David retweeted

Jun 13

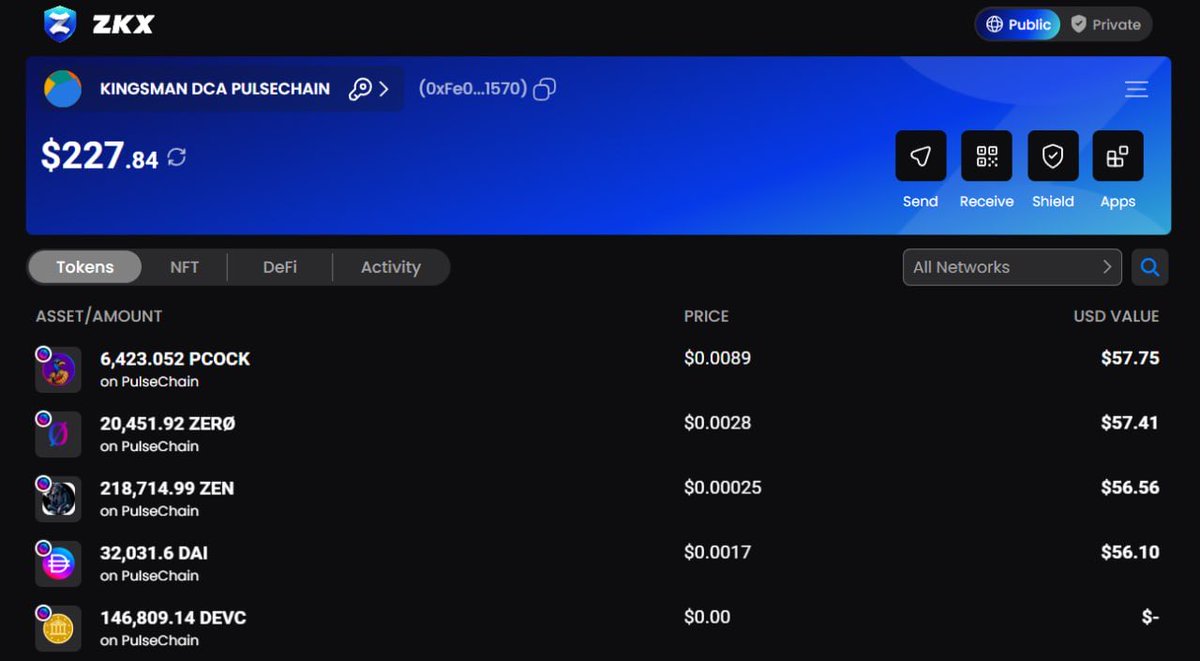

ADDING ANOTHER $100 TO MY PUBLIC DCA ON PULSECHAIN ⚡

$20 INTO EACH COIN :

$PCOCK

$ZERO

$ZEN

$DEVC

$pDAI

TOTAL PUBLIC DCA: $300 💰

THE JOURNEY TO GLORY CONTINUES.

POWERED BY @LibertySwapFi AND @zkxwallet 🚀

WALLET :

