(Bio)tech Investor. Not an investment advice, do your DD. DM for specific topics.

Joined March 2021

- Tweets 2,068

- Following 731

- Followers 821

- Likes 2,853

365 Photos and videos

Jun 13

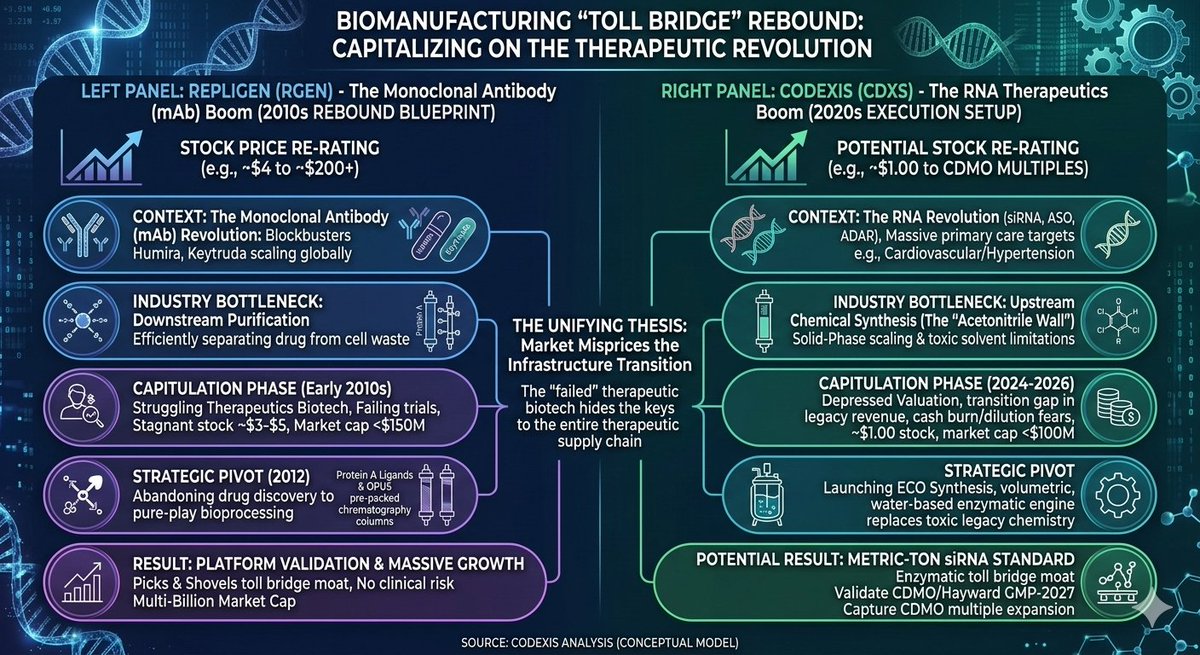

Like $gdyn a lot. Valued like a body shop, doing AI projects with fixed price contracts using internal tooling that makes delivery predictable. And all the physical AI stuff is completely not priced in

