This is the case for modular, software-designed housing. Toxic FEMA trailers were a procurement failure—not a design law. Steel-frame, factory-built, sensor-monitored units: no formaldehyde, no rot, redeployable after the next disaster. America can build emergency housing that's durable AND dignified.

5

Jun 11

The Control Sprint

In tech, when a team wants to ship something fast before anyone can object, they run sprints. Short cycles. Rapid iteration. Lock in the architecture before the stakeholders fully understand what they’re agreeing to.

The UK government is running the most consequential sprint in modern British history. And nobody called the stand-up.

Look at the velocity.

Online Safety Act. Passed. Platforms now legally liable for content. Moderation outsourced to corporations under government direction.

Age verification. Shipping. Biometric identity tied to internet access. The ID layer is live.

Device-level scanning before encryption. In development. Not the network. Not the platform. The device itself. Your phone becomes the surveillance endpoint.

PoliceAI. Just announced. A national centre rolling AI tools to every force in the country. 6 million officer hours freed per year. Redeployable at will.

Canada moves to cut under-16s from social media. Macron applauds. The international dependencies are being committed.

That is not a series of independent policy decisions. That is a sprint backlog being worked through with deliberate, coordinated velocity. Each ticket closes. The next one opens. The architecture hardens with every merge.

In agile, you call the thing you’re building the product. So what is the product here?

A population that cannot communicate privately, cannot access information anonymously, cannot organise outside monitored channels, and exists within an AI-assisted enforcement environment that scales infinitely at negligible marginal cost.

Every single feature was shipped under a different name. Child safety. Crime reduction. Officer efficiency. Counter-terrorism. Each one reasonable in isolation. Each one a dependency in a system whose final form was never put to a public vote.

This is how you build authoritarian infrastructure in a democracy. You don’t announce the architecture. You ship the features. You move fast. You lock in before the population understands what they’re running on.

The sprint is nearly done.

The question isn’t whether they’re building it. The question is whether enough people read the changelog before the system goes to production.

34

Jun 10

Per clerk: 1h40 × 10 deeds/week = 17h/week freed. ~€40K/year of clerk time redeployable. 20-40% fees on the same portfolio. Setup under a month on a pilot deed type. 4/5

1

9

Jun 9

Cost efficiency is often reduced to transaction fees, but the deeper variable is opportunity cost. In delayed settlement systems, capital remains idle while awaiting confirmation.

TRON reduces idle capital time.

When transfers finalize within seconds and at minimal cost, liquidity becomes immediately redeployable. For traders, this means faster arbitrage cycles. For businesses, it means tighter working capital management. For individuals, it means funds are available precisely when needed.

The compound effect is subtle but powerful. Shorter settlement cycles increase capital velocity. Higher velocity increases productive capacity without increasing supply.

TRON’s dominance in stablecoin transfer volume reflects this structural efficiency. Stablecoins function as programmable cash equivalents. When paired with smart contracts, they enable automated yield strategies and decentralized lending mechanisms that operate continuously.

In contrast to batch-based banking infrastructure, TRON’s ledger updates in real time. The difference between periodic and continuous settlement may appear technical, but economically it alters resource allocation behavior.

Lower friction increases experimentation. Developers build more tools when cost barriers are minimal. Users transact more frequently when uncertainty declines.

In financial history, infrastructure improvements have always preceded innovation waves. TRON’s efficiency positions it as a catalyst rather than merely a competitor.

Efficiency scales influence.

@justinsuntron @trondao #TRONEcoStar

Jun 9

Resilience in financial infrastructure is tested during stress, not stability. TRON’s relevance becomes clearer when examined under high transaction demand.

Centralized systems rely on human-managed scaling. When volumes spike, delays increase. Congestion is often addressed administratively rather than structurally. Blockchain networks, by contrast, must encode scalability into protocol design.

TRON’s delegated consensus model prioritizes throughput while maintaining deterministic confirmation. The result is a network capable of handling substantial stablecoin volume without proportional fee escalation. Stability under load is not incidental; it is engineered.

