Jun 11

Indian military, commercial both. Dual use allows for faster return on investment. But you can't always transfer a civilian product to a military use case by add on ruggedization. Access to finance is a key issue.

51

Jun 4

#SME #HIGHNESS #HighnessMicroelectronics

Highness Microelectronics Limited H2 FY26 Earnings Call Highlights

👉 FY27 & Future Outlook:

▫️Management targets FY27 revenue of ₹30-32 Cr with EBITDA margins around 35% and PAT margins >25%

💠For FY28, revenue is guided to exceed ₹50 Cr while maintaining similar margin profile.

💠Steady-state EBITDA margins post-stabilization of new lines expected at 30-32% and PAT at 15-17%; near-term guidance reflects optimism from favourable project mix, high-margin contracts and backward integration benefits.

💠Goa COG/FOG facility on track for first commercial production in ~1 year (July-Aug 2027); will drive 10-15% reduction in input costs through in-house open-cell manufacturing.

💠Advanced glass cutting line at existing Rabale facility to be operational by end-July / mid-August 2026, immediately supporting railways & metro orders.

💠Phased machine capex of ~₹20 Cr (first phase ₹10-12 Cr, second ₹8-10 Cr) focused on automation and capacity tripling.

💠Key growth drivers: defence indigenization, railway modernization, medical electronics and industrial automation.

💠Strategic focus on higher value-add solutions, localization, technology partnerships (including Axiom USA) and global market expansion.

👉 Current Order Book / Projects and Future Pipeline:

▫️Order pipeline described as healthy and growing with customer engagement and diversified demand across all four segments

💠Three design wins already secured from APAC (including Australia) in railways and aerospace — revenue already booked >₹5-6 Cr; another three railway design wins in advanced pipeline expected to close during FY27.

💠Defence & Aerospace contributed 39% (₹6.38 Cr) of FY26 revenue; value-addition currently 40-45% (target 50-60% post-capex).

💠Railways 27% (₹4.36 Cr), Medical & Healthcare 26.7% (₹4.30 Cr), Industrial Automation 6.6% (₹1.07 Cr).

💠Export revenue at 43.8% (₹7.06 Cr) with established orders from Australia & Gulf and rising interest from Western countries; management targeting gradual increase in global share.

💠Addressable opportunity in railways/metro display market; roadmap to capture initial 10% market share once Goa facility ramps up, with further domestic and export upside.

💠Delayed export trade receivables largely cleared; final tranche expected by September 2026.

👉 Other Notable Points:

▫️Vertically integrated player with 19 years of experience, 45 team size, 17 product offerings and in-house design-to-manufacturing capabilities; claims as only Indian manufacturer for certain specialised displays competing with global giants.

💠Competitive strengths highlighted: ISO 13485:2016 & ISO 9001:2015 certifications, customisation-led OEM solutions, repeat customer base, rugged/weather-resilient products engineered for extreme conditions

💠Sourcing primarily display glass from Far East Asia followed by significant in-house value addition and ruggedization (especially for defence); minimal direct geopolitical impact.

💠Business model split between off-the-shelf products and customised market-specific solutions across Defence & Aerospace, Railways, Medical & Healthcare, and Industrial Automation

Mar 26

👉Mainboard stocks often get all the attention but some of the most compelling businesses are hiding in plain sight — on the SME Platform.

👉Smaller. Less covered, though noisy at times. Yet occasionally, genuinely exceptional.

———

👉Introducing SME Gems — a new independent series on Hidden Champions of the SME Platform :

💠 OBSC Perfection

💠 Aimtron Electronics

💠 Yash Highvoltage

💠 CFF Fluid Control

💠 DSM Fresh Foods

💠 L.T. Elevator

💠 Monolithisch India

💠 GSM Foils

👉Across Different Sectors. One common place.

🔗 smeresearch.github.io/SMEGem…

👉Stay tuned for more insights

———

⚠️ For educational purposes only. Not investment advice. Please DYODD.

#SMEGems #SMEPlatform #HiddenChampions #SME

4

6

41

6,126

@Shiblisights, a highly specialized private defense contractor from Pakistan that focuses exclusively on advanced optronics and military-grade thermal imaging solutions.

The Falcon by SHIBLI represents an elite step up from their standard uncooled gear, serving as their premier Cooled Multifunctional Thermal Binocular.

Falcon integrates a high-resolution, cooled High Operating Temperature (HOT) sensor. Because cooled sensors physically drop the system's internal temperature to reduce thermal noise, the Falcon achieves unparalleled thermal sensitivity (\le 25\text{ mK}) and a massive tracking reach.

It operates on a dual-channel framework, allowing the operator to instantly switch between a crisp, high-resolution thermal imaging feed (640\times480 pixels with a 15\mu\text{m} pixel pitch) and a visible-light digital day camera. This multi-sensor fusion provides incredible situational awareness, letting troops spot structural details in low light or pick out heat signatures through heavy smoke, fog, and absolute darkness.

Engineered for forward artillery observation, long-range reconnaissance, and specialized border patrol, the unit functions as a self-contained target acquisition hub. It incorporates an eye-safe Laser Range Finder capable of clocking accurate distance measurements from 1\text{ km} out to 10\text{ km}. When paired with its onboard GPS, GLONASS, and Digital Magnetic Compass (DMC), the binocular automatically calculates precise target location coordinates rather than just showing where a threat is, allowing operators to instantly relay exact geographical data to artillery units or command centers.

