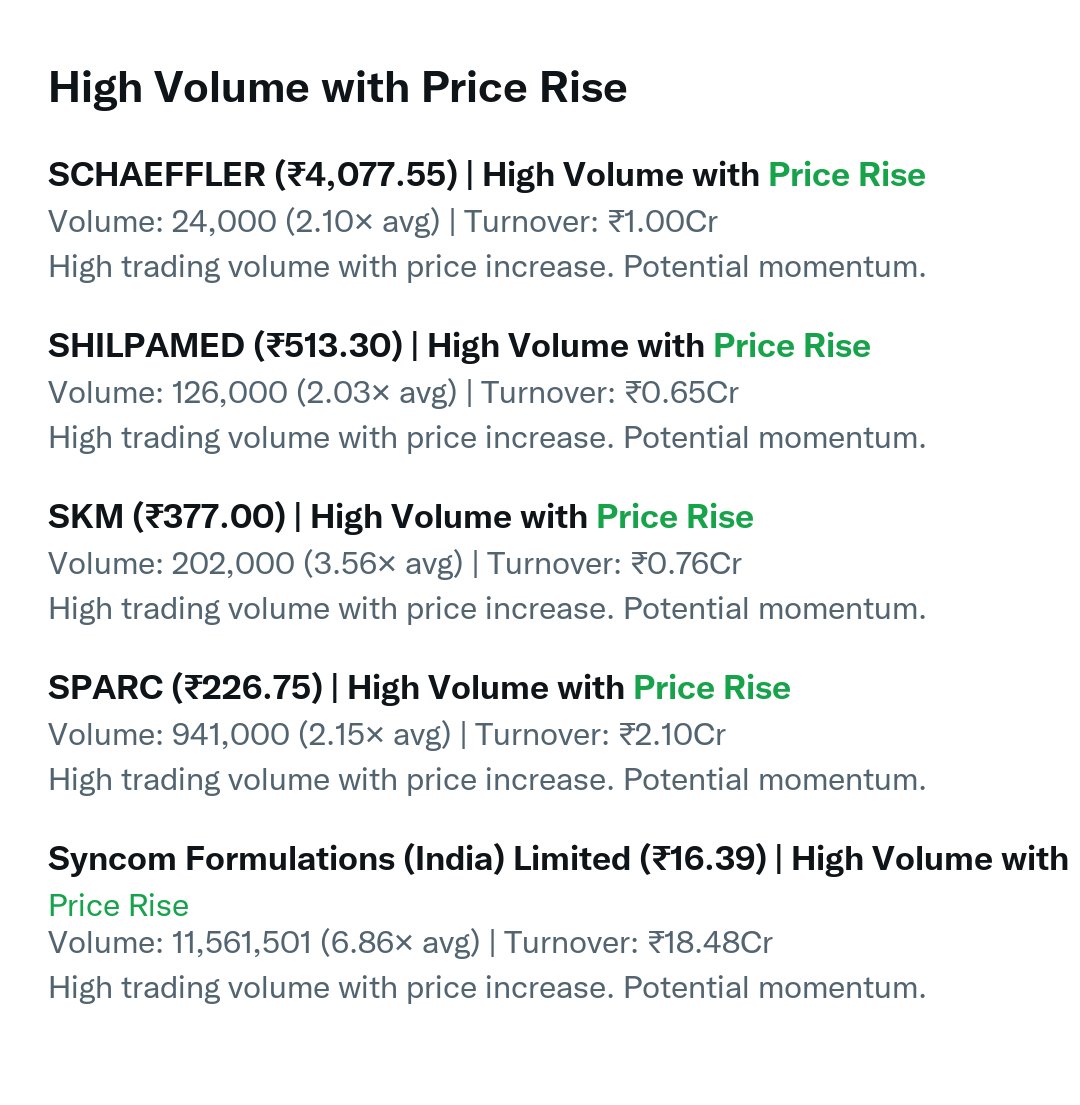

📊 𝗛𝗶𝗴𝗵 𝗩𝗼𝗹𝘂𝗺𝗲 𝘄𝗶𝘁𝗵 𝗣𝗿𝗶𝗰𝗲 𝗥𝗶𝘀𝗲

Stocks in focus: SCHAEFFLER, SHILPAMED, SKM, SPARC, Syncom Formulations (India) Limited