0xFe04A5F0E3C76bEC68C734e46e2610aB865F1570

CONSISTENCY. CONVICTION. PULSECHAIN. ⚡👑

Jun 7

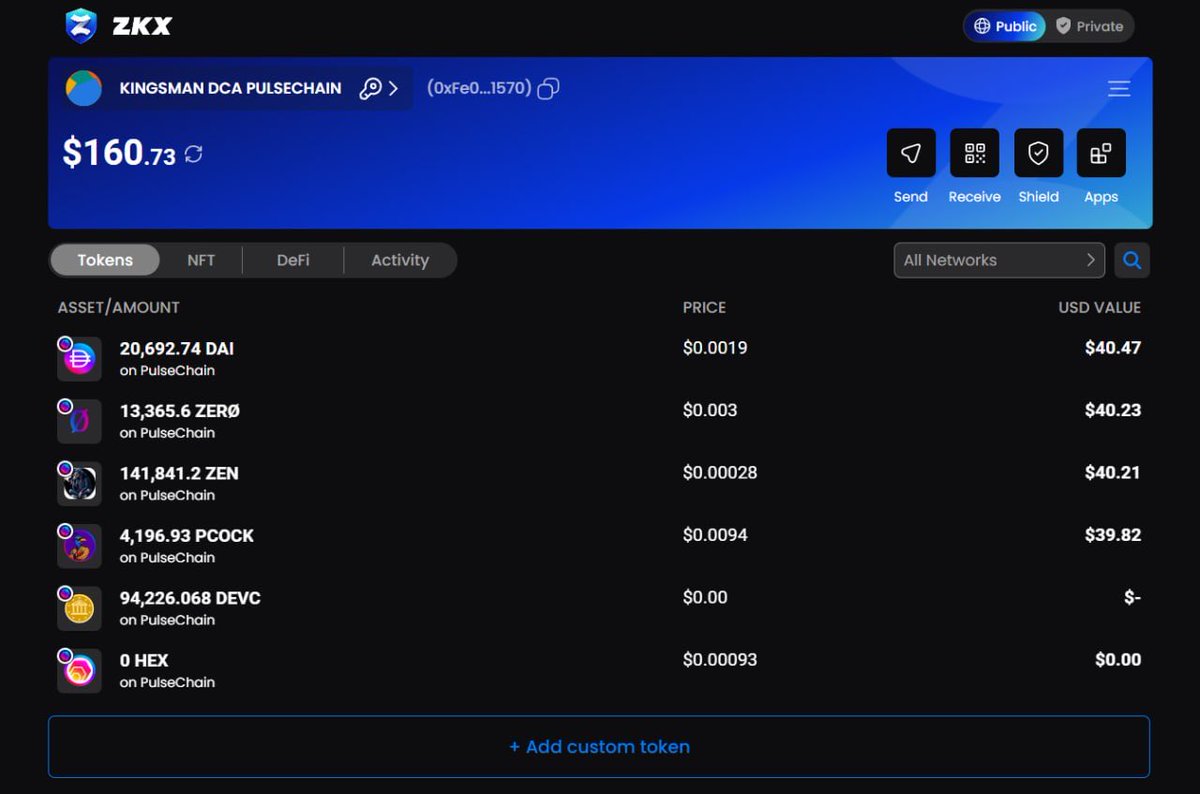

MY FIRST PUBLIC DCA ON PULSECHAIN STARTS TODAY WITH $200 ⚡

LET THE JOURNEY TO GLORY BEGIN.

POWERED BY @LibertySwapFi AND @zkxwallet 🚀

WALLET :

0xFe04A5F0E3C76bEC68C734e46e2610aB865F1570

TOKENS :

$PCOCK $ZERO $ZEN $DEVC $pDAI

5

6

93

1,948

Marissa, não é pq eu reclamei devc que eu queria que vc tivesse morrido 😕

182

Jun 9

Very nicely written, Tanisha, esp the point that notes are a way to force yourself to have an opinion.

In fact, at DeVC/Z47, everyone is required to write down reflections & an overall rating decision basis each meeting with a founder

It is a very good habit to have 👍

1

8

1,164

Jun 8

$pzen just got a godly candle ... after a few months of red candles and been out for 2 years ... We got better tokenomics , better game theory and more products about to launch ... everything we launch is innovative . new ... different. Not a meme coin or another copy cat.

$pmint $pdai $pfly $plsx $hex $pcock $solidx $doubt $steth $upx $loan $most $zero $devc $emit $plsb $tophat $finvesta

1

2

10

328

Jun 7

MY FIRST PUBLIC DCA ON PULSECHAIN STARTS TODAY WITH $200 ⚡

LET THE JOURNEY TO GLORY BEGIN.

POWERED BY @LibertySwapFi AND @zkxwallet 🚀

WALLET :

0xFe04A5F0E3C76bEC68C734e46e2610aB865F1570

TOKENS :

$PCOCK $ZERO $ZEN $DEVC $pDAI

Jun 2

12

27

196

8,773

🚀 Riverline is hiring AI Engineers!

Built by founders from IIT Madras, CMU & Navi and backed by South Park Commons, GradCapital & DeVC.

