17 Dec 2025

🚀 Build, Backtest, and Iterate Quant Strategies Faster with Swordfish

Our latest tutorial shows how to use PySwordfish’s event-driven backtesting framework to efficiently develop and validate multi-asset trading strategies—without getting buried in infrastructure details.

👉 medium.com/@DolphinDB_Inc/a-…

Designed for developers with Python skills, Swordfish helps you focus on strategy logic, not infrastructure complexity—making it ideal for medium- to high-frequency research and multi-asset portfolios.

Learn more about us: dolphindb.com/

#DolphinDB #QuantTrading #Backtesting #AlgorithmicTrading #PythonForFinance #SystematicTrading

3

54

6 Nov 2025

Beyond the Python and AI hands-on sessions, this training includes a leadership module led by Dr. Belinda Nwosu of LBS.

Slots are almost full. Send an email to info@nigeria.cfasociety.org to request participation details.

#CFANaija #CodingToCapital #PythonForFinance

2

13

710

1 Oct 2025

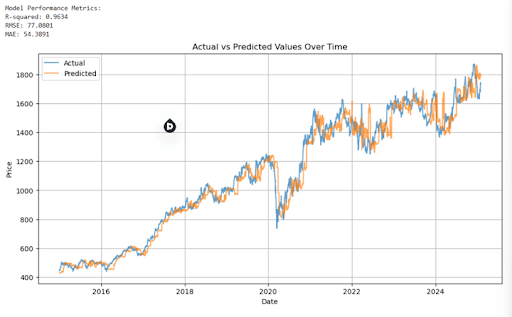

Have you ever noticed how a model that once predicted stock prices with pinpoint accuracy suddenly starts missing the mark? This isn’t just bad luck, it’s often the result of concept drift or model drift, common challenges in the ever-evolving world of quantitative finance.

Financial markets are anything but static; their dynamic nature means yesterday’s data patterns might not hold true today.

That’s where Walk-Forward Optimization (WFO) comes into play. By continuously retraining your model on the most recent data, WFO helps maintain predictive accuracy even as market conditions shift.

In this guide, you’ll learn how to implement WFO in Python, using XGBoost for stock price prediction.

👉blog.quantinsti.com/walk-for…

Want to learn more about Algo Trading, Check out our industry standard courses here: quantra.quantinsti.com/

And for those aiming to build a career in quant finance, explore the Executive Programme in Algorithmic Trading (EPAT) our flagship certification trusted by professionals worldwide.

👉 quantinsti.com/epat

#AlgorithmicTrading #QuantFinance #MachineLearning #XGBoost #WalkForwardOptimization #TradingStrategy #FinancialMarkets #DataScience #QuantInsti #EPAT #PythonForFinance

3

1

329

26 Sep 2025

What exactly is forward propagation in neural networks? Well, if we break down the words, "forward" implies moving ahead, and "propagation" refers to the spreading of something.

In neural networks, forward propagation means moving in only one direction: from input to output. Think of it as moving forward in time, where we have no option but to keep moving ahead!

In this blog, we will delve into the intricacies of forward propagation, its calculation process, and its significance in different types of neural networks, including feedforward propagation, CNNs, and ANNs.

👉blog.quantinsti.com/forward-…

This blog also explores the components involved, such as activation functions, weights, and biases, and discusses its applications across various domains, including trading.

Additionally, discuss the examples of forward propagation implemented using Python, along with potential future developments and FAQs.

Want to learn by doing?

Explore hands-on courses on Neural Networks, Machine Learning, and AI in Trading with Quantra.

👉 Don’t miss out on our 15th Anniversary Sale – enroll today and get a minimum of 75% off on any course!: quantra.quantinsti.com/

And if you’re aiming to build a career in algorithmic and quantitative trading, check out our flagship program, the Executive Programme in Algorithmic Trading (EPAT): quantinsti.com/epat

#NeuralNetworks #MachineLearning #DeepLearning #QuantFinance #ArtificialIntelligence #AlgorithmicTrading #PythonForFinance #ForwardPropagation #QuantInsti #Quantra #EPAT

4

1

222

20 Sep 2025

Fibonacci trading tools are used to determine support/resistance levels or to identify price targets.

It is the presence of the Fibonacci series in nature which attracted technical analysts’ attention to use Fibonacci for trading. Fibonacci numbers may work like magic in some cases, in finding key levels in any widely traded security. Fibonacci's retracement strategy relies on key retracement levels to predict future price movements.

In this guide, we delve into Fibonacci retracement levels and their implementation using Python, enabling traders to leverage these mathematical principles for informed decision-making.

👉blog.quantinsti.com/fibonacc…

By combining technical analysis with programming capabilities, traders gain a deeper understanding of market dynamics and enhance their ability to execute trades with maximum returns.

Don’t miss out!

More than 11,000 quants, finance professionals, and tech experts are already registered for the Algorithmic Trading Conference 2025 – happening 23rd September | Virtual | Free to attend.

Explore how AI is shaping trading with insights from top global experts.

