In today's digital economy, faster verification means faster business.

Verify first. Transact confidently.

#PennyDrop #BankAccountVerification #Fintech #DigitalPayments #APIIntegration #FraudPrevention #KYC #Automation #BankingAPI #AeronPay

1

What's the biggest challenge in bank account verification today?

#PennyDrop #BankAccountVerification #Fintech #DigitalOnboarding #PaymentAutomation #FraudPrevention #BankingAPI #CustomerExperience #AeronPay

0%

Wrong account details

0%

Manual verification

0%

Fraud risk

0%

Slow onboarding

0 votes • Final results

4

A failed payment often starts with one small mistake: an unverified bank account.

Penny Drop Verification helps businesses validate account ownership before money moves, reducing fraud, minimising payment failures, and improving operational accuracy.

#DigitalPayments #AccountVerification #FintechIndia #PaymentOps #BankingAPI #FraudDetection #BusinessTechnology #FinOps #CustomerOnboarding #SecureTransactions #AutomationFirst #EnterpriseSolutions #FinancialInfrastructure #TechForBusiness #AeronPay

linkedin.com/pulse/penny-dro…

16

Every successful transaction starts with a verified bank account.

With Penny Drop (Bank Account Verification API), businesses can instantly validate account details, reduce payment failures, prevent fraud, and streamline customer onboarding, all in real time.

Faster verification. Better trust. Smarter payments.

#PennyDrop #BankAccountVerification #Fintech #DigitalOnboarding #APIIntegration #PaymentSolutions #KYC #FraudPrevention #BankingAPI #FintechIndia #Automation #AeronPay

12

10 Feb 2025

Power Up Your Business with Smart API Integration!

Seamlessly integrate our powerful APIs to enhance operations, enable secure transactions, and drive scalable growth.

Visit: nikatby.com

#BankingAPI #AEPS

#SaifAliKhan

#RanveerAllahabadia

#samayraina

#indiasgotlatent

ALT Smart API Integration

3

57

8 Feb 2025

Seamlessly integrate secure and scalable APIs to enhance transactions, automate processes, and expand your business.

📩 Enquiries: enquiry@nikatby.com

🌐 Visit: nikatby.com

#BankingAPI #AEPS #PlayStationNetworkDown

#DelhiElectionResults

#dhruvrathee

#KaranKundrra

5

279

4 Feb 2025

TAKE TIME TO LEARN ABOUT BANKING APIS AND PI NETWORK WHEN OPEN NETWORK LAUNCHES

When Pi Network enters the Open Network phase, the digital financial ecosystem could witness a major transformation with the integration of banking APIs to facilitate Pi transactions. Below are the potential impacts and integration possibilities of banking APIs with Pi Network in the global digital financial landscape.

1. CONNECTING PI NETWORK WITH THE TRADITIONAL FINANCIAL SYSTEM

Currently, banks use Open Banking APIs to connect with fintech platforms and e-wallets like MoMo and VNPay. If Pi Network gains support, banking APIs could enable:

Direct conversion of Pi into fiat currency from the Pi Wallet via banking systems.

Integration of Pi with e-wallets such as ZaloPay and MoMo, making transactions more convenient.

Providing digital financial services, such as using Pi as collateral for loans or staking Pi to earn interest.

2. PAYMENT SYSTEMS USING PI VIA BANKING APIS

Banking APIs could support Pi payments in various scenarios:

Stores accepting Pi: If banks integrate APIs with QR code payment networks (VNPay, Payoo, etc.), users could easily pay with Pi.

E-commerce platforms: Shopee, Tiki, or Lazada could use APIs to support Pi payments via intermediary banks.

Interbank transfers: If major banks like Vietcombank or Techcombank support Pi transactions via API, users could transfer Pi between bank accounts seamlessly.

3. OPEN NETWORK AND EXPANDING THE BLOCKCHAIN ECOSYSTEM

Many global banks have adopted Blockchain APIs to facilitate faster cross-border transactions. When Pi Network enters the Open Network phase, several possibilities could emerge:

Banks may provide APIs to accept Pi as a digital asset within traditional financial systems.

