267 Photos and videos

Jun 11

Asked to predict what SpaceX will do 12 months after the IPO: My basic take is that it runs to $175 (in MK 2.3 trillion) pretty quickly before it chills out and starts to drop after that. I'm thinking 6-8 months into the IPO, we go to 88.5 (1.065 trillion), and then recover. So, 1 year after the IPO, we're 122.5 (1.61 trillion) and recovering on a healthy slope. Bookmark this and come back in a year to see if I was right.

Jun 11

Predict what price SpaceX $SPCX stock is trading at 1 year after its IPO

10

15

8,948

Jun 11

Exited my $VG hedge position (U.S. natural gas exporter to our allies). The threat to bomb Kharg was a tactic, and the repercussions would be disastrous for markets; as a result, a deal of some kind could be reached. The hedge comes off, and the game goes on.

Jun 11

🇺🇸 PRESIDENT TRUMP JUST SAID THIS:

"I have, as President of the United States of America, cancelled the scheduled strikes and bombings against Iran this evening"

215

Jun 11

The gameplan

Jun 11

My First purchase of SpaceX will be in 10 months.

All IPOs trade in a similar trend.

Shocking stats:

- Most IPOs drop 50% after going live. Look at $CAVA $RDDT $ALAB $CRWV $CART $CBRS

- Some drop further to 70-80%, look at $HOOD $PLTR

- And some never recover: $MBLY $CRCL $KLAR

1

49

Jun 11

There are several reasons this could be accurate: Everyone knows the $SPCX valuation is egregious that they haven't yet booked a profit, and that true data centers in space won't be until the 2030s (I'm speaking mega-scale). So look at Coreweave: they grew revenue in the triple digits last quarter, but the stock is flat. Why? Because the company is heavily in debt and is burning cash every quarter. So, it has an extreme valuation, but it grows extremely fast; it has a lot of debt and burns cash every quarter; doesn't that sound like $SPCX?

50

Jun 11

So I love Elon and his enterprises, but my thoughts are that I will not be buying the SPCX IPO until at least the share lock-ups begin to somewhat be in my favor

SpaceX's IPO uses a tiered lockup (S-1 details):

Most insiders/pre-IPO holders:

• Up to 20% after Q2 earnings ( 10% if stock ≥30% above $135 for 5/10 days).

• 7% each at 70/90/105/120/135 days post-IPO.

• 28% after Q3 earnings.

• Rest at 180 days.

Elon Musk certain major investors: 366-day lockup.

5% of IPO shares reserved exempt for select buyers.

Exact unlocked $ value isn't aggregated publicly (billions of shares total); releases are deliberately spread over ~6 months to limit volatility vs. a single dump. IPO pricing expected today.

1

42

Jun 11

The first lockup period begins 70 days out. Just remember super investor Peter Lynch's great advice: "If you aren't willing to own a stock for ten years, don't even think about owning it for ten minutes."

23

Jun 10

Anthropic just released a Mythos-based coding model, their most advanced yet, and it is blowing away the competition. This is not your typical chatbot; it's capable of chewing through the hardest, meatiest coding and engineering problems frontier labs are facing.

Why this matters to the AI thesis? 2 things: It means the race is on. Secondly, because the model is so good at coding, you're going to see a flurry of new models in the next 6-12-24-36 months, vastly more capable, essentially because creating better models is a coding and engineering problem exactly what Fable excels at.

I know the market has been volatile lately, but anybody that thinks the AI race is done hasn't been paying attention. Just be thankful for the dips. Which is why I've been buying $NBIS, $MU, $DRAM, $TSM, $NVDA and $AMD on every large dip

66

As someone who has a cost average below $30 and then averaged up to below $90, $NBIS does seem to be an opportunity in extremely high-growth data center deployments and is the largest holding in Leo's Situational Awareness and the second-largest holding in my portfolio. So I've started a DCA averaging up from 200-250

3

502

May 31

How are we feeling about the title for this summer, as the summer comeback of SAAS or the summer of SAAS? Regardless, what changed in the delta performance in SAAS vs semis? First off, Micron is no longer at $350; it's now at $950, so the opportunity cost of owning SAAS has become more attractive. Secondly, Trump is buying from $NOW, $WDAY, $ADBR, and $CRM. In this thread, I am going to offer my personal favorites and longs that I have in software 🧵