🔗 Register here: quantinsti.com/algorithmic-t…

#RiskManagement #TradingStrategy #AlgoTrading #QuantFinance #PythonForFinance #TradingCommunity #QuantInsti

1

2

233

16 Sep 2025

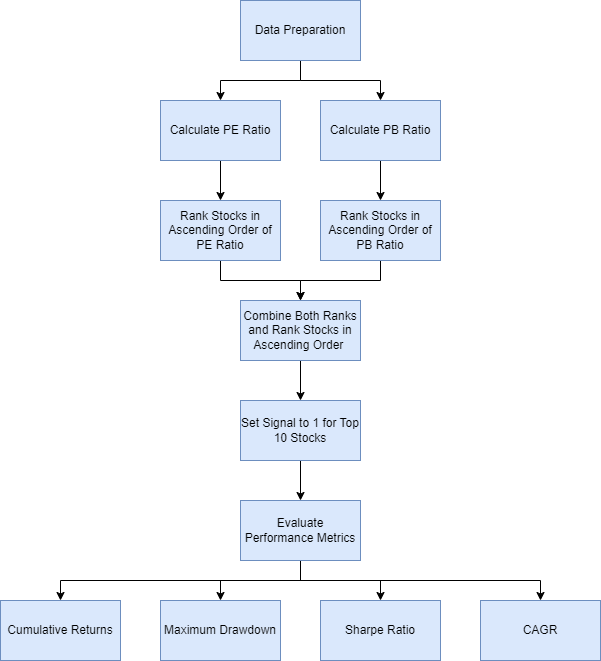

What is Value? And how can you use it?

Value is what you attribute to a thing or concept. One way is to use the relative value approach. Here, you compare companies on the basis of their financial ratios, like the PE and PB ratios, and choose the stocks which are value for money.

At Quantra, we’ve a comprehensive course on Factor Investing: Concepts and Strategies [Free preview available].

Link to free preview: quantra.quantinsti.com/start…

The steps to create the value strategy are as follows:

Retrieve the financial statements required to calculate the financial ratios, PE Ratio and PB Ratio for your stock portfolio. In the course, we have used the fundamental data of the top 100 companies in the S&P 500 according to the market cap in 2017.

Calculate PE and PB ratio. The formula is as shown below:

PE ratio = (Price of asset) / (Earnings per share)

PB ratio = (Price of asset) / (Book value per share)

Rank the assets in ascending order for the day. Note that the undervalued assets possess a low PE and PB Ratio. Thus, the most undervalued asset will be the one with the lowest PE and PB Ratio.

Combine both ranks and find the top 10 undervalued stocks.

Go long on the top 10 stocks in the portfolio.

💡 The markets reward those who understand the factors driving them.

Are you ready to turn value into growth? Then learn more with the Quantra course.

Link to the full course: quantra.quantinsti.com/cours…

Share your thoughts below 👇

Do you think value still beats growth in today’s markets?

📢 Want to learn how the concepts are evolving with AI in trading?

Join the AI in Trading Summit 2025 by QuantInsti on 23rd September 2025 and discover how global experts are using AI to spot "unusual" market opportunities.

✅ Free to attend | Virtual Event

👉 Register here: quantinsti.com/algorithmic-t…

#FactorInvesting #QuantitativeFinance #InvestingStrategies #OptionsAndFactors #PortfolioManagement #SystematicInvesting #AlgoTrading #ValueInvesting #GrowthVsValue #PERatio #PBRatio #FinancialMarkets #StockSelection #InvestmentStrategy #Quantra #QuantInsti #LearnTrading #PythonForFinance #BacktestingStrategies #TradingEducation #FinanceWithAI #AIinTrading #TradingSummit2025 #AlgorithmicTrading #FinTechInnovation #FutureOfTrading

3

302

12 Sep 2025

🌍 From Chile to Quant Finance, Elías Andrés Gaete Fuenzalida turned his capstone into a practical strategy that makes diversification both simple and effective.

His project developed a risk-based rebalancing portfolio of 22 S&P 500 stocks across 11 sectors, adjusting allocations quarterly based on volatility. The strategy showed resilience during COVID-19, delivering lower drawdowns, reduced volatility, and a stronger Sharpe ratio than the benchmark. He even added a hedging layer by shorting the benchmark proportional to portfolio beta, demonstrating real sophistication in portfolio construction.

In the words of Elías:

“The idea was simple: help people understand how to reduce risk through diversification, and rebalance the portfolio regularly to maintain stability.”

Read the details in this blog link:

blog.quantinsti.com/elias-jo…

Additionally, you can download the Python code using the downloadable button located at the bottom of the blog.

📢 Want to learn how the concepts are evolving with AI in trading?

Join the AI in Trading Summit 2025 by QuantInsti on 23rd September 2025 and discover how global experts are using AI to spot "unusual" market opportunities.

✅ Free to attend | Virtual Event

👉 Register here: quantinsti.com/algorithmic-t…

#QuantFinance #AlgorithmicTrading #QuantTrading #MachineLearning #AIinTrading #PortfolioManagement #RiskManagement #TradingStrategy #Backtesting #Investing #QuantCommunity #FinanceInnovation #PythonForFinance #QuantResearch #TradingWithAI #EPAT #QuantInsti

1

1

3

507

From Idea to Execution with Jason Strimpel | Python Algo Trading Workshop Sept 27 📈

⚡ Seats Are Limited. Register Today: [eventbrite.com/e/algorithmic…]

#AlgoTrading #Quant #PythonForFinance

1

2

6,319

16 Aug 2025

📈 Gamma Scalping: A Professional’s Approach to Volatile Markets

Have you ever wondered which options strategies traders rely on when markets are unpredictable?

One technique used by professionals is Gamma Scalping, dynamically adjusting positions to profit from price swings while controlling risk.

