Transform your marketing 🌟

Educate instead of selling! Trust creates conversations.

#MarketingStrategy #BuildTrust #ValueFirst #LYTaxAdvisors #PervasiveMarketing #Business #Taxes #Texas #Houston

lytaxadvisors.com/

4

Triba retweeted

You’re more than a transaction.

You’re the reason we do what we do. 💚

At nuMoni, value always comes first.

#ValueFirst #nuMoni #ExtraValue

2

5

15

The 'Unsubscribe' Test: 📧

If you looked at your own social feed, would you unsubscribe?

If the answer is 'Yes,' you're not providing enough value.

Shift from 'Look at me' to 'How I can help you.'

#ValueFirst #RealtorMarketing

connectiko.io

1

4

Jun 8

The hard truth about content creation? Nobody cares what you like.

Save this for the next time you're stuck on what to post!

#ContentCreatorTips #SocialMediaStrategy #ContentMarketing #GrowYourAudience #CreatorEconomy #InstagramTips #ValueFirst #CreativeEntrepreneur

5

Jun 8

Start a speech as an action movie! #hook #grabattention #valuefirst #pub... youtube.com/shorts/FVAOAKUDb… via @YouTube

7

Jun 7

CORE-ZENITH

Your ERC-721 domain is a living crypto-walletReal on-chain tests on OpenSea confirmedNest lands heroes and 9900 GAC insideYour NFT owns assets and accumulates valueFirst 100 free slots under total controlSecure your Web3 empire foundation now#GenesisCoreWars #ERC6551

44

In a world where everyone is busy but almost no one is building, it’s easy to get caught up in just reacting. Real progress comes from creating with intention. 🚀

Focus beats speed every time. When we shift our energy from busy-work to building real authority, we set ourselves apart. At Webriseup, we believe in growth through strategic action.

#MarketingStrategy #BrandAwareness #Webriseup #DigitalGrowth #ValueFirst #BusinessTips

14

61

May 1

@heyaura

isn’t about visibility — it’s about accountability. Before posting, ask yourself: • Does this add clarity or just noise? • Am I sharing insight or chasing impressions?