Financial institutions could use Pi for international payments through bank APIs and decentralized exchanges.

Blockchain API integration could support DeFi (Decentralized Finance), enabling Pi staking, lending, and borrowing.

4. CHALLENGES OF INTEGRATING BANKING APIS WITH PI NETWORK

Despite its potential, integrating Pi Network with banking APIs faces significant challenges:

Regulatory hurdles: Some countries have yet to recognize Pi as a legally tradable asset within banking systems.

Legacy financial system integration: Banks still rely on SWIFT, so API integration for Pi may take time.

Security and KYC compliance: Banks will require robust APIs to ensure Pi Network’s KYC (Know Your Customer) meets international financial standards.

5. FUTURE PROSPECTS: WILL PI NETWORK DEVELOP ITS OWN BANKING API?

A fascinating prospect is that Pi Network could develop its own Pi Banking API, allowing:

Direct connection of Pi Wallet with bank accounts.

Conversion of Pi into fiat or other digital assets via API.

Integration with POS (Point-of-Sale) systems for real-world payments.

If Pi Network gains widespread adoption upon Open Network launch, it could become part of the global banking API ecosystem, promoting seamless and secure crypto payments.

CONCLUSION

Banking APIs and Pi Network could revolutionize digital finance if integrated effectively. When Pi enters the Open Network phase, leveraging APIs for payments, transactions, and investments could help Pi become a widely accepted payment asset in the future.

#Tags: #PiNetwork #BankingAPI #OpenBanking #Fintech #Blockchain #FinancialTechnology #OpenNetwork

5

51

184

6,573

4 Feb 2025

TAKE TIME TO LEARN ABOUT BANKING APIS AND PI NETWORK WHEN OPEN NETWORK LAUNCHES

When Pi Network enters the Open Network phase, the digital financial ecosystem could witness a major transformation with the integration of banking APIs to facilitate Pi transactions. Below are the potential impacts and integration possibilities of banking APIs with Pi Network in the global digital financial landscape.

1. CONNECTING PI NETWORK WITH THE TRADITIONAL FINANCIAL SYSTEM

Currently, banks use Open Banking APIs to connect with fintech platforms and e-wallets like MoMo and VNPay. If Pi Network gains support, banking APIs could enable:

Direct conversion of Pi into fiat currency from the Pi Wallet via banking systems.

Integration of Pi with e-wallets such as ZaloPay and MoMo, making transactions more convenient.

Providing digital financial services, such as using Pi as collateral for loans or staking Pi to earn interest.

2. PAYMENT SYSTEMS USING PI VIA BANKING APIS

Banking APIs could support Pi payments in various scenarios:

Stores accepting Pi: If banks integrate APIs with QR code payment networks (VNPay, Payoo, etc.), users could easily pay with Pi.

E-commerce platforms: Shopee, Tiki, or Lazada could use APIs to support Pi payments via intermediary banks.

Interbank transfers: If major banks like Vietcombank or Techcombank support Pi transactions via API, users could transfer Pi between bank accounts seamlessly.

3. OPEN NETWORK AND EXPANDING THE BLOCKCHAIN ECOSYSTEM

Many global banks have adopted Blockchain APIs to facilitate faster cross-border transactions. When Pi Network enters the Open Network phase, several possibilities could emerge:

Banks may provide APIs to accept Pi as a digital asset within traditional financial systems.

Financial institutions could use Pi for international payments through bank APIs and decentralized exchanges.

Blockchain API integration could support DeFi (Decentralized Finance), enabling Pi staking, lending, and borrowing.

4. CHALLENGES OF INTEGRATING BANKING APIS WITH PI NETWORK

Despite its potential, integrating Pi Network with banking APIs faces significant challenges:

Regulatory hurdles: Some countries have yet to recognize Pi as a legally tradable asset within banking systems.

Legacy financial system integration: Banks still rely on SWIFT, so API integration for Pi may take time.

Security and KYC compliance: Banks will require robust APIs to ensure Pi Network’s KYC (Know Your Customer) meets international financial standards.