Here’s a quick breakdown from our recent Quantra Classroom:

1️⃣ What is Gamma in Options Trading?

Gamma measures how much an option’s delta changes when the underlying asset’s price moves.

High gamma = delta changes quickly (common in at-the-money options)

Low gamma = delta changes more gradually

2️⃣ What is Gamma Scalping?

A strategy to stay delta-neutral is to adjust positions as the market moves, buy low, sell high, and capture small gains over time.

3️⃣ How Gamma Scalping Works

Step 1: Start with a delta-neutral position

Step 2: Monitor underlying price changes

Step 3: Adjust holdings to stay delta-neutral (buy when the price falls, sell when it rises)

4️⃣ Managing Transaction Costs

Frequent trading means costs can add up, professionals minimise them through:

- Low-cost platforms

- Careful position sizing

5️⃣ Example Scenario

📍 Stock at $100, call delta = 0.5, gamma = 0.05

Price rises to $101 → delta = 0.55 → sell 5 more shares

Price falls to $99 → delta = 0.45 → buy 5 shares

In both cases, small profits are captured from the price movement due to the changing delta.

💡 Key Takeaway: Gamma scalping thrives in volatile markets by leveraging price swings for incremental gains, but it requires discipline, monitoring, and cost management.

📌 Explore the complete walkthrough with examples and Python code in our Quantra course: Options Trading Strategies in Python: Advanced.

quantra.quantinsti.com/cours…?

Also, get the code here:

quantra.quantinsti.com/start…

#OptionsTrading #GammaScalping #DeltaNeutral #VolatileMarkets #TradingStrategy #PythonForFinance #Quantra

1

1

4

456

24 Jul 2025

📷

The Role of a Quantitative Trader

Quantitative traders are not merely executing pre-built algorithms—they are actively managing and optimizing them in dynamic market environments. Operating at the intersection of mathematics, programming, and high-speed execution, they serve as the decision-makers responsible for translating quantitative models into live trading strategies.

Core Responsibilities of a Quantitative Trader

A quantitative trader typically oversees the full lifecycle of algorithmic trading operations:

1. Pre-Market Preparation:

Assess macroeconomic trends and market sentiment

Review prior day’s performance, including profit and loss (P&L), slippage, and volatility conditions

Align strategy parameters with current market regimes

2. Live Trading Operations:

Monitor real-time market data and system performance

Adjust strategy parameters based on intra-day developments

Execute trades and rebalance portfolios as needed

Respond swiftly to anomalies and unexpected events

3. Post-Market Analysis:

Conduct performance attribution and execution quality analysis

Identify areas of inefficiency or risk exposure

Collaborate with quantitative researchers to incorporate feedback into model refinements

Beyond Execution: Strategic Involvement

Quantitative traders play an active role beyond automated execution. Their responsibilities include:

Real-time strategy adaptation based on evolving market conditions

Latency management and execution optimization

Communication with researchers, software engineers, and risk management teams

Maintaining robustness and precision under volatile market conditions

Employment Contexts

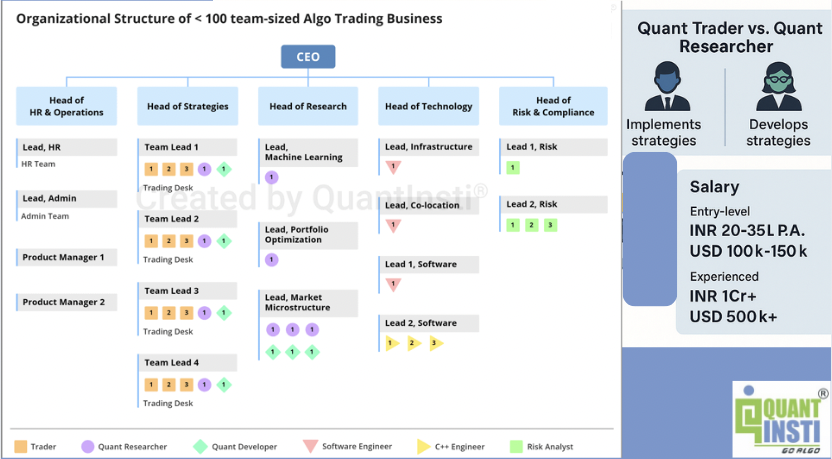

Quantitative traders work across a range of financial institutions, each with distinct operational styles:

Proprietary Trading Firms (e.g., DRW, Quadeye, iRage): Agile and risk-tolerant environments focused on rapid innovation and iteration

Investment Banks (e.g., JPMorgan, Goldman Sachs): Structured settings with high-volume execution and regulatory oversight

Hedge Funds and Crypto Firms: Diverse opportunities for model-driven trading in traditional and digital asset markets

🎓 Start Your Journey Today:

✅ Take the 10-minute Quant Aptitude Test

🔗 quantinsti.com/admissions#be…

✅ Read the full Quant Trader Career Guide

🔗 quantinsti.com/articles/quan…

✅ Ready to build the skills for this demanding role? Get a personalized roadmap and see how our Executive Programme in Algorithmic Trading (EPAT) can help you get there.

🔗 Schedule a free career counseling call with our experts: calendly.com/counsellor-1/sp… ak-to-epat-counsellors

📌 Whether you're a coder, math geek, or market enthusiast,if you're ready to trade with precision and speed, the world of Quant Trading awaits.