Built to MIL-STD-810G ruggedization standards, the unit features an internal OLED display (1280\times1024), built-in 32\text{ GB} photo and video recording storage, and a universal tripod interface for continuous, fixed-position surveillance operations.

1

6

6

256

May 26

$SMTC KEY READ-THROUGHS FROM SEMTECH Q1 2027 EARNINGS CALL

Semtech’s Q1 FY2027 call was an important cross-sector signal for AI data-center connectivity, optical modules, active copper cables, high-speed analog components, coherent optics, LPWAN IoT, and premium consumer component content. The strongest broader-market message was that AI infrastructure demand is accelerating across multiple interconnect layers rather than concentrating in a single product cycle. Semtech guided data-center revenue to grow 35% sequentially and 85% year-over-year in Q2, supported by 800G, initial 1.6T optical shipments, 1.6T CopperEdge shipments for ACC, and HieFo optical components. Management also stated that demand acceleration is broad-based across FiberEdge, CopperEdge, 800G, 1.6T, LPO, LRO, and lasers, with visibility extending into the first half of FY2028. This creates high-conviction positive read-throughs for AI optical module makers, analog optical component suppliers, active-copper cable suppliers, OSAT/test providers, and certain networking platform companies. The most important negative read-through is that hyperscaler preference for linearized LPO/LRO and lower-power ACC architectures could pressure portions of the optical DSP, retimer, and DSP-based active cable content stack over time, even though the initial 1.6T optical ramp remains FRO-based.

AI DATA CENTER OPTICAL MODULES AND TRANSCEIVERS

800G AND 1.6T OPTICAL DEMAND IS BROADENING FASTER THAN EXPECTED (READ-THROUGH 1)

Affected companies: Coherent (COHR: US) — positive, high magnitude; Lumentum (LITE: US) — positive, high magnitude; Fabrinet (FN: US) — positive, moderate-to-high magnitude; Zhongji Innolight (300308: China) — positive, high magnitude; Eoptolink Technology (300502: China) — positive, high magnitude; Accelink Technologies (002281: China) — positive, moderate magnitude.

The call provides a high-conviction positive read-through for optical module makers and optical component suppliers with exposure to 800G and 1.6T AI data-center deployments. Semtech reported Q1 data-center revenue of $71.6M, up 14% sequentially and 39% year-over-year, and guided Q2 data-center revenue to 35% sequential growth and 85% year-over-year growth. Management attributed the ramp to strong 800G FiberEdge demand, initial 1.6T FiberEdge revenue, 1.6T CopperEdge shipments, and HieFo optical components. The critical cross-portfolio signal is that this is not a narrow customer or product-specific ramp. Management said it has qualified with almost all major module manufacturers, including both established and emerging suppliers, and that demand acceleration is broad-based across fiber, copper, 800G, 1.6T, LPO, LRO, and lasers.

The transmission mechanism is direct volume pull-through from hyperscaler AI cluster deployments into optical modules, optical transceivers, TIAs, laser drivers, lasers, and module manufacturing capacity. Coherent and Lumentum benefit through optical components, lasers, and datacom optical exposure. Fabrinet benefits through optical module manufacturing and advanced assembly demand. Chinese optical module vendors benefit from Semtech’s explicit statement that 800G LPO deployments are occurring at leading hyperscalers in both the US and China, which supports the view that Chinese AI optical demand remains active despite export-control and geopolitical overhangs.

The near-term trading catalyst is Q2/H2 estimate revision risk across the optical module supply chain. Semtech’s data-center guide is materially stronger than the prior 50% FY2027 growth framework and implies the broader optical chain may see faster backlog conversion than current sell-side models assume. The longer-duration fundamental shift is the move from a single-cycle 800G upgrade to a multi-cycle 800G/1.6T/3.2T optical architecture transition, with Semtech’s visibility extending into the first half of FY2028.

LINEAR OPTICS ADOPTION IS A STRUCTURAL POSITIVE FOR ANALOG OPTICAL COMPONENT SUPPLIERS (READ-THROUGH 2)

Affected companies: MACOM Technology Solutions (MTSI: US) — positive, high magnitude; Coherent (COHR: US) — positive, moderate-to-high magnitude; Lumentum (LITE: US) — positive, moderate magnitude; Semtech (SMTC: US) — positive, high magnitude.

Semtech’s commentary materially reinforces the thesis that LPO and LRO are becoming mainstream AI-networking architectures rather than niche hyperscaler experiments. Management said hyperscalers are showing increased conviction around 1.6T LRO and LPO as preferred first-layer scale-out fabric solutions because of power savings. In Q&A, management stated that the growth in LPO/LRO is primarily driven by customer migration from FRO to LPO/LRO and that linearized solutions could represent approximately 25% of the total transceiver mix within 1-2 years.

The transmission mechanism is content migration from fully retimed DSP-centric optics toward analog signal-chain components, including linear TIAs, linear drivers, equalizers, and associated high-speed analog ICs. MACOM is the most direct public peer beneficiary because its data-center portfolio is levered to high-speed analog optical components and linear-drive architectures. Coherent and Lumentum benefit through module/component demand, although the impact is more mixed because each has exposure across multiple optical architectures rather than only linearized optics.

The near-term trading catalyst is likely to be investor reassessment of the linear-optics revenue opportunity ahead of 1.6T ramps in H2 CY2026 and CY2027. The longer-duration shift is more important: a 25% linearized transceiver mix would structurally lift the relative value of analog optical components and reduce the assumption that every bandwidth upgrade must proportionally increase DSP content.

