Jun 9

not sure about true hypescaler leverage, agree their not primary baggie. brin & page said worth bankrupting google to do but they can break contracts. necloud backers then litigating for penalties. at real scale, PC/PE would be in trouble, which metastasizes into the BSL issue

1

171

May 21

On the early side of their earnings growth, so their valuations don't look good yet, but these are 2 and 4-billion-dollar companies, so a hyperscaler contract could yield a 10x $TE and $CLSK. TE is at the cross-section of American onshoring of clean solar energy and data centers. $CLSK is Clean Spark most people know that one it's a 4 billion dollar company so it could 10x were it to become a necloud. Yes I'm following Leopold. would throw $BE in the same bucket except it's already an $85 B MK

3

6

4,346

May 18

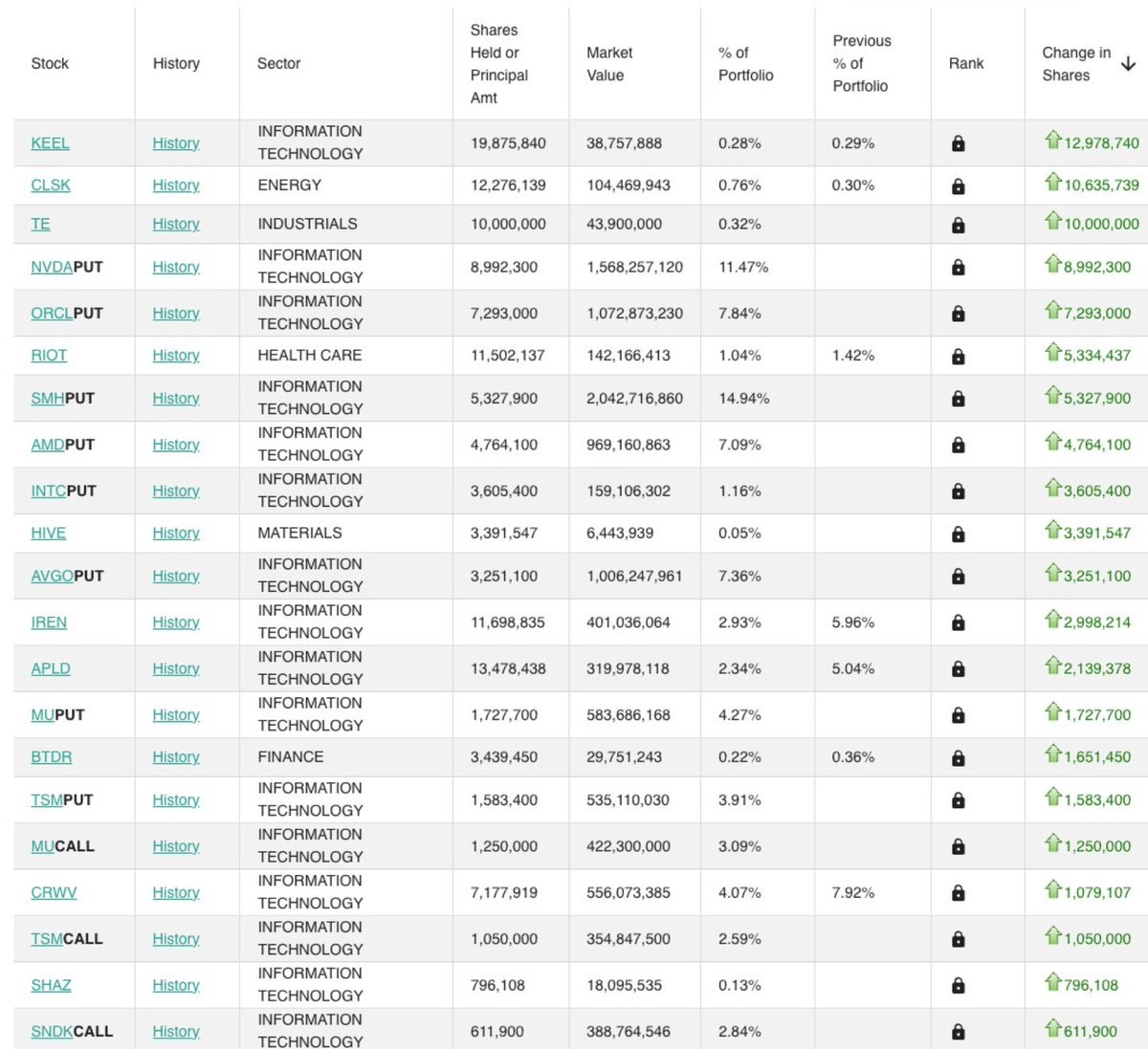

$340 milyon doları $2.5 milyar dolara katlayan LEOPOLD yeni portföyünü paylaştı.