#QuantTrader #AlgoTrading #TradingCareers #QuantJobs #FinanceCareers #QuantitativeFinance #PythonForFinance #MarketMicrostructure #PropTrading #QuantInsti #EPAT #Quantra

1

3

360

22 Jul 2025

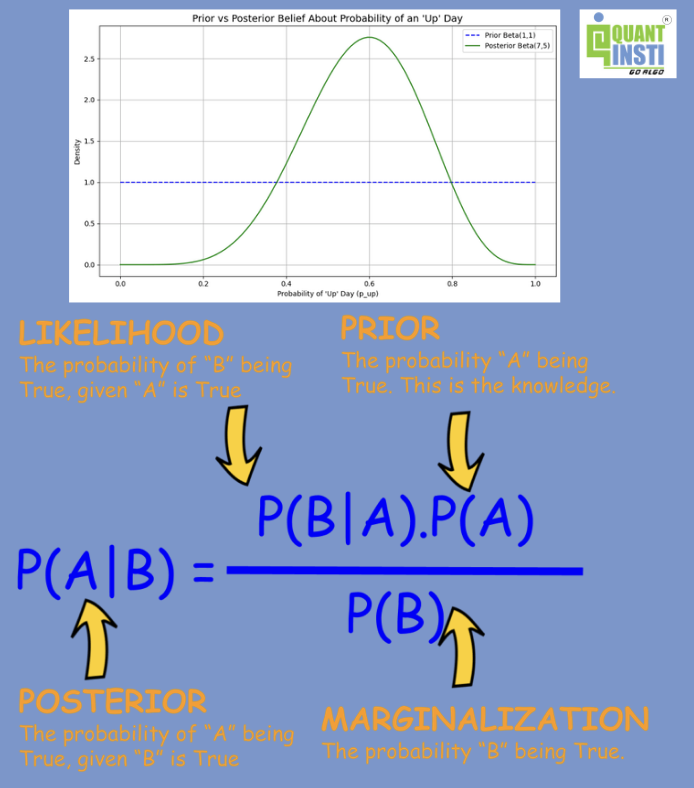

📊 Exploring Bayesian Techniques in Algorithmic Trading

Bayesian methods provide a framework in which probabilities are updated as new information becomes available, making them particularly relevant for evolving financial systems.

This project outlines how such techniques were applied to trading-related tasks involving price prediction, parameter adaptation, and risk evaluation.

🔍 Project Highlights

• Built two deep learning models to forecast open prices of the Bank Nifty index and its top five constituents

• Used 21 months of 1-minute data and 20 years of daily data for training/testing

• Integrated techniques such as SMOTE for class imbalance and XGBoost for feature ranking

• Applied Keras callbacks (EarlyStopping, ModelCheckpoint) to address overfitting

• Focused on consensus-based signals, where both models must agree before executing trades

• Managed minute-level and daily datasets using a MySQL database

🧠 Tools and Techniques Used

TensorFlow & Keras

Scikit-learn, XGBoost, TA-Lib

SMOTE (Imbalanced-learn)

Feature engineering with RSI, MFI, ATR, Bollinger Bands, and more

Read the full guide with the entire project here: blog.quantinsti.com/introduc…

📚 For readers interested in related topics:

Quant Roles Overview: quantinsti.com/quant-roles

Quantitative Trader: quantinsti.com/articles/quan…

Quant Analyst & Researcher: quantinsti.com/articles/quan…

Quant Developer: quantinsti.com/quant-roles/q…

Risk Analyst: quantinsti.com/articles/risk…

🔗 Learn more about the EPAT programme: quantinsti.com/epat

📣 🔴 Detailed EPAT Walkthrough & AMA | Live Webinar

Join us for a dedicated session exploring the Executive Programme in Algorithmic Trading (EPAT).

Get a comprehensive overview of the 6-month journey, support offered, alumni success, and post-programme career services. The session concludes with a live Q&A.

🗓️ Thursday, July 24, 2025

🕗 8:30 AM EST | 6:30 PM IST | 9:00 PM SGT

🎤 Speaker: Rohan Mathews, Global Business Head – QuantInsti

🔗 Register: quantinsti.com/epat

#QuantInsti #EPAT #AlgorithmicTrading #QuantRoles #DeepLearning #PythonForFinance #BayesianModel #TradingSystems #FinancialData #Backtesting #QuantitativeFinance #FeatureEngineering

1

3

289

20 Jul 2025

📈 Cross-Sectional Momentum Trading: a strategy that’s less about predicting market direction and more about riding the wave of proven outperformers.

Instead of guessing which stock might go up, this approach identifies those already demonstrating strong price performance and doubles down on winners while filtering out the laggards.

At QuantInsti, we recently backtested this strategy using a carefully constructed portfolio. The results?

🔹 Long-Short Strategy: Riding top performers while shorting the underperformers

🔹 Long-Only Strategy: Tailored for institutions restricted from shorting

Both strategies showed compelling returns. (And yes, the Python code used is available in Section 14, Unit 12 of our Momentum Trading Strategies course on Quantra!)

Link: quantra.quantinsti.com/start…

🧠 So what is cross-sectional momentum trading?

It’s a relative performance-based approach.

Let's take a look at a popular example: Palantir Technologies Inc. This company has been on fire in terms of its stock price for quite some time. A long-time favourite, Apple's stock has been on a steady upward trajectory, with impressive relative gains year after year. Meanwhile, another tech giant, Microsoft, has also been performing well over the years. The strategy assumes that recent winners will likely continue outperforming.

