African Proverb retweeted

DON'T IGNORE THIS ⚠🚨

X ALGORITHM MARKED MY ACCOUNT SPAM AND MY FOLLOWERS AS BOT !!

DROP A COMMENT TO BREAK THE ALGORITHM

REPLY WITH A DOT, CAN YOU SEE THIS POST ?

304

326

687

6,034

OLUMIDE retweeted

Ronaldo’s 41, had no service all game and was constantly marked by 3–4 defenders, yet he gets the blame while a midfield that created nothing gets a pass. Casuals everywhere.

101

987

8,707

97,903

Not a bad idea. One should send mail to Commissioner Secretary Tourism so that application is marked to sub ordinate offices.

Comrade Héctor 🇵🇸🪂 retweeted

11h

But .. but .. I marked your words ☹️

The blockade is already gone.

36

400

3,502

70,002

How do you compound defensive bodies if you don't perceive an attacking threat in the box, we all watched that game maybe you didn't, Ronaldo alone was marked by 2 defenders.

2

1/2 📸 #InPictures

Yesterday, JF Kapnek Zimbabwe marked #WellnessWednesday with activities designed to encourage connection, teamwork, and positive engagement. By prioritising employee wellbeing, we continue to cultivate a healthy and inclusive workplace culture where everyone..

1

2

The defenders were always watching him as they should. Even if there was no special plan he was still marked heavily in counter attacks and set pieces

59

'In February 1637, at a routine auction, buyers simply stopped showing up to pay the exorbitantly inflated prices. The market abruptly collapsed, and prices fell to just a tiny fraction of their peak value within a few weeks.'

The tulip collapse was not a fundamental repricing. It was a liquidity event. The asset did not change. The marginal buyer disappeared. What looked like a store of value was revealed, overnight, to be a market of one direction with no depth on the other side.

Krishnam's central observation in Market Tremors is that every major dislocation in recorded market history shares this architecture.

Price is not discovered in equilibrium @TrustlessState. It is discovered at the margin, and the margin is always thinner than the chart suggests. The 1929 margin calls, the 1987 program selling cascade, the 2008 repo freeze: each began not with a fundamental deterioration but with the sudden absence of a bid.

The asset was the same asset it was the day before. The clearing mechanism was not.

This is why metrics built on marked assets are structurally incomplete.

They measure the numerator at the last traded price. They have no opinion on what that price becomes when the auction room empties.

The structural answer is not to avoid exposure. It is to own the convexity that pays when the room empties. Long volatility is not a hedge in the portfolio insurance sense. It is the only instrument that is explicitly long the gap between quoted price and clearing price.

Tulips were not a story about greed. They were a story about what happens to any asset when the bid is structural rather than fundamental.

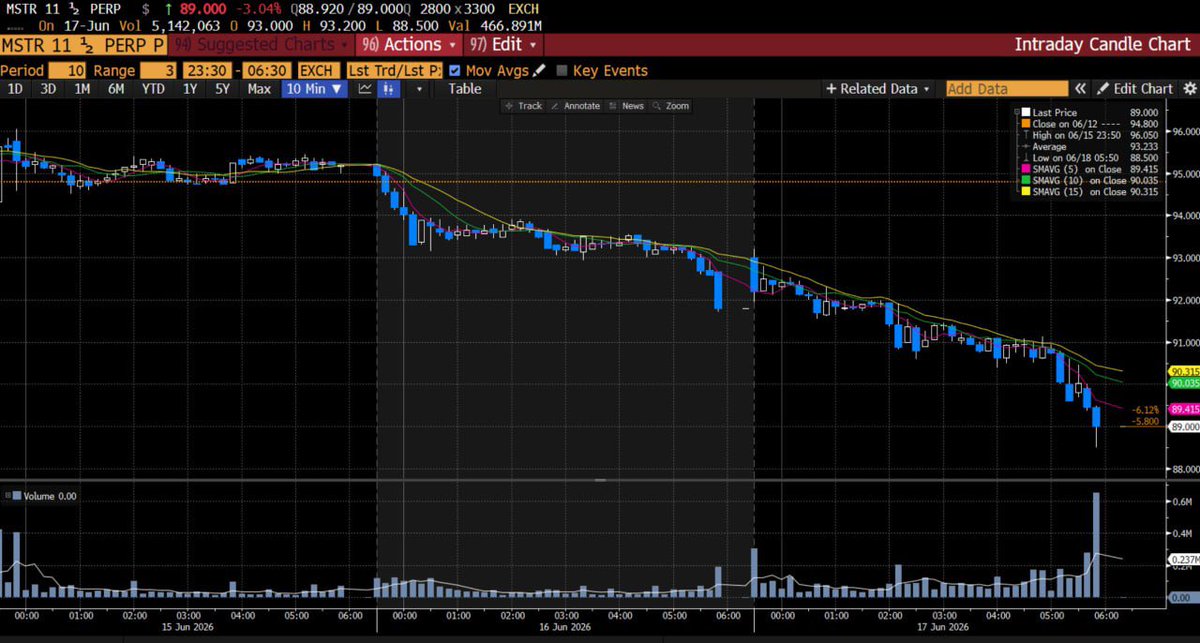

Fade D2 at your own risk. 30 straight positive months.

steady lads

• 32yr of dividend coverage on an asset that yields you zero.