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/bsevg | wegro.app/nsevg

1

269

May 24

#Q4FY26 Mainboard #results on 22nd May -

Blockbuster Set –

Modison (#ModisonLtd )

Manaksia Steel (#Manaksteel )

Marsons (#Marsons )

Solid Set -

Minda Corp (#MindaCorp )

Gulshan Poly (#GulPoly )

Shilpa Medicare (#ShilpaMed )

SKM Egg (#SKMEggProd )

Tinna Rubber (#TinnaRubr )

Narayana Hrudayalaya (#NH )

Birla Cable (#BirlaCable )

Vikran Engg (#Vikran ) - Margins down

Hariom Pipes (#HariomPipe )

Good/Decent Set –

S chand (#Schand )

Hindalco (#Hindalco )

Fortis Healthcare (#Fortis )

20 Microns (#20Microns )

3M India (#3MIndia )

Bansal Roofing (#BRPL )

Century Plyboard (#CenturyPly )

NTPC Green (#NTPCGreen )

Greenlam (#Greenlam )

EMIL (#EMIL )

Naukri (#Naukri )

Ganesh Consumer (#GaneshCp )

Eicher Motor (#EicherMot ) - Good YoY, down QoQ

Euro Panel (#EuroBond )

Kovai Medical (#Kovai )

Aarvi Encon (#Aarvi )

Syncom Formulation (#SyncomF )

Manomay Tex (#Manomay )

GHV Infra (#GHVInfra )

