Jun 12

That is correct!

$ABVX from VectivBio AG (acquired by Ironwood Pharmaceuticals in June 2023)

Vectiv from Arena Pharmaceuticals (acquired by $PFE in 2022)

2001 - 2017 worked at Actillion (acquired by $JNJ in 2017)

PM is a stand up guy. I mean it, not a lot of IR folks you would say that about. I can't prove it, but honestly feel like a lot of the disconnect is coming from the Paris side.

1

5

681

20 Dec 2025

Hikâyeyi en baştan, sade bir dille anlatalım.

Ironwood Pharmaceuticals $IRWD uzun yıllardır sindirim sistemi (GI) hastalıklarına odaklanan bir biyoteknoloji şirketi. Şirketin bugün ayakta durmasını sağlayan ana ürün LINZESS adlı, onaylı ve hâlihazırda ciddi nakit üreten bir ilaç. Yani Ironwood “hayal satan” bir şirket değil; gerçek geliri olan, FDA ile defalarca çalışmış bir yapı.

LINZESS I zaten ayrı tutuyorum. O taraf para basmaya devam edecek benim odağım daha çok şuan 0$ fiyatlanan APRAGLUTIDE (kısaca APRA)

APRA nedir, neden önemliydi?

APRA, Short Bowel Syndrome (SBS) denen, çok nadir ama çok ağır bir hastalık için geliştirilen bir ilaç. Bu hastalarda bağırsak yeterince çalışmadığı için hastalar damar yoluyla beslenmek zorunda kalıyor. Hayat kalitesi çok düşük, maliyeti çok yüksek.

Buradaki kritik nokta şu:

Bu hastalık için FDA onaylı bir ilaç zaten var: Teduglutide.

Yani APRA’nın arkasındaki bilim denenmemiş değil.

APRA da aynı biyolojik yolu kullanıyor: GLP-2 mekanizması.

Farkı şu: Daha uzun etkili, haftada bir kullanılıyor,( diğer her gün ) teoride daha stabil ve hasta dostu

Yani FDA’nın karşısına çıkan şey şuydu: Aynı mekanizma, daha iyi bir versiyon.

Bu yüzden başından beri APRA, bilimsel olarak yüksek riskli bir ilaç değildi.

IRWD APRA’yı ne zaman aldı?

APRA’yı Vectivbio diye bir şirket geliştiriyordu. İrwd 2023 de bu şirkete 1 milyar dolar ödeyerek satın aldı ve apra da portföye dahil edilmiş oldu

Faz 3 (STARS) çalışması ne gösterdi?

APRA için yapılan Faz 3 çalışması (STARS):

Bu hastalık alanındaki en büyük çalışma. Güvenlik profili temizdi. Hastaların önemli bir kısmı damar yoluyla beslenmeyi bırakabildi (27 kişi sanırım) (enteral autonomy bu çok güçlü bir klinik sonuç)

Bilimsel açıdan bakıldığında:İlaç çalışıyordu

FDA’nın reddedeceği bir etkisizlik yoktu

Peki FDA neden onaylamadı?

İşte yatırımcıların en çok kafasının karıştığı yer burası.

FDA, ilacı bilimsel olarak reddetmedi.

Sorun ilacın ne yaptığı değil, *nasıl verildiği* ile ilgiliydi.

STARS çalışması sonrasında yapılan detaylı analizlerde şunu fark ettiler:

Çalışmada hedeflenen doz ile hastalara fiilen verilen doz tam örtüşmüyordu. Yani farmakokinetik (PK) açıdan:

İlaç çalıştı ama planladığınız dozun gerçekten verildiğini net şekilde kanıtlayamadınız.

Bu FDA için şuna benzer: Sonuç güzel ama prosedürü eksik.