OPTICAL DSP CONTENT FACES A REAL, BUT NOT IMMEDIATE, ARCHITECTURAL HEADWIND (READ-THROUGH 3)

Affected companies: Marvell Technology (MRVL: US) — negative, moderate magnitude; Broadcom (AVGO: US) — mixed, low-to-moderate magnitude; MaxLinear (MXL: US) — negative, low-to-moderate magnitude where exposed to high-speed connectivity silicon.

The clearest negative read-through is for merchant optical DSP content in portions of the AI transceiver market. Semtech stated that the initial 1.6T optical volume ramp is FRO, which still supports DSP-based designs. However, management also said customers are shifting toward LPO/LRO for power savings and that linearized solutions could approach 25% of the total transceiver mix within 1-2 years. This creates a credible medium-term headwind for DSP attach rates in first-layer AI scale-out fabrics.

The transmission mechanism is architectural substitution. In a fully retimed optical module, DSP content is central to signal recovery and retiming. In LPO/LRO, the architecture relies more heavily on high-quality host SerDes and analog linear signal-chain components, reducing DSP content per optical link. Marvell is the most directly affected public company because of its Inphi-derived optical DSP franchise. Broadcom is mixed because any loss of optical DSP content can be offset by strong switch ASIC and SerDes demand, while MaxLinear’s impact is less direct and depends on specific high-speed connectivity exposure.

The near-term trading impact should be limited because Semtech explicitly said the initial 1.6T ramp is FRO. The longer-duration fundamental shift is more negative: as hyperscalers optimize AI clusters for power efficiency, linear optics can cap the growth rate of DSP dollars per port even as optical port counts grow sharply.

ACTIVE COPPER, CONNECTORS, AND AI CABLE INFRASTRUCTURE

ACC ADOPTION IS MOVING FROM SINGLE-CUSTOMER VALIDATION TO BROADER HYPERSCALER AND ENTERPRISE EVALUATION (READ-THROUGH 4)

Affected companies: Amphenol (APH: US) — positive, high magnitude; TE Connectivity (TEL: US) — positive, moderate magnitude; Luxshare Precision (002475: China) — positive, moderate-to-high magnitude; BizLink Holding (3665: Taiwan) — positive, moderate magnitude; Credo Technology (CRDO: US) — mixed, high magnitude.

Semtech’s ACC commentary is a high-conviction positive read-through for active copper cable supply chains. Management said ACC continues to gain meaningful traction and that Q1 included shipments of 1.6T CopperEdge ICs to cable partners for deployment at a US hyperscaler. Management also said ACC samples are being evaluated by multiple hyperscalers and enterprise customers, and that the ACC MSA could accelerate adoption once specifications are finalized.

The transmission mechanism is higher AI cluster density and larger rack topologies driving demand for short-reach, lower-power, higher-performance copper interconnects. Amphenol and TE Connectivity benefit through connector, cable, and interconnect system content. Luxshare and BizLink benefit through cable assembly and high-speed interconnect manufacturing exposure. Credo is more complex: the overall active electrical cable/active copper market validation is positive, but Semtech’s claim that its approach delivers power savings versus DSP-based alternatives creates a competitive overhang for DSP-based active cable approaches where hyperscalers prioritize power.

The near-term trading catalyst is the potential finalization of ACC MSA specifications, which management said could act as a catalyst for broader adoption. The longer-duration fundamental shift is that copper is not being displaced as quickly as bearish optical-only narratives imply. Semtech’s management explicitly pushed back on the view that copper has reached end-of-life at higher data rates, arguing that copper remains relevant beyond 224G and that onboard equalization and ACC create a multi-year opportunity.

LOWER-POWER LINEAR ACC IS A COMPETITIVE THREAT TO DSP-BASED ACTIVE CABLE NARRATIVES (READ-THROUGH 5)

Affected companies: Credo Technology (CRDO: US) — negative-to-mixed, high magnitude; Astera Labs (ALAB: US) — negative-to-mixed, low-to-moderate magnitude; Marvell Technology (MRVL: US) — negative-to-mixed, low magnitude.

Semtech’s active copper commentary carries a targeted negative read-through for DSP-based active cable and retimer approaches in applications where linear equalization can achieve sufficient reach and signal integrity. Management said customers evaluating ACC are seeing advantages in link margin versus passive/direct copper and power savings versus DSP-based solutions. That framing is important because it directly identifies DSP-based alternatives as a power-disadvantaged architecture in at least some hyperscaler deployment scenarios.

The transmission mechanism is share shift within active electrical interconnects. If hyperscalers can use linear equalized ACC or onboard linear equalizers to meet reach and signal-integrity requirements at lower power, the value pool can migrate from DSP/retimer silicon toward lower-power analog equalization. Credo is the most exposed because investor expectations are highly sensitive to active electrical cable adoption and hyperscaler AI interconnect content. Astera Labs is less directly exposed because its core franchise is PCIe/CXL retimers rather than Ethernet ACC, but the broader message that hyperscalers are willing to use simpler, lower-power linear architectures is incrementally relevant. Marvell’s impact is limited but directionally negative in edge cases where DSP-based approaches compete with linearized alternatives.