3

6

1,384

May 23

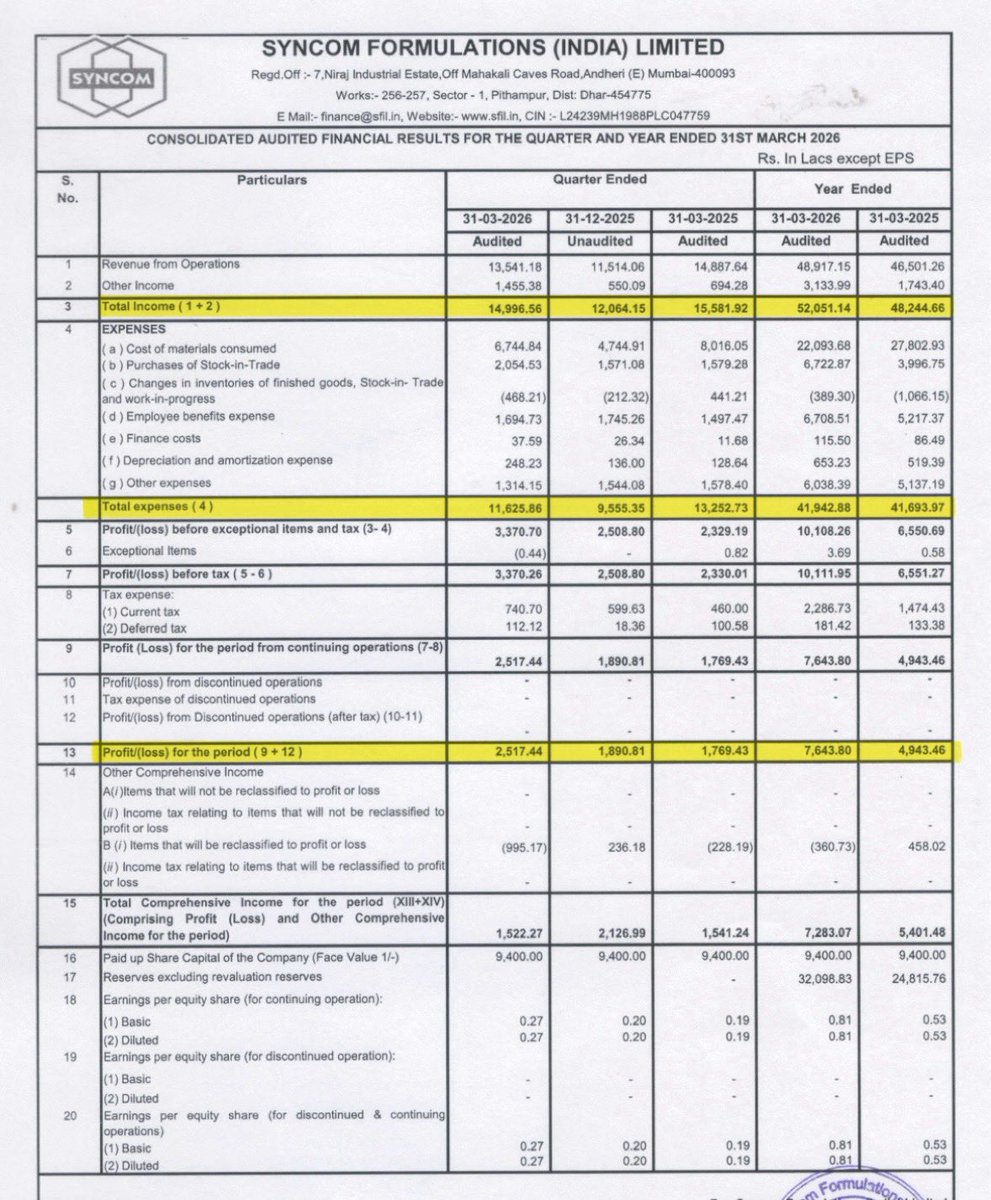

💊 Syncom Formulations (India) Ltd Q4FY26 Results 📊

💰 Revenue: ₹135.41 Cr vs ₹148.88 Cr

⬇️ -9.04% YoY | 🚀 17.61% QoQ

🔥 EBITDA: ₹22.01 Cr vs ₹17.75 Cr

⬆️ 23.99% YoY | 📈 3.78% QoQ

📌 EBITDA Margin: 16.26%

vs 11.92% YoY & 18.42% QoQ

⚖️ PBT (Ex-Exceptional Items): ₹33.71 Cr vs ₹23.29 Cr

🚀 44.72% YoY | 📈 34.36% QoQ

✅ PAT: ₹25.17 Cr vs ₹17.69 Cr

🚀 42.27% YoY | 📈 33.14% QoQ

💵 Other Income: ₹14.55 Cr

vs ₹6.94 Cr YoY & ₹5.50 Cr QoQ

#SyncomFormulations #Q4Results #PharmaStocks #IndianStockMarket #StockMarket #EarningsSeason #SmallCapStocks #Investing #MarketUpdate #StocksToWatch

1

5

372

May 22

22nd May 2026 Q4FY26 Results Snapshot:-

#Q4Results #Q4FY26 #Nifty

🚩Decent / Good / Blockbuster 👏🔥😀

1) Anondita Medicare (SME)(Blockbuster)

2) Shilpa Medicare (Decent)(Track)

3) Tinna Rubber and Infrastructure (Decent)

4) SKM Egg Products Export (Solid)

5) Info Edge

6) Narayana Hrudayalaya (Acquisitions reflected)(Margin will eventually catch up)(Cayman revenue up 48%)

7) Eicher Motors

8) Fortis Healthcare (Good)

9) Grand Continent Hotels (SME)(Blockbuster)

10) Galaxy Infotech (SME)(Solid)

11) TechD Cybersecurity (SME)(Blockbuster)

12) Minda Corporation (Solid)

13) Aelea Commodities (SME)(Blockbuster)

14) SK Minerals & Additives (SME)(Solid)

15) TTK Prestige (Margin Expansion)

16) Bansal Roofing Products (Solid)(Now need to see does growth trajectory continue in FY27 or not)

17) HRS Aluglaze (SME)(Blockbuster)

18) Electronics Mart India (Q4 SSSG of 12.1%)

19) 3M India

20) Faze Three (Revenue up 31.6% EBITDA up 38.5% PAT up 12.4%)

21) Hariom Pipe Industries (Good)

22) NTPC Green Energy (Margin down)(PAT down due to lower other income)

23) Modison (Blockbuster)

24) Manaksia Steels (Blockbuster)

25) Birla Cable (Blockbuster)

26) S Chand and Company (Good)(We expect FY27-28 to see complete adoption of the new syllabus books for the K-12 segment which should strongly support our growth trajectory over the next 2 years)

27) S&S Power Switchgear (Margin Expansion)

28) Greenlam Industries (Decent)(Margin Expansion)(Overall laminate business grew 14.4% in value terms on YoY basis)

29) Zota Health Care Ltd (Solid)(Revenue up 68% EBITDA up 253%)(But still in losses)

30) Marsons (Solid)

31) Star Cement (Margin up)(Better than peers)

32) Century Plyboards (Decent)