3

356

Jun 10

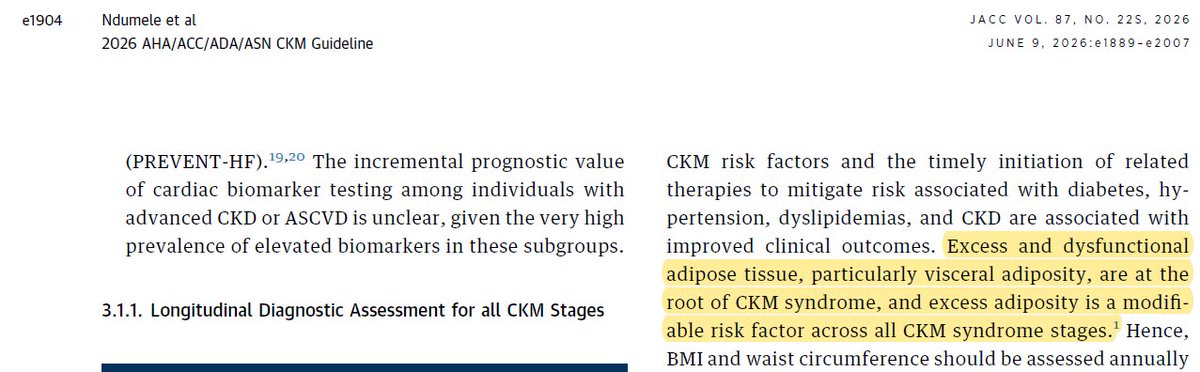

4 stage CKM classification reminds a bit of 4 stage MALSD/MASH.

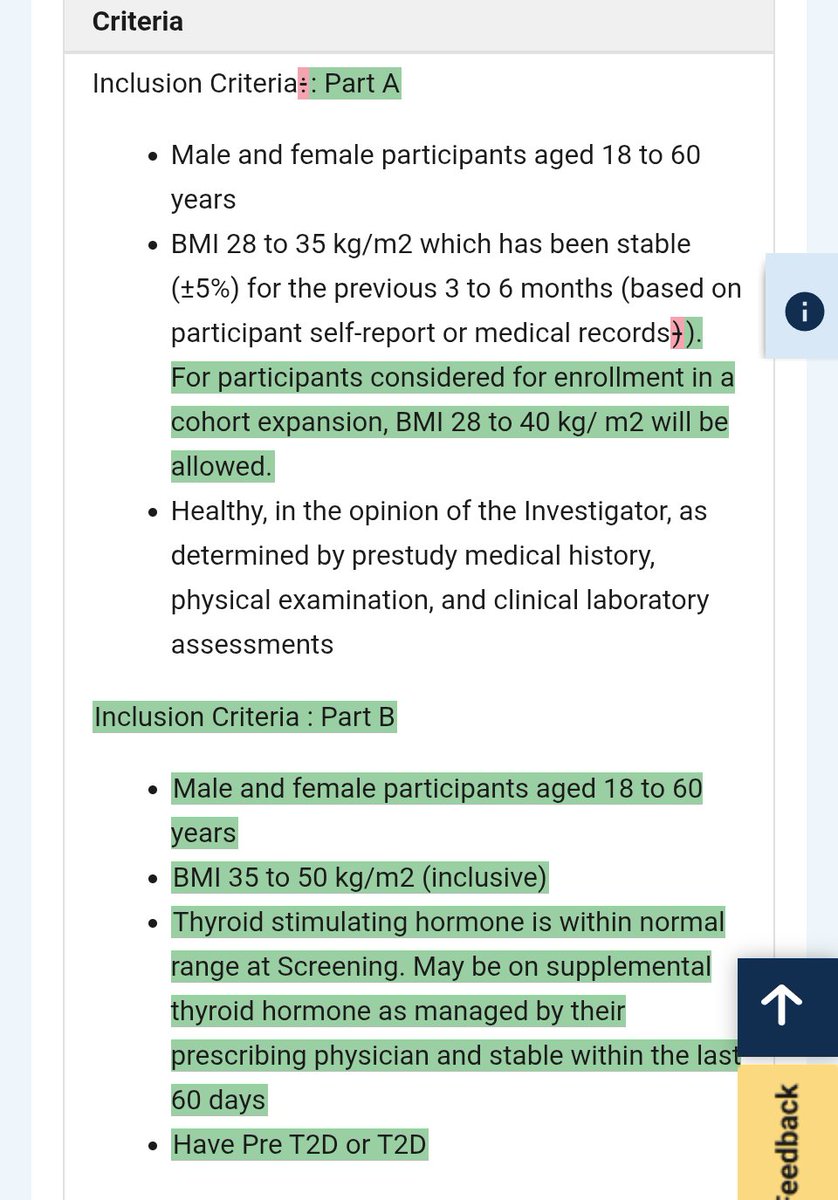

Targeting INHBE/ALK7 and PNPLA3 is a way to reach very large population. Big Pharma should lead. Players like $wve should not go beyond phase 2a with such assets. Upcoming redomiciliation is a hint.