4

233

May 31

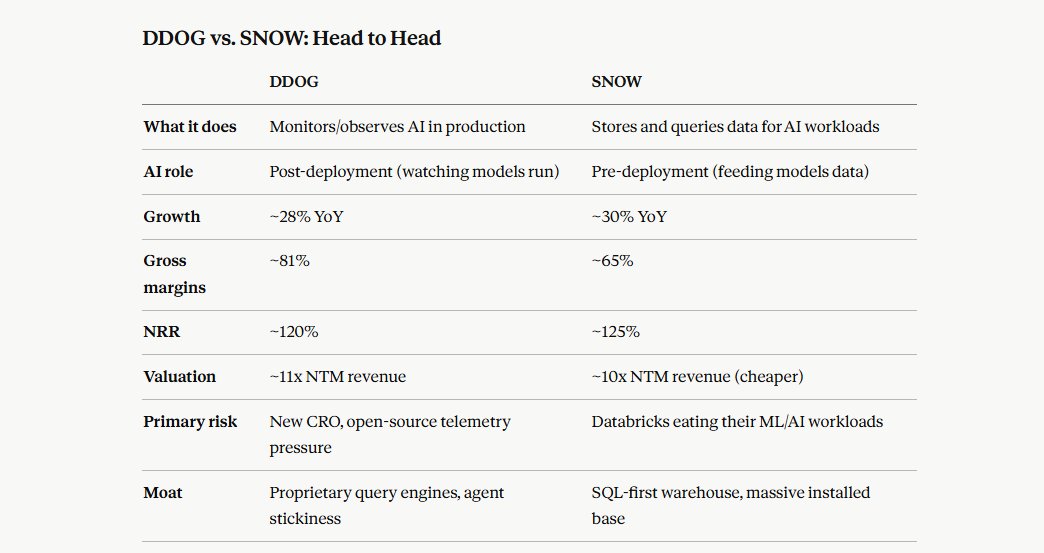

$DDOG

the Moat

DDOG's platform is sticky, with a net revenue retention rate of 120% and continued adoption of its multi-product offerings. It has beaten consensus estimates in every reported quarter. The multi-product compounding is key: once a team instruments one layer (infra, logs, APM), the switching cost to rip it out grows dramatically. Analysts pointed to DDOG's purpose-built storage and query engines — including the Monocle metrics database and Husky event engine — as difficult to replicate, pushing back on concerns that open-source telemetry tools could commoditize the platform.

The Agentic AI Kicker

As of early 2026, DDOG's business model is increasingly shifting toward "Agentic AI" tiers, where customers pay for autonomous capabilities that investigate and resolve issues without human intervention — the Bits AI SRE Agent and Security Analyst — marking the transition from observability (knowing what's wrong) to actionability (fixing what's wrong). This is a second monetization layer on top of the core telemetry business.

Here's why, within my framework specifically, $DDOG works over $SNOW:

1. Moat is harder to replicate. SNOW faces direct, credible substitution from Databricks, BigQuery, and Redshift — all competing for the same enterprise data budget. DDOG's Monocle Husky proprietary engines are not easily open-sourced away, and the multi-product lock-in compounds over time.

2. Margin structure is superior. 81% gross margins vs. ~65% means DDOG earns dramatically more on each dollar of revenue at scale. SNOW's consumption model is compute-heavy by nature — that ceiling doesn't go away.

3. AI complexity is a one-way ratchet. Every agentic AI deployment, every LLM in production, every new model version creates more demand for observability, not less. SNOW's tailwind (bigger models need more storage) is real, but DDOG's tailwind (more AI in production needs more monitoring) is structural and accelerating.

4. The Databricks overhang is real for SNOW. Once Databricks IPOs — likely H2 2026 — institutions will directly compare SNOW vs. Databricks with full public financials. Databricks is growing at 65% vs. SNOW's 30% and is already eating SNOW's ML pipeline customers. That's a valuation-compression risk on the horizon for SNOW specifically.

115

May 31

My personal favorite for playing the SAAS summer comeback are the defensive cybersecurity names $CRWD and $PANW, because AI is expanding the attack surface, not shrinking it. Every new AI agent, API endpoint, and autonomous workflow is a new vulnerability. That's a secular tailwind independent of any rotation thesis.

103

May 31

$ZETA Zeta is the stealth AI SAAS story most people overlook because it sits in "martech," not "enterprise software." But the AI angle is genuinely different from its peers.

Zeta just posted its 18th consecutive beat-and-raise quarter — that's not a company with bad earnings; that's a company nobody is watching. Q1 2026 revenue grew 50% year-over-year to $396M, beating consensus by $26M, with organic growth of 29% stripping out the Marigold acquisition.