Smallcap olarak $HIVE ve $SHAZ ikilisini ekledi. Bütün pozisyon eklemeleri, hisse artırımları ve çıkarmalar aşağıda.

$HIVE Kanada'da 3.5 Milyar dolarlık dev yatırım açıkladı. Eski bir bitcoin madenciliği şirketi, yapay zeka ve yüksek performanslı bilgi işlem alanlarına hızla yöneliyor. Piyasa değeri yaklaşık 581 milyon dolar. Kanada, İsveç ve Paraguay'da yeşil enerjiyle çalışan veri merkezleri işletiyor, yıllık bazda )0 hash oranı büyümesi kaydetti ve küresel Bitcoin ağının %2'sinden fazlasına sahip. Paraguay'da BUZZ adında özel olarak tasarlanmış bir yapay zeka bulut platformu başlattı ve Nisan ayında yapay zeka ve veri merkezi genişlemesi için 75 milyon dolar tutarında değiştirilebilir tahvil fonu topladı.

$SHAZ ise Avusturyalı necloud ve GPU cloud alanında faaliyet gösteriyor. Piyasa değeri yaklaşık 897 milyon dolar. Şubat 2026'da NASDAQ'da 30 dolardan halka arz edildi ve Oaktree ve Two Seas liderliğinde 125 milyon dolar topladı. İlk çeyrek verileri, toplam sözleşme değerinin 2,2 milyar doların üzerinde olduğunu ve 2026'da en az 470 milyon dolarlık bir gelir hedefi olduğunu gösterdi. 1,25 milyar dolarlık beş yıllık ESDS anlaşması ve 950 milyon dolarlık beş yıllık Asya Pasifik sözleşmesiyle desteklenen şirket, her iki anlaşmanın da 2026'nın 3. ve 4. çeyreklerinde devreye girmesini hedefliyor. Kapasite hedefi 2026 ve 2027 başları için 70 MW'tan 100 MW'a yükseltildi. GPU tedariki için 350 milyon dolarlık dönüştürülebilir tahvil fonu toplandı.

$878.7M of Bloom Energy $BE

$724.4M of Sandisk $SNDK

$556.1M of CoreWeave $CRWV

$401M of Iren Limited $IREN

$389.1M of Core Scientific $CORZ

$320M of Applied Digital $APLD

$142.2M of Riot Platforms $RIOT

$104.5M of Cleanspark $CLSK

$62.5M of Solaris $SEI

$43.9M of T1 Energy $TE

$38.8M of Bitfarms $29.8M of Bitdeer $BTDR

$26.3M of Power Solution $PSIX

$21M of Corning $GLW

$20.9M of WhiteFiber $WYFI

$20.2M of $AMD

$19.9M of Babcock and Wilcox $BW

$18.1M of SharonAI $SHAZ

$13.1M of Propetro $PUMP

$10.3M of $SMH

$8.9M of Intel $INTC

$7.6M of Taiwan Semi $TSM

$6.4M of Hive Digital $HIVE

$6.1M of $ASML

$5.9M of Micron $MU

Pozisyon kapatımları:

$COHR, $LBRT, $TSEM, $HUT, $LITE, $KRC

23

33

201

34,725

May 13

Necloud最大的风险其实一直都是执行力,比如能不能拿到电力,土地,客户,和高效利用资金。

这份几乎完美的财报大概率会让更多资金重新评估 $NBIS ,并从 $CRWV / $IREN 等同板块公司中流向它。

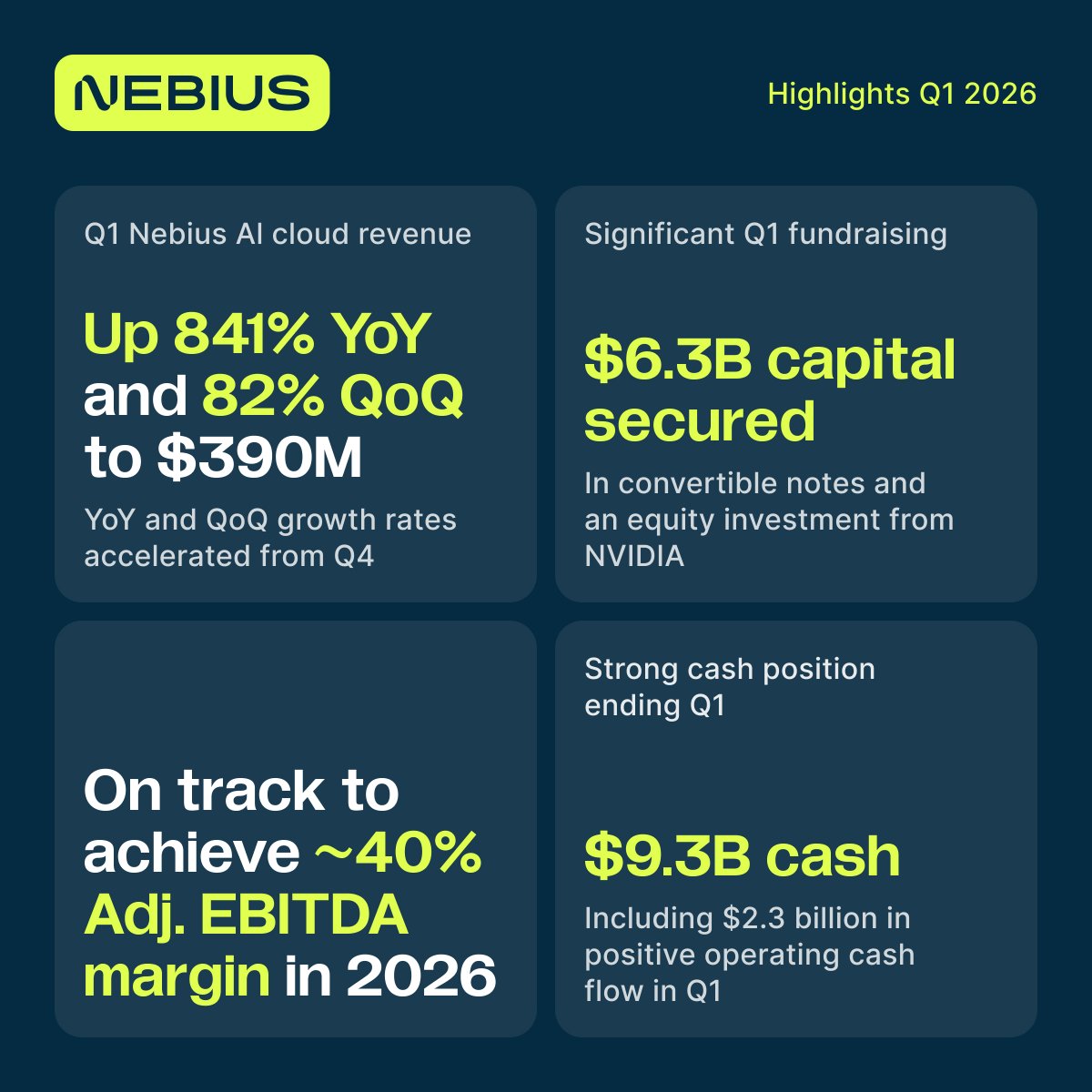

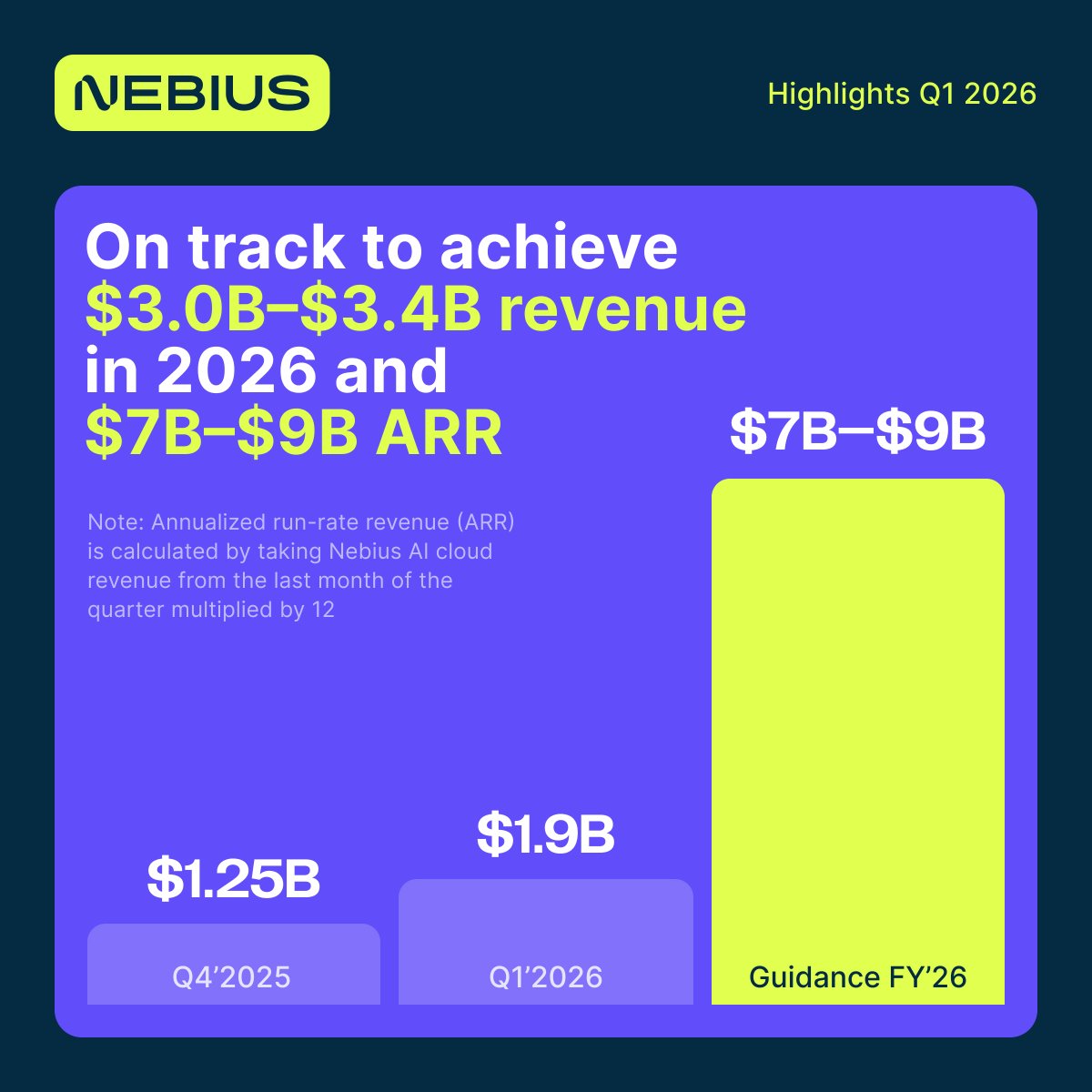

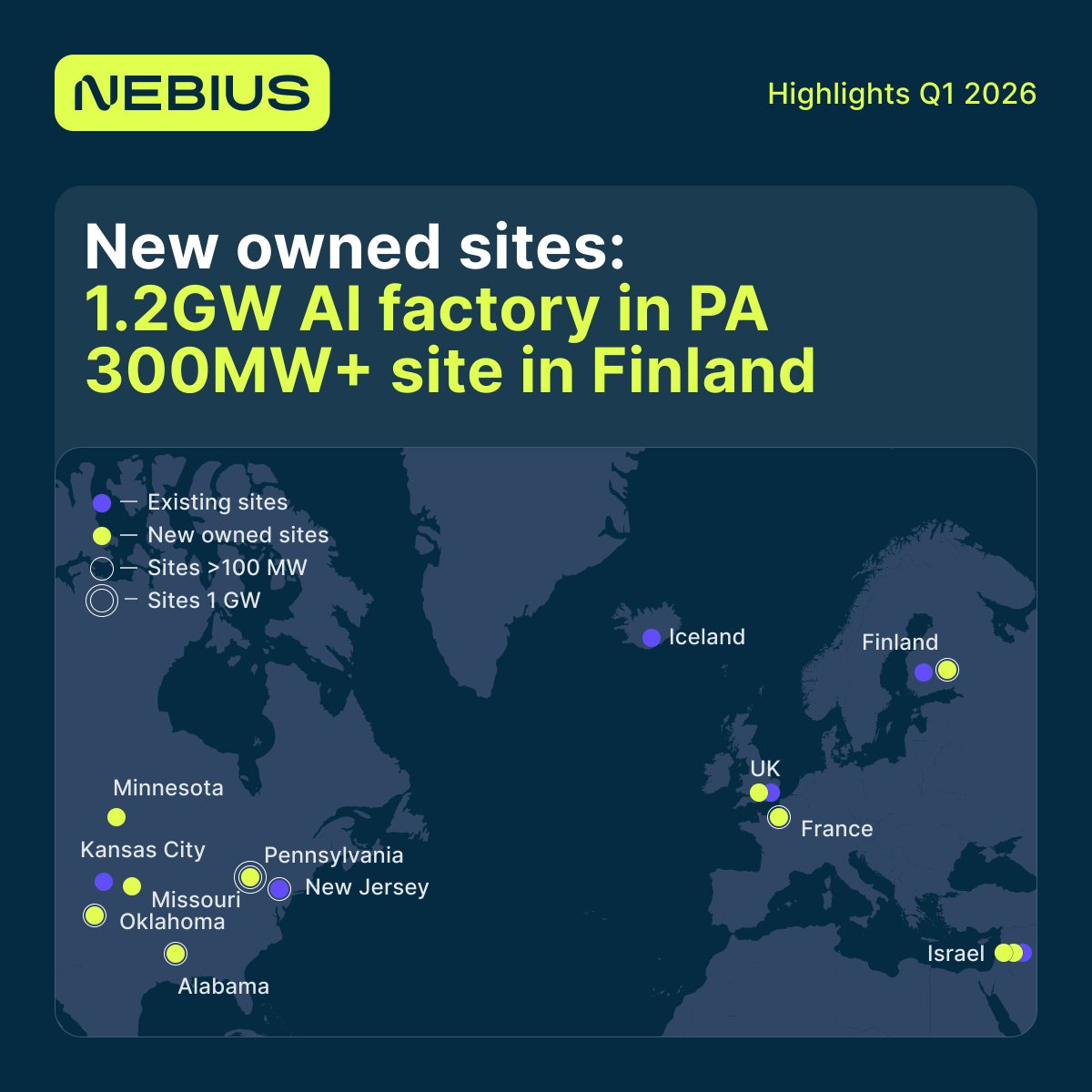

Today, we announced our Q1 2026 financial results. Here are the highlights:

- ARR grew 674% year-over-year; full-year guidance has been updated to ARR of $7-$9 billion and revenue of $3.0-3.4 billion.

- Adjusted EBITDA margin in our AI cloud business nearly doubled quarter-on-quarter to 45%.

- Contracted capacity now exceeds 3.5 GW, surpassing our 3 GW target; we now expect to have more than 4 GW of contracted capacity by the end of 2026.

We also announced today that we have secured up to 1.2 GW of power and land for a new owned AI factory in Pennsylvania, bringing our total number of sites exceeding 100 MW to seven.