Jun 10

The guidelines state that excess adipose tissue, particularly VAT, is 'at the root' of #CKM syndrome.

Given the development of fat-specific targeting agents like #inhibinE and #alk7, sponsors like $arwr and $wve should now work together w/ #FDA to agree on VAT loss as a primary endpoint for pivotal trials.

1

4

1,040

Jun 4

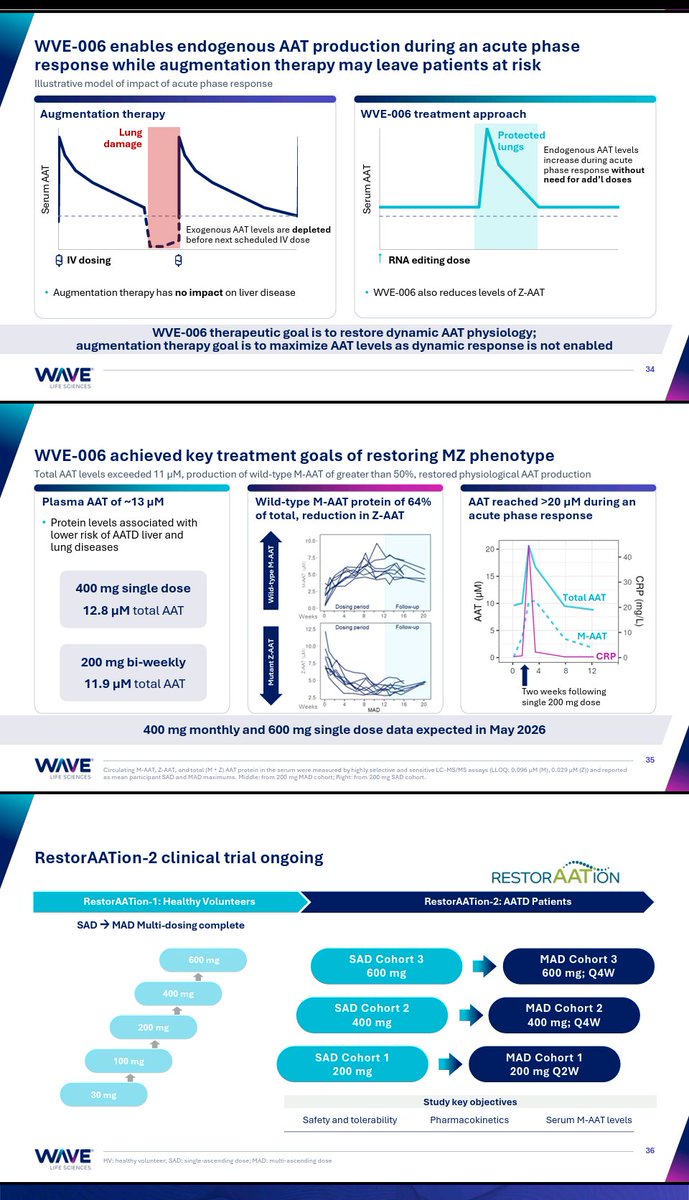

$wve will likely PR their ADA 2026 presentation tomorrow. I expect they concentrate on WVE-007 phase 1 data with detailed DXA scan metrics and MRI-PDFF readouts demonstrating targeted visceral fat reduction and lean muscle preservation.

Bought more in 5.70-5.80 area

7

1,035

Jun 2

$ABVX This is exactly the moment when M&A thesis might really materialize. Euphoria is over, pragmatic reality is here. M&A deals are rarely signed when execs and the board have too rosy valuation picture in their mind

1

16

1,303

May 31

5/5

The goal of oncology is to help cancer patients live longer, not to get better CT scans. Mature OS will always trump an early ORR flex.