The AI angle: their Athena AI suite enables real-time marketing automation across email, social, and Connected TV, built on a proprietary data cloud of 2.4 billion consumer identities — that's a data flywheel in martech. The more campaigns run through Athena, the smarter the targeting gets.

152

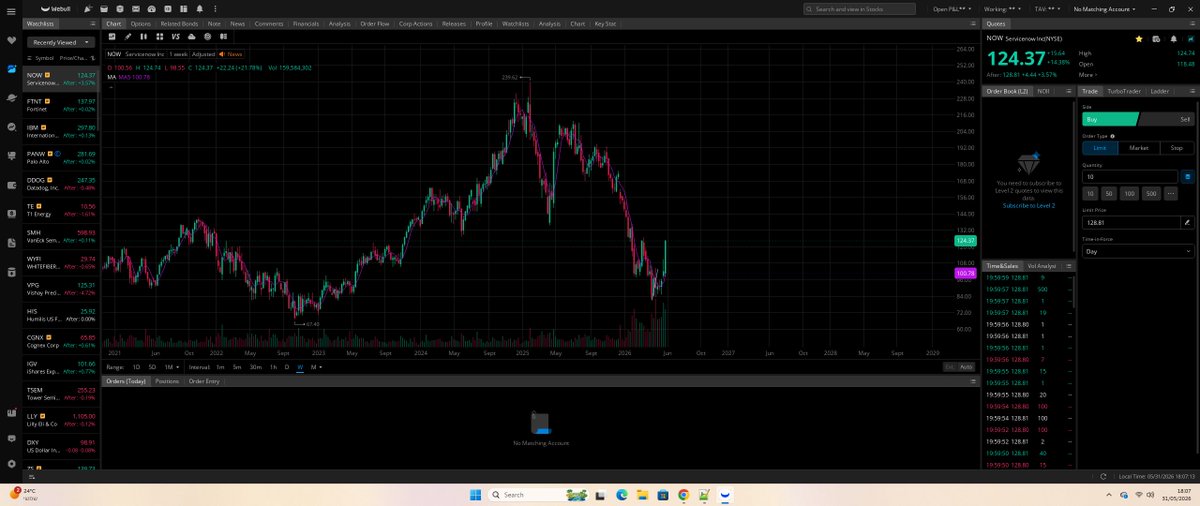

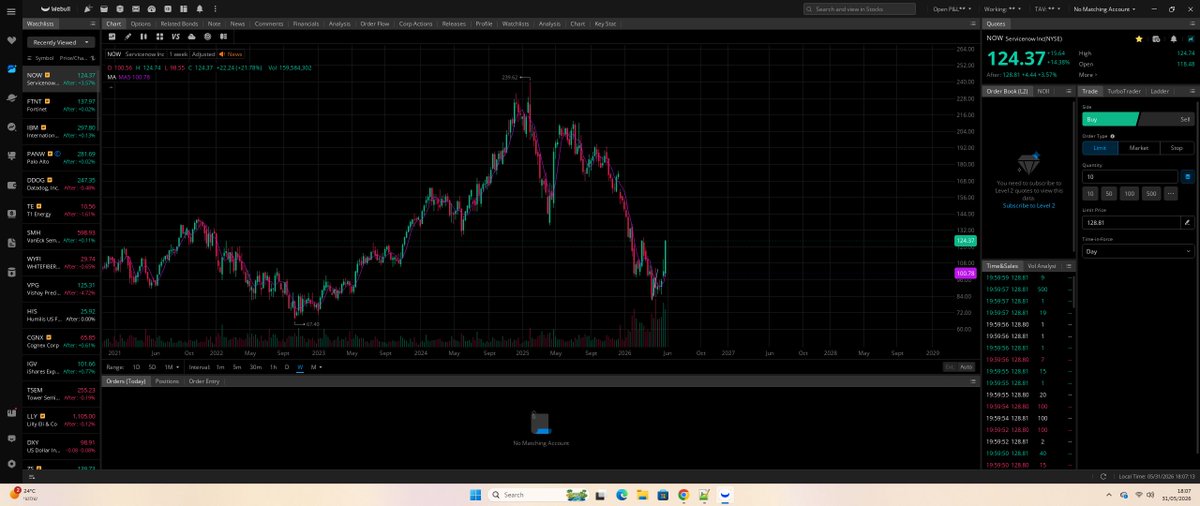

May 31

$NOW ServiceNow is arguably the single cleanest AI-native SAAS story in enterprise. CEO Bill McDermott said on the Q1 2026 call: "There has never been a tailwind for ServiceNow like AI" — crediting enterprise context and system interconnectivity as the moat. The numbers back it up.

