27 Dec 2025

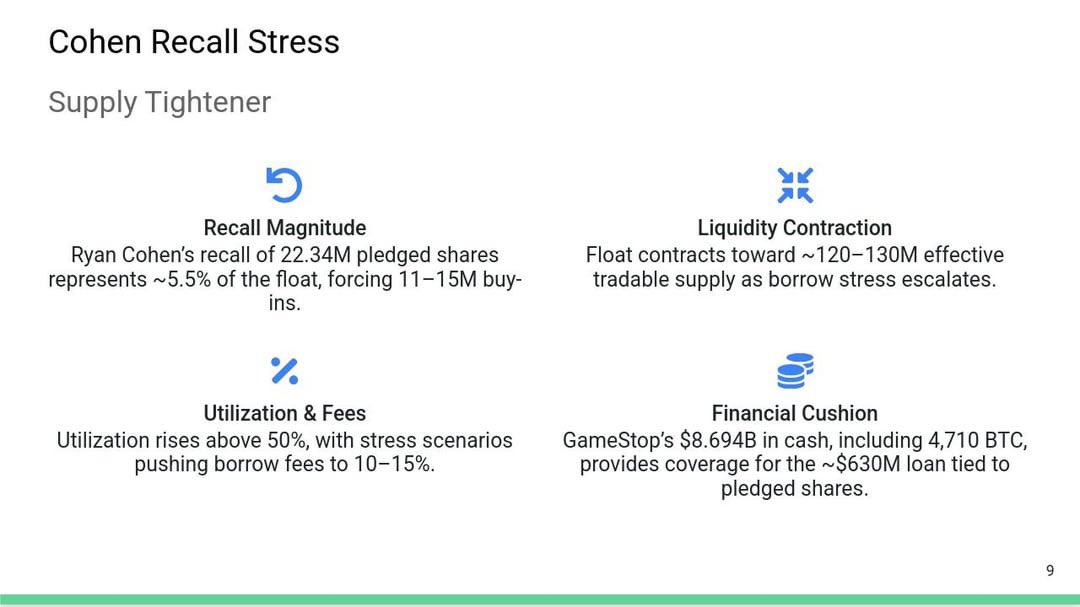

1 Ryan Cohen recall of 22.34M shares on loan as collateral

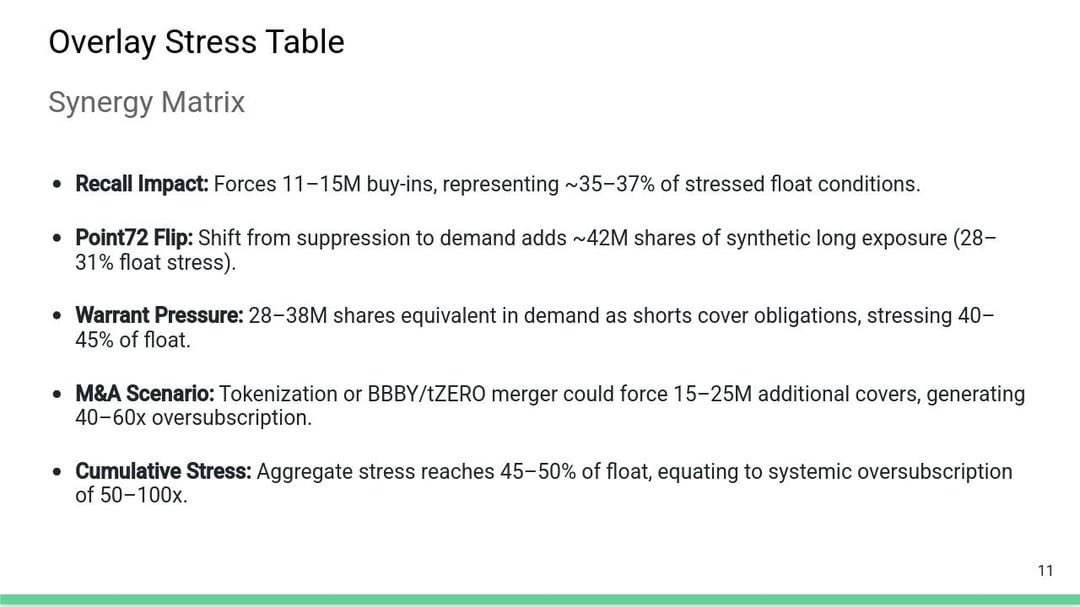

2 removes 11–15M loaned shares, stress on borrow pool. (Assuming 50% loan and no rehypotication