⏱️ The Role of the Lookback Period

Choosing the right lookback window is critical. Too short (<1 month), and you risk mean reversion. Too long (>1 year), and returns may reverse.

🧪 We found the sweet spot lies in the 1-12 month range, strong enough to detect momentum, but not so long that it fades.

🧮 Ranking, Filtering & Turnover

To build an effective portfolio:

Start by filtering for top 100 stocks by daily turnover

Rank them based on past returns (lookback window)

Go long on the top decile (winners) and short the bottom decile (losers)

This ranking methodology helps uncover hidden relative strength and trading opportunities.

📦 Portfolio Construction & Constraints

💡 A 20-stock portfolio (10 long 10 short) often strikes the right balance between diversification, capital efficiency, and transaction cost control.

And for those restricted from shorting? A long-only variation of this strategy remains highly viable, especially with proper risk management and position sizing.

🔑 Key Takeaways

✅ Focus on winners, avoid laggards

⚖️ Balance between risk and return

📊 Use turnover to filter and rank smartly

🛠️ Applicable even for long-only institutional portfolios

This strategy is part of our broader Momentum Trading Strategies course on Quantra, where we empower traders and quants to make data-driven decisions. You'll learn not just cross-sectional momentum, but also, time-series momentum, used widely across asset classes.

📌 Reminder: These are backtest results. Real-world performance may vary based on execution and market conditions.

Dive deeper into both cross-sectional and time-series momentum in the full Momentum Trading Strategies course on Quantra.

🎯 Free Resource:

Want to go from market basics to building data-driven strategies?

🚀 Explore this Free Learning Track for Beginners and start your quant journey today:

quantra.quantinsti.com/learn…

#QuantInsti #Quantra #MomentumTrading #CrossSectionalMomentum #AlgoTrading #TradingStrategies #PythonForFinance #Backtesting #QuantitativeFinance

1

2

6

383

17 Jul 2025

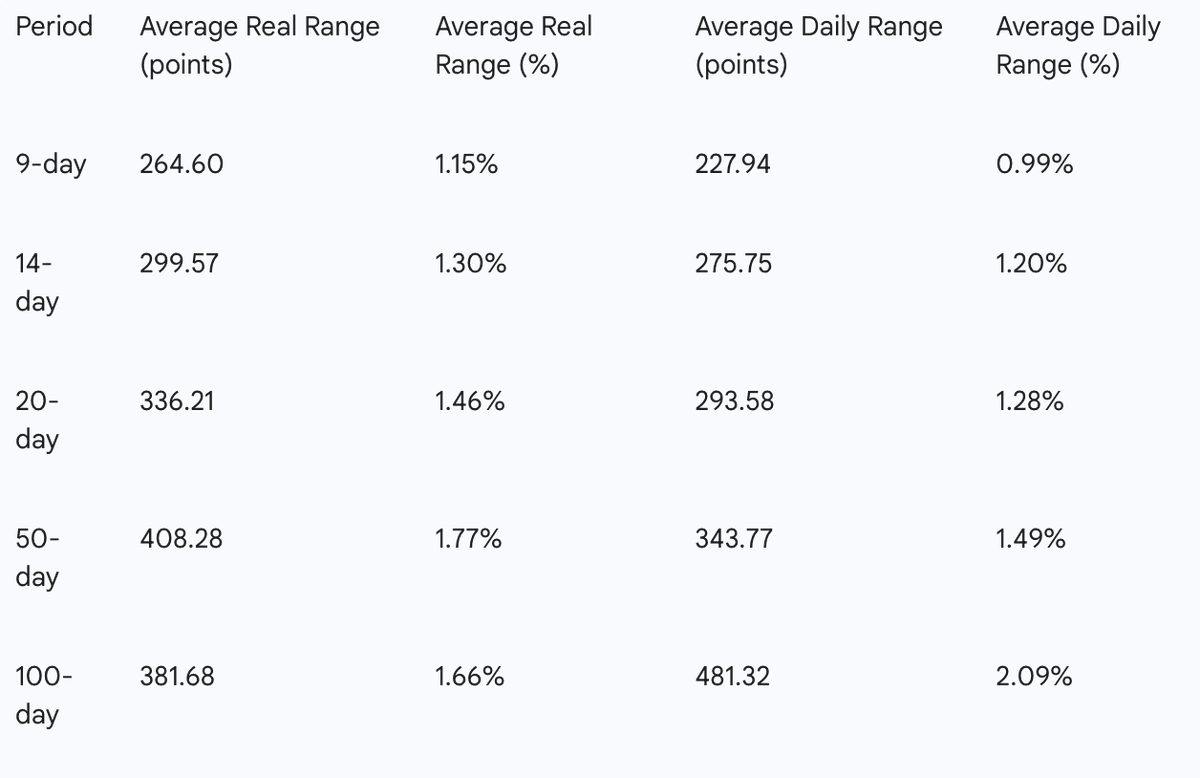

📊Digging into market volatility:

Here's a look at average daily and real ranges across different periods (9-day to 100-day). Interesting to see how these metrics evolve.

