At the #EDPS, we monitor emerging technologies to anticipate their impact on #DataProtection. Through TechSonar, TechDispatch and IPEN, we work towards embeding privacy into innovation from the start.

👉 Subscribe to stay informed: link.europa.eu/PkGJQ8

#InCaseYouMissedIt

ALT TechSonar and TechDispatch logos on an abstract digital data background

4

494

New #TechDispatch on Digital Identity Wallets 🚨

#EDPS has published its latest TechDispatch on Digital Identity Wallets (DIWs) titled "The path towards a data protection by design and by default approach"

Learn more link.europa.eu/BJJnnj

5

5

642

#TePuedeInteresar 💡

De la ‘IA con humano’ a la supervisión humana efectiva”

El nuevo TechDispatch by @EU_EDPS desmonta mitos: humano en el loop ≠ control real.

La supervisión significativa exige:

• Agencia para contradecir al sistema.

• Tiempo y formación para revisar.

• Interfaces y explicabilidad orientadas a la decisión.

• Auditoría, muestreo y desconfianza institucionalizada para evitar la “supervisión decorativa”.

Resultado: menos sesgos, más confianza y cumplimiento.

#Compliance #Ciberseguridad #AI #DataProtection #EthicsByDesign

edps.europa.eu/system/files/…

2

5

293

🔴The new #TechDispatch is out! AI-driven systems increasingly make decisions shaping people’s lives. How do we ensure fairness & rights protection?

Read more 👉 link.europa.eu/WGpfgp

1

2

5

569

At the #EDPS, we monitor, assess and oversee tech developments and IT systems to ensure #EUIs process personal data securely and lawfully.

🔍 How we do it: europa.eu/!96kY4x

📘 Read our #TechDispatch reports: europa.eu/!qWvRYk

#InCaseYouMissedIt

3

3

676

🔴 #TechDispatch on Federated Learning is out now!

Read the #EDPS & @AEPD_es TechDispatch on FL and how it is developing machine learning by allowing multiple data sources to collaboratively train a shared model while keeping data decentralised.

➡️europa.eu/!qWvRYk

7

5

1,057

#InCaseYouMissedIt 🔒 At #EDPS, our #Technology & #Privacy unit anticipates tech trends in data protection. How? With #TechSonar & #TechDispatch reports exploring tech's challenges & opportunities to safeguard citizens' rights 👉europa.eu/!YvdKRj & europa.eu/!mkRqct

ALT Illustration on purple background with the logos of two EDPS projects: Techsonar and Techdispatch

1

2

4

690

#InCaseYouMissedIt

Who says you can’t learn something about data protection with a podcast you can enjoy anywhere? ☀️