3 Point72 unwind of 3.85M put hedge results in 85% exposure gone, net long via calls.

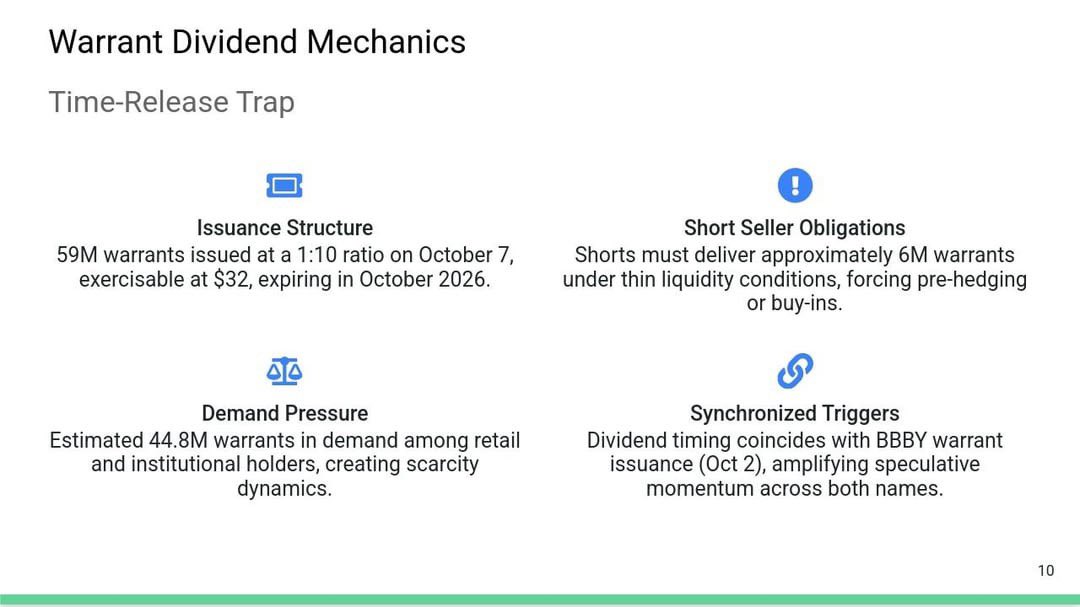

4 Warrant dividend (59M issued) → shorts owe ~6M (on book assumes mismatches with synthetics calculated through FTD’s

5 Bb/ttZERO merger scenario → tokenized float audit, 15–25M forced covers.

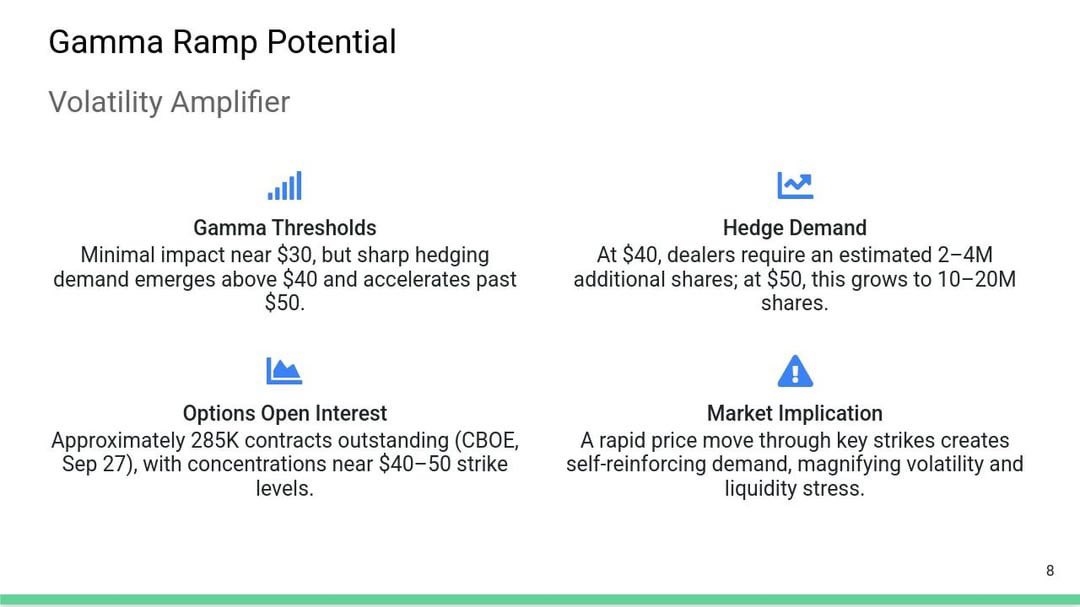

Combined stress: 35–45% of float under pressure → 2021-style squeeze risk, extended duration 2025