The near-term impact is stock-specific and narrative-driven rather than immediate revenue displacement, because Semtech did not quantify competitive wins against DSP cable vendors. The longer-duration risk is that the AI interconnect market may bifurcate, with DSP/retimer solutions reserved for the most difficult reach or protocol cases and linear ACC taking a larger share of high-volume, power-sensitive rack-scale links.

SWITCH ASIC, SERDES, AND AI NETWORKING PLATFORMS

HIGH-QUALITY SWITCH SERDES IS EXTENDING THE LIFE OF DISCRETE COPPER AND OPTICAL ECOSYSTEMS (READ-THROUGH 6)

Affected companies: Broadcom (AVGO: US) — positive, moderate magnitude; Arista Networks (ANET: US) — positive, moderate magnitude; Marvell Technology (MRVL: US) — mixed, low-to-moderate magnitude; Cisco Systems (CSCO: US) — positive, low magnitude.

Semtech’s comments on Broadcom were unusually important for broader AI networking. Management stated that high-quality Broadcom SerDes improves the performance envelope for linear re-drivers and equalizers, making Semtech a “pure beneficiary” of Broadcom signal quality rather than a victim. Management also noted that the current ACC cable customer uses Broadcom, implying compatibility between high-performance merchant switch ASIC platforms and active copper deployments.

The transmission mechanism is architectural complementarity. Better switch SerDes enables longer usable copper reach, better LPO/LRO performance, and higher confidence in lower-power linear interconnect solutions. Broadcom benefits through continued switch ASIC leadership and SerDes leverage into AI networks. Arista benefits because broad adoption of 800G/1.6T Ethernet fabrics, active copper, and LPO/LRO reinforces hyperscaler Ethernet switching demand. Cisco benefits more modestly because the same technology vectors can support high-end AI networking, though its hyperscaler exposure is lower than Arista’s. Marvell is mixed because it benefits from custom silicon and networking exposure but may face optical DSP pressure where LPO/LRO displaces retimed optics.

The near-term catalyst is stronger confidence in AI Ethernet networking ramps rather than a direct Semtech-to-Broadcom revenue bridge. The longer-duration shift is more significant: high-quality host SerDes is becoming a strategic control point in AI networking because it determines how much of the link budget can be served by lower-power linear optical and copper components.

CPO/NPO/XPO, COHERENT OPTICS, AND DATA-CENTER INTERCONNECT

NEAR-TERM CPO DISPLACEMENT RISK LOOKS LOWER, BUT 2028 LIGHT-SOURCE DEMAND LOOKS STRONGER (READ-THROUGH 7)

Affected companies: Broadcom (AVGO: US) — mixed, moderate magnitude; Coherent (COHR: US) — positive, moderate-to-high magnitude; Lumentum (LITE: US) — positive, moderate magnitude; MACOM Technology Solutions (MTSI: US) — positive, moderate magnitude.

Semtech’s comments imply that CPO is not yet disrupting the discrete pluggable optical ecosystem at scale. Management described XPO as a compelling alternative to CPO scale-out and said current CPO approaches are not a direct opportunity for existing FiberEdge products because customers use integrated solutions. At the same time, Semtech is investing in DWDM lasers, gain chips, and light-source solutions for CPO scale-up opportunities around 2028.

The transmission mechanism is timing and content reallocation. If CPO volume adoption is later than feared, the discrete pluggable optics and active copper ecosystem retains a longer revenue runway. That is positive for Coherent, Lumentum, MACOM, and module makers. For Broadcom, the read-through is mixed: delayed CPO displacement could reduce near-term CPO monetization expectations, but Broadcom still benefits from switch ASIC leadership and the broader AI networking ramp.

The near-term trading catalyst is relief for optical module and component names exposed to pluggables, because Semtech’s call supports the idea that FRO, LPO, LRO, XPO, and ACC remain highly relevant through FY2027 and into FY2028. The longer-duration shift is that CPO may still become important, but the value pool may migrate toward external light sources, DWDM lasers, gain chips, and photonic-electronic co-optimization rather than only fully integrated switch-packaged optics.

COHERENT AND SCALE-ACROSS DATA-CENTER INTERCONNECT DEMAND IS EMERGING AS A 2028 CYCLE (READ-THROUGH 8)

Affected companies: Ciena (CIEN: US) — positive, moderate magnitude; Coherent (COHR: US) — positive, high magnitude; Lumentum (LITE: US) — positive, moderate-to-high magnitude; Marvell Technology (MRVL: US) — positive, moderate magnitude; Nokia (NOK: Finland) — positive, low-to-moderate magnitude.

Semtech’s HieFo commentary is a high-conviction positive read-through for coherent optics and data-center interconnect. Management said mega-data centers are increasingly being built as clusters, requiring high-bandwidth scale-across connectivity between facilities. Management also indicated coherent light production could ramp around mid-2028, and that HieFo’s CW lasers have been sampled to major module manufacturers. Separately, gain-chip demand reportedly exceeds supply by approximately 3x, with capacity expected to expand 3x-4x by the end of 2026 and another 3x-4x by the end of 2027.

The transmission mechanism is AI cluster geography. As single data-center campuses hit power, cooling, and land constraints, hyperscalers may distribute compute across multiple facilities that require high-bandwidth, low-latency optical interconnect. That supports coherent modules, coherent DSPs, optical line systems, DCI transport, lasers, gain chips, and InP components. Ciena benefits through DCI and coherent optical systems. Coherent and Lumentum benefit through lasers, InP, and optical component exposure. Marvell benefits through coherent DSP and high-speed connectivity silicon. Nokia benefits through optical transport, though the magnitude is lower given broader portfolio diversification.