✅ Interviews w/experts

✅ Bite size info on EDPS work w/ Newsletter Digest

✅ Tech trends w/ TechDispatch Talks

Discover EDPS On Air europa.eu/!WcHyCx 🎧

ALT EDPS on air podcast logo on a blue background

4

5

749

13 Aug 2024

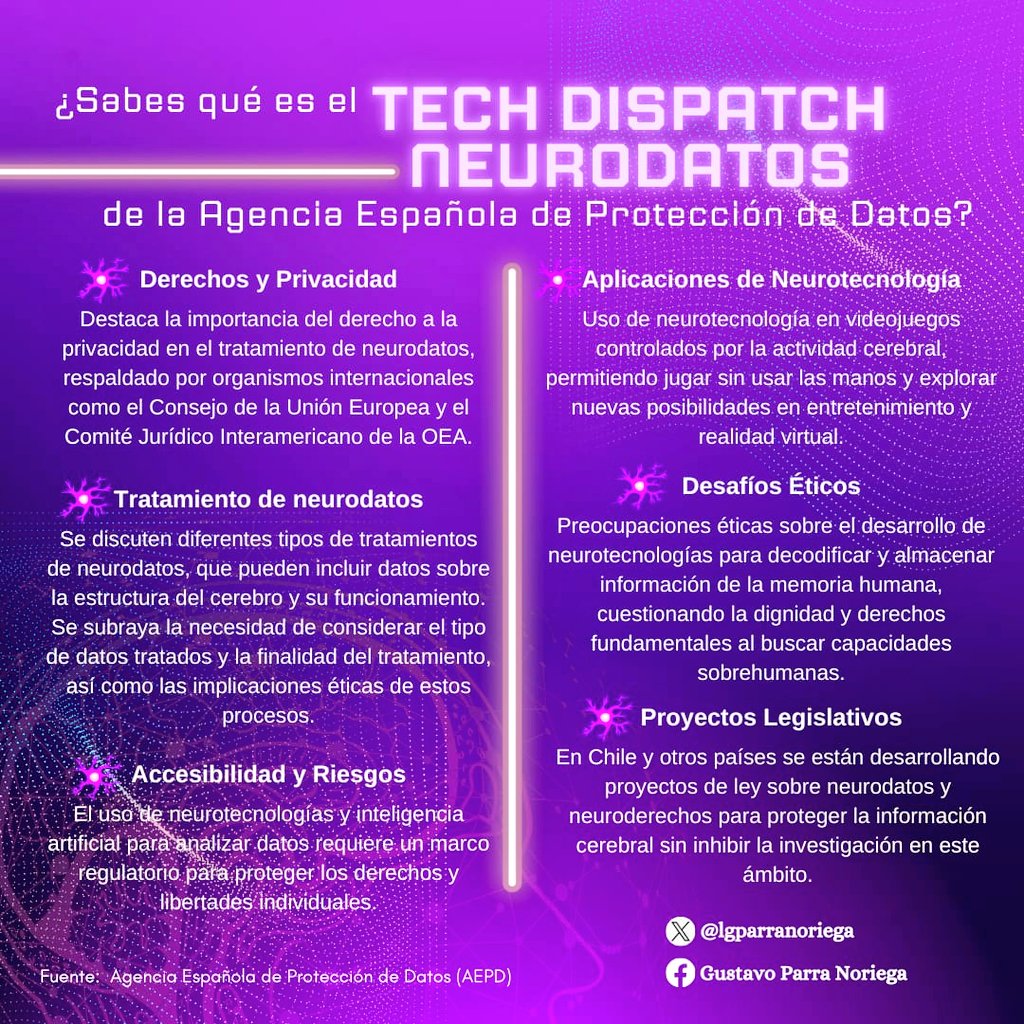

Conoce los temas que se desarrollan en el documento “TechDispatch Neurodatos” de la @AEPD_es y la @EU_EDPS, sobre las implicaciones éticas y legales del uso y protección de los #Neutodatos. #PrivacyProtection

Consulta aquí: aepd.es/guias/neurodatos-aep…

4

11

268

#InCaseYouMissedIt Stay up-to date with new and emerging #technologies, their opportunities and limits, with our TechDispatch reports. Subscribe to not miss our next edition europa.eu/!YP87wU and read our latest issue on Neurodata & Neurotechnologies europa.eu/!vW9GFt

ALT Violet, pink and yellow visual to illustrate the techdispatch report on neurodata

3

640

TechDispatch Talks ep3 is out now!

#EDPS & @ @AEPD_es @MBeltranPardo discuss the topic of Neurodata & Neurotechnologies.

🎙️Have a listen on our website, on Spotify #EDPSonAir, or wherever you get your podcasts!

🔗europa.eu/!6v737Y

5

7

1,240

📢New #TechDispatch is out!