1

2

51

1. Stainless (TTZero)

2. Illiterate graduate

3. You forget I am a mathematics graduate

4. She texted me first

5. Park chairman

6. Orgy organizer

7. Property pawn

8. TG Oboughri (Oko Lagos LGBTQIA )

9. “This plug no take him hustle serious”

10. Kosewe Kosepo

19 Oct 2025

73. Name 10 oomfs without saying their names

2

1

3

995

23 Mar 2025

もう日が変わりましたが

3/23ホビワさんでのタミチャレRd.0にGT TTZERO Mとさんかしてきました

MはMB01よくわかんない

TTはギリAメインだけど結果は…

GRは終盤まで2位を死守したが、一瞬のスキ❤️をつかれましたね

3位です

精進します。

1

1

21

736

2 Mar 2025

今日は新北総サーキット船橋にてレース出てきました!

タミチャレGTはうーん😓

F1はうーん😓

TTZEROはうーん😓

な感じでした💦

次がんばるます💪

1

19

429

14 Jun 2024

来年2025年の #マン島TTレース 日程が確定しました。

スケジュールは今年と同じ。各種予約はもう始まっています。

公式アナウンスはありませんが、#TTZero(電動バイクなどのクラス)は今後復活することはない見込みです

14 Jun 2024

TT 2025 DATES CONFIRMED

With TT 2024 now in the rear-view, the countdown is already on for 2025 with 346 days to go.

Bank Holiday Monday (26th May) #TT2025 begins, concluding with the prestigious Milwaukee Senior TT Race on Saturday 7th June

📆 buff.ly/3KKs1IU

5

50

4,492

17 Apr 2023

Oliveira jogou muito ontem mais a ttzero só reclama dele enquanto o queridinho do Bruno Rodrigues é intocável mesmo jogando nada

5

9

1,135

23 Feb 2023

#ThrowbackThursday way back to 2016 and the never exciting TT Zero race. William Dunlop, Daley Mathison, Matthew Rees & Bruce Anstey

#TTZero #IOMTT #ManxGP #RoadRacing #MotoGP #BSB #Wsbk

📷 C Price

1

18

548

28 May 2022

Hasta ahora había 8 carreras (9 con el TTzero):

- 2 de Superbike (Sbk y Senior).

- 2 de Supersport.

- 2 de Sidecars.

- 1 de Lightweight (Supertwins).

- 1 de Supertock 1000.

Para el 23 habrá 10 carreras, pues añaden una segunda carrera de Lightweight y de Superstock 1000

1

4

25 Jan 2022

𝕾tar 𝕾eekers club presents 𖤣𖥧

b̲e̲h̲i̲n̲d̲ ᴘᴇᴛɪᴏɴɪsᴛᴀ taengoo!

Cozy aftern𝕠𝕠ns with 𝐩aw__𝐩al

{ #𝕥𝕥𝚣𝚎𝚛𝚘 } and me having fun

at the 𝑠𝑜𝑓𝑡core : episode 𝟸𝟶

૮๑ˊ 🧺 ๑ˊ for more su𝕟𝕟y days at

𝚗𝚊𝚝𝚞𝚛𝚎 land ㅡ find us at spc ♡

51

21 Nov 2021

主に初音ミク関連でフォローしてくださった皆様へ

私の名前ttzeroですが、元はこれです

TT零13

ちゃんとフィギュアも買っております

バイクにもレーミクがいるんですよ

6

i’d usually say it’s ok but it’s really not lol, the extent you took things to was almost obsessive. you need help, and you need to never do this to anyone again. your apologies hold no weight now since you’ve said sorry before, but thanks for trying. hope 7th times a charm

6

10 Jun 2021

I was moots with you and I didn’t even noticed that you did this and it’s really disappointing finding this out..

5