Q1 2026 subscription revenue hit $3.67B, up 22% YoY, with cRPO of $12.64B growing 22.5% — and large deal momentum is accelerating with nearly 80% YoY growth in transactions over $5M ACV. The agentic AI angle is the key: Now Assist has evolved from GenAI summarization to a full agentic platform with 20 AI specialists automating end-to-end workflows across HR, FinOps, and security — with tiered SKUs from Foundation to Autonomous.

McDermott's framing is quotable: "our platform has gone from land-and-expand to control-and-compound." That's the rotation thesis in one sentence — every new agentic workflow deployed on NOW is sticky, recurring revenue that doesn't exist anywhere in the semi supply chain.

165

May 29

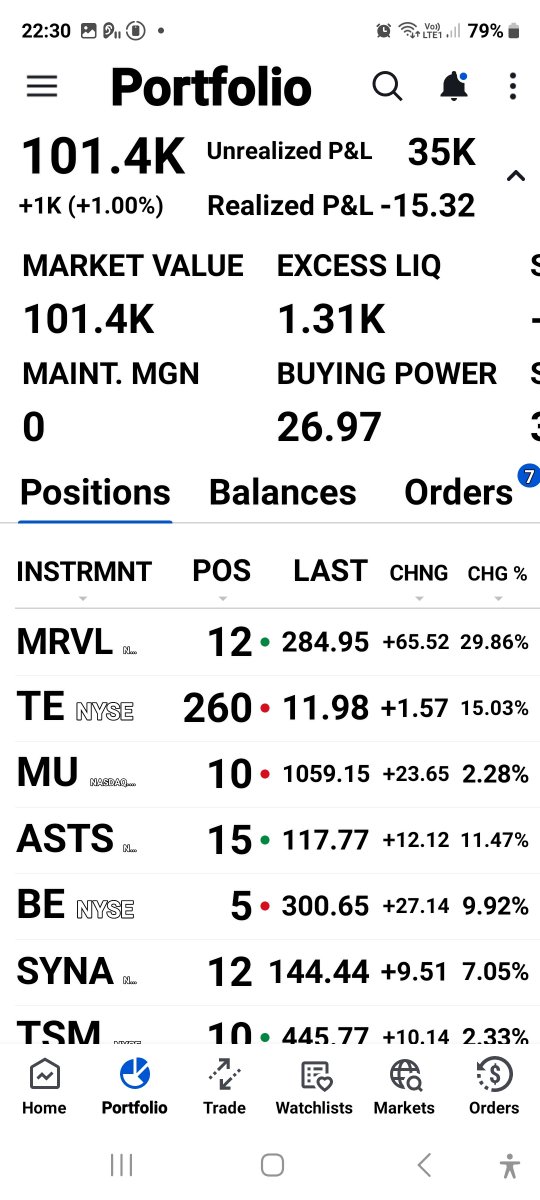

Every stock I own in my updated AI & Growth Portfolio:

AI Chips & Semiconductors:

$MU

$NVDA

$TSM

$AMD

$CRDO

$MRVL

$AVGO

$DRAM

$ARM

Cloud, Data Centers, Infrastructure & Power:

$NBIS

$DELL

$VRT

$TE

$APLD

$CLSK

$BE

$NOK

$CRWV

$GEV

Software:

$CRWD

$NOW

$ZETA

$DDOG

$SHOP

$PANW

$APP

$FTNT

Robotics:

$TSLA

$SYNA

$VPG

Big Tech and biotech:

$GOOG

$AMZN

$MSFT

$ORCL

$LLY

Space, Fintech & quantum:

$RKLB

$ASTS

$HOOD

$IBM

1

650

May 27

$MRVL has earnings after the bell. They make custom silicon XPUs for Anthropic, OpenAI, and AWS.

Analysts are expecting 27% revenue growth to $2.4 billion quarterly and 29% EPS growth to $ 0.80 quarterly.

$MRVL is a direct beneficiary of Claude and OpenAI compute demand from bot swarms of coding agents, with rising demand for Claude; the estimates might be too low.

Watch for data center guidance and any insight on their larger competitor, $AVGO. As well as guidance on the Microsoft deal

2

794

May 26

1

342

May 26

Also bought $WYFI and $VPG for the week. VPG sells sensors for humanoid robotics and physical AI, which is already benefiting from AI Capex and retail enthusiasm.

$WYFI is a purchase Leopold made in Q1 and is one of the smallest neoclouds retrofitting data centers to serve compute, electricity, and tokens

1

5

473