5. FUTURE PROSPECTS: WILL PI NETWORK DEVELOP ITS OWN BANKING API?

A fascinating prospect is that Pi Network could develop its own Pi Banking API, allowing:

Direct connection of Pi Wallet with bank accounts.

Conversion of Pi into fiat or other digital assets via API.

Integration with POS (Point-of-Sale) systems for real-world payments.

If Pi Network gains widespread adoption upon Open Network launch, it could become part of the global banking API ecosystem, promoting seamless and secure crypto payments.

CONCLUSION

Banking APIs and Pi Network could revolutionize digital finance if integrated effectively. When Pi enters the Open Network phase, leveraging APIs for payments, transactions, and investments could help Pi become a widely accepted payment asset in the future.

#Tags: #PiNetwork #BankingAPI #OpenBanking #Fintech #Blockchain #FinancialTechnology #OpenNetwork

6

28

136

6,992

8 Jul 2024

The widespread adoption of APIs and Banking-as-a-Service (BaaS) marks a shift in the banking sector, promising a future of enhanced connectivity, efficiency, and innovation.

#bankingapi #fintech #bankingasaservice

1

31

19 Jun 2024

Free global banking. And free coffee. Only at the Truly Financial booth.

#Collision #CollisionConference #BankOnTruly #GlobalBanking #BankingAPI

19 Jun 2024

Come meet us at Booth hashtag#E252, Ontario Pavilion at Collision today, anytime between 9 a.m. to 5 p.m., or email us at collision@trulyfinancial.com to meet us any day.

#TrulyFinancial #Fintech #CollisionConference #BankingWithoutBorders #TrulyGlobal

1

1

4

134

24 May 2023

A Bank #AccountVerification API is used to locate and verify a valid bank account with the IFSC code and client bank account number. Using a Pinwallet #bankingAPI can help remove manual errors when payouts are sent to verified accounts by starting with bulk account verification.

ALT Account verification API

39

15 Apr 2023

APIs are Revolutionizing the Banking Sector!! 📷 📷

Our State-of-the-Art Technology is creating New Avenues for Smooth Financial Transactions and Advancements in Banking Services. Visit: pinwallet.in/