The near-term catalyst is limited because management framed production ramp timing around 2028 rather than Q2/Q3 FY2027. The longer-duration fundamental shift is more material: AI scale-across could become a new optical transport cycle layered on top of intra-data-center 800G/1.6T demand.

SEMICONDUCTOR MANUFACTURING, OSAT, AND TEST

AI CONNECTIVITY CAPACITY CONSTRAINTS ARE DRIVING INCREMENTAL FOUNDRY, OSAT, AND TEST DEMAND (READ-THROUGH 9)

Affected companies: Amkor Technology (AMKR: US) — positive, moderate magnitude; ASE Technology (3711: Taiwan) — positive, moderate magnitude; Advantest (6857: Japan) — positive, low-to-moderate magnitude; Teradyne (TER: US) — positive, low magnitude; TSMC (TSM: US) — positive, low magnitude.

Semtech’s supply commentary is a clear positive read-through for OSAT and test capacity tied to AI connectivity components. Management said capacity is a key constraint, that Semtech began preparing around 18 months ago, and that the company can currently support drop-in orders. More importantly, management said Semtech is working with foundry and OSAT partners and adding test capacity to “double or triple the current capacity.”

The transmission mechanism is straightforward: AI interconnect components require wafer supply, package assembly, OSAT support, and high-speed test capacity. Amkor and ASE benefit most directly through OSAT demand. Advantest and Teradyne benefit through incremental high-speed semiconductor test requirements, although Semtech alone is too small to be a large earnings driver. TSMC benefits only modestly because Semtech’s volumes are immaterial relative to TSMC’s scale, but the commentary reinforces a broader pattern of AI-related analog, mixed-signal, and photonics demand competing for capacity.

The near-term catalyst is not Semtech-specific orders alone; it is the probability that multiple AI connectivity suppliers are making similar capacity commitments. The longer-duration shift is that AI interconnect is becoming a capacity-constrained semiconductor category, not merely an assembly or module bottleneck.

LOW-POWER IOT, LORA, AND INDUSTRIAL CONNECTIVITY

LORA’S REACCELERATION SUPPORTS SMART UTILITY AND INDUSTRIAL SENSOR DEMAND, BUT CREATES PRESSURE ON CELLULAR IOT IN OVERLAP USE CASES (READ-THROUGH 10)

Affected companies: Itron (ITRI: US) — positive, moderate magnitude; Landis Gyr (LAND: Switzerland) — positive, moderate magnitude; Badger Meter (BMI: US) — positive, low-to-moderate magnitude; Quectel Wireless Solutions (603236: China) — negative-to-mixed, low-to-moderate magnitude; Fibocom Wireless (300638: China) — negative-to-mixed, low-to-moderate magnitude; u-blox (UBXN: Switzerland) — mixed, low-to-moderate magnitude.

Semtech’s LoRa update was materially stronger than a simple inventory recovery. LoRa-enabled revenue was $44.5M, up 12% sequentially and 14% year-over-year, and management guided LoRa revenue to an all-time high with greater than 15% sequential growth in Q2. Management cited smart utilities, smart buildings, smart cities, asset management, public safety, healthcare monitoring, and industrial predictive maintenance. Management also said LoRa endpoints have reached approximately 150M and that integrators have been adding gateways over the last 9-12 months.

The transmission mechanism is increased deployment of low-power, long-range sensor networks, particularly where battery life, coverage, and low operating cost matter more than high bandwidth. Itron, Landis Gyr, and Badger Meter benefit from stronger smart utility and metering network adoption. Quectel and Fibocom face a mild negative read-through in overlap markets where LoRaWAN, LoRa Plus, or Amazon Sidewalk can substitute for NB-IoT/LTE-M modules in low-data-rate or edge-sensor applications. u-blox is mixed because it has exposure to both cellular and non-cellular IoT positioning/connectivity modules.

The near-term catalyst is Q2 confirmation that LoRa revenue can exceed prior historical levels and sustain above the old recovery range. The longer-duration shift is the emergence of LoRa Plus as a higher-throughput LPWAN platform, with management citing 2.6 Mbps capability and edge-AI use cases such as audio verification, healthcare confirmation, and predictive maintenance.

PREMIUM CONSUMER ELECTRONICS AND PROTECTION COMPONENTS

PREMIUM HANDSET CONTENT GROWTH REMAINS BETTER THAN UNIT GROWTH (READ-THROUGH 11)

Affected companies: Littelfuse (LFUS: US) — positive, moderate magnitude; Vishay Intertechnology (VSH: US) — positive, low-to-moderate magnitude; Apple (AAPL: US) — neutral-to-positive, low magnitude; Samsung Electronics (005930: Korea) — neutral-to-positive, low magnitude.

Semtech’s high-end consumer segment provides a modest but useful read-through for premium handset and portable-device component content. High-end consumer revenue was $38.4M, up 5% sequentially and 8% year-over-year. Management said TVS revenue continues to outpace underlying handset volumes, driven by share gains and content expansion at premium brand handset manufacturers. Management also highlighted higher-voltage power-delivery protection and rugged portable applications.

The transmission mechanism is content-per-device growth rather than unit acceleration. Littelfuse and Vishay benefit from the broader trend toward higher-performance circuit protection, surge suppression, and power-delivery protection in compact consumer devices. Apple and Samsung are neutral-to-positive beneficiaries as end customers of higher-reliability protection and sensing content, but the impact is not large enough to change device OEM earnings power.