Bu yüzden FDA:

İlaç işe yaramıyor demedi

Mekanizma yanlış demedi

Baştan her şeyi çöpe at demedi

Şunu dedi:

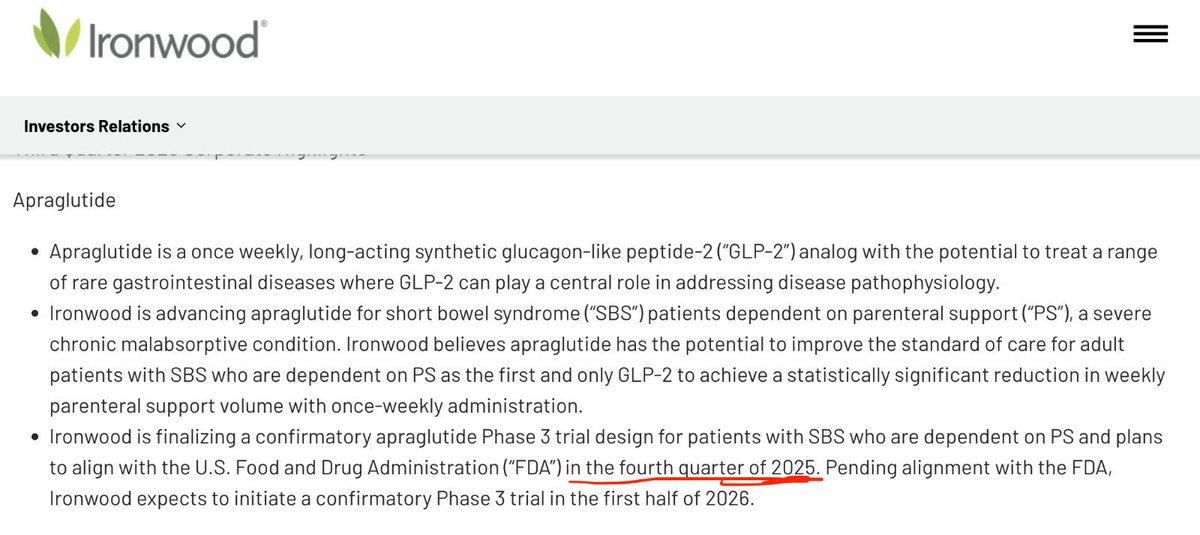

Bir confirmatory (doğrulayıcı) Faz 3 daha yap, bu sefer doz ve maruziyeti net şekilde göster. (Tabi bu denemeler basit değil şimdi başlasa 2027 sonuna anca sonuçlara ulaşıyorsun zaman ve para kaybı)

Şirket ne yaptı?

FDA ile görüşmelere başladı. Yeni Faz 3’ün tasarımını konuşuyor. Aynı anda Goldman Sachs ile çalışarak:

Şirket satışı, APRA’nın satışı, ortaklık gibi opsiyonları araştırıyor

Bugün itibarıyla şunu bekliyoruz:

FDA ile confirmatory Faz 3’ün nasıl olacağına dair nihai uzlaşı

Kaç hasta? Ne kadar sürecek? STARS verisi NDA’da nasıl kullanılacak?

2025 in son çeyreğinde fda ile yapılan görüşmeler dair bir update almamız gerekiyordu. Hala bir şey yok ortada

13

18

159

46,672

23 Oct 2025

$irwd VectivBio office leases in Basel expired in 2024. My understanding is that all Swiss employees working on the apra program are actually remote. Takeda EU HQ is in Zürich, lots of GI focus there. Easy to integrate in case of acquisition of the asset or irwd overall

5

494

14 Oct 2025

$bcrx deal reminds me a bit of $irwd buy of VectivBio. Bet on phase 3 asset, but no CVR used, all upfront. And fat debt to finance all that. This ended up badly for $irwd. Not sure how this plays out for BCRX.

I prefer $fold approach - pay a small option fee for flipping ph3 card

2

12

2,564

24 Sep 2025

) How each bidder would extract value / synergies (practical mechanics)

•AbbVie: integrate full gross margin, negotiate payer contracts directly (more aggressive rebates to offset Medicare pressure), bundle with other Allergan/AbbVie products in specialty contracts, optimize sales force to reduce co-promotion overlap.

•Takeda / Bausch: cross-sell to their GI salesforces, reallocate SG&A to improve margin, deploy promotional tactics in primary care & GI clinics to maintain NBRx.

•PE / royalty funds: lean operating structure, targeted marketing support via 3rd party commercialization partners, monetize via sale-leaseback of the revenue stream (royalty sale or asset securitization) and then exit ahead of generic erosion.

•Generics: buy rights to manufacture or secure authorized generic agreements to capture low-price volume when the clock ticks.

⸻

6) Illustrative deal math — how I’d value U.S. LINZESS rights (transparent assumptions)

(All figures in USD millions; these are illustrative — I show three cases so you can see sensitivity to sales, margin, multiple and conservatism for patent/Medicare risk.)

