Jun 11

Threat Brief: Escalation of Cyber Risk Related to Iran.

In late March 2026, Unit 42 discovered a new cluster of threat activity we are tracking as CL-STA-1128 (aka Cyber Av3ngers, Storm-0784).

The attacker behind this activity targeted operational technology and industrial control systems (OT/ICS) equipment manufactured by Rockwell Automation.

This activity represents a shift from the cluster’s historic focus on internet-connected Unitronics programmable logic controllers (PLCs).

On April 7, the U.S. Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency (CISA) released an advisory mirroring our findings.

In particular, CISA noted that Cyber Av3ngers was also exploiting PLCs manufactured by Allen-Bradley.

unit42.paloaltonetworks.com/…

42

【2023年の記事】イランのサイバー攻撃者がUnitronics社のシステムを侵害 | SOPHOS sophos.com/en-us/blog/irania…

3

343

May 22

𝗔𝗺𝗯𝗲𝗿 𝗘𝗻𝘁𝗲𝗿𝗽𝗿𝗶𝘀𝗲𝘀 𝗜𝗻𝗱𝗶𝗮 𝗟𝘁𝗱. 𝗤4 & 𝗙𝗬'26 𝗘𝗮𝗿𝗻𝗶𝗻𝗴𝘀 𝗖𝗮𝗹𝗹 𝗦𝘂𝗺𝗺𝗮𝗿𝘆 📈:

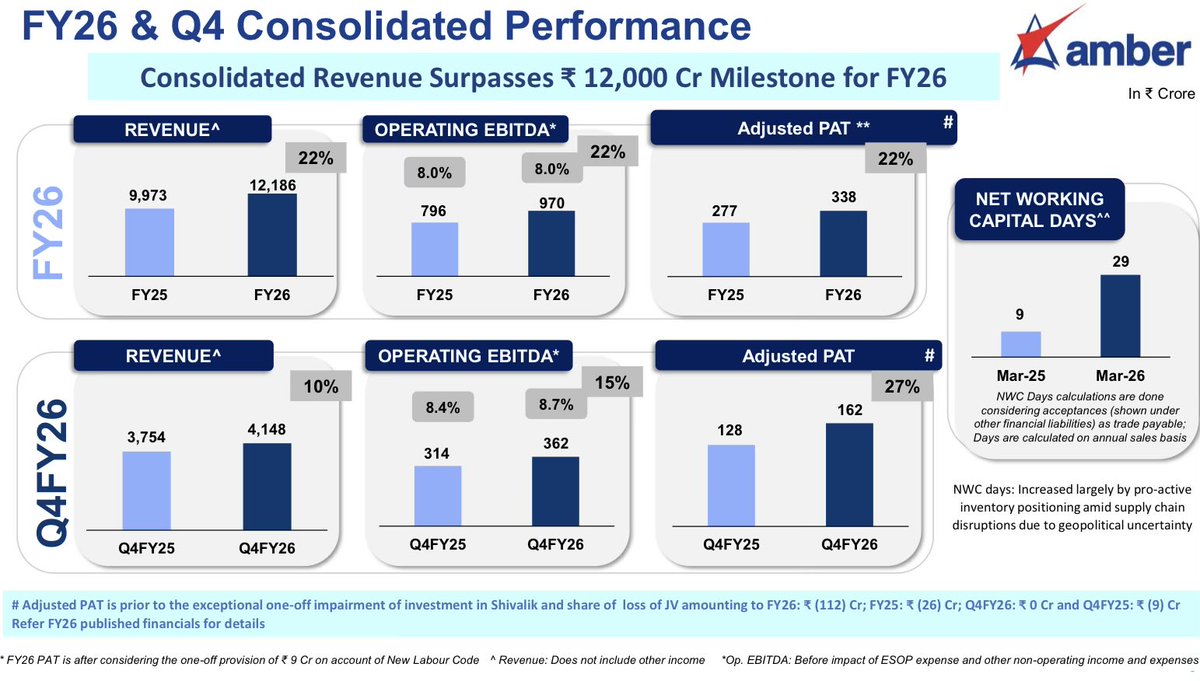

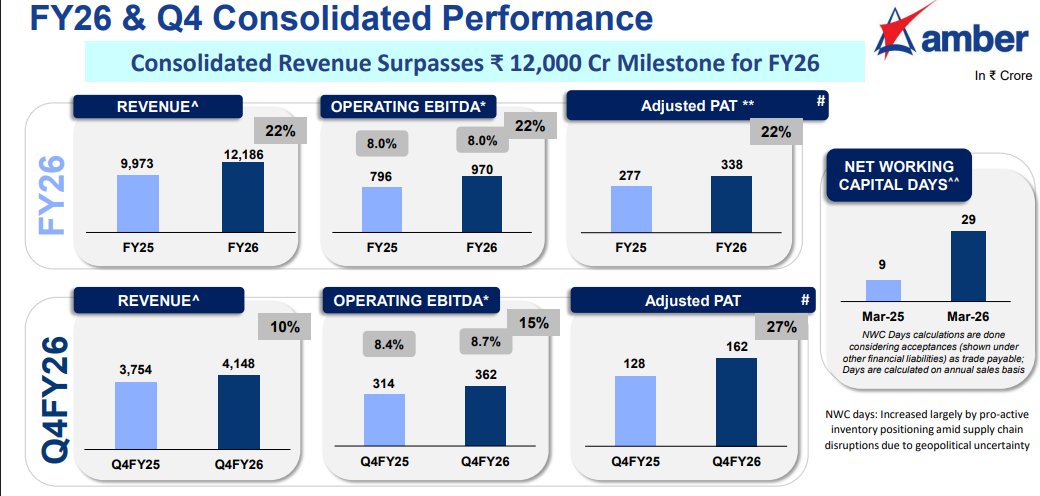

Amber Enterprises India Limited achieved a significant milestone in FY'26, with consolidated revenue surpassing ₹12,000 𝗰𝗿𝗼𝗿𝗲𝘀, reaching ₹12,186 𝗰𝗿𝗼𝗿𝗲𝘀, marking a robust 22% 𝗬𝗼𝗬 𝗴𝗿𝗼𝘄𝘁𝗵. This strong performance was driven by resilience across all three diversified divisions.

𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 𝗳𝗼𝗿 𝗙𝗬'26:

- 𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗲𝗱 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹12,186 Cr (↑ 22% YoY)

- 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗘𝗕𝗜𝗧𝗗𝗔: ₹970 Cr (↑ 22% YoY)

- 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗣𝗔𝗧: ₹338 Cr (↑ 22% YoY)

𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻𝗮𝗹 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- 𝗖𝗼𝗻𝘀𝘂𝗺𝗲𝗿 𝗗𝘂𝗿𝗮𝗯𝗹𝗲𝘀 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻:

▸ Revenue grew 14% 𝗬𝗼𝗬 to ₹8,383 Cr, outperforming the flattish industry due to challenging weather conditions.

▸ Augmented RAC production capacity at Sri City.

▸ Proactive inventory buildup to mitigate supply chain risks.

▸ Expects industry volume growth of 12-13% for FY'27, with Amber moving in tandem.

▸ Rupee per unit margin remains intact despite price inflation. 💰

- 𝗘𝗹𝗲𝗰𝘁𝗿𝗼𝗻𝗶𝗰𝘀 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻:

▸ Strong growth momentum with revenue of ₹3,268 𝗖𝗿 (↑ 49% 𝗬𝗼𝗬).

▸ Operating EBITDA surged 89% 𝗬𝗼𝗬 to ₹287 Cr.

▸ Expected to grow by ~40% in FY'27.

▸ Strategic expansion includes partnerships & increased stake in Unitronics (Israel) to 50.4%.

▸ Significant investment approvals for Ascent-K Circuit (Noida) & Ascent Circuits (Hosur) for HDI & multilayer PCB manufacturing.

▸ Bare PCB business well-positioned to become India's largest PCB manufacturer.

▸ Margins in PCBA are ~5%, PCB ~12-13%.

- 𝗥𝗮𝗶𝗹𝘄𝗮𝘆 𝗦𝘆𝘀𝘁𝗲𝗺𝘀 & 𝗗𝗲𝗳𝗲𝗻𝘀𝗲 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻:

▸ Revenue growth of 19% 𝗬𝗼𝗬 to ₹535 Cr.

▸ Operating EBITDA grew 8% 𝗬𝗼𝗬 to ₹90 Cr.

▸ Sidwal's new Greenfield facility in Faridabad is ready for commercial production.

▸ Optimistic of 30-35% growth for FY'27 & FY'28, backed by a strong order book of ₹2,600 Cr .

▸ Margins expected in the range of 16-17%.

𝗞𝗲𝘆 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗜𝗻𝗶𝘁𝗶𝗮𝘁𝗶𝘃𝗲𝘀 & 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻:

- 𝗣𝗖𝗕 𝗠𝗮𝗻𝘂𝗳𝗮𝗰𝘁𝘂𝗿𝗶𝗻𝗴: Investment approvals of over ₹4,500 Cr for HDI PCB & multilayer PCB applications. Ascent-K Circuits' HDI PCB facility construction to commence by June '26, with trial production by Q3 FY'28. 🏭

- 𝗜𝗻𝗱𝘂𝘀𝘁𝗿𝗶𝗮𝗹 𝗔𝘂𝘁𝗼𝗺𝗮𝘁𝗶𝗼𝗻: Increased stake in Unitronics (Israel) to 50.4%.