@heyaura

. #QualityContent #BuildInPublic #Web3Community #ValueFirst

2

39

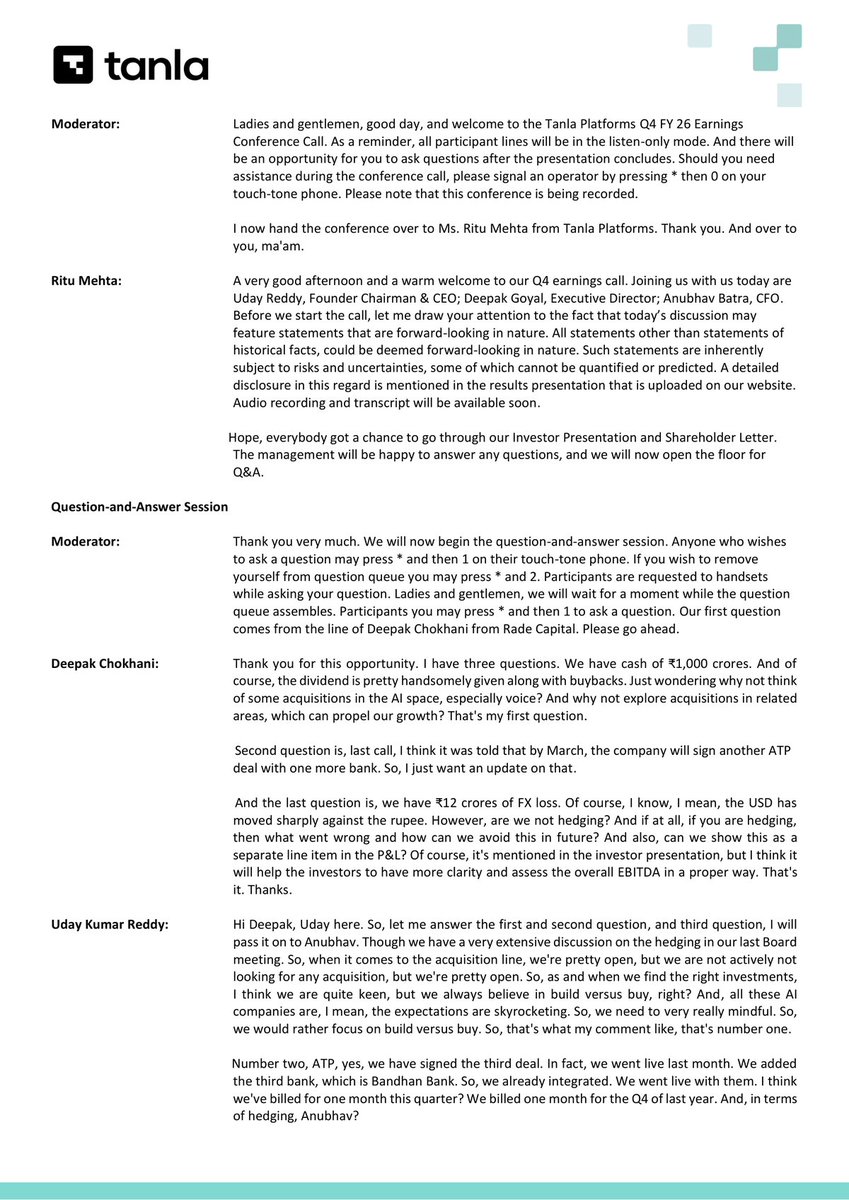

📈 Tanla Platforms Expands with Indosat Deal for 100M Subscribers, Eyes AI Launch in Q1 FY27 | MCap 6,219.75 Cr

• Signed deal with Indosat for 100 million subscribers

• New AI platform launch planned for Q1 FY27

• International expansion mentioned as growth driver

• Expects accelerated growth in Digital Platforms

• Targets resolution of ValueFirst UAE acquisition in Q1 FY27

• Annual capex expected to remain ₹100-150 crores

• Digital Platform segment revenue reached ₹395 crores in FY26

• ValueFirst UAE business generating ₹150-170 crores revenue at 22% gross margin

• OTT channels (WhatsApp, RCS) contributed 31-32% of revenue

• Digital Platform segment achieved 98.2% gross margin

• FX loss of ₹12 crores due to USD-INR fluctuations

Disc: Information provided in this tweet can be inaccurate, verify through the source in reply before making any investment decision.

Preview 👇 (First 4 out of 13 pages)

1

2

580

Apr 30

@heyaura

isn’t about visibility — it’s about accountability. Before posting, ask yourself: • Does this add clarity or just noise? • Am I sharing insight or chasing impressions?