Learn about #Neurodata - Neurotechnology has a positive impact on the lives of individuals, e.g. in medical treatment. However, its misuse in marketing or education poses ethical & legal risks

In cooperation w @AEPD_es

Read now europa.eu/!vW9GFt

5

10

1,311

4 Jan 2024

🚀 Exciting News! 🌍 Goods Dispatched to Iraq! 🇮🇶

We are Thrilled to announce the dispatch of cutting-edge products to Iraq! 🌟✨

Our innovation & quality reflect in each product, tailored for your tech experiences! 💡🌐

#TescaTechnology #Innovation #TechDispatch #Iraq

2

3

147

What is explainable artificial intelligence? What are the risks of opaque #AI systems and how can #AI embed transparency, interpretability and explainability? Read our latest #TechDispatch on #XAI to find out more now available here europa.eu/!JTpWny

ALT boxes

1

18

29

4,633

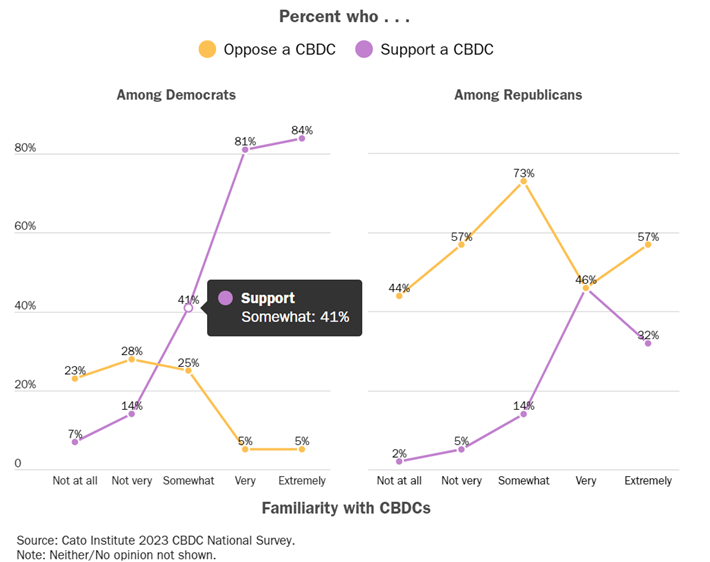

6 Oct 2023

Will governments be able to resist the greater control they have over their currencies by issuing Central Bank Digital Currencies (CBDCs)?

In the next few weeks, the EU Parliament is set to vote on legislation that will set guidelines for and permit the ECB to continue researching and testing the launch of an ECB-backed #CBDC, #CBDCs .

If this vote passes, momentum will continue to build towards a launch in the next 2-3 years. If the EU Parliament authorizes the ECB to proceed, the likelihood of a US CBDC is likely to rise.

Here is a discussion of the issues and why the EU may vote to proceed. Advocates of CBDCs point to the following potential benefits:

1) Improve the payments systems

a. Instantaneous transactions

b. Help the unbanked population with banking services

c. Lower costs of retail transactions

d. Securing privacy of transactions

e. Ease of use

2) Protect against the rise of private digital currencies and foreign CBDCs

3) Prevent, detect and enforce financial crimes

4) Secure privacy

a. Private companies cannot be trusted with consumer spending data

b. Today’s financial system is already monitored closely by private sector and government surveillance; a CBDC would change this only modestly and would make it more efficient and effective

5) Enhance innovation in payments

It is worth noting that a feature of a CBDC, and not one that is being touted by advocates, is that CBDCs are software-based, and therefore programmable. This would allow governments to control welfare payments for instance, and central banks to more directly implement monetary policy.

Opponents cite the following issues:

1) Security:

a. Government control provides a single point of failure and an attractive target for cyber-attacks from the outside

b. Government control is also vulnerable to abuse from bad actors inside

2) CBDCs displace deposits in fractional banking, cannot be used for leverage or lending

3) CBDCs displace payment systems as digital currencies can be transmitted instantaneously at low/no cost

4) Concentration of power in the federal government a. CBDCs are centralized, not decentralized, and therefore cannot be reliably monitored

b. This means they can be programmed to monitor, control, cancel, and target

c. This means there is no reliable means to prevent these from occurring US CBDC:

The chances that a US CBDC gets approved and issued are remote for now. Not only is there very little public support for the issuance of a CBDC, but there is also a very vocal group of elected officials in Congress who will fight aggressively against it, as well as a bipartisan group that are against: likely due to the American heritage of individual rights, liberty and privacy. Though there are supporters, Congress is also lacking proponents that are vocal about advocating for a CBDC.