Read more in our press release: nebius.com/newsroom/nebius-r…

4

5

42

13,874

Apr 27

Last Friday, together with @e27co, we hosted an exclusive roundtable with founders and senior leaders to discuss how businesses can move from #AI experimentation to real-world deployment.

The discussion was energetic and highly practical, with participants sharing real use cases, deployment challenges, and solution approaches across industries, from SME operators to enterprise teams.

One message came through clearly: AI is moving beyond experimentation into execution, integration, and measurable business impact.

A few key takeaways stood out:

🤖 AI adoption is gaining traction across customer service, coding, sales, productivity, robotics, IoT, and agentic AI.

🎯 Scaling AI still requires companies to address cost, infrastructure complexity, trust, regulation, data privacy, and internal readiness.

🚀 The fastest-moving companies are shortening planning cycles, launching practical solutions earlier, testing in real-world environments, and iterating quickly.

At Bitdeer AI, we believe scalable AI infrastructure is essential to helping businesses turn AI ideas into production-ready outcomes. As our commitment is to eliminate infrastructure complexity and cost barriers, enabling teams to build, deploy, and scale AI with speed and confidence.

Thank you to e27 and all participants for the insightful discussion.

#AIAdoption #necloud #AIInfrastructure #AI

7

2,000

Apr 7

La tesis principal de Maraver es que (i) los índices están muy concentrados en el AI trade, (ii) el ROIIC de los hyperscalers va a peor y el negocio de cloud ya es commodity (necloud)

Más allá del equal weighted S&P es difícil escapar del AI trade - tendrá razón?