33) Manomay Tex India

34) GHV Infra Projects

35) Torrent Pharmaceuticals (Revenue up 42% EBITDA up 41%)(PAT down due to increase in depreciation & Interest Expense)

36) Vikran Engineering (Revenue up 82% EBITDA up 36% PAT up 48%)(Total order book as on 22nd May 2026, stands at Rs. 5,737 crores)

🚩Bad / Poor / Weak 😠😡🤬

1) DAM Capital Advisors (No IPO No Party)

2) Trident Techlabs (SME)

3) Sealmatic India (SME)

4) Remsons Industries(Revenue up 23%)(Margin down)(FY30 Revenue Aspiration ₹900–1,000 Cr)(Implies Revenue CAGR of 24–29% over FY26–FY30 from the FY26 base)

5) GSFC (Margin down)(Revenue up 37%)

6) SMS Pharmaceuticals (PAT up only due to Share of JV & Associates)

7) All Time Plastics

8) Shree Tirupati Balajee FIBC (SME)

9) Jubilant Pharmova (Margin down)(Already priced in)(Revenue growth has stepped up, EBITDA Margins will start to inch up from H2’FY27 onwards)

10) Ircon International (Revenue down but Margin up)

11) Tarsons Products (Margin down)

12) Unichem Laboratories

13) Motisons Jewellers (Margin down)(Revenue up 15.7%)

14) Arrow Greentech

15) Manoj Vaibhav Gems N Jewellers (Margin down)

16) TruAlt Bioenergy (Ethanol offtake remained significantly impacted due to a sharp reduction in lifting by OMCs despite operational readiness and available production capacities)

17) Jindal Drilling & Industries (Margin down)

18) Prostarm Info Systems (Margin down)(Revenue up 27%)

19) EIH Associated Hotels

20) Lehar Footwears

21) Swiss Military Consumer (Margin down)

22) Kolte Patil Developers (Poor revenue recognition)(FY26 Pre Sales down -7% YoY)(Collections up 11% YoY)

23) Pix Transmissions

24) Precision Camshafts

25) Maharashtra Seamless

26) VTM (Margin down)

27) Alphalogic Techsys (Revenue down but Margin Expansion)

28) Godavari Biorefineries (Q4 FY26 was marked by a challenging operating environment for the sugar and ethanol industry, with elevated cane and feedstock costs impacting overall sector profitability)

29) Concord Enviro Systems (QoQ improvement)

30) Yatra Online (Adj. EBITDA down by 33.8%)(Gross bookings grew 8.3% YoY)(War-related disruption significantly affected the company’s MICE business, particularly international corporate group travel. Several Q4 bookings were either cancelled or deferred into FY27)

🚩 Mixed / Neutral / Average🙄😑🆗

1) Excelsoft Technologies (Margin down)

2) Prakash Industries (Avg to below Avg)

3) Australian Premium Solar (SME)(Okish)

4) Sun Pharmaceutical Industries (Margin down)(Inline with estimates)

5) Paramount Communications (Margin down)(QoQ improvement)

6) The Ramco Cements (Margin up)

7) Kovai Medical Center & Hospital

8) Ellenbarrie Industrial Gases (Okish)

9) Khazanchi Jewellers (Revenue down but Solid Margin Expansion)

10) Euro Panel Products

11) Gokaldas Exports (Exporter)(YoY weak)(QoQ improvement)

12) Indigo Paints

13) Ganesh Consumer Products (Revenue down but Margin Expansion)(QoQ Margin down)(While headline revenue growth was modest, we deliberately prioritised the structural quality of the business over short-term volume)

14) Syncom Formulations (Revenue down but Margin Expansion)

15) Excel Industries

16) SPIC (Revenue down but Margin Expansion)

17) Alufluoride (Revenue down but Margin Expansion)

18) Hindalco Industries (Margin down)(Track)(PAT down due to Exceptional losses)

19) Viceroy Hotels (EBITDA up 50% YoY)(PAT down due to huge increase in finance cost)

20) TVS Electronics (Solid Margin Expansion)

21) 20 Microns (Margin down)

22) Pudumjee Paper Products (Margin up)

23) Gulshan Polyols (Solid Margin Expansion)

24) Max Estates

25) Colgate Palmolive

26) TCC Concept (Acquisition integrated in numbers)(Margin down)

27) Industrial & Prudential Investment Company (No view)

28) Crest Ventures (No view)

29) Sera Investments & Finance India (No view)