𝗙𝘂𝘁𝘂𝗿𝗲 𝗢𝘂𝘁𝗹𝗼𝗼𝗸 & 𝗖𝗵𝗮𝗹𝗹𝗲𝗻𝗴𝗲𝘀:

- 𝗚𝗿𝗼𝘄𝘁𝗵 𝗠𝗼𝗺𝗲𝗻𝘁𝘂𝗺: FY'27 is poised for strong growth.

- 𝗠𝗮𝗿𝗴𝗶𝗻 𝗛𝗲𝗮𝗱𝘄𝗶𝗻𝗱𝘀: Anticipates a temporary margin pressure of 50-100 bps at the consolidated level due to high commodity prices (CCL, Gold ↑ ~60%), currency depreciation, and minimum wage revisions.

- 𝗖𝗼𝗺𝗺𝗼𝗱𝗶𝘁𝘆 𝗖𝗼𝘀𝘁𝘀: Copper clad laminate prices increased >60% YoY; Gold prices also up ~60% YoY. Price increases are being passed on with a lag.

- 𝗖𝗮𝗽𝗲𝘅: FY'27 capex expected around ₹1,200-1,300 Cr (cash outflow), with FY'28 around ₹1,400-1,500 Cr. Significant incentives expected for PCB projects. 💰

- 𝗡𝗲𝘁 𝗗𝗲𝗯𝘁: Stood at ₹511 Cr in March '26. Expected to increase slightly to ₹700-800 Cr by end of FY'27.

- 𝗣𝗟𝗜 𝗦𝗰𝗵𝗲𝗺𝗲: Expected to receive ₹78 Cr in FY'27 for FY'26.

The company is focused on balancing volume & value plays in its B2B model, strengthening its position in high-margin, sticky businesses with entry barriers. 💪

📊 AMBER ENTERPRISES INDIA LTD | 🏷️ Earnings Call Transcript

🌐 Details: wegro.app/tk3dEs

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

1

5

128

May 18

Amber Enterprises Ltd Concall Summary for Q4FY26

🔹 MANAGEMENT

• Revenue crossed ₹12,000 Cr milestone

• Strong growth across all divisions

• Electronics expansion accelerated

• PCB ecosystem scaling rapidly

🔹 OUTLOOK

• Electronics business guided 40% growth

• Electronics EBITDA margin target 9.5%-10%

• Sidwal revenue growth guided 30%-35%

• RAC industry growth estimated 12%-13%

• Temporary 50-100 bps margin pressure expected

🔹 INDUSTRY

• CCL prices surged over 60%

• Gold prices also jumped 60%

• Haryana wage hike reached 35%

• RAC import relaxations extended

• Electronics localization opportunity expanding

🔹 GROWTH DRIVERS

• Mega HDI PCB plant construction starts June 2026

• Unitronics Israel stake increased to 50.4%

• Sidwal Faridabad facility commissioned

• Automotive PCBA alliance with Sumitronics

• ODM conversion improving margins

🔹 PRODUCT MIX

• Shift toward higher-value ODM solutions

• B2B electronics exposure increasing

• Industrial automation portfolio expanding

• Aerospace and medical electronics scaling

🔹 RISKS

• Two-quarter pricing lag in PCB business

• Fixed-price railway contracts vulnerable

• Commodity inflation impacting margins

• Environmental approval delays impacted Hosur

🔹 FINANCIALS

• Revenue ₹12,186 Cr ( 22%)

• EBITDA ₹970 Cr ( 22%)

• Adjusted PAT ₹338 Cr ( 22%)

• Electronics revenue ₹3,268 Cr ( 49%)

• Consumer durables revenue ₹8,383 Cr

• Net debt reduced to ₹511 Cr

🔹 KEY TAKEAWAYS

• Amber evolving into diversified electronics platform

• PCB leadership position strengthening

• Strong railway order book visibility

• Long-term import substitution opportunity large

• Short-term margins under pressure from inflation

#Amberenterprises #Amber #stockmarket #Q4FY26

2

11

1,445

May 18

Amber Enterprises India Ltd

(CMP: Rs 7,133 | M-Cap: Rs 25,124 cr)

Key Concall Takeaways

🔹Business Segments

Consumer Durables (AC & components): Outperformed flattish industry growth driven by diversification, wallet share gains, and shift to ODM, despite weak RAC demand due to weather.

Electronics: FY26 Revenue/EBITDA/EBITDA Margin at Rs 3,268 cr/Rs 286 cr/8.8%, which was led by strong PCBA/PCB growth and acquisitions.

Railways & Defence: FY26 Revenue/EBITDA/EBITDA Margin at Rs 535 cr/Rs 90 cr/16.8%, driven by metro, railway, and defence demand, backed by a Rs 2,600 cr order book and new Sidwal Greenfield facility starting by 1QFY27.

🔹FY27 Outlook:

Electronics division expected to grow by 40% with margins at 9.5-10% and Railways & Defence to grow by 30-35% with margins at 16-17%. Strong growth momentum expected but temporary margin pressure

🔹Investments & Expansions:

Electronics: Unitronics stake increased to 50.4%. Strategic alliance with Sumitronics (Japan) & ILJIN to expand EMS solutions for Japanese and global customers in India, leveraging ILJIN’s footprint and manufacturing excellence.

Railways & Defence: Sidwal greenfield facility to start production in 1QFY27, while the Yujin JV is progressing across key products like couplers, brakes, and pantographs, supporting future growth.

🔹Electronics manufacturing ecosystem: Approved large investments under ECMS for PCB ecosystem: Ascent-K (Rs 3,200 cr) construction starts June’26 with trial by 3QFY28., Ascent (Rs 991 cr) trial by 2QFY27, and Shogini (Rs 500 cr). Also secured 100-acre land in YEIDA (UP).

🔹Cost pressure: Margins may decline by 50-100 bps due to wage hikes, commodity inflation, currency impact, and pass-through lag (1 quarter for RAC; 2 quarter for PCB & Railways limited pass-through due to fixed-price contracts ), though normalization is expected

🔹Capex: FY26 capex at Rs 1,070 cr and Rs 1,800-2,000 cr planned for FY27 (cash outflow Rs 1,100–1,200 cr), focused on PCB and supported by incentives (Up to 48% plant subsidy for ECMS State incentives) which will be realized over 5-6 years.

🔹Net debt is expected to rise from Rs 511 cr to Rs 700-800 cr, while working capital increased (29 vs 9 days) due to inventory build-up to derisk supply chain.

🔹No major shortage expected in compressor supply, as the government allows 30% import of sub‑2‑ton compressors

Disclaimer: bit.ly/R_disclaimer02

2

4

510

May 18

🚨The Margin Squeeze: Amber Enterprises Slumps 15% 📉 on Rising Input Cost Worries 📈

💠Q4 FY26 Highlights:

▶️Revenue: Rs 4,148 crore (↑ 10% YoY)

▶️Operating EBITDA: Rs 362 crore (↑ 15% YoY)

▶️EBITDA Margins: 8.7% vs. 8.4% (↑ 30 bps YoY)

▶️PAT: Rs 162 crore (↑ 27% YoY)

💠FY26 Highlights:

▶️Revenue: Rs 12,186 crore (↑ 22% YoY)

▶️Operating EBITDA: Rs 970 crore (↑ 22% YoY)

▶️EBITDA Margins: 8% vs. 8% (Flat YoY)

▶️PAT: Rs 338 crore (↑ 22% YoY)

▶️PAT Margins: 2.8% vs. 2.3% (↑ 50 bps YoY)

▶️Cash for the year-end: Rs 231 crore (↑ 9% YoY)

💠Segment Performance:

▶️Consumer Durables: Rs 8,383 crore (↑ 14% YoY)

▶️Electronics: Rs 3,268 crore (↑ 49% YoY)

▶️Railway Sub-systems & Defense: Rs 535 crore (↑ 19% YoY)

🔍 Reason behind fall

Despite strong historical numbers, the stock plummeted following management's warning of a 50-100 basis point margin contraction ahead. This is driven by surging input costs, particularly sharp price hikes in copper-clad laminates for PCBs. Furthermore, new government regulations have tightened supply chains by capping compressor imports, restricting refrigerator units to 40% and air-conditioner units to 30% of previous volumes. These inflationary pressures and regulatory constraints have triggered significant investor concern regarding near-term profitability.

🔍 Analysis:

Amber continues to strengthen its market position through strategic expansion, recently increasing its stake in Unitronics to 50.4%. While the short-term outlook is clouded by costs, the company anticipates a robust FY27, backed by a projected 30-35% growth in the railway division and an expected 40% surge in the electronics segment.

7

1,078

May 16

Amber Enterprises FY26. The print speaks. 📊

🔹 Revenue ₹12,186 Cr ( 22% YoY) — crossed ₹12K Cr for the first time

🔹 Op EBITDA ₹970 Cr ( 22%), margin steady at 8%

🔹 Adj PAT ₹338 Cr ( 22%) ✅

Reported PAT looks -10% - entirely a ₹112 Cr one-off impairment of an Italian JV that’s now sold for ₹1.10 lakh. Cleanup, not a miss. 🧹

The standout: Electronics division. ⚡

📈 Revenue 49% YoY to ₹3,268 Cr

📈 EBITDA 89% YoY, margin 6.9% → 8.8%

📈 Q4 margin hit 10.8% (was 5.9% LY)

🎯 Mgmt guides 40% in FY27

Consumer Durables ₹8,383 Cr ( 14%) — held up well in a weak RAC year. 🌡️

Railway 19%, order book ₹2,600 Cr, 30-35% guided for FY27. 🚆

Inorganic: acquired Shogini, Power-One, Unitronics this year. 🤝 ₹4,700 Cr ECMS-backed PCB capex ahead.