#pinwallet #pinwalletpayment #bankingapi #fintechapi #API

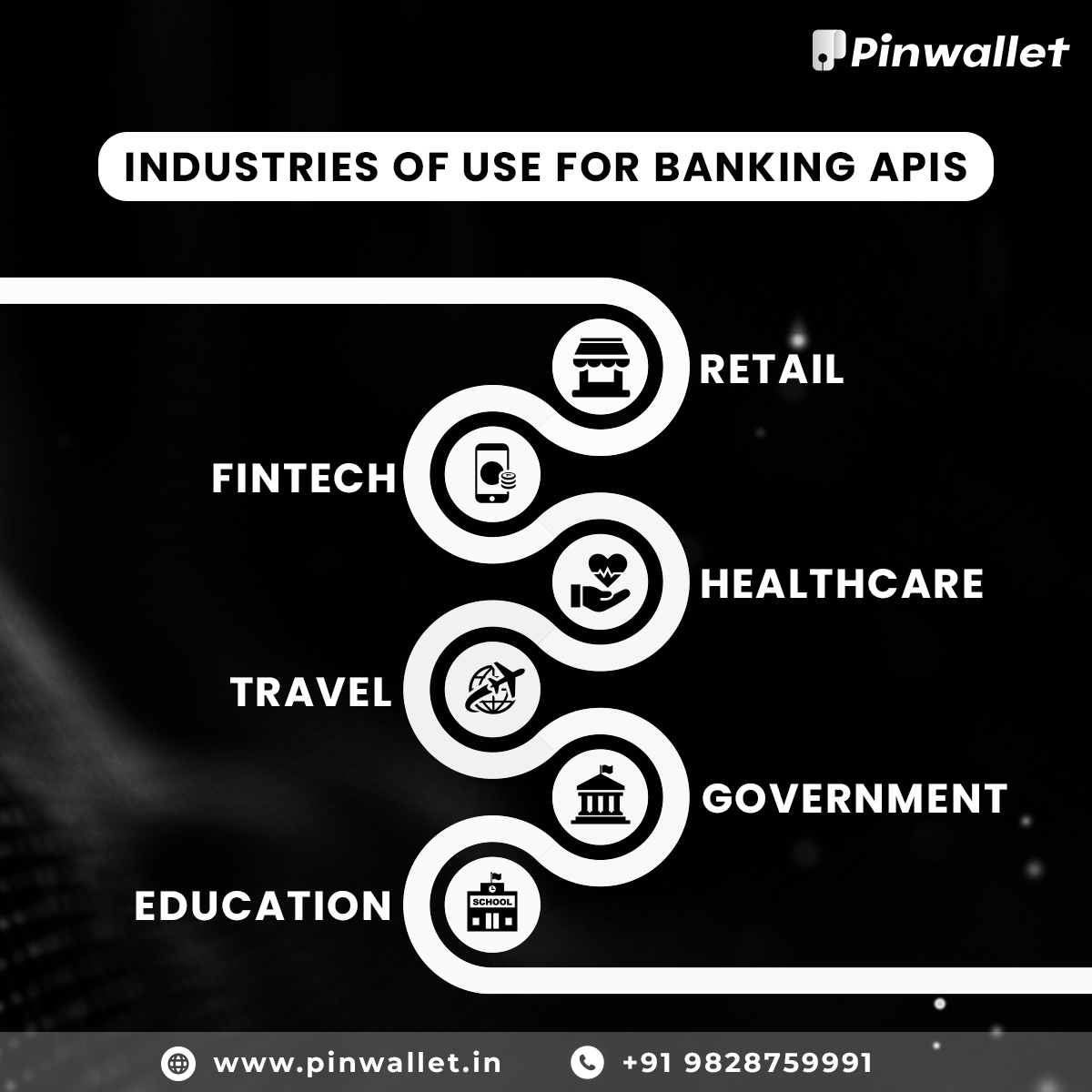

ALT Industries that needs banking API

1

11

20 Feb 2023

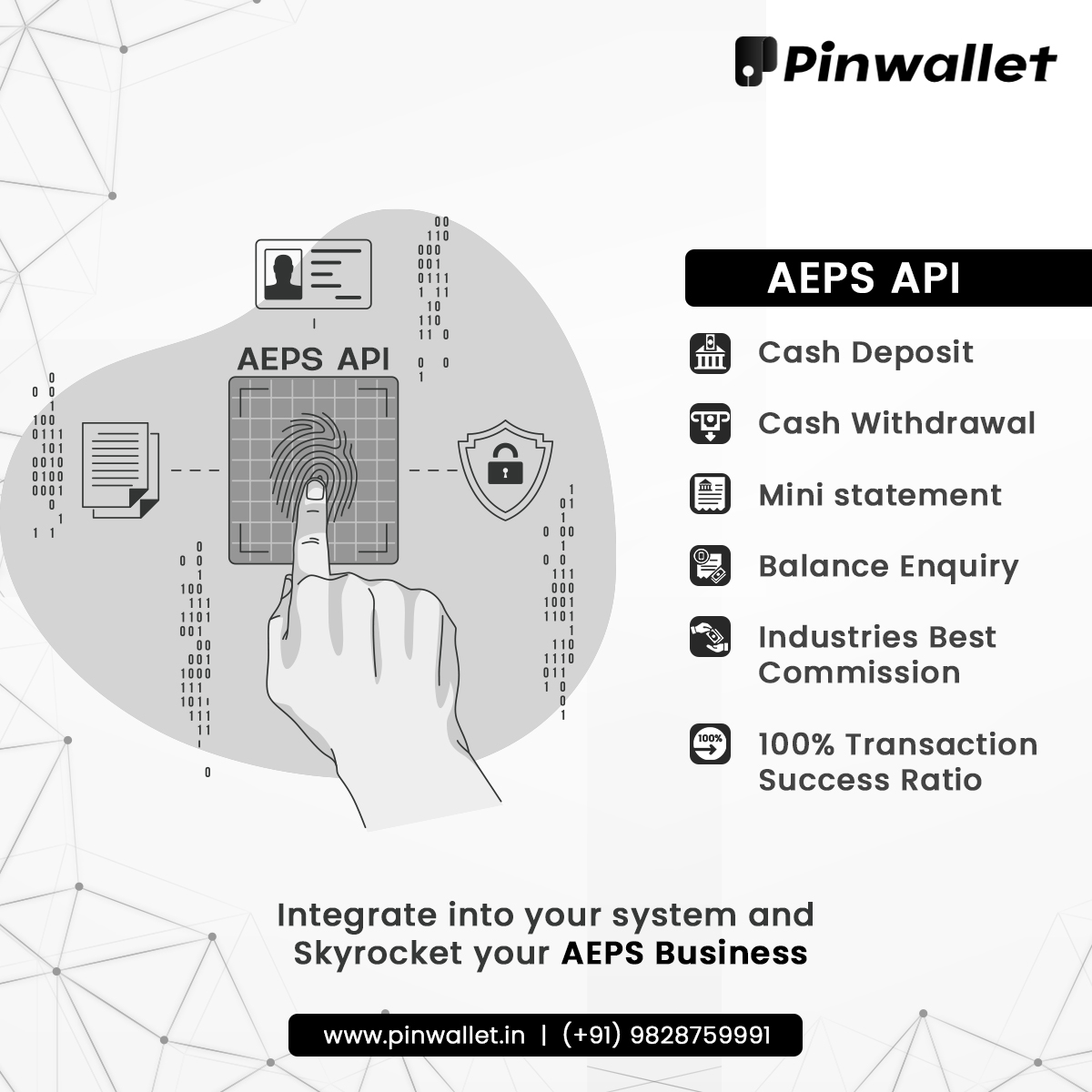

Empower your business with our AEPS API! With seamless integration and secure transactions, you can provide your customers with a hassle-free banking experience. pinwallet.in/

#pinwallet #pinwalletpayments #API #fintechapi #aepsapi #bankingapi #openbankingapi

ALT India's top aeps api provider company

2

18

1 Dec 2022

Hurry Up Fintech #Sales #Discountoffer closes #soon.

Justforpay is your #onestopsolution for all your #Banking needs! 🤩

B2B Portal & API> justforpay.co.in

91 8882171675

#NexGenBanking #BankingAPI #APIbanking #API #APIservices #APIprovider #APIcompany #Banking #KYCWallet

1

18 Oct 2022

With the emergence of the API economy during the past 10 years, we have witnessed a significant transformation in everyday banking.

Here, we have mentioned three types of bank APIs and how it is helping all of us