This matters for businesses integrating blockchain rails. Predictable confirmation times reduce treasury risk. Merchants and exchanges can automate reconciliation without waiting for multi-day clearing processes.

Additionally, TRON’s ecosystem maturity strengthens resilience. Decentralized exchanges, lending platforms, and payment gateways operate in parallel rather than sequentially. If one component experiences disruption, others continue functioning. The architecture avoids single-point institutional bottlenecks.

The broader implication is strategic: infrastructure reliability encourages institutional experimentation. When enterprises observe consistent performance, they allocate more activity on-chain.

Trust, in this context, is performance-based. TRON’s sustained transaction volume reinforces confidence not through marketing, but through operational continuity.

Systems that endure stress attract long-term adoption.

@justinsuntron @trondao #TRONEcoStar

63

It slows you down gradually, cause of momentum, this has been like this for years, on the redeployable gliders at least, I loved messing with them and other features on Creative a few years ago.

1

16

867

Jun 4

ServiceNow $NOW 🇺🇸

Je reviens comme promis sur ma logique derrière cette vente.

24 mai → analyse complète en newsletter

26 mai → prise de position

2 juin → sortie avec 36% de PV en 7 jours

Depuis :

135,9$ → 117,9$ (4 juin)

soit environ -13,3% 🔴

Est-ce que j’ai “prédit” quoi que ce soit ?

Non.

Et ce n’est pas l’objectif.

Ce qui s’est passé est assez simple.

ServiceNow a connu un mouvement très vertical en très peu de temps.

Dans ce type de configuration, mon approche est la suivante :

Quand une position fait 30 à 40% très rapidement :

→ je sécurise une partie de la performance

→ je libère du capital

→ je garde la flexibilité de me réexposer si le marché corrige

Ce n’est pas un pari sur le top.

Ce n’est pas une remise en cause de la thèse.

Les fondamentaux de ServiceNow restent inchangés.

Mais le prix, lui, évolue en permanence.

Et c’est là que se joue la gestion de portefeuille.

Un point important souvent mal compris :

On peut être long terme sur une entreprise

et ajuster activement son exposition court terme.

Les deux approches ne s’opposent pas.

Dans mon cas :

→ une partie du capital a été réallouée sur d’autres opportunités (Mastercard $MA)

→ une autre est redeployable sur repli

Ce type de mouvement n’est pas exceptionnel.

C’est une logique de rotation de capital.

L’enjeu n’est pas d’avoir “raison sur le timing”.

L’enjeu est d’optimiser l’utilisation du capital à chaque instant.

Il est d’ailleurs tout à fait possible que je me repositionne sur ServiceNow dans les prochains jours (voir graph), avec une décote estimée d’environ 13,5% selon mon calcul de juste prix.

Je continuerai à partager ce type de décisions de manière transparente dans la newsletter.

Jun 3

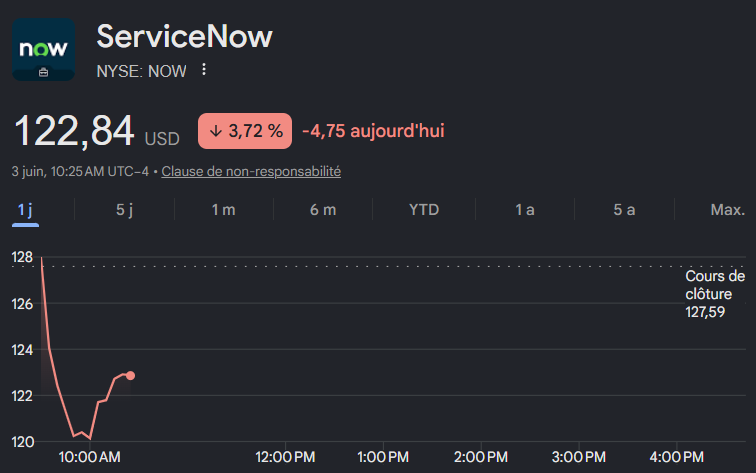

ServiceNow $NOW 🇺🇸

Vendu à 135,9$

Actuellement à 122,8$

Soit près de -10 % depuis ma vente.