Watch: NWC days 9 → 29. Goodwill ₹1,678 Cr. ⚠️

⚠️Valuations are rich

#AMBER (Not a buy/sell rec.)

3

6

897

May 16

Stop scrolling, log in to CompoundingAI !

Amber Enterprises (AMBER) - Q4 FY26 Results

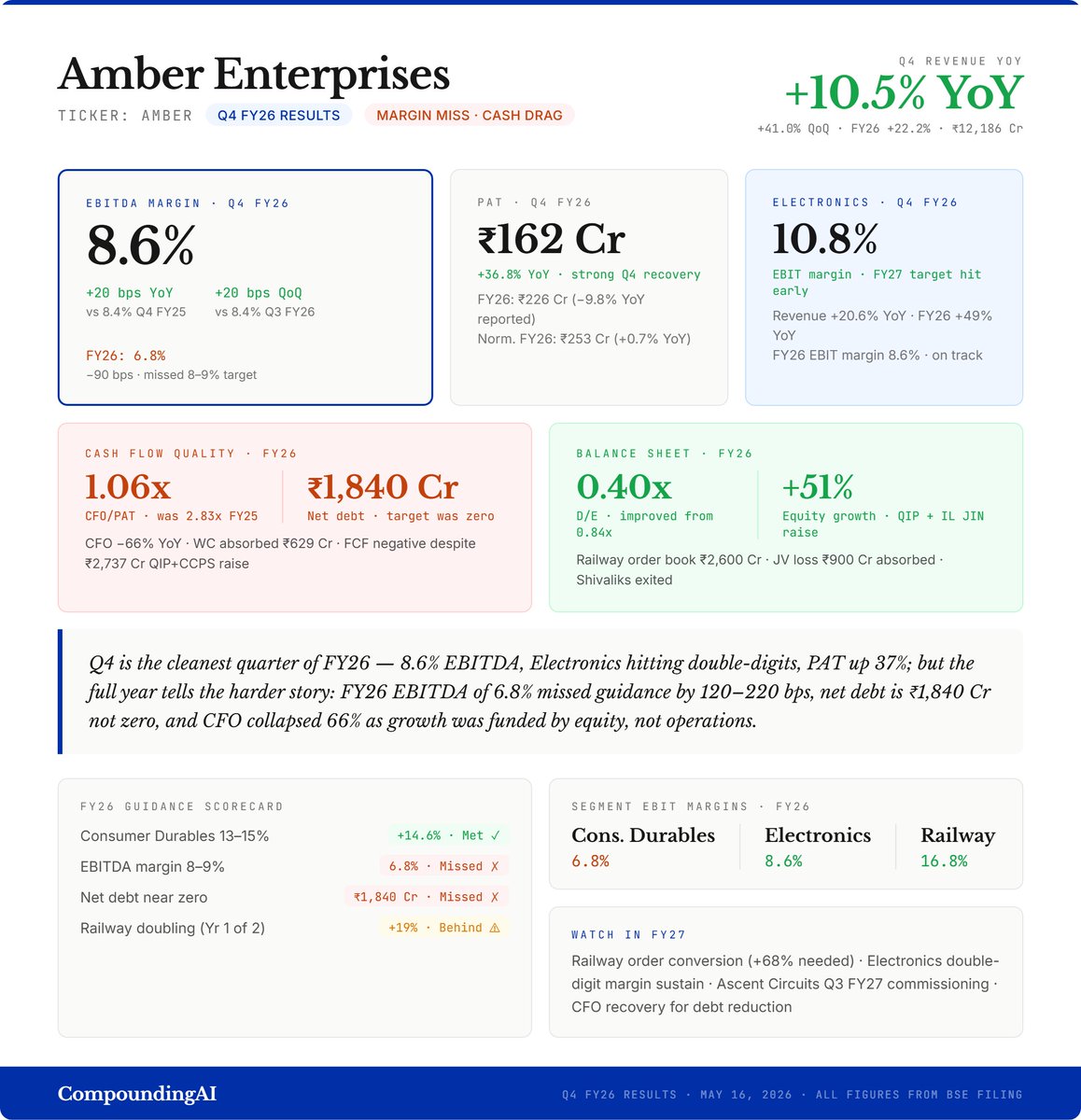

Q4 is the cleanest quarter of FY26. The full year is the harder story.

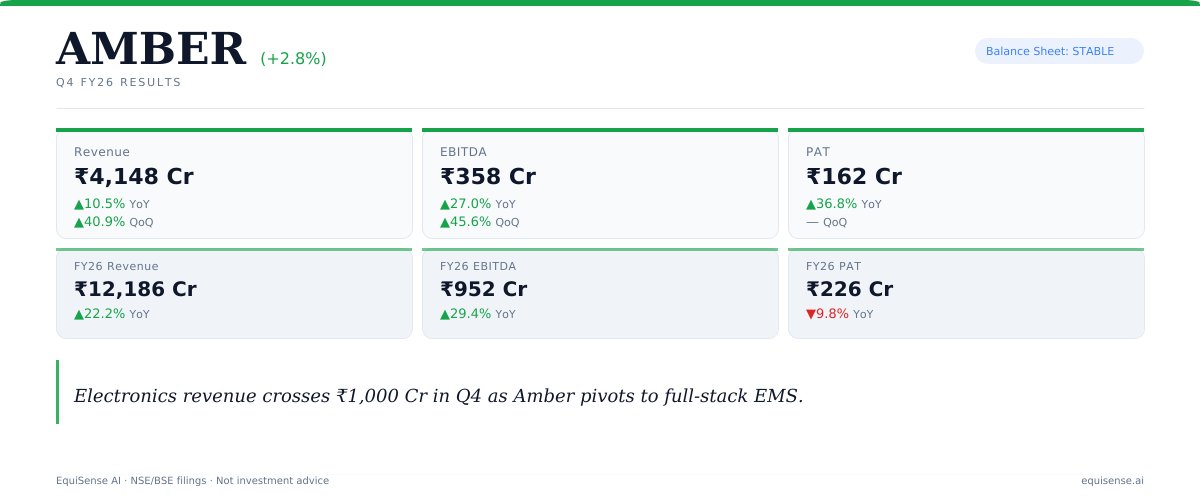

Q4 headline numbers: Q4 revenue: ₹4,148 Cr, 10.5% YoY and 41.0% QoQ - peak summer AC season driving the sequential surge.

Q4 EBITDA margin: 8.6%, 20 bps YoY - improving sequentially and ahead of Q3's 8.4%. Q4 PAT: ₹162 Cr, 36.8% YoY - strong recovery after Q3's loss.

Q4 Electronics EBIT margin: 10.8%, the FY27 double-digit target, achieved a year early.

(FY26 context: revenue ₹12,186 Cr 22.2% YoY; EBITDA margin 6.8%, −90 bps, missed 8–9% guidance; PAT ₹226 Cr −9.8% reported, normalized 0.7% after Firema exceptional items.)

The segment picture:

Consumer Durables Q4: ₹3,032 Cr revenue ( 6.1% YoY), EBIT margin 7.2%. FY26: 14.6% - squarely within the 13–15% guidance. Wallet share gains in a flat industry. Non-AC now ~22% of division.

Electronics Q4: ₹1,015 Cr ( 20.6% YoY). FY26: ₹3,268 Cr, 49% YoY - acquisitions (Unitronics, Power-One, Shogini) contributed. EBIT margin FY26: 8.6%, Q4: 10.8%. The double-digit target for FY27 is already here.

Railway Q4: ₹153 Cr ( 22.2% YoY). FY26: ₹535 Cr, 19% YoY. The problem: management guided doubling from ₹450 Cr FY25 in two years. Year 1 delivered 19%. Year 2 (FY27) needs 68% to hit ₹900 Cr. Order book is ₹2,600 Cr - conversion is the question.

Where the FY26 story gets complicated:

EBITDA margin: 6.8% vs guided 8–9%. Employee costs 41% YoY, depreciation 41% YoY, finance costs 36% YoY - all growing nearly twice as fast as revenue. The acquisition integration is expensive before it's profitable.

JV losses: ₹900 Cr FY26 from Firema (vs ₹300 Cr FY25). Shivaliks exited the JV - the impairment (₹946 Cr in Q3) and the settlement adjustment (₹640 Cr in Q4) together explain why reported PAT fell 9.8% while normalized PAT grew 0.7%.

Cash is the real story:

CFO: ₹240 Cr in FY26 vs ₹711 Cr in FY25 - down 66% YoY. CFO/PAT: 1.06x (from 2.83x). Working capital absorbed ₹629 Cr. FCF is deeply negative. Net debt: ₹1,840 Cr - against a guidance of near zero/cash positive.

The company raised ₹2,737 Cr through QIP and IL JIN's CCPS issuance. Despite that, net debt remains because capex ran ₹1,295 Cr against a ₹700–850 Cr guidance, 52–85% above plan.

What's genuinely positive:

D/E improved from 0.84x to 0.40x - the equity raise structurally deleveraged the balance sheet even if net debt didn't zero out. Electronics hitting double-digit margins ahead of schedule is a meaningful signal on the integration thesis.