Key input datapoints used (public): 2024 U.S. LINZESS net sales ≈ $916.3M; reported brand commercial margin cited ~65%; Ironwood/AbbVie commentary on price erosion risk and patent settlement windows.

Scenarios (rounded):

•Base case (mid): Sales = $916.3M · margin 65% → EBITDA ≈ $596M. Apply industry multiple 8x → raw EV ≈ $4,765M. Apply risk haircut for patents/payer (≈30%) → EV ≈ $3.34B.

•Conservative: Sales = $800M · margin 60% → EBITDA = $480M; multiple 7x → raw EV = $3,360M; haircut 40% → EV ≈ $2.02B.

•Bull case: Sales = $1,000M · margin 70% → EBITDA = $700M; multiple 10x → raw EV = $7,000M; haircut 20% → EV ≈ $5.6B.

Takeaway: a rational strategic buyer paying for stable branded pharma cash flow could bid ~$2.0B to $5.6B for the U.S. LINZESS franchise depending on confidence in exclusivity, payer pressure, and synergy capture. Conservative acquirers (PE, risk-averse strategics) will cluster near low-$2bn; aggressive strategics (AbbVie capturing full synergy) can justify paying towards the higher end. (See assumptions & math above.)

I used current reported sales/margins and applied standard branded-pharma multiples, then applied haircuts for patent and pricing risk. These numbers are directional — final price depends on whether the deal includes global rights, pipeline (apraglutide), or only U.S. rights and any transition/service agreements.

⸻

7) Deal structures Ironwood should consider (to maximize proceeds / optionality)

1.Straight asset sale – U.S. LINZESS rights (highest immediate cash): buyer pays up front for U.S. rights; Ironwood keeps ex-US/pipeline. Best for fast monetization; downside is loss of long-term upside. Strategic buyers pay premium.

2.Sale licensing carve-outs (geographic tranching): sell EMEA/APAC rights to regionals (Almirall previously had EMEA experience with Constella), keep U.S. or vice versa — can harvest highest bids per region.

3.Royalty/receivable monetization: sell future revenue stream (e.g., 5–6 years of profits) to royalty fund; keeps upside post-generic but provides cash now. Attractive if Ironwood wants to fund pipeline (apraglutide).

4.AbbVie purchase of remaining share (cross-purchase): simple and logical given current collaboration arrangement — reduces integration friction and preserves continuity for prescribers.

5.Contingent/earn-out deal: buyer pays base plus milestones tied to patent outcomes, price erosion thresholds, or preservation of pre-generic market share. Lower upfront price but shares downside.

⸻

8) Negotiation/auction playbook — how Ironwood extracts the most value

1.Run a two-track process: (A) strategic auction with 4–6 pharma buyers (AbbVie, Takeda, Bausch, large diversifiers); (B) parallel financial auction (PE royalty funds). Competitive tension lifts price.

2.Carve rights intelligently: sell U.S. separately from ROW (regional buyers value local channels more). Offer AbbVie exclusive first-look on U.S. but keep timeline to auction other bidders.

3.De-risk revenue for buyers: provide audited IR data, payer contracts, Rx trends (IQVIA), and a realistic attrition model that shows steady NBRx vs price erosion — transparency reduces required haircuts.

4.Protect optionality on pipeline: keep apraglutide (or include it in a separate negotiation package) — pipeline assets materially lift strategic valuations. Many buyers will price a package higher if apraglutide (SBS-IF) is included. Ironwood’s recent VectivBio acquisition and apraglutide progress is a crucial optionality point.

5.Structure earn-outs tied to exclusivity duration: if buyer fears earlier generic entry, price part of the deal contingent on no authorized generic before X date or on certain net-price floors.

⸻

9) Risks & failure modes buyers will stress

•Generic entry earlier than modeled (court decision or weaker patents). That kills value. Settlements do not eliminate all legal risk.

•Medicare / PBM pricing pressure accelerating price erosion beyond forecasts. Ironwood has publicly signaled this as a material risk.

•Clinical or safety surprises (diarrhea leading to dropouts/new label constraints) — a smaller risk but buyer due diligence will re-audit safety database.