The near-term catalyst is seasonal 2H premium handset build support, but the call does not indicate a broad handset unit recovery. The longer-duration shift is positive for protection and sensing suppliers because higher power density, faster charging, thinner form factors, and ruggedization can allow component suppliers to outgrow handset units.

May 26

$SMTC EXECUTIVE CALL SUMMARY: SEMTECH (05/26/26)

Semtech delivered a materially positive Q1 FY2027 earnings call, with the investment debate shifting from a recovery narrative to a higher-confidence AI data-center connectivity growth narrative. Q1 revenue of $291.0M rose 6% q/q and 16% y/y, exceeding the prior $283.0M midpoint and the $288.0M high end of guidance. Adjusted diluted EPS of $0.51 rose 34% y/y and exceeded the prior $0.48 high end. Management guided Q2 revenue to $328.0M /- $5.0M, implying 13% q/q and 27% y/y growth at the midpoint, with adjusted EPS of $0.61 /- $0.02, implying 20% q/q and 49% y/y growth. The guidance was more important than the Q1 beat because it incorporated a step-function in data-center revenue: management expects Q2 data-center revenue to grow 35% q/q and 85% y/y, driven by 800G strength, initial 1.6T optical shipments, 1.6T CopperEdge shipments, and HieFo optical components. The call’s core message was that demand, design wins, backlog, and capacity positioning have all improved simultaneously. Management’s most important short phrases were “record quarterly revenue supported by very strong bookings and backlog,” “data center business is firing on all cylinders,” and “double or triple the current capacity.”

The quarter was a clean beat against prior company guidance. Prior Q1 guidance called for $283.0M of revenue /- $5.0M, adjusted gross margin of 52.8% /- 50 bps, total semiconductor products gross margin of 60.4% /- 50 bps, adjusted OpEx of $96.9M /- $1.0M, adjusted operating margin of 18.6% /- 70 bps, adjusted EBITDA of $59.5M /- $3.0M, and adjusted EPS of $0.45 /- $0.03. Actual Q1 results were $291.0M of revenue, adjusted gross margin of 53.0%, total semiconductor products gross margin of 60.7%, adjusted OpEx of $95.1M, adjusted operating margin of 20.4%, adjusted EBITDA of $66.4M, and adjusted EPS of $0.51. The revenue beat was $8.0M versus the midpoint and $3.0M versus the high end. The EPS beat was $0.06 versus the midpoint and $0.03 versus the high end. The quality of the beat was strong because it came from revenue upside, favorable mix, OpEx timing discipline, and operating leverage rather than from a single below-the-line item.

The Q2 guide is the major estimate-reset event. The Bloomberg estimate header in the call transcript showed current-quarter sales of $301.727M and EPS of $0.521, while management guided $328.0M and $0.61, implying guide upside of approximately 8.7% on revenue and 17.1% on EPS versus those printed estimates. The current-year Bloomberg header showed sales of $1.242B and EPS of $2.229. Q1 actual plus Q2 guidance already totals $619.0M of revenue and $1.12 of EPS, leaving only $622.8M of revenue and $1.109 of EPS required in H2 to reach those printed full-year estimates. That equates to only $311.4M of revenue per quarter and $0.555 of EPS per quarter in H2, both below the Q2 guide. If Q2 revenue and EPS were merely sustained through H2, the implied FY2027 revenue would be approximately $1.275B and implied adjusted EPS would be approximately $2.34 before any additional acceleration. Since management explicitly described accelerating demand through FY2027 and visibility into H1 FY2028, the call creates upward pressure on consensus unless H2 seasonality, customer mix, or capacity conversion disappoints.

Historical context strengthens the signal. In Q4 FY2026, Semtech delivered $274.4M of revenue, up 3% q/q and 9% y/y, with FY2026 revenue of $1.05B, up 15% y/y. At that time, Q4 data-center revenue was $63.0M, up 12% q/q and 26% y/y, while FY2026 data-center revenue was $223.0M, up 58%. Management then expected FY2027 data-center revenue growth to exceed 50%, with ACC, 1.6T FiberEdge, and onboard linear equalizers cited as major drivers. Q1 FY2027 data-center revenue of $71.6M and the Q2 implied level of approximately $96.7M create an H1 FY2027 data-center base of approximately $168.3M. Against FY2026 data-center revenue of $223.0M, a 50% FY2027 growth outcome would require only about $166.2M of H2 revenue, or $83.1M per quarter, which is already below the implied Q2 level. A 70%-75% FY2027 data-center growth outcome would require roughly $105M-$111M per quarter in H2, only modestly above the implied Q2 level. Management did not formally guide to 70%-75%, but the Q2 guide and acceleration commentary make the prior “>50%” framework look increasingly conservative.

DATA CENTER: BROAD-BASED UPSIDE, NOT A 1-PRODUCT BEAT

The data-center update was the central investment event. Q1 data-center revenue was a record $71.6M, up 14% q/q and 39% y/y, representing approximately 24.6% of total company revenue and approximately 72.5% of infrastructure revenue. Management attributed the strength to 800G FiberEdge demand, strong TIA demand across transceiver programs, LPO deployments at leading hyperscalers in the US and China, customer engagement, portfolio alignment, and supply assurance. The Q2 data-center guide implies approximately $96.7M of revenue, a 35% q/q step-up, which would make data center close to 29.5% of Q2 total company revenue at the guide midpoint. This is a meaningful mix shift toward higher-value semiconductor products and away from slower-growth IoT systems exposure.