Railway order book at ₹2,600 Cr provides real FY27 visibility if execution follows. Ascent Circuits (PCB) commissioning due Q3 FY27 - a new growth vector.

FY26 guidance scorecard:

-Consumer Durables 13–15% → Met (14.6%)

-EBITDA margin 8–9% → Missed (6.8%)

-Net debt near zero → Missed (₹1,840 Cr)

-Railway doubling Year 1 → Behind ( 19%, needs 68% in FY27)

-Capex ₹700–850 Cr → Exceeded (₹1,295 Cr)

FY27 requires margin recovery of 120–220 bps, Railway acceleration of 68%, and CFO improvement to actually reduce debt. The building blocks are visible - Electronics margins, Railway order book, Ascent Circuits. The execution gap between Q4's promise and FY26's delivery is what the market will be pricing.

Note: This is not investment advice.

1

4

1,636

May 16

⚡ Amber Enterprises India

📊 FY26 Consolidated Highlights

• Revenue ▲ 22% YoY – ₹12,186 Cr 💰

• Operating EBITDA ▲ 22% YoY – ₹970 Cr ⚙️

• Operating EBITDA Margin – 8.0% 📈

• Adjusted PAT ▲ 22% YoY – ₹338 Cr 💵

• Gross Profit ▲ 25% YoY – ₹2,239 Cr 🚀

• FY26 Revenue crossed ₹12,000 Cr milestone 🌟

Amber delivered strong growth across all major business divisions 🔥

📊 Q4FY26 Highlights

• Revenue ▲ 10% YoY – ₹4,148 Cr 💰

• Operating EBITDA ▲ 15% YoY – ₹362 Cr 📈

• EBITDA Margin improved to 8.7% ⚙️

• Adjusted PAT ▲ 27% YoY – ₹162 Cr 🚀

• Gross Margin improved to 18.8% 🔥

Operational momentum remained strong despite commodity and currency pressures ⚡

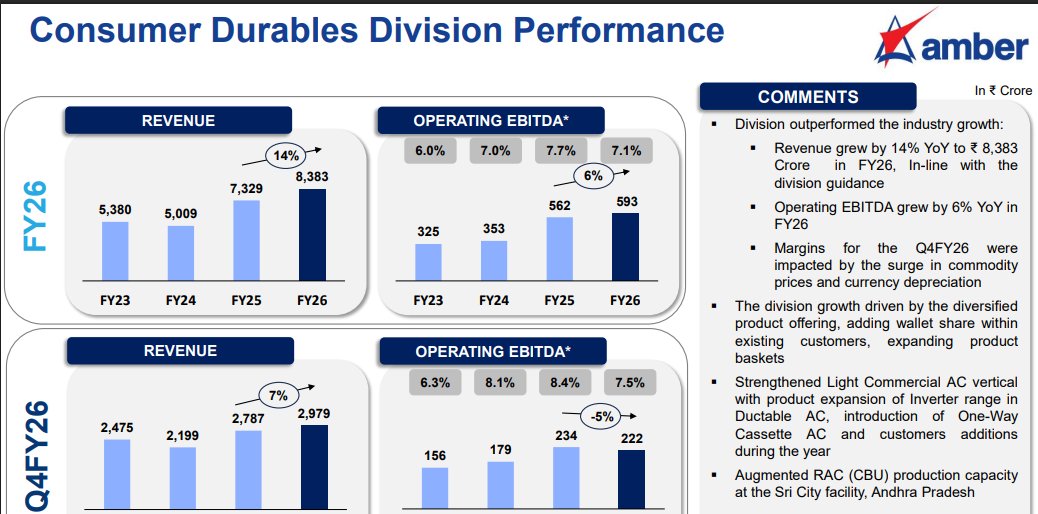

🏭 Consumer Durables Division Performance

FY26:

• Revenue ▲ 14% YoY – ₹8,383 Cr 📈

• Operating EBITDA ▲ 6% YoY – ₹593 Cr ⚙️

• EBITDA Margin – 7.1% 💰

Q4FY26:

• Revenue ▲ 7% YoY – ₹2,979 Cr 🚀

• EBITDA – ₹222 Cr 📊

Key Highlights:

• Division outperformed industry growth 📈

• RAC production capacity expanded at Sri City facility 🏗️

• Diversified product portfolio driving wallet share growth ⚡

• Light Commercial AC portfolio strengthened 🌍

Consumer Durables remains Amber’s largest business vertical 🔥

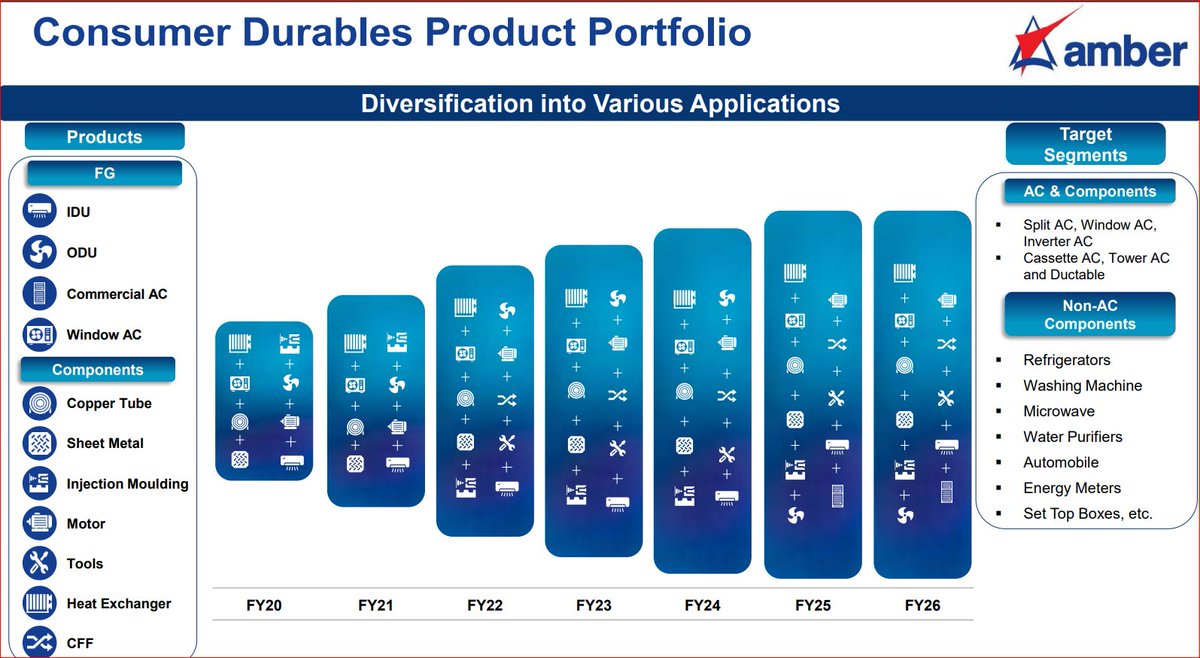

❄️ Massive Consumer Durable Ecosystem

• 24 manufacturing facilities 🏭

• ~70% Bill of Material catering capability ⚙️

• RAC, CAC & components ecosystem 🚀

• Strong diversification beyond RAC CBU business 📈

• RAC CBU contribution reduced from 72% (FY18) to 47% (FY26) 🌍

Amber continues transforming into a diversified manufacturing platform ⚡

🔌 Electronics Division Becoming Major Growth Engine

FY26:

• Revenue ▲ 49% YoY – ₹3,268 Cr 🚀

• Operating EBITDA ▲ 89% YoY – ₹287 Cr 📈

• EBITDA Margin expanded to 8.8% ⚙️

Q4FY26:

• Revenue ▲ 21% YoY – ₹1,015 Cr 💰

• EBITDA ▲ 119% YoY – ₹110 Cr 🔥

• EBITDA Margin surged to 10.8% 🚀

Management expects ~40% revenue growth in FY27 ⚡

🏗️ Strategic Electronics Acquisitions

Amber strengthened electronics division through acquisitions:

• Shogini Technoarts – Bare PCB manufacturing ⚙️

• Unitronics – Industrial automation (PLC & HMI) 🤖

• Power-One Microsystem – Solar inverters, UPS, EV chargers & BESS 🔋

Stake Holdings:

• Shogini – 80% 📈

• Unitronics – 50.4% 🚀

• Power-One – 60% ⚡

Acquisitions are accelerating value-added electronics manufacturing growth 🌍

⚡ Massive Electronics Expansion Pipeline

📍 Ascent-K Circuit Expansion – Jewar, U.P

• JV with Korea Circuit 🇰🇷

• HDI, Flex & Semiconductor Substrate PCB manufacturing ⚙️

• Planned investment – ₹3,200 Cr 💰

• Construction starts June’26 🏗️

• Trial production targeted by Q3FY28 🚀

📍 Ascent Circuits Expansion – Hosur, T.N

• Multi-layer PCB facility ⚡

• Trial production expected Sep/Oct’26 📈

📍 Pune PCB Assembly Expansion

• Facility expansion progressing well 🔥

Amber is positioning itself strongly in India’s electronics manufacturing ecosystem 🌍

🏭 ECMS & Land Allocation Boost

• ECMS approvals received for multiple PCB projects ⚡

• Amber secured 100 acres land in YEIDA, U.P 🌍

• ILJIN Electronics raised ₹1,750 Cr from marquee investors 💰

• Amber raised ₹1,000 Cr via QIP 🚀

Balance sheet strengthened significantly for future expansion 🔥

🚄 Railway Sub-systems & Defense Division

FY26:

• Revenue ▲ 19% YoY – ₹535 Cr 📈

• EBITDA ▲ 8% YoY – ₹90 Cr ⚙️

Q4FY26:

• Revenue ▲ 22% YoY – ₹153 Cr 🚀

Key Highlights:

• ₹2,600 Cr order book visibility 💰

• Defense projects gaining strong traction ⚡

• Greenfield facility nearing commercialization 🏗️

• FY27 revenue growth guidance: 30-35% 📊

Railway & defense business continues scaling rapidly 🌍

🚄 Expanding Railway Product Portfolio

Products Include:

• HVAC systems 🚆

• Doors & Gangways ⚙️

• Couplers 🔋

• Pantographs ⚡

• Brakes 🚀

• Driving Gears 🌍

• Defense HVAC systems 🛡️

• Data Centre HVAC ❄️

Diversification continues improving wallet share and growth visibility 📈

🏦 Strong Balance Sheet Expansion

• Total Assets increased to ₹13,767 Cr 📊

• Equity strengthened to ₹5,802 Cr 💰

• Gross PPE increased to ₹3,182 Cr 🏭

• Inventory increased proactively amid supply chain disruptions 📦

• Working capital days increased to 29 ⚡

Expansion capex and acquisitions significantly strengthened business scale 🚀

💬 Strategic Focus Areas

• Deepening electronics manufacturing ecosystem ⚡

• Expanding RAC & component leadership ❄️

• Scaling PCB & semiconductor-linked manufacturing 🔋

• Strengthening railway & defense systems 🚄

• Increasing localization & value addition 🇮🇳

• Building diversified high-growth manufacturing platform 🌍

Amber is rapidly evolving into a multi-sector manufacturing powerhouse 🚀

⚡🏭🚄 With strong growth across consumer durables, electronics manufacturing, railway systems and strategic PCB expansion, Amber Enterprises India Limited continues positioning itself as one of India’s fastest-growing diversified manufacturing and EMS platforms 📈🌍

#AmberEnterprises #EMS #ElectronicsManufacturing #ConsumerDurables #Railways #Defense #PCB #MakeInIndia #Manufacturing #IndianStockMarket #AirConditioners #Semiconductor #IndustrialGrowth #Investing #FY26

3

283

May 16

Amber Enterprises India Ltd announced its audited financial results for the quarter & financial year ended 31st March 2026, reporting a robust performance. 🚀

𝗙𝗬26 𝗖𝗼𝗻𝘀𝗼𝗹𝗶𝗱𝗮𝘁𝗲𝗱 𝗙𝗶𝗻𝗮𝗻𝗰𝗶𝗮𝗹 𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀:

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹12,186 Cr, marking a substantial 22% YoY growth. This milestone surpasses the ₹12,000 Cr revenue mark. 📈

- 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗘𝗕𝗜𝗧𝗗𝗔: ₹970 Cr, a 22% increase compared to the previous year. 💪

- 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗣𝗔𝗧: ₹338 Cr, showing a 22% YoY growth (prior to exceptional items of ₹112 Cr).

𝗤4 𝗙𝗬26 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- 𝗥𝗲𝘃𝗲𝗻𝘂𝗲: ₹4,148 Cr, up 10% YoY.

- 𝗢𝗽𝗲𝗿𝗮𝘁𝗶𝗻𝗴 𝗘𝗕𝗜𝗧𝗗𝗔: ₹362 Cr, a 15% increase YoY.

- 𝗔𝗱𝗷𝘂𝘀𝘁𝗲𝗱 𝗣𝗔𝗧: ₹162 Cr, demonstrating a strong 27% YoY growth.

𝗞𝗲𝘆 𝗦𝘁𝗿𝗮𝘁𝗲𝗴𝗶𝗰 𝗗𝗲𝘃𝗲𝗹𝗼𝗽𝗺𝗲𝗻𝘁𝘀 & 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻𝗮𝗹 𝗣𝗲𝗿𝗳𝗼𝗿𝗺𝗮𝗻𝗰𝗲:

- 𝗠𝗗'𝘀 𝗖𝗼𝗺𝗺𝗲𝗻𝘁𝗮𝗿𝘆: Mr. Daljit Singh highlighted the remarkable financial performance & resilience of the business despite industry challenges.

- 𝗘𝗹𝗲𝗰𝘁𝗿𝗼𝗻𝗶𝗰𝘀 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻: Continued its rapid growth trajectory with a 49% YoY revenue increase in FY26, fueled by strategic acquisitions like Power-One (solar inverters, EV chargers), Unitronics (PLCs), & Shogini Technoarts (PCBs). 💡

- 𝗖𝗼𝗻𝘀𝘂𝗺𝗲𝗿 𝗗𝘂𝗿𝗮𝗯𝗹𝗲𝘀 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻: Achieved 14% revenue growth in FY26, navigating a challenging RAC season.

- 𝗥𝗮𝗶𝗹𝘄𝗮𝘆 𝗦𝘂𝗯-𝘀𝘆𝘀𝘁𝗲𝗺𝘀 & 𝗗𝗲𝗳𝗲𝗻𝘀𝗲 𝗗𝗶𝘃𝗶𝘀𝗶𝗼𝗻: Recorded 19% revenue growth in FY26, supported by a healthy order book of ₹2,600 Cr.

- 𝗘𝘅𝗽𝗮𝗻𝘀𝗶𝗼𝗻 & 𝗖𝗼𝗹𝗹𝗮𝗯𝗼𝗿𝗮𝘁𝗶𝗼𝗻𝘀:

▸ Secured approvals under the ECMS scheme for PCB applications. 🏭

▸ Acquired land for new manufacturing facilities in Uttar Pradesh (YEIDA). 📍

▸ Entered a strategic alliance with ILJIN Electronics & Sumitronics Corporation (Japan) for EMS solutions.

These strategic initiatives across divisions position Amber Enterprises for its next phase of growth. ✨

📊 AMBER ENTERPRISES INDIA LTD | 🏷️ Press Release / Media Release

🌐 Details: wegro.app/IY8fnP

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 wegro.app/go

2

548

May 16

Amber Enterprises India #HarResultKuchKehtaHai

#FANTASTIC

The real story is the explosion in the Electronics division, which saw revenue cross ₹1,015 Cr this quarter. This segment is no longer just a component supplier but a full-stack EMS provider, with EBITDA margins benefiting from the integration of Shogini and Unitronics. The pivot is working. While the core AC business grew at a modest 10%, the high-margin Electronics and Railway segments are now contributing nearly 30% of the total revenue mix. Capital work-in-progress has jumped to ₹500 Cr, up from ₹198 Cr last year. This is the smoking gun for future growth.

You do not invest that heavily in the Jewar and Hosur hubs unless you have firm visibility into the PCB and industrial automation pipeline for FY27. The Railway segment, though small at 4% of revenue, is delivering 19% margins and sits on a ₹2,600 Cr order book that provides visibility for the next eight quarters. Management has finally cleaned up the balance sheet by exiting the failed Italian joint venture, Shivaliks Mercantile, for a nominal ₹1.10 lakhs. This stops a multi-quarter cash drain that had previously clouded the earnings quality. For every ₹100 of profit, the company generated ₹106 in real operating cash this year, proving that the growth is not just an accounting mirage.

The ₹1,750 Cr equity infusion in the Iljin subsidiary further de-risks the massive capex plan. The primary risk remains the valuation, with the market pricing the company at 133 times earnings. However, the structural shift from seasonal assembly to high-tech engineering justifies a different multiple than the historical AC business. The next major trigger is the commissioning of the advanced PCB facilities in early FY27, which could further expand margins as the company moves up the value chain into HDI substrates.

Full breakdown → equisense.ai/app/deep-dive.h…

Public NSE/BSE filings · Not Investment Advice

#AMBER #Q4FY26 #StockMarket #Earnings

2

1

8

1,032

May 16

📊 AMBER ENTERPRISES INDIA LTD - 540902 | 🪒 Press Release / Media Release

Revenue for FY26 reached ₹12,186 Cr, reflecting a 22% YoY growth, with significant contributions from the electronics division and strategic acquisitions.

Key Highlights:

Financial Performance

- Q4 FY26 revenue of ₹4,148 Cr, growth of 10% over Q4 FY25.

- FY26 revenue of ₹12,186 Cr, growth of 22% YoY.

- Operating EBITDA for Q4 FY26 at ₹362 Cr, growth of 15% YoY.

- Adjusted PAT for FY26 at ₹338 Cr, growth of 22% YoY, prior to one-off impairments.

Divisional Growth

- Consumer Durables Division recorded a revenue growth of 14% in FY26.

- Electronics Division achieved a revenue growth of 49% in FY26.

- Railway Sub-systems & Defense Division reported a revenue growth of 19% in FY26, supported by a healthy order book visibility of ₹2,600 Cr.

Strategic Acquisitions

- Acquired Shogini Technoarts, Power-One, and Unitronics to enhance electronics capabilities.

- Secured approvals under the Electronics Component Manufacturing Scheme for multi-layer PCB applications.

Executive quote:

Mr. Daljit Singh, Managing Director, stated: “We are pleased to report FY26 has been a remarkable year both in terms of progression and performance of the company.”

Overall, the company is well-positioned for continued growth through strategic initiatives and acquisitions.