It is worth discussing some of the “benefits” listed above:

1) Improve the payments system.

Many disagree that in the developed world, the private sector has already implemented the technologies that have led to payments improvements. In testimony before the House Financial Services Committee on September 14, 2023, a main theme was that a US CBDC would not improve what is an efficiently functioning banking and payments system in the US.

2) Protect against the rise of private digital currencies.

The OECD emphasized this, but in the US, there is little fear that crypto currencies pose enough of a threat to the US payments and banking infrastructure that it needs to be addressed at this point and that even if it did, that a CBDC would be an effective alternative to the private sector. There is likely an element of skepticism of foreign companies in other parts of the world like Europe that is missing in the US.

3) Financial crimes prevention is a universally shared benefit of CBDCs that can be programmed to monitor transactions.

4) Secure Privacy.

For Europeans, this is a perceived positive - many trust the government more than private companies, especially foreign ones. In the US, there is a greater confidence that the private sector has checks and balances including answering to customers, employees, shareholders and government regulators that the government is not reliably subject to.

5) Improve innovations in finance.

Much like privacy, there are advocates of public sector competition, and opponents argue that government damages free market competition by virtue of its different motivations.

Problem #1: CBDCs erode the capital base of banks and reduce lending capacity. As a direct liability of the central bank, banks cannot hold CBDC balances except as a custodian. This is what Representative Sean Casten (D-IL) focused on as an inherently self-defeating aspect of any government introduction of a CBDC, in that the more CBDCs (as a percent of monetary base), the lower the lending capacity will be in the banking system, something that would hinder the economic growth of the CBDC issuer. In the EU, the legislation will set limits on CBDC per person to prevent this from inhibiting bank lending capacity to too great an extent.

Problem #2: CBDCs are fundamentally programmable and introduce a single point of failure for controls and security. It is this programmability that is the root of most of the opposition to CBDCs and is one of the primary features of China’s CBDC that is cited as an example. Proponents of CBDCs believe that protections in the original programming are safe from being altered, and the EU legislation offers guardrails, for instance, that prevent certain data in transactions from reaching the ECB. If a CBDC were based on a decentralized and public blockchain, public monitoring would be possible and might prevent altering, but would at least provide detectability. CBDCs however are necessarily centralized and therefore vulnerable to altering. Problem

#3: CBDCs do have the capability of instant and low/zero cost transmission and that hurts Payments Service Providers (PSPs). Proponents of CBDCs believe that payment service providers are charging excessive payments fees and that a CBDC that can be transacted instantaneously and at low/no cost would be a welcomed competitive force to drive costs lower. In the EU, advocates of CDBCs and the EU legislation concede that CBDCs should not burden the free market but offer the solution of ensuring “fair and adequate” compensation, something that would be subject to changing political attitudes, and is not likely to gather much support in the US at this time.

CBDCs are likely to become bigger news if the EU Parliament does pass the legislation in October.

Footnotes:

[1] “It’s not until later in October that the [ECB] Governing Council will decide whether we can move ahead with more piloting of the project,” ECB President Christine Lagarde told lawmakers on the EU Parliament's Economic and Monetary Affairs Committee. Source: Coindesk Article “Digital Euro at least 2 years away” Link HERE.

[2] Briefing, EU Legislation in Progress, Martin Hflmayer. Link HERE.

[3] “Central bank digital currencies: defining the problems, designing the solutions”- Speech by Fabio Panetta, 2/18/23. Link HERE

[4] “SEEING THROUGH MONEY: DEMOCRACY, DATA GOVERNANCE, AND THE DIGITAL DOLLAR” Raúl Carrillo. Link HERE

[5] “Central bank digital currencies: defining the problems, designing the solutions”. Speech by Fabio Panetta 2-18-22. Link HERE .