1

2

702

May 31

1/6

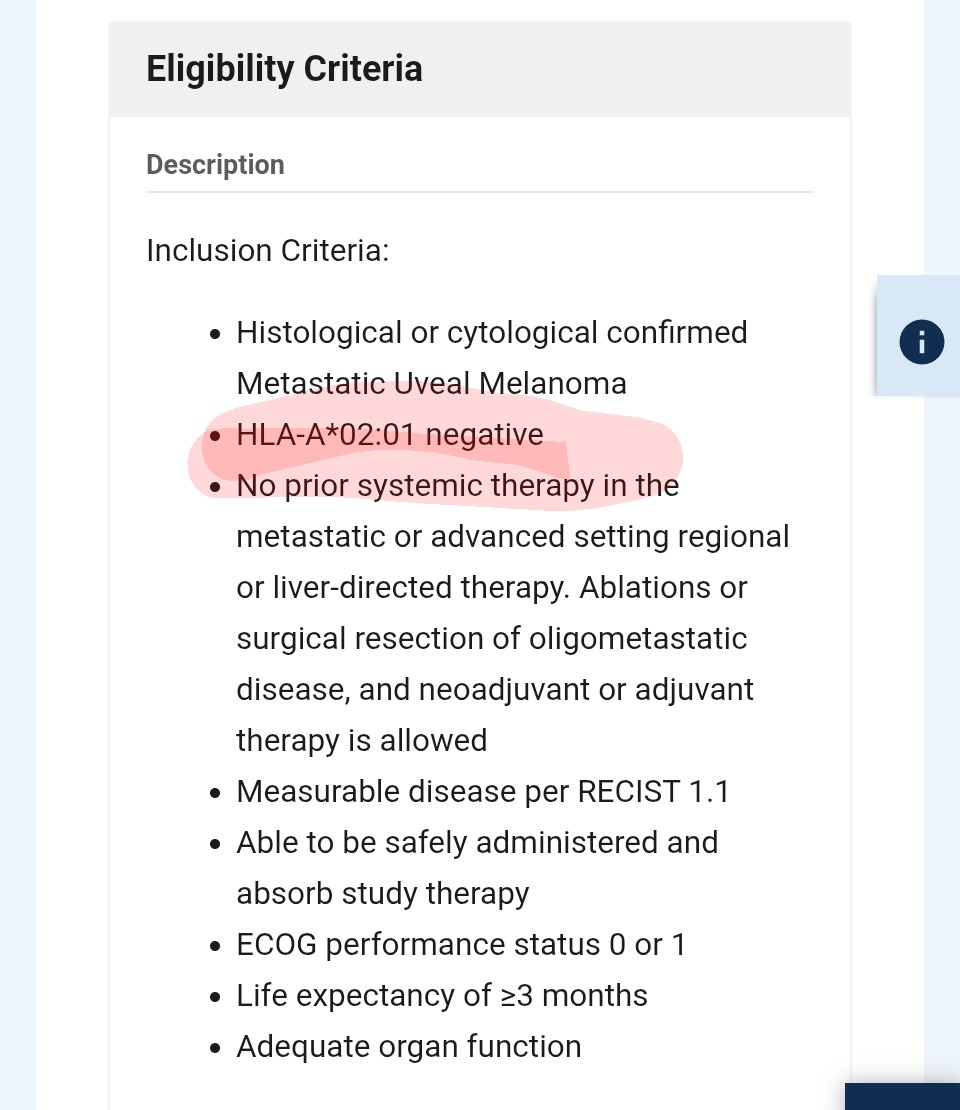

After ASCO 2024 $IMCR was sold because the market panicked over a low ORR, ignoring early ctDNA data, survival curves weren't mature. Today's ASCO release completely changes this, brene OS data unlocks the true potential of the ImmTAC platform. 🧵

immunocore.com/investors/new…

1

5

750

May 31

5/6

Competitors pushing autologous cell therapies may post higher ORRs, those come with massive logistical hurdles, including lymphodepleting chemo and ICU monitoring. ImmTACs are off-the-shelf bispecifics: standard IV bags in community clinics, wat lower COGS, ease of admin

1

1

290

May 31

6/6

The Setup: market currently prices $IMCR strictly as a niche uveal melanoma business, pricing the pipeline at zero. Mature OS data heavily de-risks the ongoing frontline cutaneous Phase 3 trial, exponentially larger TAM provides a clean fundamental path for a major re-rating.