#QuantAnalysis #Stats #DataScience #FinancialModeling #AlgorithmicTrading #MachineLearning #MarketData #FinancialEngineering #Econometrics #TimeSeries #QuantitativeFinance #BigData #PythonForFinance #RStats #NumericalMethods #TradingStrategy #RiskManagement #MarketAnalytics #PredictiveModeling #ComputationalFinance

2

4

1,394

5 Jul 2025

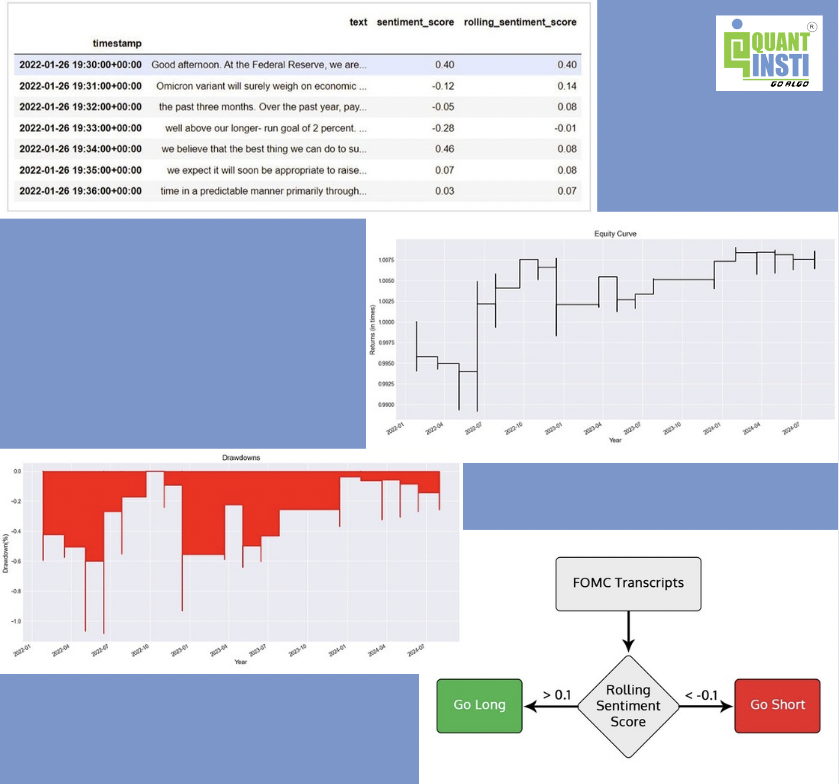

💬 Trading with Market Sentiment? LLMs Just Changed the Game.

Every trader is aware of the impact of FOMC meetings, earnings calls, and central bank announcements. But what if you could quantify market sentiment from these events and trade on it in real-time?

That’s exactly what you’ll learn in the Quantra course: Trading Using LLM, Concepts and Strategies (Get the free preview of the code).

⚙️ What You’ll Explore:

🔹 How to apply LLMs like FinBERT for financial sentiment analysis

🔹 Extract rolling sentiment scores from FOMC transcripts

🔹 Build a strategy with Python to go long or short based on sentiment shifts

🔹 Set thresholds to trigger trades and manage exits

🔹 Backtest and analyse strategy performance

🔹 Learn from real examples between Jan 2022 - Jul 2024

Example: A rolling sentiment score above 0.1? - Go long.

Below -0.1? - Go Short.

And yes, the drawdown was under 1.1% during backtests.

📌 You can get the entire code in the free preview in Section 16, Unit 7 of the course ‘Trading Using LLM: Concepts and Strategies’.

Link: quantra.quantinsti.com/start…?

🔗 Available after login at: quantra.quantinsti.com

🎓 New to Python? Start with Python for Trading on Quantra to build the foundation.

Link to Course: quantra.quantinsti.com/cours…

💻 Real-time application. Real strategy building. Real sentiment signals.

🎓 Want to learn from scratch and build stronger trading foundations?

✅ Free Learning Track: 8-Course Starter Kit

Perfect for beginners starting their journey in algorithmic trading

🔗 quantra.quantinsti.com/learn…

💡 Considering a deeper career transition into algorithmic trading?

📅 EPAT Summer Sale: Save up to ₹35,000

Schedule a call with our admissions team:

🔗 calendly.com/counsellor-1/ad…

📚 #LLMTrading #SentimentAnalysis #FinBERT #AlgoTrading #FOMC #QuantitativeTrading #PythonForFinance #MarketSentiment #TradingStrategy #NLPinFinance #QuantInsti #Backtesting #VolatilityTrading #AIinFinance

1

3

312

The Quantitative Developer Certificate (QDC) - A High-Calibre Programme – Without the High Price Tag

Full Information Session: lnkd.in/e6TtT8SG

#QuantDev #QuantFinance #FinancialEngineering

#QuantitativeFinance #FinTech #PythonForFinance #DataScience

3

302

1 Jul 2025

⏳ Only 1 more day left!

If you’ve been waiting for the right time to level up your trading skills; this is it.

🎯 Whether you’re just starting out or scaling up:

✅ Learn Python from scratch

✅ Build and automate your trading strategies

✅ Analyse financial data like a pro

✅ Explore machine learning for real-world finance

📦 25 expert-led courses in one bundle

🎁 Get 86% Off the All Courses Bundle

👉 quantra.quantinsti.com/all-c…

📚 Popular Courses Included:

Python for Trading

Options Trading Strategies

Machine Learning for Trading

Technical Indicators & Strategies

Portfolio Optimization

⚡ Unlock lifetime access. No subscription. Just skills that scale with you.