[6] McKinsey report “Central bank digital currencies: An active role for commercial banks” 10/13/22. “Some central banks perceive erosion in their role as payments innovators—thought leaders advancing next-generation models beyond today’s cash and infrastructure. CBDCs offer the potential to improve on legacy cash use cases, such as by reducing cross-border transaction costs and enhancing financial inclusion. By spearheading the design process and clarifying use cases, central banks can ensure that these strategic conversations take place in a public forum.” Link HERE.

[7] BIS Report on CBDCs – March 2018. Link HERE

[8] Testimony before the House Financial Services Committee on September 14, 2023. Link HERE.

[9] Bank Policy Institute: 4/7/21, Link HERE

[10] McKinsey Report: “What is central bank digital currency (CBDC)?” Link HERE

[11] Testimony before the House Financial Services Committee on September 14, 2023. Link HERE.

[12] Testimony before the House Financial Services Committee on September 14, 2023. Link HERE.

[13] Cryptocurrency Dangers and the benefits of EU Legislation, Ref.: 20220324STO26154. Link HERE.

[14] “Know your (holding) limits: CBDC, financial stability and central bank reliance”; Barbara Meller, Oscar Soons. This paper studied the impact of how an EU CBDC would erode the lending capacity of the EU banking system and concluded that had a limit of Euro3,000 per person applied to the EU banking system in 2021 and 2019 “that bank funding structures would not have changed extraordinarily and no additional Eurosystem funding would have been needed.” Link HERE.

[15] “TechDispatch #1/2023 - Central Bank Digital Currency”, “Programmability of CBDC is also an important design choice. Programmable payments are different from programmable money. Programmable money consists of a CBDC with built-in rules, imposing restrictions on the usage of that money. With this feature, a government could also define a positive or negative interest rate to incentivise or disincentive the use of money for the purchase of a particular good; limit its use to a certain category of services; set an expiry date. Programmable payments enable automatic transfers of money when pre-determined conditions are met. For example, a person can instruct their bank account to send a certain amount of money at the end of every month to another account. In a machine-to-machine payment scenario, payments can be automated and money can be sent when a parcel is checked as delivered at a certain store room. At the same time, CBDC could be used as payments programmed as automatic transfers by a State actor (e.g. for welfare payments). While programmability of money needs to be wired in the core design features of a CBDC, and it is something that has been rarely natively implemented in the current payment system, the case for programmable payments is different. We can already program our payments throughout bank accounts. In a similar way, in case of CBDC, the programmability of money would be provided, as value-added services, by financial institutions to their customers (notably businesses and citizens), on top of the CBDC infrastructure.”

[16] “U.S. Adoption of a Central Bank Digital Currency Could Revitalize Payments Markets With Competition”, Owen Glist, Kristian Soltes. Link HERE. [17] Questioning and testimony before the House Financial Services Committee on September 14, 2023. Link HERE.

#Libertarian

28

66

319

93,377

#InCaseYouMissedIt Interested in new, emerging technologies? Would you like to learn more about Central Bank Digital Currency or Fediverse? Subscribe to our #TechDispatch reports here: europa.eu/!YP87wU Listen to our TechDispatch Talks on the go: europa.eu/!M68dXN

ALT TechDispatch Talk logo

4

3

1,011

🚀Update from the 52nd #EDPS DPO Meeting: Luis Velasco Head of the EDPS Technology a f Privacy Unit highlights recent achievements and challenges, in particular our #Techdispatch on CBDC europa.eu/!wFGXNK & upcoming #IPEN event on Explainable #AI europa.eu/!rRQKWD

ALT Luis Velasco speaking, behind him the flags of the EU member states

5

6

1,091

Newsletter #101 is out! Looking for something to do in May? Meet us & @EU_EDPB at EU Open Day ! Also in this edition, our key achievements of 2022, TechDispatch on Central Bank Digital Currency. Catch up on our Newsletter Digest podcast episodes as well europa.eu/!WfhTwc

ALT person on a bike with flowers

7

9

1,235