#winsoft #winsoftechnologies #API #APIintegration #bankingAPI

1

3

Get a one-stop b2b API solution for Travel, Banking and Payment. Visit: bit.ly/3BDIZFg

#ezulix

#apiservices

#API #fintech #fintechapi #bankingapi #aepsapi #rechargeapi #moneytransferapi #aadhaarpayapi #bbpsapi #payoutapi #busbookingapi #travelapi #hotelbookingapi

ALT best b2b api solution for banking, payment and travel services

2

@Forbes_DACH article on @OpenWealthAPI -

We are proud to be part of the association.

hubs.ly/H0P8bgy0

#weopenbanking #openwealth #openapi #bankingapi

2

7 Apr 2021

Hallo Karl, die Firma @finapi bietet eine #BankingAPI an. Bei Bedarf kannst Du auch die App von @zuperbank oder @Outbank nutzen, somit hast Du Zugriff auf alle deine Konten. @ingdiba betreibt u.a. ein Developer Portal bit.ly/3wC3T2Q

2

25 Jan 2021

1

1

2

8 Sep 2020

@newgensoftware Integrates with @Celero #Xchange to Deliver Scalable #Lending Solutions to #CreditUnions. #digitallending #Canada #Integrationstrategy #bankingapi celero.ca/news/celero-news/2…

1