1 Oct 2025

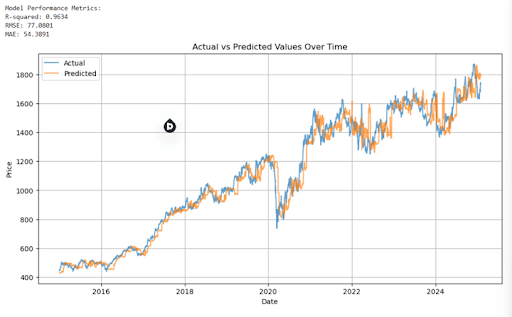

Have you ever noticed how a model that once predicted stock prices with pinpoint accuracy suddenly starts missing the mark? This isn’t just bad luck, it’s often the result of concept drift or model drift, common challenges in the ever-evolving world of quantitative finance.

Financial markets are anything but static; their dynamic nature means yesterday’s data patterns might not hold true today.

That’s where Walk-Forward Optimization (WFO) comes into play. By continuously retraining your model on the most recent data, WFO helps maintain predictive accuracy even as market conditions shift.

In this guide, you’ll learn how to implement WFO in Python, using XGBoost for stock price prediction.

👉blog.quantinsti.com/walk-for…

Want to learn more about Algo Trading, Check out our industry standard courses here: quantra.quantinsti.com/

And for those aiming to build a career in quant finance, explore the Executive Programme in Algorithmic Trading (EPAT) our flagship certification trusted by professionals worldwide.

👉 quantinsti.com/epat

#AlgorithmicTrading #QuantFinance #MachineLearning #XGBoost #WalkForwardOptimization #TradingStrategy #FinancialMarkets #DataScience #QuantInsti #EPAT #PythonForFinance

3

1

329

23 Mar 2023

Walk-Forward Optimization - The complete guide for

@ProRealTime™

Are you spending hours on backtestning but nothing on forwardtesting? Then you're an idiot🤡

youtu.be/Pu1P7o3syHM

@ProRealTimeFR @ProRealTimeDE #ProRealTime #WalkForwardTesting #WalkForwardOptimization

3

7

1,380

26 Apr 2021

Tweetimi düzeltiyorum.. #WalkForwardOptimization türünün ikinci örneği ilk gününü artı da kapattı. Darısı diğer günlere.

1

1

23 Apr 2021

Yeni #WalkForwardOptimization bakalım bu da yüzümüzü kara çıkarmazsa anlatım videosu yada flood' u yapacağım.

2

29

13 Apr 2021

#WalkForwardOptimization ...Bu arkadaş " beni artık canlıya almalısın " diye bas bas bağırıyor.

2

4

13 Mar 2021

Sadece boyuna segmentasyon yetmez, birazda enine segmentasyon lazım. Bakalım #PARA ve #WalkForwardOptimization neler yapabilecek...

1

14