@heyaura

. #QualityContent #BuildInPublic #Web3Community #ValueFirst

1

5

61

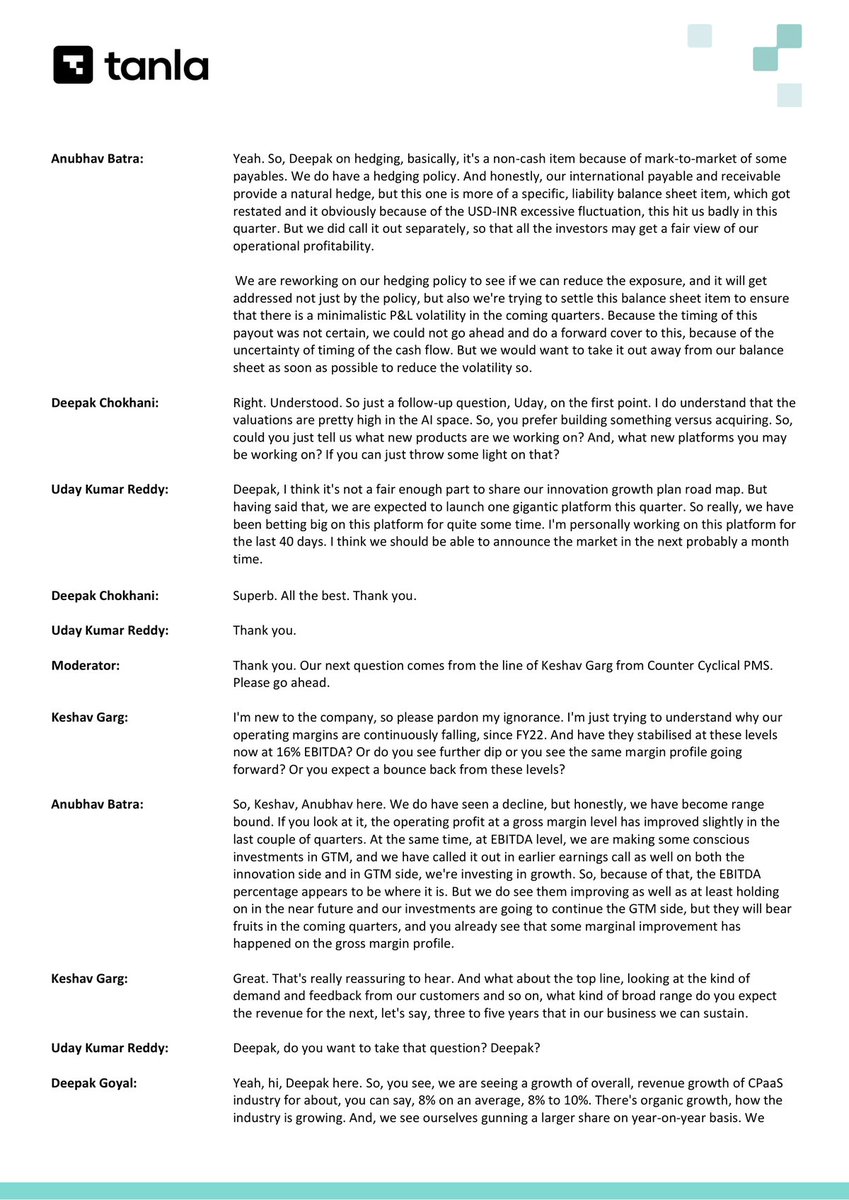

Tanla concall: Sharad kohli asked whether valuefirst uae business went from 200 cr to 300 or 400 cr now. N whether margins increased from single digits to double digits on that.

2

146

Apr 24

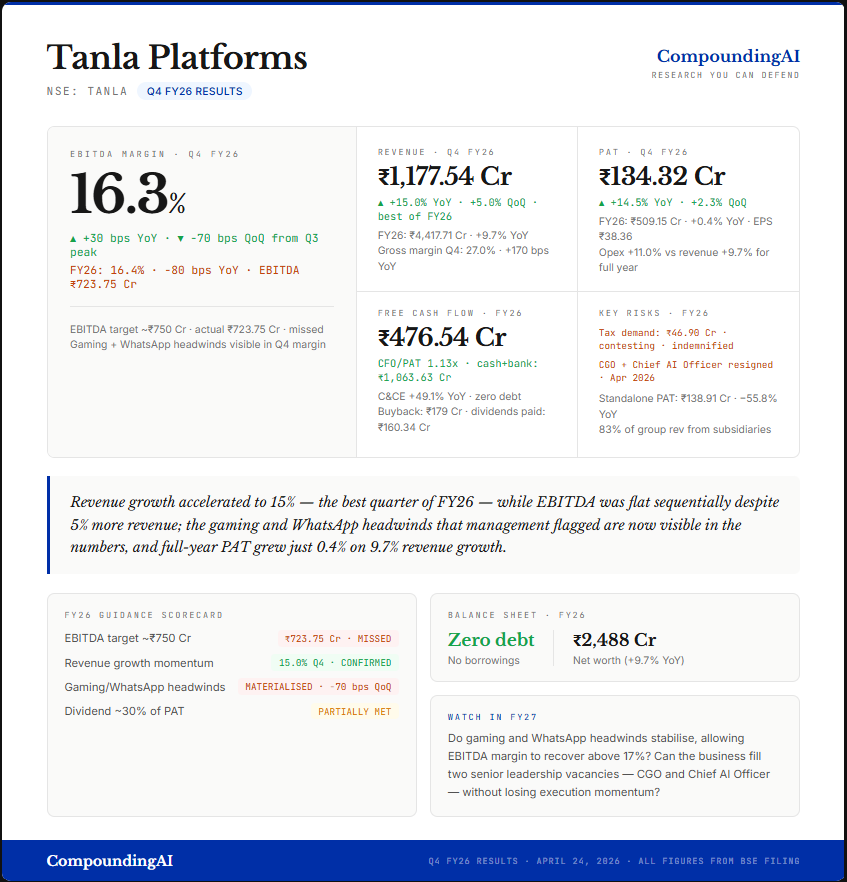

Tanla Platforms - Q4 FY26 Result Analysis

-Revenue: ₹1,177.54 Cr. Up 15.0% YoY.