💰 CMP: ₹8,471.70 ( 2.24%)

🏢 MCap: ₹29,837 Cr

🌐Details: tinyurl.com/2xscs753

⚡️Instant stock alerts on WhatsApp - Try FREE 👉 speedystox.com

2

230

May 15

Amber Enterprises India Ltd Q4FY26 Results:-

#Q4Results #Q4FY26 #Stockmarket #Nifty #Amber

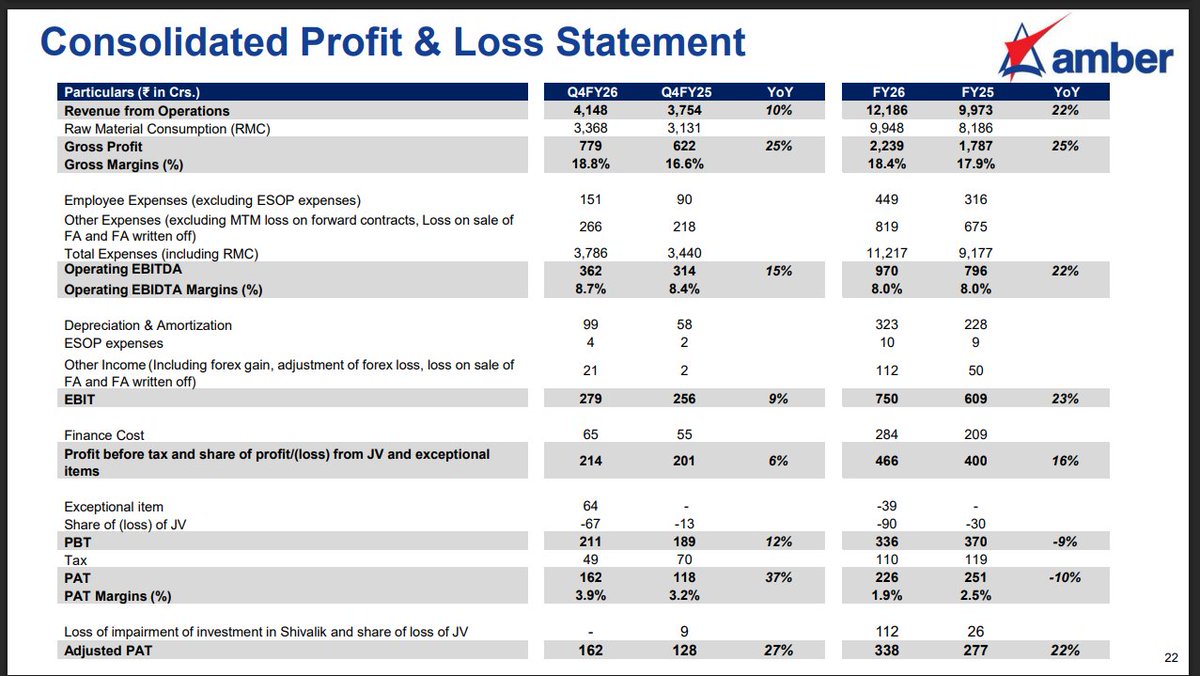

➤ Revenue ₹4,148 Cr ( 10% YoY)

➤ Gross Profit ₹779 Cr ( 25% YoY)

Gross Margin 18.8% ( 220 bps YoY)

➤ Operating EBITDA ₹362 Cr ( 15% YoY)

Operating EBITDA Margin 8.7% ( 30 bps YoY)

➤ EBIT ₹279 Cr ( 9% YoY)

➤ PBT ₹211 Cr ( 12% YoY)

➤ PAT ₹162 Cr ( 37% YoY)

➤ Adjusted PAT ₹162 Cr ( 27% YoY)

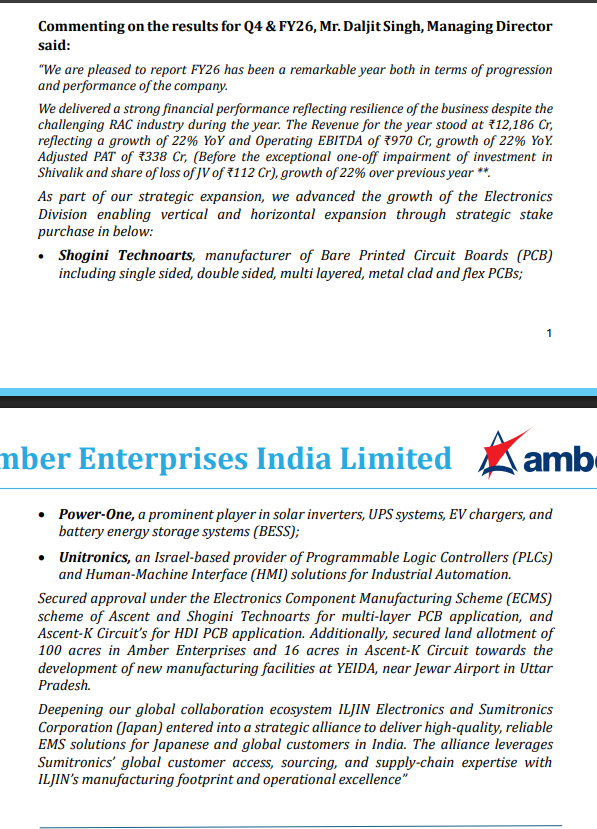

➤ Management Commentary:-

✓ FY26 as a remarkable year in terms of both operational progress and financial performance despite challenging RAC industry conditions

✓ FY26 performance highlights:

✓ Revenue ₹12,186 Cr ( 22% YoY)

✓ Operating EBITDA ₹970 Cr ( 22% YoY)

✓ Adjusted PAT ₹338 Cr ( 22% YoY) excluding impairment and JV losses

✓ Amber continued strategic expansion of its Electronics Division through stake acquisitions in:

✓ Shogini Technarts:

Manufacturer of bare PCBs including single-sided, double-sided, multilayer, metal-clad, and flex PCBs

✓ Power-One:

Player in solar inverters, UPS systems, EV chargers, and battery energy storage systems (BESS)

✓ Unitronics:

Israel-based provider of PLC and HMI solutions for industrial automation

✓ Secured approvals under Electronics Component Manufacturing Scheme (ECMS) for:

✓ Ascent Circuits

✓ Shogini Technarts for multilayer PCB applications

✓ Ascent-K Circuit for HDI PCB applications

✓ Land allotments received:

100 acres for Amber Enterprises

16 acres for Ascent-K Circuit

near Jewar Airport, Uttar Pradesh for new manufacturing facilities.

✓ ILJIN Electronics and Sumitronics Corporation (Japan) entered strategic alliance with Amber to deliver high-quality EMS solutions for Japanese and global customers in India

✓ Partnership expected to leverage:

Sumitronics’ customer access and sourcing network

ILJIN’s manufacturing expertise and operational capabilities.

1

1

25

2,486

Apr 28

Redfish-inside PLCs — driven by Unitronics — are reshaping cooling, control and DCIM integration. Learn more in the feature by @unitronics.

ow.ly/MaIo50YLgIR

5

1

2

97

Apr 13

گروههای هکری وابسته به ایران از مارس ۲۰۲۶ بهطور فزایندهای زیرساختهای حیاتی آمریکا را هدف قرار دادهاند و در این حملات سایبری، دستگاههای کنترل منطقی برنامهپذیر (PLC) ساخت شرکت Rockwell Automation/Allen-Bradley را نشانه رفتهاند. بر اساس هشدار مشترک چندین نهاد فدرال آمریکا، این حملات منجر به اختلال عملیاتی و خسارات مالی شده و شامل استخراج فایلهای پروژه و دستکاری دادهها در سامانههای نمایش HMI و SCADA بوده است.

شرکت امنیت سایبری Censys گزارش داده که از میان بیش از ۵٬۲۱۹ سامانه کنترل صنعتی (ICS) در معرض اینترنت در سراسر جهان، ۷۴.۶ درصد آنها (۳٬۸۹۱ دستگاه) در خاک آمریکا قرار دارند که بخش قابلتوجهی از آنها از طریق مودمهای سلولی به اینترنت متصلاند.

این کمپین در ادامه حملات مشابه پیشین است؛ از جمله حملات گروه CyberAv3ngers وابسته به سپاه پاسداران که بین نوامبر ۲۰۲۳ و ژانویه ۲۰۲۴ دستکم ۷۵ دستگاه PLC ساخت Unitronics را در شبکههای آب و فاضلاب آمریکا به خطر انداخت. همچنین گروه هکتیویست Handala وابسته به وزارت اطلاعات ایران، حدود ۸۰٬۰۰۰ دستگاه از جمله تلفنهای همراه کارکنان و رایانههای شخصی شرکت پزشکی Stryker را پاک کرد. مقامات آمریکایی به مدیران شبکه توصیه کردهاند که PLCها را پشت فایروال قرار دهند یا از اینترنت جدا کنند، احراز هویت چندعاملی (MFA) را اجرا نمایند و سرویسهای بلااستفاده را غیرفعال سازند.