1

2

394

2 Dec 2023

It’s all the other complications that arise from #IBD medications and surgery which can easily go under the radar. Your post shows some of additional trials and tribulations we go through #IBDAwarenessWeek

3

78

30 Oct 2023

Entrepreneur of the Year Award für Urban Connect und VectivBio Gründer

startupticker.ch/en/news/ent…

2

241

21 Sep 2023

We were recently featured in an In Vivo article that quoted our CEO, Tom McCourt, and highlighted our recent acquisition of @VectivBio our incredible #GI leadership and the strength of our growing pipeline.

#WorkinginGIHealth

1

3

162

11 Aug 2023

We’re proud to join forces with VectivBio, now part of Ironwood, and support patients who experience #shortbowelsyndrome with #intestinalfailure (SBS-IF). Often the physical and mental scars of people living with SBS-IF are hidden and many face #misdiagnosis.

#ShortGut #Awareness

2

157

28 Jul 2023

We’re taking some time to reflect that Ironwood successfully completed the tender offer of VectivBio. Earlier this month, on the heels of this momentous milestone, we announced Jana Noeldeke as the new site leader of our Basel, Switzerland site.

#WorkinginGIHealth

2

182

REVERSALtoDOWN: $VECT VectivBio Holding AG Ordinary Shares via ➡️ alerttrade.us

304

29 Jun 2023

BREAKING: We’re pleased to announce that we successfully completed the tender offer of VectivBio, a global clinical-stage biotechnology company pioneering novel, transformational treatments for severe rare gastrointestinal conditions.

1

6

321

9 Jun 2023

💼 #Ironwood to acquire #VectivBio for $17.00 per share in an all-cash.

🥊 Investors suspect $VECT misrepresented its financial projections.

11thestate.com/cases/vectivb…

1

3

106

30 May 2023

Kodiak Sciences $KOD and VectivBio $VECT Financial Comparison modernreaders.com/?p=7618109 #investingnews

2

78

26 May 2023

Cooley advised VectivBio, a clinical-stage biotech company, on its acquisition by Ironwood, with an estimated aggregate consideration of approximately $1 billion. Congratulations, all.

➡️ Read more: bit.ly/3q9Evm7

2

260

25 May 2023

31

24 May 2023

Today's startup funding news: @hellocareme raises CHF6M, @AntefilTech raises CHF1.5M, $1B exit for #VectivBio, #Datacolor acquires @matchmycolor, @hydromeanews and #Inergio receive €2M and €1.2M from #Eurostar, and avoid down rounds venturelab.ch/startupfunding

1

5

320

23 May 2023

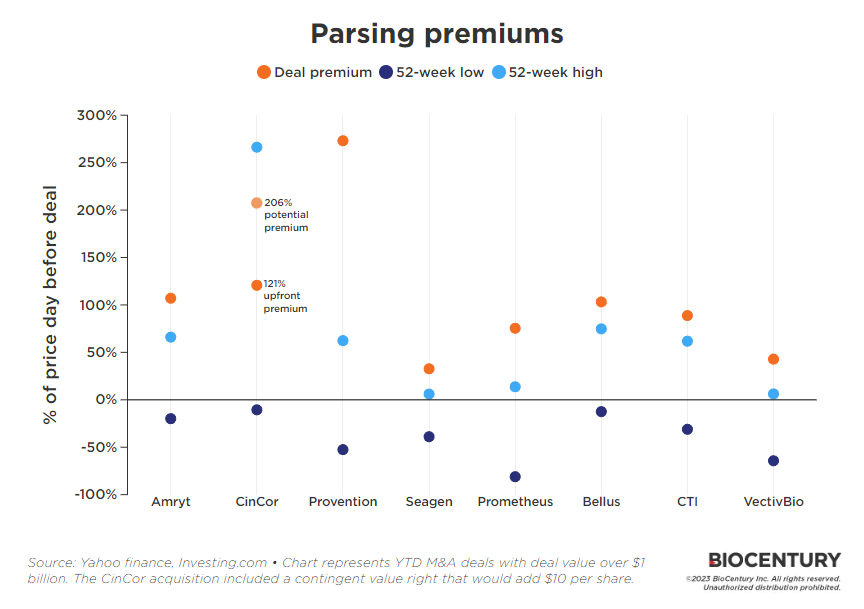

So how are biotech takeout premiums shaping up this year? @BioBonanos takes a look at M&A premiums vs 52-week highs and lows, and puts the VectivBio acquisition by Ironwood in context. Via @BioCentury. biocentury.com/article/64802…

1

9

25

5,643