-EBITDA margin: 16.3%. Up 30 bps YoY, down 70 bps QoQ.

-PAT: ₹134.32 Cr. Up 14.5% YoY.

Q4 was the strongest revenue quarter of FY26. And yet EBITDA was flat sequentially despite 5% more revenue. That gap is the story.

The full year tells it plainly. Revenue grew 9.7%. Expenses grew 11.0%. PAT grew 0.4%. The business grew - the cost structure grew faster.

Three lines drove that cost inflation. Employee costs were up 24.1% YoY, partly from RSU amortisation on the ValueFirst acquisition. Depreciation was up 25.0% YoY from capitalised intangibles. Other expenses were up 36.6% YoY. The one bright spot: cost of services grew 8.9% - slower than revenue, so gross margin expanded 50 bps for the full year to 26.6%. That improvement was entirely swallowed by the lines above it.

The EBITDA target for FY26 was ~₹750 Cr. Actual: ₹723.75 Cr. Management had flagged two specific headwinds - gaming sector revenue softness and removal of Meta WhatsApp incentives. Both showed up in Q4: gross margin fell 60 bps QoQ, EBITDA margin fell 70 bps QoQ from Q3's peak of 17.0%.

Cash flow is the clear positive. FCF for FY26 was ₹476.54 Cr. CFO/PAT: 1.13x. Cash and bank balances on the balance sheet: ₹1,063.63 Cr. Zero debt. The company returned ₹179 Cr via buyback and ₹160 Cr in dividends during the year. The balance sheet is in good shape even if the P&L isn't.

Two things to watch heading into FY27. First, the Chief Growth Officer and Chief AI Officer both resigned in April 2026 - key roles for a company trying to pivot toward AI-driven platform services. Second, a ₹46.90 Cr tax demand on the Karix acquisition is being contested; the seller bears this under the acquisition agreement, so financial impact is limited, but it adds noise.

Note : This is not an investment advise.

1

4

666

Apr 18

You don’t need more followers.

You need more VALUE.

A small audience that trusts you will always pay you more than a large audience that ignores you.

Stop chasing numbers.

Start building trust.

That’s where the money is.

#web3 #PersonalBrand #ValueFirst

1

2

4

41

Stop chasing money and start creating value. When your business solves real problems, customers will come and income will follow.

Follow TIO for more: instagram.com/theisraelogund…

#TIOBOI #ValueFirst #BusinessGrowth #smallbusiness

2

8

Apr 9

Stop chasing approval. Start creating value. That’s how real influence begins. #GrowthMindset #ValueFirst