The call reduced the probability that data-center upside is concentrated in 1 customer or 1 architecture. Management said Q1 data-center revenue was predominantly 800G FRO and LPO, with LPO increasing sequentially from the mid-single-digit revenue contribution discussed in Q4. For Q2, management expects continued 800G FRO/LPO strength, continued 1.6T CopperEdge ramp for ACC demand, and initial FiberEdge revenue supporting 1.6T optical transceivers using new DSP designs. Management also said revenue sources are broad-based, with qualification across almost all major module manufacturers, including established and emerging vendors, and some ability to support unforecasted drop-in demand within lead times. The breadth matters because Semtech’s upside is being pulled by a hyperscaler/module ecosystem transition rather than by a narrow inventory restocking cycle.

The 1.6T optical ramp appears to be earlier and broader than previously modeled. Management indicated that 1.6T optical design wins have been secured with major module makers for transceivers incorporating latest-generation DSPs, supporting second-half module ramps. The initial 1.6T volume ramp is expected to be FRO, not LPO/LRO, but Semtech’s linearized drivers and TIAs are being evaluated for 1.6T LRO and LPO. This is strategically important: Semtech is participating in the retimed architecture that is ramping 1st, while retaining exposure to the linearized architecture that hyperscalers prefer for power savings. Management also expects linearized solutions to represent approximately 25% /- of the total transceiver mix over a 1-2 year time frame, suggesting a meaningful LPO/LRO adoption curve even if FRO remains material.

CopperEdge and ACC also moved in a positive direction. Management said Q1 included shipments of 1.6T CopperEdge ICs to cable partners for deployment at a US hyperscaler. ACC continues to be evaluated against incumbent solutions, with management highlighting link margin advantages versus passive copper and power savings versus DSP-based approaches. The ACC MSA is not finalized, and management acknowledged that standardization could accelerate adoption by aligning cable manufacturers around common specifications. This leaves a catalyst path, but also a timing risk: ratified interoperability standards could unlock more CSP demand, while delays could slow broader adoption beyond the leading customer.

The onboard linear equalizer opportunity is incremental to ACC and potentially expands Semtech’s copper SAM beyond cable assemblies into system-level backplane and board-level connectivity. Management said hyperscalers and ODM manufacturing partners are engaged on real programs, that multiple potential customers are evaluating onboard linear equalizers, and that additional design wins are expected in coming quarters. Current CopperEdge products support unidirectional equalization, while customer requests for bidirectional equalization have led Semtech engineers to formulate a preliminary architecture to integrate bidirectional capability on 1 chip. This is not yet a mature product cycle, but it is strategically relevant because board-level equalization can extend copper usefulness as rack architectures become larger and higher data rates stress reach.

The call also challenged the bear argument that copper is nearing terminal decline as optical and CPO adoption increase. Management argued that higher-quality SerDes from Broadcom and others benefits linear re-drivers because better transmitter quality gives the equalizer a stronger signal to preserve and extend. The statement that copper remains useful beyond 224G and that Semtech is engaging customers on higher data rates pushes against the view that ACC is only a short-lived bridge product. That said, the architecture debate remains real. CPO scale-out can eventually alter the available content pool for discrete FiberEdge products, and management acknowledged that current CPO approaches are not a direct opportunity for existing FiberEdge products because integrated solutions may be used. The investment conclusion is that CopperEdge appears to have a multi-year runway, but the duration depends on system topology, CPO timing, switch platform evolution, and the economics of optical scale-up versus copper scale-up.