Aurais-je vendu le top local ? 😱

Beaucoup n'ont pas compris cette décision.

Je vous expliquerai plus en détail demain mon point de vue sur $NOW et les raisons de cette vente (il est 1h du matin chez moi).

Spoiler : je ne remets absolument pas en cause les fondamentaux de ServiceNow.

8

4

67

37,844

May 28

$ASTI

• ultra-light thin film solar

• rollable/redeployable arrays

• radiation tolerant

• built for satellites, defense, lunar & orbital AI infra

As orbital data centers, SDA constellations, and lunar systems scale, lightweight deployable power may become critical infra. 👀

3

245

May 18

組織の目標設定は、金融オプションで行使価格。それ越えれば総取りとみなすインセンティブ作る。行使価格が競合だとチキンレースに。チキンレースの結末は勝者総取りで敗者=焦土か?そうでもない、生じた資産は結構、再配置可能(redeployable)。これチキンレース参加者に共通の行使価格下げるはず。

7

276

May 14

From redeployable gliders to infinite sprinting, today brought a lot of changes to Fortnite Zero Build

gameobserver.com/fortnite-ze…

2

24

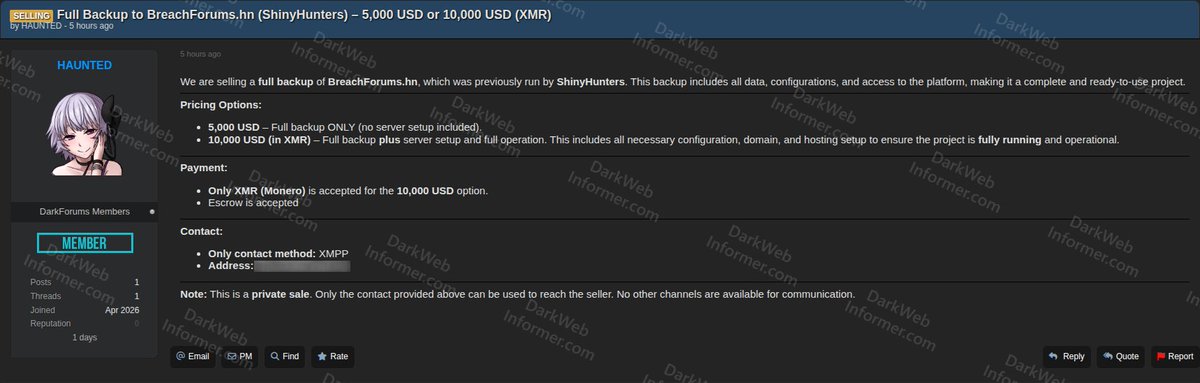

⚠️ A threat actor is selling a full backup of BreachForums[.]hn, the cybercrime forum previously operated by ShinyHunters. The seller advertises the backup as containing all data, configurations, and access to the platform, ready for redeployment.

⠀

‣ Threat Actor: HAUNTED

‣ Category: Forum Backup Sale

‣ Offering: Full BreachForums.hn backup (ShinyHunters era)

‣ Industry: Cybercrime Infrastructure

⠀

The listing offers two tiers: a $5,000 USD option for the backup data only, or a $10,000 USD option (XMR only) which includes server setup, domain, and hosting configuration to bring the platform back online. The seller states this is a private sale.

⠀

Risk to defenders:

⠀

▪️ Forum backups typically contain full user databases including hashed passwords, IP addresses, private messages, and internal staff communications useful for threat actor identification and attribution

▪️ A redeployable backup could be used to spin up a successor forum and re-aggregate the existing user base under new ownership

▪️ ShinyHunters era data spans years of breach trading, IAB activity, and ransomware affiliate communications

3

5

48

12,265

Apr 27

“Testnet live”≠ decentralized

redeployable contracts, resettable frontend, single dev infra, and a curl-to-run install still = control points

this is a sandbox on Sepolia, not a trustless system

$CAW

.