30) Prabha Energy (No view)

2

6

58

6,518

May 22

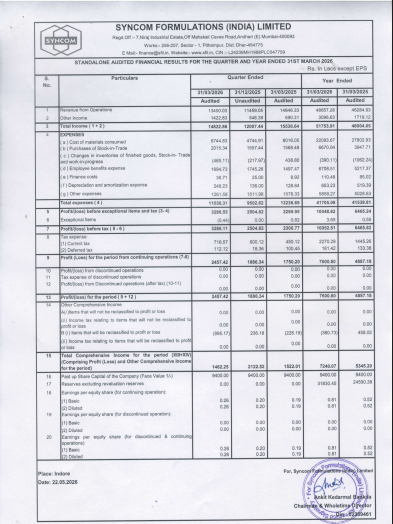

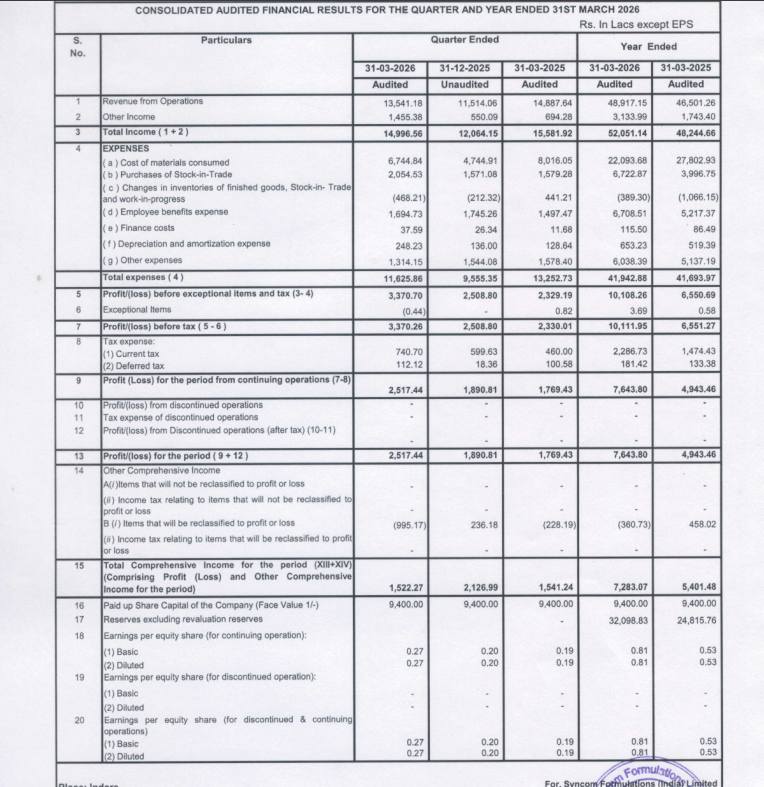

Syncom Formulations (India) Ltd Q4FY26 Results:-

#Q4Results #Q4FY26 #Stockmarket #Nifty #Syncom

Revenue 135.41 Cr vs 148.88 Cr

(-9.04% YoY┃ 17.61% QoQ)

EBITDA 22.01 Cr vs 17.75 Cr

( 23.99% YoY ┃ 3.78% QoQ)

EBITDA Margin 16.26% vs 11.92% YoY & 18.42% QoQ

PBT Ex-Exceptional Items 33.71 Cr vs 23.29 Cr

( 44.72% YoY┃ 34.36% QoQ)

PAT 25.17 Cr vs 17.69 Cr

( 42.27% YoY┃ 33.14% QoQ)