Work on:

🤖 AI Products

🧠 LLMs

⚡ Automation

📈 Fintech Innovation

Apply:

riverline.notion.site/ai-eng…

1

83

Jun 5

12 Sep 2025

You have to understand why

(Pump . tires) was created, it’s because core holders does not fully complete a blockchain ecosystem, it must be equally distributed between many things, I’ve said before memes will run first, I stand on that & a $1 $pDAI. ⚔️🛡️

$pDAI IS $1. 💥⚡️🚀🌕

1

1

34

591

Jun 2

Starting June 1st, 2026, I’ve decided to begin my DCA journey with the PulseChain Community, inspired by my good friend @10dollarsdream. 🚀

I’ll be DCA’ing $100 every Friday into 5 tokens on PulseChain:

$20 $PCOCK 🦚

$20 $ZERO Ø

$20 $ZEN 🧘

$20 $DEVC 🕵️♂️

$20 $pDAI 💵

Let the journey begin… ⚡️

25

13

151

10,595

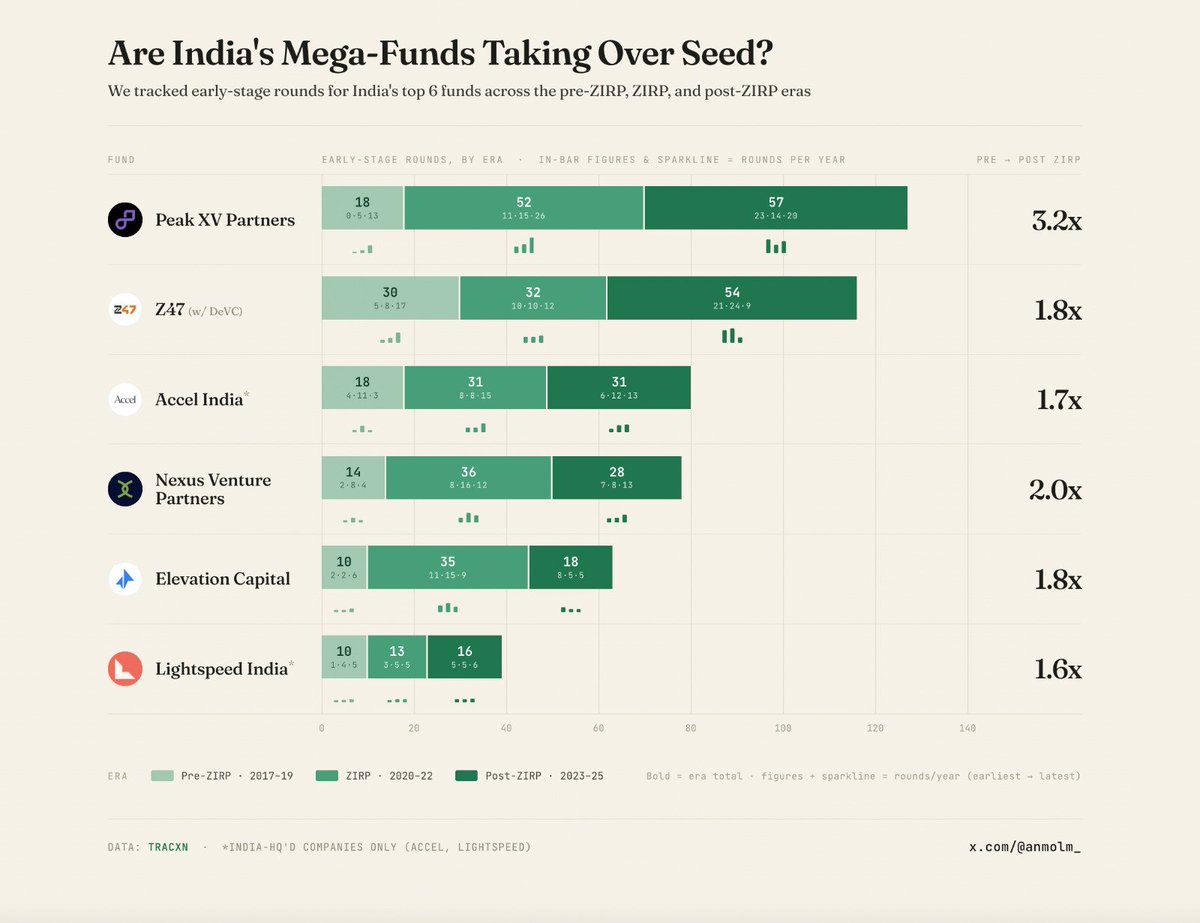

May 30

got nerdsniped into looking into this for india. wanted to see what PANZEL's impact on seed has been (all data ty to @Tracxn) across the last decade, some observations:

- most multi-stage firms didn't have seed programs in india in the pre-zirp era as they were largely series a investors and india's seed landscape was also fairly small. peak stared their seed program, surge, in 2019.