3

359

May 28

Good job by $arwr by offloading the nonsense PNPLA3 silencing asset to $mdgl. Only editing, not silencing, makes sense for this target. $prqr $wve

May 28

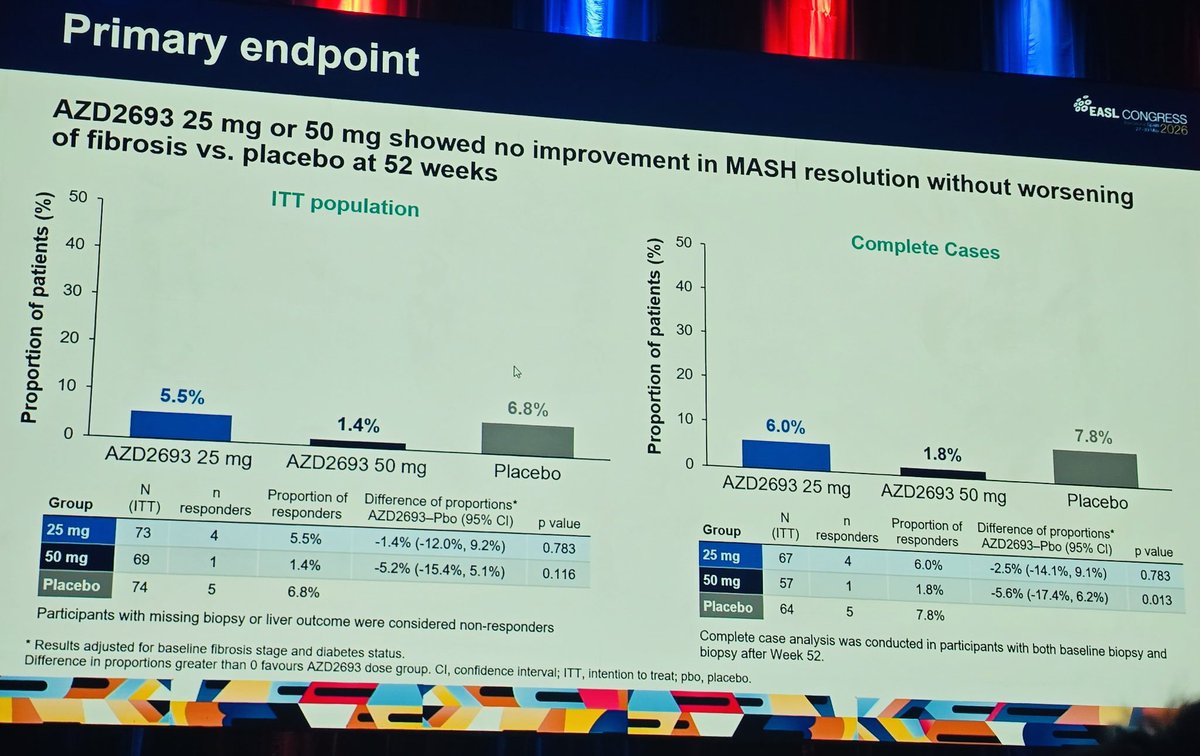

$AZN ASTRAZENECA’S MASH CANDIDATE AZD2693, A PNPLA3 ANTISENSE OLIGONUCLEOTIDE SHOWED NO IMPROVEMENT IN MASH RESOLUTION WITHOUT WORSENING OF FIBROSIS $IONS #MASH PH2 FAIL

$MDGL $NVO #MASH $XBI $VKTX

1

8

4,600