1

2

7

2,720

Apr 25

🚨 HISTORIC: India declared Maoist-free after ~50 years of Left Wing Extremism

What changes NOW:

✅ 100 CAPF battalions redeployable to borders

✅ Mineral-rich Bastar & Saranda open for investment ✅ Tribal rights under FRA finally enforceable

2

21

Deployable and redeployable are two diffrent metrics.

2

12

Apr 23

Guys, I apologise for lying to you. I told you before Saudi will make minerals an important source of revenue for the country. Iran made sure to prove me wrong.

The fund Riyadh built to acquire global mining stakes is quietly retiring the strategy.

Manara Minerals, the PIF-Ma'aden joint venture launched in 2023, is pivoting away from foreign equity acquisitions. The new mandate is trading partnerships and debt investments with offtake rights. Ownership is out.

Manara's purpose was explicit. Acquire minority stakes in iron ore, copper, nickel, and lithium mines abroad. Route the raw materials into a Saudi processing hub. Bolt the kingdom into the global critical minerals architecture before the energy transition locked in its supply chains.

One deal was ever executed. A $2.5bn purchase of 10% of Vale Base Metals in April 2024, at an implied enterprise value of $26bn. Since then, nothing. Two years of scanning the market, two years of walking away. The stated reason is valuations. The real reason is capital.

This is not a strategic refinement. It is a retreat under fiscal pressure at the worst possible moment. Critical mineral prices are at or near record highs. Washington and Beijing are competing openly for offtake. A sovereign vehicle designed to buy mining equity is withdrawing exactly when it should be deploying.

The pivot reads as a euphemism. Capital efficiency. Debt over equity. Joint ventures with Glencore, Trafigura, and Mercuria rather than control stakes. Offtake-secured loans rather than ownership. Translated, Riyadh can no longer pay peak-cycle prices for minority positions in mines it will never operate.

The broader PIF posture tells the same story. Majority sale of its flagship football club this month. LIV Golf funding under review after $5bn in losses since 2022. The 2026 to 2030 strategy explicitly rebuilt around returns, portfolio discipline, and attracting foreign capital rather than deploying Saudi capital. The era of signalling-through-expenditure is winding down.

The Hormuz closure since late February has sharpened the triage. Saudi crude exports are running at around 5 million barrels a day through the Red Sea pipeline, roughly 70% of prewar volumes. Every remaining riyal of PIF capacity is being weighed against wartime logistics, AI infrastructure, Expo 2030, and the 2034 World Cup.

The war itself has rewritten the risk calculus. Iran has demonstrated it can shut Hormuz, reach Gulf infrastructure, and pull Saudi assets into an active regional exchange of fire. Illiquid foreign equity looks reckless in that environment. A ten-year mining capex commitment in Brazil, Canada, or Indonesia cannot be repositioned when a drone lands on Abqaiq or a missile volley reopens over Riyadh. Sovereign capital under active threat has to be liquid and redeployable. Locking billions into minority stakes in jurisdictions Riyadh does not control is the opposite posture. Debt with offtake rights can be restructured, rolled, or written off. Equity cannot.

Mining was supposed to be Vision 2030's third pillar, targeting a quadrupling of GDP contribution to roughly $75bn by 2030 on a $2.5tn domestic reserve estimate. The domestic leg continues. Exploration budgets are up from $21m in 2022 to $146m in 2025. The foreign equity leg, which Manara was built to deliver, is being dismantled.

Loans-for-offtake is the Chinese template for African mining. It works for Beijing because it couples with massive industrial absorption at home and state-to-state political cover. Saudi Arabia is adopting the form without either. The result is a minority stake in other people's supply chains rather than a processing hub.

4

13

38

5,331