• coverage paid by the ATM, not the stack. At 115 $MSTR ?

• the 11⅛ pref at 89 has no bid, I love you

• "volatility is vitality" until the pref needs a bid

shock absorber, or Su Zhu special?

what's your read on @saylor?

1

1

34

The Palace of Versailles has been the stage for some of history's most globally significant diplomatic and political signing ceremonies. Because of its grand symbolism, it remains a premier location for modern geopolitical agreements and historic state visits.

Easily the most famous ceremony at the palace, the signing of this peace treaty on June 28, 1919, formally ended the state of war between Germany and the Allied Powers following World War I.

The event marked a dramatic shift in global politics.

WARNING: FLASHING IMAGES

A video shared by the White House shows President Trump signing the Iran memorandum of understanding at the Palace of Versailles, just prior to a dinner hosted by French President Emmanuel Macron reut.rs/44kWeHW

6

🍰 ⁞ Tracksuit Johann 🍬🍭🍫 retweeted

I'm trading some stuff rn... ones marked with red hearts are just looking for offers, might not trade a spe ific trade i'm lf

1

4

201

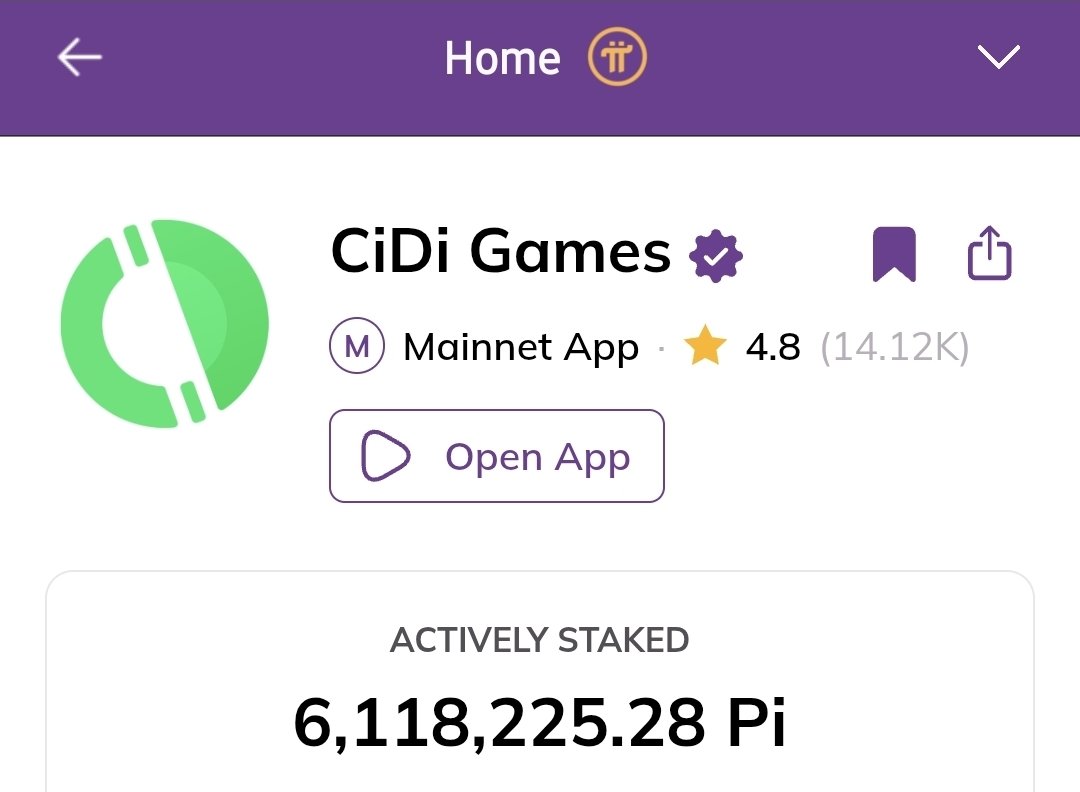

🚨 @PlayCiDi Has Officially Earned the Verified App Badge! ✅💜

CiDi Games has now been marked as a Verified App in the Pi Browser, confirming that it is a Mainnet application using real Pi and has been approved by the Pi Core Team.

With a strong 4.8⭐ rating and over 14,000 reviews, CiDi Games continues to stand out as one of the leading gaming applications in the Pi ecosystem.

This is another positive signal that the Pi ecosystem is expanding, with more real-use Mainnet applications receiving official verification. 🚀🎮

#PiNetwork #CiDiGames #VerifiedApp #PiBrowser #PiEcosystem #MainnetApps

6

9

108

2,844