3

562

UnitronicsのHMI PLC一体化のデバイスとPhoenix Contact PLC Interface Gateway とEthernetIPで遊んでいます

UnitronicsのEIP Configuratorすごく設定しやすい

#Unitronics #EthernetIP #PhoenixContact #PLC

9

975

Apr 11

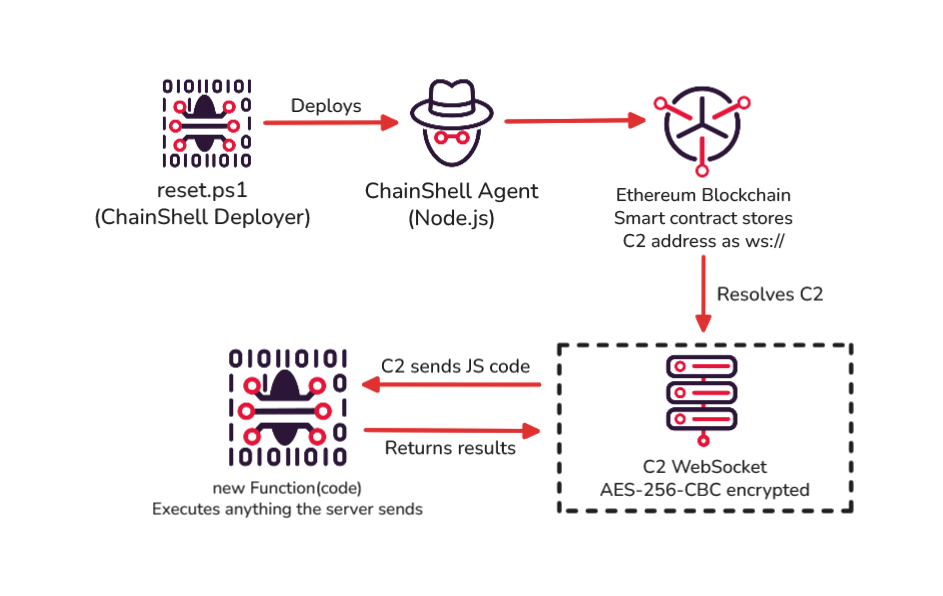

MuddyWater and TAG-150 CastleRAT have been tied to the ChainShell malware which has been used to hit SCADA, and HMI systems. With at least two CastleRat builds tied to MuddyWater at this time. Initially attributed to Iran by finding the C2 server (157.20.182.49) known to be used by MuddyWater, comments containing Farsi code, and Israeli IP ranges for targeting.

Alongside this, two native PE payloads (“Build 120” and “Build 13”) were hidden inside steganographic JPEG images, and share hardcoded MaaS (Malware-as-a-Service) template identifiers. With it also containing Russian developer strings, (“вернул”, “провайдер”) and a CIS locale exclusion (exits on Russian/Ukrainian systems), supporting TAG-150 attribution.

Central to the operations is a PowerShell deployer ("reset.ps1") that deploys a previously undocumented JavaScript-based malware called ChainShell. ChainShell is a thin execution shell, the server sends JavaScript via `new Function()` and the agent executes and returns results via `serverSend()`. With all capabilities pushed server-side, the agent itself has no built-in stealer, keylogger, or shell.

After ChainShell activates, it contacts a smart contract on the Ethereum blockchain to retrieve a C2 address and uses it to fetch next-stage JavaScript code for execution on compromised hosts. Upon obtaining initial access, the threat actors established command-and-control by deploying Dropbear, a Secure Shell (SSH) software, on victim endpoints to enable remote access through port 22 and facilitate the extraction of the device's project file and data manipulation on HMI and SCADA displays.

This is not the first time Iranian threat actors have targeted OT networks and PLCs. In late 2023, Cyber Av3ngers (aka Hydro Kitten, Shahid Kaveh Group, and UNC5691) was linked to the active exploitation of Unitronics PLCs.

#Malware #CyberSecurity #CybersecurityNews

jumpsec.com/guides/chainshel…

1

25

109

6,994

Apr 11

Aditya Raj Kaul looked at the sky over Islamabad and saw five Pakistani F-16s flying tight escort around JD Vance’s plane. He posted the image and declared Pakistan unsafe. That was the story he chose to tell.

He should have felt something sharper. Any human being who still believes in humanity should have turned away from those fighter jets and remembered the administration that stood silent while one hundred sixty eight children died in the Muneeb School massacre. That slaughter carried the stench of calculated violence yet the Indian journalist found no words for it. Instead he fixed his gaze on the escort and called it proof of danger. The hypocrisy sat there naked under the same sun that once lit the ruins of that school.

The facts of his own country tell a different tale. After October 7 2023 Israel suspended the work permits of nearly eighty thousand Palestinian construction workers from the West Bank and Gaza. The move emptied building sites across the country and created a labor vacuum that Israeli contractors refused to fill with local hands. They turned instead to India. By July 2025 more than twenty thousand Indian workers had landed in Tel Aviv and more contracts promised fifty thousand more in the coming years. Those men now pour concrete and lay rebar where Palestinians once stood. The exchange was not subtle. It was replacement dressed up as necessity.

The money followed the labor. Indian capital poured into Israel with the quiet efficiency of men who know exactly where profit hides. Adani Ports and SEZ took control of Haifa Port in a deal worth one point one eight billion dollars and the cranes now move cargo under Indian management. Sun Pharma swallowed Taro Pharmaceutical Industries whole and the pills that once bore an Israeli label now flow through Indian balance sheets. Samvardhana Motherson dropped fifteen million dollars into REE Automotive to secure electric vehicle platforms. Amber Enterprises paid forty seven million for a stake in Unitronics and its automation systems. Indian Oil sank another twenty five million into Phinergy for aluminum air batteries. Tata Consultancy Services runs digital projects from Tel Aviv offices while Tata Industries quietly feeds five million dollars into university technology funds. Reliance Industries and Jio Financial Services circle Israeli startups the way vultures circle fresh kills. Infosys Tech Mahindra Wipro L&T State Bank of India and Ola Electric all maintain footholds and all of them feed on the same ecosystem that rose after the Palestinian workers were sent home.

India depends on Middle Eastern Muslim oil and on the Muslim-controlled waterways that carry it yet Indian investors and Indian workers have begun to pocket the dividends of that displacement. The faith of Indian journalists Indian politicians and Indian capitalists is simple. It is money. They see no contradiction in condemning Pakistani security measures while their own companies profit from the very conflict that emptied Palestinian job sites. They watch the region burn and calculate the return on investment.

That is the longer sentence no one wants to read. India is not a bystander. India is not neutral. India has become part of the machinery. The same hands that type outraged tweets about Pakistani fighter jets are attached to bodies whose wallets grow heavier every time another Palestinian worker is told to leave and another Indian takes his place on an Israeli scaffold. The world should see it plainly. The escort in Islamabad was theater. The real transaction happened in the labor camps and boardrooms where Indian capital replaced Palestinian lives and called it business as usual.

4

14

776

Apr 11

Aditya Raj Kaul looked at the sky over Islamabad and saw five Pakistani F-16s flying tight escort around JD Vance’s plane. He posted the image and declared Pakistan unsafe. That was the story he chose to tell.

He should have felt something sharper. Any human being who still believes in humanity should have turned away from those fighter jets and remembered the administration that stood silent while one hundred sixty eight children died in the Muneeb School massacre. That slaughter carried the stench of calculated violence yet the Indian journalist found no words for it. Instead he fixed his gaze on the escort and called it proof of danger. The hypocrisy sat there naked under the same sun that once lit the ruins of that school.

The facts of his own country tell a different tale. After October 7 2023 Israel suspended the work permits of nearly eighty thousand Palestinian construction workers from the West Bank and Gaza. The move emptied building sites across the country and created a labor vacuum that Israeli contractors refused to fill with local hands. They turned instead to India. By July 2025 more than twenty thousand Indian workers had landed in Tel Aviv and more contracts promised fifty thousand more in the coming years. Those men now pour concrete and lay rebar where Palestinians once stood. The exchange was not subtle. It was replacement dressed up as necessity.

The money followed the labor. Indian capital poured into Israel with the quiet efficiency of men who know exactly where profit hides. Adani Ports and SEZ took control of Haifa Port in a deal worth one point one eight billion dollars and the cranes now move cargo under Indian management. Sun Pharma swallowed Taro Pharmaceutical Industries whole and the pills that once bore an Israeli label now flow through Indian balance sheets. Samvardhana Motherson dropped fifteen million dollars into REE Automotive to secure electric vehicle platforms. Amber Enterprises paid forty seven million for a stake in Unitronics and its automation systems. Indian Oil sank another twenty five million into Phinergy for aluminum air batteries. Tata Consultancy Services runs digital projects from Tel Aviv offices while Tata Industries quietly feeds five million dollars into university technology funds. Reliance Industries and Jio Financial Services circle Israeli startups the way vultures circle fresh kills. Infosys Tech Mahindra Wipro L&T State Bank of India and Ola Electric all maintain footholds and all of them feed on the same ecosystem that rose after the Palestinian workers were sent home.

India depends on Middle Eastern Muslim oil and on the Muslim-controlled waterways that carry it yet Indian investors and Indian workers have begun to pocket the dividends of that displacement. The faith of Indian journalists Indian politicians and Indian capitalists is simple. It is money. They see no contradiction in condemning Pakistani security measures while their own companies profit from the very conflict that emptied Palestinian job sites. They watch the region burn and calculate the return on investment.

That is the longer sentence no one wants to read. India is not a bystander. India is not neutral. India has become part of the machinery. The same hands that type outraged tweets about Pakistani fighter jets are attached to bodies whose wallets grow heavier every time another Palestinian worker is told to leave and another Indian takes his place on an Israeli scaffold. The world should see it plainly. The escort in Islamabad was theater. The real transaction happened in the labor camps and boardrooms where Indian capital replaced Palestinian lives and called it business as usual.