2

2

870

Apr 7

$CRWV $NBIS $IREN

If you're holding any one of the above stocks, you ought to consider what sort of customer concentration risk you're exposed to.

And what’s the big pot of gold at the end of the rainbow here?

The value proposition is this magical ability for necloud providers to offer cheaper AI compute. This value doesn’t come out of thin air. Is it defensible?

Of course, Jensen is going to talk up these customers every chance he gets because they're spenidng 70-80% of capex on $NVDA chips. Hell, he’ll even throw them a couple bucks they can give back to him.

Neoclouds have weak moats. What they do can easily be replicated by anyone with money.

10

1

16

4,484

Mar 27

We are excited to announce an exclusive #AI Roundtable in partnership with @e27co on April 24. We are bringing together founders and business leaders to explore how companies can turn AI experimentation into real, sustainable business impact.

The future of AI isn't just about more compute; it’s about how that compute is integrated and utilized. As we explore a full-stack, vertically integrated approach.

During this roundtable, we’ll dive into:

🔹Open conversations on real AI scaling challenges.

🔹Strategies on moving from experimentation to impact.

🔹Peer-to-peer learning on moving from experimentation to impact.

🔹Explore how AI Cloud platforms can simplify infrastructure and accelerate AI initiatives

Don’t miss out on this exclusive discussion. Register now👉: luma.com/vkhfm5py?utm_source…

#necloud #enterpriseai #AIStrategy #AILeadership

6

1,639

Feb 27

Scaling infrastructure shouldn’t slow down innovation. Kubernetes is now available on Bitdeer AI Cloud. Deploy production-ready clusters in just a few clicks — without complex setup or operational overhead.

⚡️ Instant cluster provisioning

⚡️ Flexible node pools

⚡️ Transparent billing

⚡️ Support for NVIDIA GB200 NVL72 for AI workloads

⚡️ Built for development, scaling, and production

Whether you're running cloud-native applications, training AI models, or deploying large-scale inference workloads, our Kubernetes service delivers the flexibility and performance to grow with confidence. 🤖 Start building today: bitdeer.ai/en/k8s/instances?…

#Kubernetes #CloudComputing #necloud #AI

2

4

3,389

Jan 31

IREN ve NBIS pozisyonlarımı kapatmadığıma çok pişman etti bu hafta. Bir anda necloud sektörünü ciddi etkileyecekler haberler silsilesi oldu