- during zirp (2020 - 2022), most multi-stage firms piled into seed and this period is when most PANZEL firms invested in the highest number of companies in a single calendar year. some firms started their own seed programs i.e Accel with Atoms (2021) & Matrix with DeVC (2022)

- post-zirp firms have re-adjusted their strategies with some firms paring down seed investments while seed is still more important to the firms than the pre-zirp era; while other firms have kept consistently backing the same or even more companies at the seed stage - these firms typically do have specialized products for companies at the seed stage or an investment team that skews to investing in the inception stage

- it is yet to be seen if winning at seed = helping these firms win at A / B and beyond or if specialized seed programs help firms in ways other than access (perhaps a future post)

couple of caveats:

- only india hq'd cos included for accel & lightspeed (was hard to distinguish b/w indian fund & american fund for cos hq'd elsewhere)

- z47 cos do include some (but not all) devc companies given how tracxn classifies the entities of two firms

May 29

Are mega-funds really taking over seed?

I decided to look at the behavior of the world's largest VC funds ($10B AUM) at early stages and answer a simple question: should EMs worry about their structural edge?

So I used @harmonic_ai and looked at all pre-seed, seed, and seed extension rounds across 3 eras:

- SaaS Era (2015–2019): 5 years of a normal market. Cloud, SaaS, fintech were the dominant theses.

- ZIRP Era (2020–2022): 3 years of zero interest rates and free capital.

- AI Era (2023–2026): from ChatGPT to the present day.

We focused on one core metric: average number of early-stage deals per year for each fund in each era.

Here are a few insights we found interesting:

1/ In the SaaS era, a typical mega-fund made 10–20 early-stage deals per year. This was moderate, targeted seed activity – a complement to the core Series A/B and later strategy.

2/ In the ZIRP era, everyone scaled up. Each of the 10 funds increased their early-stage deals/year (some by 2–3x), because capital was free, competition at later stages was fierce, and seed felt like a cheap entry point.

3/ Then came the AI era and it became clear this was no temporary effect. Even as rates rose and capital became more expensive with the end of ZIRP, @a16z and @generalcatalyst posted peak early-stage activity.

> @a16z: 16.6 → 48.7 → 75.3 deals/year. A 4x increase from the SaaS era.

> @generalcatalyst: 15.2 → 31.7 → 61.5 deals/year. Also 4x.

The most interesting finding, though, is 3 distinct behavioral models:

1/ "Accelerators" - deals/year in the AI era exceed ZIRP levels: @a16z (75.3/yr), @generalcatalyst (61.5/yr), @khoslaventures (31.5/yr). These funds didn't just stay active in seed after free money ended – they doubled down.

2/ "Stabilizers" – deals/year in the AI era are slightly below ZIRP peak, but well above SaaS-era levels: @sequoia (19.6 → 49.3 → 50.6), @Accel (15.2 → 43.3 → 34.7), @lightspeedvp (11.6 → 41.7 → 32.1). The ZIRP spike moderated, but activity levels remain sustainably 2–3x above the SaaS era. There's no return to the old normal.

3/ "Disciplined" – steady, gradual growth across all eras: @BessemerVP (9.4 → 23.0 → 20.9), @Lux_Capital (7.2 → 14.3 → 14.7), @IndexVentures (10.0 → 23.3 → 17.6). No ZIRP spikes, no AI explosions – but the baseline has durably shifted upward.

So in the SaaS era, these 10 funds collectively made roughly 140–150 early-stage deals per year. In the AI era – around 370–400. And I think they just set up a new, sustained baseline, not just doubled after a ZIRP-peak era.

For an LP evaluating an emerging seed manager, this is the most important context.

The early-stage market your GP is investing in is one where 10 funds with $10B in AUM are doing dozens deals a year.

An emerging manager needs to be able to articulate exactly where, in that market, they have the right to win.

3

1

31

5,319

May 29

AI concierge startups are becoming a rage. From kitchens getting automated to prompting someone to queue up at restaurants for them, the use cases are vast. One such app, Hulp, is already discussing a $4-6 million round w Sparrow and DeVC, sources to @chandrarsrikant and me.

2

5

44

10,292