10

10

20

486

Apr 7

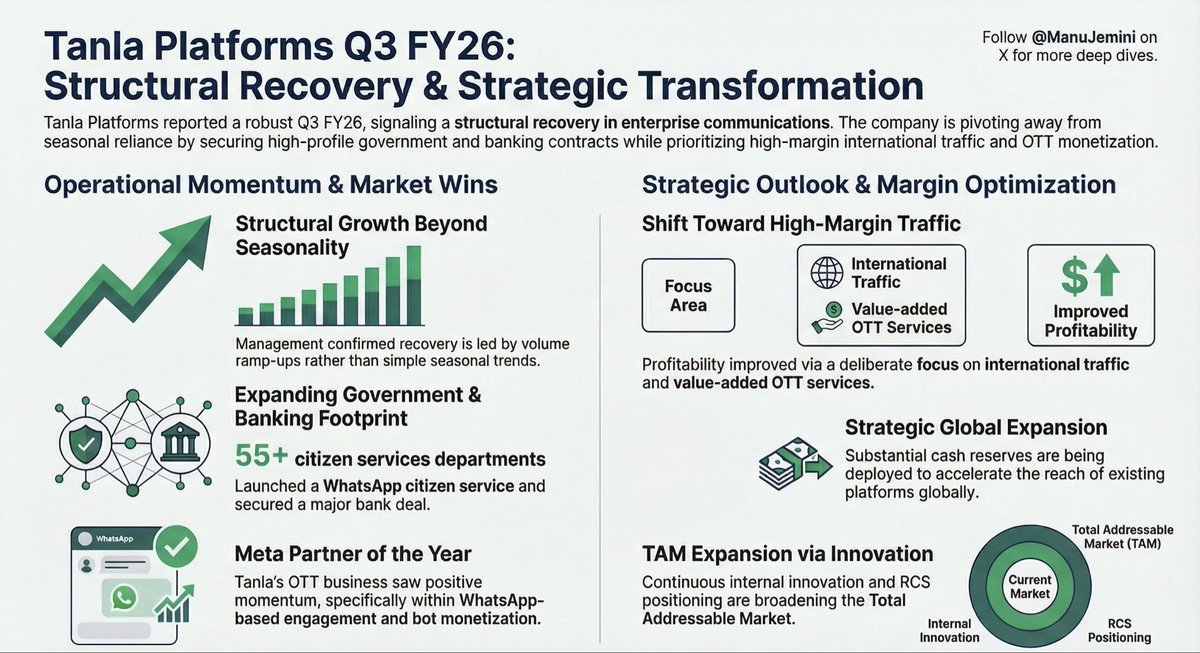

📈 Earnings Deep Dive,

Tanla Platforms Ltd

#Q3FY26 #Nifty #TANLA

Tanla Platforms Drives Growth with New Customer Wins & Strategic Mix Shift 💼✨

A deep dive into their Q3 FY26 Concall ⬇️

Tanla Platforms reported a robust Q3 FY26, highlighting a structural and mix-led recovery in enterprise communications beyond mere seasonality.

The company noted significant growth in SMS volumes driven by net new customer acquisitions and successful ramp-ups.

Management emphasized a strategic shift towards higher-margin traffic and monetizing value-added services, particularly within its burgeoning OTT business.

While competitive pricing pressure persists, Tanla maintains stability through procurement discipline and route optimization.

The company is leveraging its cash balance to accelerate global growth of existing platforms and expand its addressable market through geographic reach and continuous innovation.

🔹 Outlook & Guidance 🎯💡

- Management characterizes Q3 FY26 recovery as structural and mix-led, not just seasonal.

- Persistent competitive pricing pressure is acknowledged, though near-term stability is noted.

- Long-term growth will be fueled by geographic expansion and continuous internal innovation to broaden TAM.

- ValueFirst International acquisition approvals are still pending, with ongoing regulator questions.

- The company did not provide formal revenue or margin guidance for future periods.

🔹 Q3 Performance Highlights 📊💰

- SMS volumes saw growth driven by net new customer wins and ramp-ups across various sectors.

- A deliberate mix shift towards more profitable, higher-margin international traffic contributed to improved profitability.

- OTT (WhatsApp) business demonstrated positive momentum, with Meta recognizing Tanla as "partner of the year."

- One new ATP bank deal in India was secured, expected to go live and begin billing by February.

- A significant WhatsApp-based citizen engagement service launched across 55 Tamil Nadu government departments.

🔹 Management Tone & Strategy 🧭🛡️

- Strategy focuses on monetizing value-added services like bots for additional OTT revenue and bottom line.

- Meta's pricing volatility is managed by emphasizing customer ROI and positioning RCS as a cheaper alternative.

- New customer additions have a 3-4 quarter ramp-up cycle before fully contributing to revenue.

- The substantial cash balance is earmarked for accelerating global growth of existing platforms.

- Management downplayed the risk of passkeys impacting OTP volumes, citing growth in other SMS notifications.

- Tanla asserts strong defensibility and market leadership against international CPaaS players in India.

2

412

Apr 4

Want reach on X?

Focus on replies first, posts second. Build conversations, not noise.

#ValueFirst #XGrowth #MonetizeDaily

5

12

164

Apr 2

Networking is not just about asking for opportunities.

It’s about building genuine connections.

Check up on people, add value, share ideas.

Don’t always show up when you need something.

Build relationships that last.

#Networking #ValueFirst #Connections

5

12

99