#Quantra #SummerSale #QuantEducation #TradingSkills #PythonForFinance #AlgoTrading #QuantTrading #OnlineLearning #FinancialMarkets #LastChance

1

2

252

30 Jun 2025

🚀 Quant Traders: The Generals of the Algorithmic Battlefield

Strategy Execution Isn’t Passive; It’s Tactical Warfare.

Think of algorithms as specialised combat robots.

🧠 Quantitative researchers design these robots; brilliant, backtested, and mathematically elegant.

⚔️ But Quant Traders take them to war.

They don’t just “run” strategies. They command, adapt, and survive in live markets, where milliseconds matter.

🎯 The Quant Trader’s Lifecycle

Pre-Market: Strategy Readiness

Review overnight data, macro indicators, and volatility regimes

Analyse P&L attribution, slippage, and execution quality

Check: Are strategies aligned with today’s conditions?

Live Trading: Adaptive Execution

Deploy and monitor portfolios in real time

Respond to market events and anomalies

Adjust parameters, rebalance weights, and ensure system integrity

Post-Market: Analysis & Feedback

Review performance: What worked, what didn’t, and why

Feed insights back to researchers to improve strategy baskets

🏢 Where Do They Work?

Prop Desks (e.g. iRage, Quadeye, DRW): Fast, risk-taking

Bank Desks (e.g. JPMorgan, Goldman Sachs): Structured, regulated

Hedge Funds, Crypto, Startups: Strategy meets scale and innovation

💡 What Makes a Great Quant Trader?

🧠 Technical Skills

Python, R, SQL, C for strategy coding and automation

Advanced stats, probability, calculus, linear algebra

Market knowledge: options, ETFs, futures, microstructure

Trading systems: real-time APIs, execution engines, backtesting tools

⚔️ Analytical & Strategic Edge

Creative problem-solving in uncertain conditions

Fast, high-quality decision-making under pressure

Precision in coding, risk analysis, and execution logic

🤝 Human Factor

Clear communication with researchers, developers, and risk teams

Collaboration in fast-paced teams

Resilience: iterate after failures, stay calm under stress

🎓 Want to Become a Quant Trader?

✅ Learn Python, stats, and trading concepts

✅ Practice on platforms like BlueShift

✅ Join structured programs like EPAT

✅ Read the full Career Guide:

🔗 quantinsti.com/articles/quan…

✅ Start now with our free 5-hour Quant Interview Prep course

🔗 quantra.quantinsti.com/cours…

#QuantTrader #AlgorithmicTrading #QuantCareer #HighFrequencyTrading #QuantJobs #PythonForFinance #FinancialMarkets #TradingCareers #Backtesting #MarketMicrostructure #EPAT #Quantra #QuantInsti #PropTrading

1

2

371

27 Jun 2025

Live Today at 5 PM IST: Don’t miss Mr Nitesh Khandelwal on Face2Face Trading

QuantInsti CEO Nitesh Khandelwa joins Vivek Bajaj and Vishal Mehta to break down:

What Is Algorithmic Trading?

Is Technical & Price Analysis Needed For Algo Trading?

How Does Algo Work For Retail & Institutional?

Can Operators See Your Stop Loss?

Understanding Algo Trading Terminology

Decoding SEBI's New Algo Trading Circular

Hidden Risks Every Algo Trader Must Know

Regulation Around Algo Trading Strategy

How Have Algo Traders Evolved Over The Years?

Is Intraday Right For Retail Traders?

How To Build A Business Around Algo Trading?

What’s The Future Of Retail Traders?

📺 Set a reminder & watch the premiere → youtube.com/watch?v=6F17nvPw…

#AlgorithmicTrading #AlgoTradingIndia #QuantCareers #IntradayTrading #CommodityOptions #QuantInsti #EPAT #TradingEducation #MarketScanner #StockEdge #Elearnmarkets #NiteshKhandelwal #VivekBajaj #VishalMehta #Face2FaceTrading #FinanceCareer #MachineLearningForTrading #SystematicTrading #TradingStrategy #PythonForFinance #YouTubePremiere

3

301

27 Jun 2025

🚀 The Brains Behind a Quant Trading Desk

🔍 Who drives innovation in quantitative finance?

The roles of Quantitative Researcher and Quantitative Analyst are often used interchangeably. While both use statistics, data analysis, and computational techniques to solve complex problems, Quant Researchers stand out for one key reason: versatility.

💡 Whether in a hedge fund, HFT firm, family office, fintech, or regulatory body, quant researchers:

1. Analyse high-frequency & alternative datasets

2. Detect inefficiencies and build alpha-generating models

3. Backtest strategies with rigorous statistical frameworks

4. Integrate machine learning with financial theory

5. Optimise risk and capital deployment

They're not just coders or theorists, they're the bridge between models and markets, fluent in both Python and portfolio analytics.

📊 Quant Roles Vary Across Businesses:

In India and globally, quants power strategies at:

🏦 Trading Desks: ICICI, Goldman Sachs

🧠 Prop Firms: iRageCapital, Jane Street

💼 Wealth Managers: Kotak, Bridgewater

📈 Fintechs & Data Firms: QuantInsti, Bloomberg

📲 Robo-Advisors: Groww, Wealthfront

🔧 API/Infra Developers: Alpaca, Symphony

⚖️ Regulators: SEBI, SEC

Each setup demands different strengths, from low-latency coding in HFT to macroeconomic modelling in asset management.