Other Income 14.55 Cr vs 6.94 Cr YoY & 5.50 Cr QoQ

8

1,623

Execution-heavy earnings day today. 📊

Key companies reporting today 👇

• Birla Cable

• Ramco Cements

• Pix Transmissions

• Torrent Pharmaceuticals

• Excel Industries

• EIH

• Jyoti

• Eicher Motors

• Prakash Industries

• Modison

• AG Ventures

• Milkfood

• Voltaire Leasing & Finance

• Jindal Drilling & Industries

• Crest Ventures

• Shrydus Industries

• Libord Finance

• Ajcon Global Services

• Dhanlaxmi Cotex

• Regent Enterprises

• T T

• Agio Paper & Industries

• Arrow Greentech

• TTK Prestige

• Trigyn Technologies

• Eurotex Industries & Exports

• Advani Hotels & Resorts

• Kovai Medical Center & Hospital

• 3M India

• Swiss Military Consumer Goods

• ITI

• Syncom Formulations India

• Vivid Global Industries

• Alufluoride

• Multibase India

• Elegant Floriculture & Agrotech

• Velan Hotels

• Jubilant Pharmova

• Faze Three

• Swojas Foods

• Tinna Rubber & Infrastructure

• Shilpa Medicare

• Paramount Communications

A lot of sector signals coming in one evening. 👀

Which result are you tracking most closely today ❓❓❓

4

16

1,224

May 22

Quarterly earning results to watch out

May 22, Friday - Today

•#20microns - 20 Microns Ltd

•#3mindia - 3M India Ltd

•#Birlacable - Birla Cable Ltd

•#Centuryply - Century Plyboards India

•#Cewater - Concord Enviro Systems Ltd

•#Colpal - Colgate Palmolive India Ltd

•#Damcapital - DAM Capital Advisors Ltd

•#Eichermot - Eicher Motors Ltd

•#Eihahotels - EIH Associated Hotels Ltd

•#Ellen - Ellenbarrie Industrial Gases Ltd

•#Emil - Electronics Mart India Ltd

•#Faze3q - Faze Three Ltd

•#Fortis - Fortis Healthcare Ltd

•#Gokex - Gokaldas Exports Ltd

•#Greenlam - Greenlam Industries Ltd

•#Gsfc - Gujarat State Fertilizers

•#Hariompipe - Hariom Pipe Industries Ltd

•#Hginfra - HG Infra Engineering Ltd

•#Hindalco - Hindalco Industries Ltd

•#Indigopnts - Indigo Paints Ltd

•#Ircon - IRCON International Ltd

•#Jindrill - Jindal Drilling & Industries Ltd

•#Jublpharma - Jubilant Pharmova Ltd

•#Kovai - Kovai Medical Center

•#Mahseamles - Maharashtra Seamless

•#Maxestates - Max Estates Ltd

•#Morepenlab - Morepen Laboratories

•#Mvgjl - Manoj Vaibhav Jewellers

•#Naukri - Info Edge India Ltd

•#Nh - Narayana Hrudayalaya Ltd

•#Ntpcgreen - NTPC Green Energy Ltd

•#Pixtrans - Pix Transmissions Ltd

•#Precam - Precision Camshafts Ltd

•#Prostarm - Prostarm Info Systems Ltd

•#Ramcocem - The Ramco Cements Ltd

•#Shilpamed - Shilpa Medicare Ltd

•#Skmeggprod - SKM Egg Products

•#Smspharma - SMS Pharmaceuticals Ltd

•#Sunpharma - Sun Pharmaceutical

•#Syncomf - Syncom Formulations India Ltd

•#Torntpharm - Torrent Pharmaceuticals Ltd

•#Trualt - Trualt Bioenergy Ltd

•#Ttkprestig - TTK Prestige Ltd

•#Tvselect - TVS Electronics Ltd

•#Unichemlab - Unichem Laboratories Ltd

•#Vikran - Vikran Engineering Ltd

•#Yatra - Yatra Online Ltd

19

1,759

May 22

4QFY26 - Key Results today

22nd May 2026 (Friday)