1

2

211

25 Sep 2025

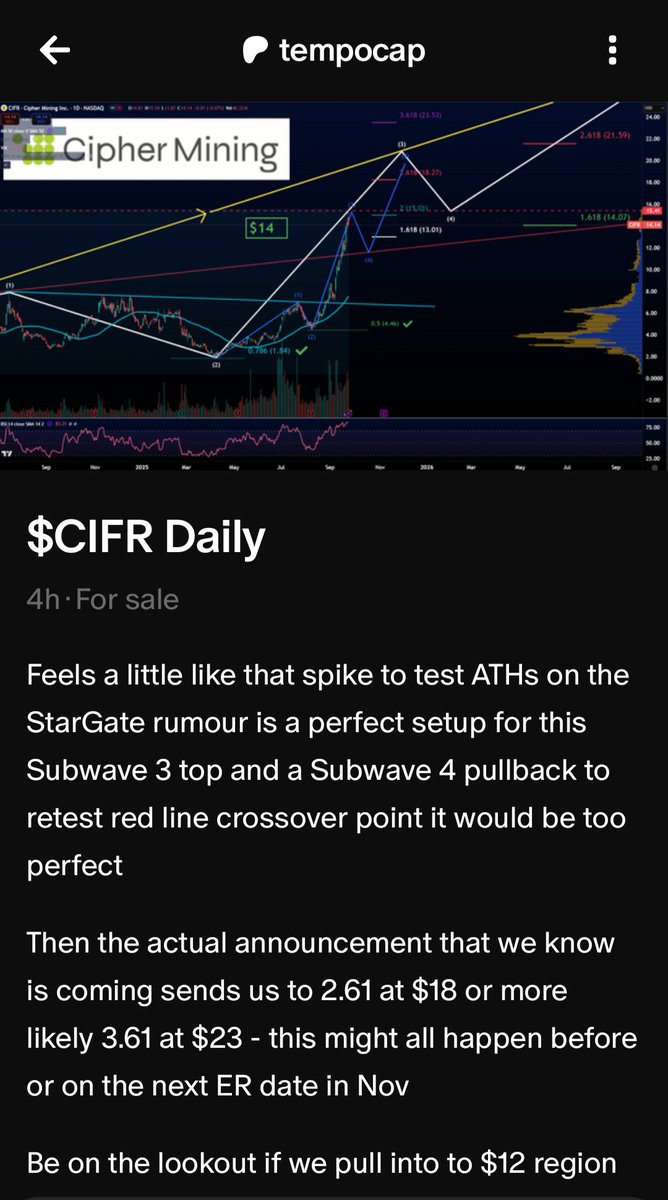

$IREN - Levels of Scarcity and Moving up the Value Chain

This Jim bro keeps talking about scarcity of power. Why does Jim bro not own any $CIFR, $BITF, $SLNH, $CAN? Does he not lift?

To preface, I think CIFR will convert on the rest of its power portfolio and much like how WULF’s second colocation deal was better than the first, CIFR a great chance of doing well. Other people who I have high respect for have good views on BITF. I don’t have any novel perspective on SLNH. Meanwhile, CAN has chicken legs. To explain why I own none of these though, I need to go through two concepts: levels of scarcity and moving up the value chain.

Levels of Scarcity

Consider water, iron ore, oil, gold, bitcoin. The scarcity of power in the coming years (2025-2030) is in between oil and gold. Oil doesn’t have shortages due to better planning and the shale revolution, so power is more scarce. Gold has major store of value while power doesn’t. CIFR ran up to $18 in pre-trading but is currently pulling back to $11.70. Some factors include 1) akin WULF’s first deal CIFR’s first deal was underwhelming 2) convertible. However, CIFR business models centers around a big contract, it’s only natural that CIFR runs up from $6.65 to $15 on the rumor and then dumps from $18 to $11.70 on the news. When zooming out, CIFR’s first deal took it from $6.65 to $11.70 - not bad at all. @tempocap2 saw this from his TA quoted below, and it makes sense from a FA perspective too - this is a good example of buy the rumor, sell the news. Now, $CIFR will have more deals as it only signed away 160MW on its 1GW (900MW EOY 2025, 100MW in 2026) capacity and 2GW 2027 pipeline (1). I respect Tyler Page (CIFR CEO) as an accomplished lawyer so he likely only states pipeline which has higher probability in. It’s important that CIFR limits its pipeline to count for power development up to 2027 while other companies include 2028, 2029 pipeline which is alot more uncertain. IREN on the other hand has moved up the value chain so it’s stock has taken less collateral damage from CIFR’s pullback compared BITF/SLNH/CAN, at the time of the writing IREN bouncing between green and red while the others are bleeding 10%-20%.

Moving up the Value Chain

By moving the value chain to IaaS, IREN creates a continuous and more smooth business model where profits and asset leverage helps it buy more GPUs for it’s IaaS business. This is why IREN has not crushed 10%-20%. In fact if you look at the inflection points, IREN trades with similar inflection points in the charts as CRWV, NBIS but higher positive magnitude (at time of writing, $IREN is up 340% YTD, $NBIS 283%, $CRWV 215%). One possible explanation for this is that institutions have put IREN, NBIS, CRWV in a Necloud basket separate from CIFR, BITF, SLNH, GXLY which trade with its similar own inflection points. Now the first order value of IaaS is that there is alot of value in guaranteeing 99.8% uptime or whatever the SLA stipulates.

The second order effect is negotiation power. IREN can do IaaS for Platforming. In the future, I’m going to do more research to compare TogetherAI to Nebius Cloud but TogetherAI is a very promising partner for IREN to do IaaS for platforming. IREN will be responsible for Hardware and Real Networking/Base Layer Software (firmware versions, drivers etc) uptime while TogetherAI is responsible for Higher Level Software and Virtualized Networking uptime. For TogetherAI who has no datacenter or hardware uptime capabilities, IREN delivers unreplaceable value. That value allows IREN to negotiate a much better slice of the pie. Having a larger slice of the pie is extremely valuable as the complete pie (Power, DC, IaaS, PaaS, SaaS) plus customer relationships is what makes Azure, GCP, AWS trillions in market cap.