Apr 11

How dangerous is it to be in Pakistan for an American leader?

American delegation aircraft to the Islamabad Talks was being escorted by five Pakistan Air Force F-16s. Not just a symbolic respect gesture. Reports emerge Americans were hesitant with security concerns in Pakistan.

13

78

474

92,972

#Stocks To Watch

Tilaknagar Industries: The company reports that sales of its Mansion House brand surpassed 10 million cases in FY26, up from 8.7 million cases in FY25.

Cochin Shipyard: The company reports that the Ministry of Corporate Affairs (MCA) has launched the second 100-day special outreach initiative titled 'Saksham Niveshak', running from April 1 to July 9.

Amber Enterprises: The company reports that its arm, IL JIN Electronics, has acquired an additional 4.85% stake in Unitronics, bringing its total shareholding to 49.66%.

Bajaj Hindusthan Sugar: The company has allotted 1.6 crore shares worth Rs. 8.5 crore on a preferential basis and separately allotted another 44 crore shares aggregating Rs. 44.57 crore.

MM Forgings: The company reports that CFO R Venkatakrishnan has resigned, and R Raghunathan has been appointed as the new CFO.

Mahamaya Steel Industries: The company reports total sales of 13,982.8 MT for the month of March in its latest business update.

Balaji Telefilms: The company reports that Dhaval Sheth has resigned from his position as Deputy CFO due to personal reasons.

NTPC: The company reports that its Jharkhand coal mine has been transferred to NTPC Mining (NML) and has declared the commencement of commercial operations at the site. Separately, the group's total installed capacity now stands at 89,108 MW, with commercial capacity at 88,028 MW.

Piramal Pharma: The company's arm, Piramal Critical Care, has completed the acquisition of Kenalog and associated brands from Bristol-Myers Squibb.

Fertilizers and Chemicals

Travancore (FACT): The company's FY26 business update highlights NP 20:20:0:13 production at 8.3 LMT (sales at 8.07 LMT) and Ammonium Sulphate production at 2.83 LMT (sales at 2.99 LMT).

IOL Chemicals and Pharmaceuticals: The company reports that the Registrar of Companies (RoC) has struck off its arm, IOL Life Sciences.

Karnataka Bank: The company's March 31 business update shows total deposits up 3.8% YoY to Rs. 1.1 lakh crore, gross advances up 6.9% to Rs. 83,337 crore, and CASA up 10% to Rs. 36,621 crore.

Pace Digitek: The company has secured a Rs. 495 crore EPC order from NTPC for the implementation of a 200 MW Battery Energy Storage System (BESS) in Bihar.

Eicher Motors: The company reports total Royal Enfield sales of 1.12 lakh units in March, meeting estimates, with motorcycle sales up 11% YoY and exports up 8% YoY.

NMDC: The company's March business update shows total production surged 51% YoY to 5.35 MT, while total sales grew 40% YoY to 5.90 MT.

Puravankara: The company has received a tax demand of Rs. 52 crore from the Bengaluru authorities.

Indian Oil Corp: The company's FY26 business update reports refinery crude throughput at 75.4 MMT, pipeline throughput at 105.3 MMT, petroleum product sales up 4% YoY to 104.4 MMT, petrochemical sales at 3.22 MMT, and the commissioning of 909 new retail outlets.

Hero MotoCorp: The company reports total 2-wheeler sales grew 8.8% YoY to 5.98 lakh units in March, driven by domestic sales growth and a 53% surge in scooter sales. Separately, it acquired 2.7 lakh shares in Euler Motors for Rs. 210 crore, maintaining a 36.67% stake.

SJVN: The company reports it generated 1,330 crore units of energy during FY26.

Bansal Wire Industries: The company reports total sales volume grew 20% YoY to 1.2 lakh MT in its Q4 business update.

Lupin: The company reports its arm has acquired a 100% stake in VISUfarma B.V., and separately, its arm Nanomi will buy a 43.3% stake in its Philippines arm for $39.6 million.

Tasty Bite Eatables: The company reports that Pradeep Poddar has retired from his position as Chairman and Independent Director.

Wipro: The company announces the creation of an AI-Native Business & Platforms unit for Core Services, with Nagendra Bandaru appointed as CEO. Suzanne Dann has stepped down as CEO for Americas-2. The company also completed the merger of its step-down arms Capco RISC and Cardinal US, while Cardinal US Holdings transferred its stake in Capco Consulting to The Capital Markets.

ABB India: The company has received a Rs. 15 crore penalty and redemption fine from Bengaluru authorities.

Yatra Online: The company reports that a Rs. 151 crore duty demand has been dropped by the Customs, Excise & Service Tax Appellate Tribunal (CESTAT) in Chandigarh.

Swaraj Engines: The company will consider its Q4 results and dividend on April 13.

Man Infraconstruction: The company has reduced its partnership interest in Man Aaradhya to 37.5% and increased its interest in Man Vastucon to 13%.

Adani Enterprises: The company reports the effective merger of Adani Green Technology and Adani Emerging Businesses into the company as of April 1, and the amalgamation of Adani Tradecom with Adani New Industries, setting April 14 as the record date for share allotment.

TVS Motor: The company reports total sales grew 25% YoY to 5.2 lakh units in March, with strong growth across 2-wheelers, 3-wheelers (up 46%), and EV sales (up 44%).

Choice International: The company has entered into a pact to acquire a 100% stake in Optimo Investment Adviser.

Glenmark Pharma: The company has received a Rs. 32 crore tax demand, including penalties, from the Mumbai authorities.

Bosch: The company's board will meet on April 8 to consider a preference shares issue.

Aavas Financiers: The company reports AUM grew 15% YoY to Rs. 23,500 crore and disbursements grew 16% YoY to Rs. 2,350 crore in its Q4 update, adding 38 branches in FY26.

HCC (Hindustan Construction Company): The company has transferred awards worth Rs. 1,979 crore to HCC Contract Solutions.

Prime Focus: The company reports Brahma India sold its PFT US stake to DNEG for $21 million, and DNEG will sell its Brahma India stake to Brahma AI for $90 million.

Sambhv Steel Tubes: The company will invest Rs. 7.5 crore to acquire a 15% stake in Vajra Alloys Private.

Smartworks Coworking Spaces: The company will invest Rs. 17 crore for capacity addition in Hyderabad.

Emami: The company has acquired an additional 36.7% stake in Axiom Ayurveda Pvt and plans to buy the remaining 36.7% stake by June.

South Indian Bank: The company's March business update shows gross advances up 15.7% YoY to Rs. 1.01 lakh crore, total deposits up 14.7% to Rs. 1.23 lakh crore, and CASA up 17.5% to Rs. 39,621 crore.

ICICI Prudential: The company has completed the transfer of investment management rights for certain AIFs of ICICI Venture Funds.

Prestige Estates Projects: The company has secured a 17.2-acre land parcel in Gurugram with a Gross Development Value (GDV) potential of Rs. 4,200 crore.

Varun Beverages: The company has fixed April 8 as the record date for its final dividend.

Nestle India: The company will invest Rs. 90 crore to add a new Maggi noodle production line at its Gujarat unit.

CG Power and Industrial Solutions: The company reports its arm CGS has sold Crompton Prima Switchgear Indonesia, which ceases to be a step-down subsidiary.

DCM Shriram: The company has started a 17,000 TPA capacity expansion at its Gujarat Epichlorohydrin plant, taking total capacity to 52,000 TPA.

Marico: The company's board has approved the voluntary liquidation of Zed Lifestyle.

Adani Ports: The company reports that the NCLT Ahmedabad has approved its merger with Adani Harbour.

Alembic Pharma: The company's board has re-appointed Pranav Amin as MD for five years. Separately, Chirayu Amin has resigned as CEO to take charge as Executive Chairman.

Mobavenue AI Tech: The company reports that Tejas Rathod has resigned from his position as CFO.

KRN Heat Exchanger: The company's arm, KRN HVAC, will purchase land in Rajasthan for Rs. 9 crore.

Ola Electric: The company reports daily orders exceeded 1,000 units in the last week of March, with registrations surging 150% YoY to 10,117 units.

Sanathan Textiles: The company's arm, Sanathan Polycot, has commissioned a polymerisation line and completed the Phase I ramp-up at its Punjab unit.

Maruti Suzuki: The company's March production volume grew 19% YoY to 2.32 lakh units, driven by passenger vehicle production.

Shriram Finance: The company reports its tax demand has been significantly reduced from Rs. 102 crore to Rs. 5 crore.

Indegene: The company has signed a pact to buy trade and business assets from Trilogy Writing and Consulting for GBP 1.9 lakh.

Power Grid: The company has promoted Pradeep Kumar to the post of Executive Director.

V2 Retail: The company reports Q4 revenue grew 59% YoY to Rs. 798 crore, achieving a 7.74% Same Store Sales Growth, and ended FY26 with 325 stores.

Texmaco Rail: The company has secured a Rs. 41 crore order from Sushila Transport Pvt.

Vedanta: The company has received a Rs. 33 crore demand from the Delhi Environment Body.

AGI Infra: The company has received a license from GMADA for a 10.26-acre land parcel.

Emcure Pharma: The company's arm, Mantra Pharma, has acquired Canada-based Cutimed for CAD $5.05 million.

Shree Cement: The company has received a Rs. 149 crore tax demand from the Rajasthan authorities.

1

5

7

2,132