1. Sun Pharma

2. Hindalco Industries

3. Eicher Motors

4. Torrent Pharmaceuticals

5. NTPC Green Energy

6. Fortis Healthcare

7. Info Edge (India)

8. Colgate Palmolive (India)

9. Narayana Hrudayalaya

10. 3M India

11. The Ramco Cements

12. Century Plyboards (India)

13. Jubilant Pharmova

14. Ircon International

15. Minda Corporation

16. Shilpa Medicare

17. Star Cement

18. Maharashtra Seamless

19. TTK Prestige

20. Gujarat State Fertilizers & Chemicals

21. Max Estates

22. Greenlam Industries

23. Kovai Medical Center & Hospital

24. Gokaldas Exports

25. Indigo Paints

26. Electronics Mart India

27. Zota Health Care

28. Ellenbarrie Industrial Gases

29. TruAlt Bioenergy

30. SMS Pharmaceuticals

31. H.G. Infra Engineering

32. Kolte-Patil Developers

33. Prakash Industries

34. Unichem Laboratories

35. Marsons

36. Morepen Laboratories

37. Prabha Energy

38. Pix Transmissions

39. EIH Associated Hotels

40. Belding India

41. Jindal Drilling

42. Paramount Communications

43. TCC Concept

44. GHV Infra Projects

45. Godavari Biorefineries

46. Vikran Engineering

47. All Time Plastics

48. Precision Camshafts

49. Yatra Online

50. Southern Petrochemicals Industries Corp

51. Syncom Formulations (India)

52. Tinna Rubber and Infrastructure

53. Gulshan Polyols

54. Excel Industries

55. Faze Three

56. Motisons Jewellers

57. Industrial & Prudential Investment

58. Tarsons Products

59. Dam Capital Advisors

60. Hariom Pipe Industries

61. SKM Egg Products Export (India)

62. Excelsoft Technologies

Disclaimer: bit.ly/R_disclaimer02

1

15

1,879

May 21

Quarterly earning results to watch out

May 22, Friday - Tomorrow

•#20microns - 20 Microns Ltd

•#3mindia - 3M India Ltd

•#Birlacable - Birla Cable Ltd

•#Centuryply - Century Plyboards India

•#Cewater - Concord Enviro Systems Ltd

•#Colpal - Colgate Palmolive India Ltd

•#Damcapital - DAM Capital Advisors Ltd

•#Eichermot - Eicher Motors Ltd

•#Eihahotels - EIH Associated Hotels Ltd

•#Ellen - Ellenbarrie Industrial Gases Ltd

•#Emil - Electronics Mart India Ltd

•#Faze3q - Faze Three Ltd

•#Fortis - Fortis Healthcare Ltd

•#Gokex - Gokaldas Exports Ltd

•#Greenlam - Greenlam Industries Ltd

•#Gsfc - Gujarat State Fertilizers

•#Hariompipe - Hariom Pipe Industries Ltd

•#Hginfra - HG Infra Engineering Ltd

•#Hindalco - Hindalco Industries Ltd

•#Indigopnts - Indigo Paints Ltd

•#Ircon - IRCON International Ltd

•#Jindrill - Jindal Drilling & Industries Ltd

•#Jublpharma - Jubilant Pharmova Ltd

•#Kovai - Kovai Medical Center

•#Mahseamles - Maharashtra Seamless

•#Maxestates - Max Estates Ltd

•#Morepenlab - Morepen Laboratories

•#Mvgjl - Manoj Vaibhav Jewellers

•#Naukri - Info Edge India Ltd

•#Nh - Narayana Hrudayalaya Ltd

•#Ntpcgreen - NTPC Green Energy Ltd

•#Pixtrans - Pix Transmissions Ltd

•#Precam - Precision Camshafts Ltd

•#Prostarm - Prostarm Info Systems Ltd

•#Ramcocem - The Ramco Cements Ltd

•#Shilpamed - Shilpa Medicare Ltd

•#Skmeggprod - SKM Egg Products

•#Smspharma - SMS Pharmaceuticals Ltd

•#Sunpharma - Sun Pharmaceutical

•#Syncomf - Syncom Formulations India Ltd

•#Torntpharm - Torrent Pharmaceuticals Ltd

•#Trualt - Trualt Bioenergy Ltd

•#Ttkprestig - TTK Prestige Ltd

•#Tvselect - TVS Electronics Ltd

•#Unichemlab - Unichem Laboratories Ltd

•#Vikran - Vikran Engineering Ltd

•#Yatra - Yatra Online Ltd

1

6

1,221

May 20

$AVEX earnings call had some things worth flagging

The 4 core programs (OWA, LRPS, Launched Effects, Syncom) already represent >$2B in opportunity value. But what stood out more was what’s not in guidance yet:

— USV (unmanned surface vehicles) quietly being built out

— International: Finland, Chile, Lithuania already won. Single digits % of revenue today, expected to grow significantly. At accretive margins.

— Zero Ukraine follow-on is in the 2027 numbers. If it comes: pure upside.

Management on Ukraine: “if they come through, we’re well positioned to execute — it’ll offer upside to our existing forecasted growth rates”

30 customers, 100 active contracts/year. This isn’t a one-trick pony.

Book-to-bill 1.16x. Backlog expected higher at year-end than start. 2027 growth guided with conviction.

Still a small cap. Still under the radar. That’s the point.

$AVEX

6

473