In the case of CIFR’s deal, CIFR’s slice of the pie is power (and construction?); Fluidstack likely owns the DC design IaaS; Google has the PaaS/SaaS. Although Google can do Power to SaaS, it’s out of powered DCs so it’s working with CIFR and Fluidstack. Very likely Google is also out of DC operations teams as Google is always training them at max to fill out its own DCs. IREN has 2 more slices of the pie because it owns Power, DC, IaaS. Not only is this lucrative in terms of margin, but also gives it much more leverage in terms of choosing partners.

Nebius for it’s Finland DC owns Power, DC, IaaS, PaaS, SaaS and in Vineland NJ DataOne (BSO division) owns power and construction, while Nebius owns the rest of the stack. I am very interested in the terms of both the DataOne and Microsoft deals but Nebius doesn’t release them for some reason. From what we know, Vineland NJ DC depends on behind the meter gas turbines and has higher capex and operation cost than west Texas mostly renewables. BSO is a much more established player than CIFR and is probably getting much better chunk of the pie than even WULF’s second deal. Before you laugh at BSO, BSO is actually the big dog in the room. BSO is private and has no public financials but is likely larger than NBIS, IREN, TogetherAI combined as BSO has 240 datacenters world wide (2); EQIX has ~270 datacenters and is worth 75B.

I am interested in NBIS's future pipelines but as of now, whatever NBIS margins are in PaaS/SaaS, IREN more than makes up for in 10x in power. Unless NBIS can get 5-6GW of power, it cannot become a hyperscaler whereas IREN can pair with the best platform whether it be TogetherAI, Databricks, or even NBIS to split the value of a 5-6GW hyper scaled Cloud by 2030.

12

22

189

81,315

28 Jul 2025

The $CORZ crowd is right.

If $IREN hasn't gotten a deal by now, then $IREN will never get a deal in the foreseeable future.

Power is an overrated asset, and time-to-value of power is completely overvalued by these $IREN goons.

I have been mislead by $IREN analysts, and should not be held accountable for my own decisions.

I don't understand BAFTA, and I have no idea why a company would not sell its megawatts for cheap.

I don't understand the significance of having a GPU fleet that is 50% blackwells.

I don't understand the significance of 60-80 kw rack density in Canada.

I don't understand the significance of having bitcoin mining as a flexible load-balancing revenue generator.

I don't understand how game-changing DGX Nvidia Cloud Lepton is for the necloud space.

I don't understand how Nvidia needs companies like $IREN to succeed.

I don't understand how you can't just manifest power interconnects, long-lead items, data centers with high performance cooling overnight.

I don't understand how 100 kw density specs for next-generation GPU's will probably make those GPU's more sticky.

I don't understand how impressive it is to soon be one of the first companies in the world to have 50 critical-IT megawatts at scale with 200 kw direct liquid-to-chip cooling.

I don't understand the difference between traditional datacenters and AI factories, and that the implications of this is that value will migrate down the stack.

I don't understand the difference between $NBUS, $CRWV, and $IREN.

Even worse, I don't understand the difference between $IREN and $MARA.

I don't understand that stock price doesn't go up when I want it to.

I don't like it when Mr. Market disagrees with me.

I don't like it when Mr. Market gives me red days.

I don't have the patience, conviction, or long-termism to succeed in any investments.

I don't deserve to make money and be rich.

And I don't like it when you tell me I'm wrong, because I never am.

Good luck, $IREN bulls, this price action is bullshit.

I'm out.

Yours Truly,

Marblesats

41

6

154

36,383

26 Nov 2023

NECloud is good. Read like any cloud.

2

186

3 Apr 2023

Cloud necloud, pro hostovani DNS je potreba sluzba, ktera se neodporouci kazdy tyden nekolikrat. Takze rozumne naskalovana, s rozumnou kapacitou (konektivita, requests per second) a redundanci. A s rozumnym vyvazenim ceny/ziskanych sluzeb. A to soucasne DNS Justice nesplnuje. 🤷🏻♂️

1

3

130

17 Dec 2022

12月17日は「PS幻想水滸伝Ⅱ」発売日🎉

Gothic Necloud(ネクロード戦)

作曲 東野美紀

音楽はもちろんストーリーの評価が非常に高い

一人一人のキャラも魅力

2種類のエンディングがありそれも賛否両論

来年1、2のリマスターが発売される

#幻想水滸伝2

#コナミ

#レトロゲーム

youtu.be/_mwPJC3GunI

2

184