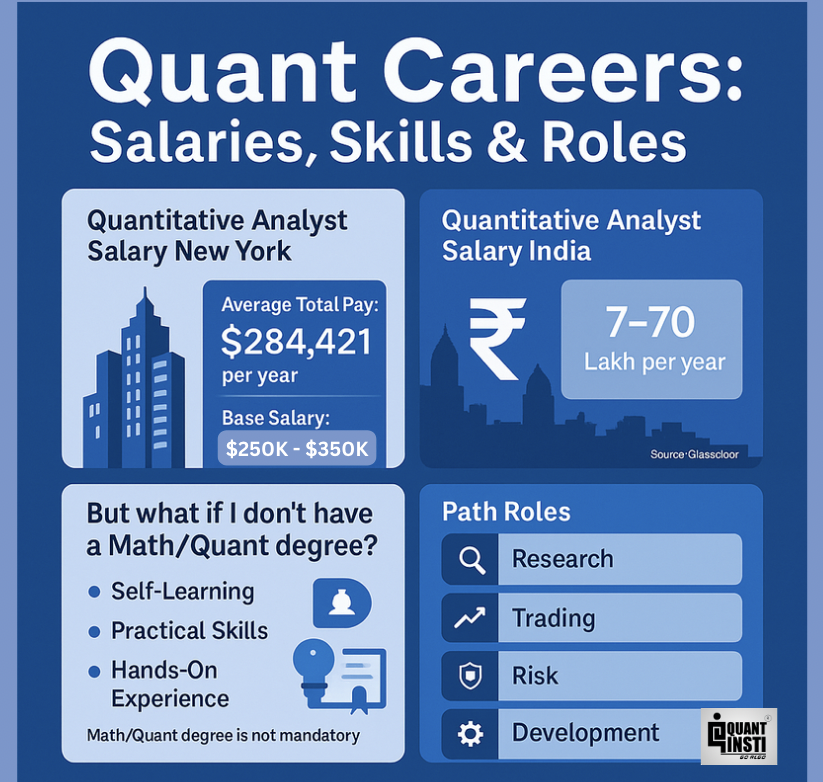

💰 What About Salaries?

In NYC, Quant Research roles at firms like Citadel offer $250K–$350K base salary

In India, salaries range from ₹7 LPA to ₹70 LPA, depending on experience and firm

🧠 Don’t Have a Math or Engineering Background?

You can still break in.

Start with:

✅ Python, statistics & financial modeling

✅ Strategy backtesting & market analysis

✅ Online programs like EPAT & Quantra for hands-on learning

✅ Projects, internships, or Kaggle-style challenges

Even without a formal quant degree, consistent learning, coding, and curiosity will take you far.

🎯 Quant Career Paths

Pre-trade: Quant Researcher

Execution: Quant Trader

Risk: Risk Analyst

Infrastructure: Quant Developer

💬 Can You Guess?

"Conduct statistical research, work on unconventional datasets, backtest models, and deploy in low-latency environments..."

(Yes, this is from a Citadel Securities job post)

🔗 Ready to explore the full quant landscape, including firms, salaries, and skills?

👉Read here: quantinsti.com/articles/quan…

#QuantitativeResearcher #QuantCareer #QuantTrading #AlgorithmicTrading #QuantJobs #MachineLearning #PythonForFinance #HighFrequencyTrading #FinancialMarkets #HedgeFunds #DataScience #FinanceCareers #EPAT #Quantra #QuantInsti #TradingCareers #Backtesting #PropTrading

4

384

24 Jun 2025

Using Python to Build End-to-End Trading Automation with MT5

Python remains the most popular language for traders ,and in our recent webinar, QuantInsti’s quant researcher Varun Pothala walked through exactly how it’s used to automate real trades using MetaTrader 5 (MT5).

In this practical session, Varun covered:

🔹 How to connect Python to the MT5 terminal

🔹 How to pull market data into a notebook

🔹 How to place, monitor, and cancel trades programmatically

🔹 Key steps to structure an automated strategy pipeline (from analysis to execution)

He also explained why Python continues to dominate quant workflows:

✅ Open source, easy to learn

✅ Huge ecosystem for data analysis & backtesting

✅ Seamless integration with brokers, platforms, and APIs

✅ Extensive support for automation, signal generation, and reporting

Whether you’re a retail trader or a professional quant, Python gives you the control and flexibility to build trading systems that scale with you.

📅 Free Webinar: First Steps into Algorithmic Trading

📆 24th June 2025 | Tuesday | 6pm

💡 Learn how industry professionals build trading careers from scratch

🎙️ Experts from BlackRock, iRage & Santander

🔗 Register: quantinsti.com/algorithmic-t…

Explore these hands-on Quantra courses:

📘 Getting Started with Algorithmic Trading : quantra.quantinsti.com/cours…

📘 Python for Trading: Basic : quantra.quantinsti.com/cours…

📘 Introduction to Machine Learning for Trading : quantra.quantinsti.com/cours…

📘 Options Trading Strategies in Python: Basic : quantra.quantinsti.com/cours…

📘 Getting Market Data: Stocks, Crypto, News : quantra.quantinsti.com/cours…

📽️ Watch the full walkthrough: youtube.com/live/H_C9P-nAuKc

#QuantInsti #PythonForFinance #TradingAutomation #MT5 #AlgoTrading #QuantTools #TradingAPIs #Backtesting #QuantResearch

1

5

337