2

1

12

13,835

May 24

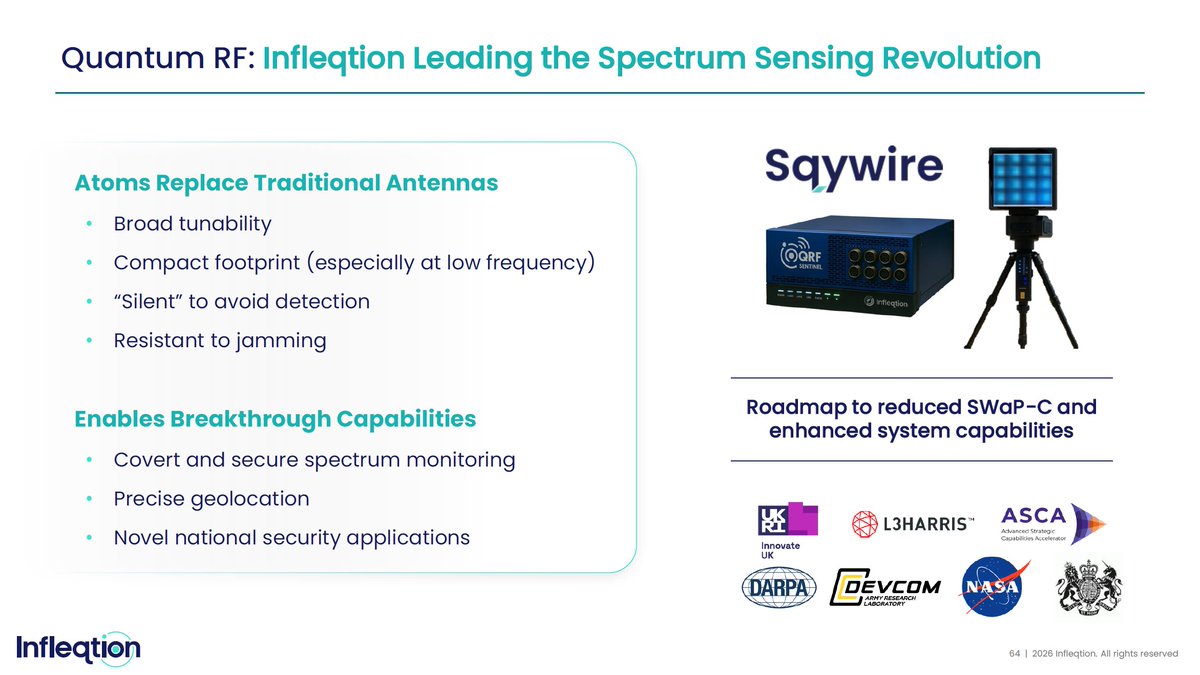

$INFQ Quantum Spectrum = 국방 RF sensing 독점 기업

Dr Kris Naudts는 Firgun Ventures 양자기술 전문 VC 파트너

*** Infleqtion is the first company with defence programs for atom-based RF sensing in three allied nations. 최초 = 독점 Aukus 방산 (미국,영국,호주)

* INFQ Quantum Spectrum은 GPS spoofing, jamming, 드론, 전자전 시대에 “원자 기반 RF 수신기”라는 새 국방 카테고리를 만들려는 기술.

* 현재 국방 field trial과 ruggedization 단계에 진입하여 중단기 매출 발생 유력

1. 핵심 기술: 'Quantum Spectrum'의 등장

* 기존 안테나를 고에너지 상태의 원자(Rydberg atoms)로 대체하는 기술.

하나의 장치로 광범위한 주파수 신호를 감지할 수 있고, 재밍이나 스푸핑 환경에서도 작동한다는 점이 핵심 차별점

* "수십 년 만에 RF 신호 탐지 방식의 첫 번째 근본적 전환

기존의 금속 안테나를 '리드버그 원자(Rydberg atoms, 고도로 들뜬 상태의 원자)'로 대체하여 작동

* INFQ는 Gen 1 제품을 9U, 3MHz~6GHz, Gen 2를 4U, 1MHz~12GHz, Gen 3를 modular rugged VPX product로 제시

*** 차별점: 하나의 기기로 방대한 범위의 신호를 감지할 수 있으며, 현대전의 주요 위협인 재밍(Jamming, 전파 방해)과 스푸핑(Spoofing, 신호 기만)에 강한 내성을 가짐

이는 양자 시계, 중력 센서 등에 이어 '양자 센싱' 내에 새로운 범주를 개척한 것으로 평가

2. 전략적/국방적 중요성

최근 드론의 군사적 활용과 GPS 교란(Spoofing/Jamming)이 국방의 핵심 위협으로 떠오르면서, 전파 방해에 영향을 받지 않는 '항재밍(Jam-resistant)' RF 센싱 기술이 필수적인 방어 수단으로 급부상하고 있음

이 기술은 GPS가 차단된 환경에서도 안정적인 내비게이션과 신호 모니터링을 가능하게 해줌

3. 글로벌 국방 도입 및 파트너십 현황

가장 주목할 만한 점은 이 기술이 단순한 이론적 연구를 넘어, 주요 동맹국(미국, 영국, 호주)의 실제 국방 프로그램에 도입되고 있다는 것

🇺🇸 미국: 미 육군 DEVCOM ARL (GPS 거부 환경에서의 내비게이션 및 신호 모니터링용 이동식 시스템)

* Rydberg atom 기반 transportable quantum RF demonstration system을 설계·fielding

* 이 시스템은 PNT, spectrum monitoring, jammed 또는 GPS-denied 환경에서 Army mission utility를 평가하는 mobile test bed 역할

** INFQ의 Quantum Spectrum이 단순 연구가 아니라 전장 배치 가능성 검증 단계에 들어갔다는 의미

🇬🇧 영국: Innovate UK 프로그램 (장거리 통신용 저주파 신호의 방향 탐지)

* 여러 개의 공간적으로 분리된 QRF sensor head를 사용해 signal angle-of-arrival을 정밀 측정하고, 특히 기존 안테나 기반 시스템이 어려워하는 저주파 장거리 통신·항법 대역에서 방향탐지 능력을 확보하려는 구조

** 그 신호가 어디서 오는지 찾는 것으로 군사적으로는 적 통신기, 드론 조종 신호, 레이더 방사원, 교란 장비의 위치를 찾는 데 직접 연결

🇦🇺 호주: 첨단 전략 역량 가속기(ASCA) 산하의 광대역 수신기 (오커스(AUKUS) 동맹 간 상호 운용성 확보)

* transportable Rydberg atom receiver를 개발해 sensitivity와 instantaneous bandwidth를 높이고, 미국·영국 프로그램과의 AUKUS interoperability를 강화하는 데 목적

** 호주 프로그램은 단순 호주 단독 프로젝트가 아니라, 미국·영국·호주 동맹권 방산 RF sensing 표준화 가능성과 연결

*** AUKUS 상호운용성은 향후 국방 조달 시장에서 동맹국 공동 플랫폼으로 확장될 가능성이 높아짐

주요 협력사: Dell Technologies Federal, L3Harris Technologies, SAIC 등 대형 방산 및 IT 통합업체들이 이미 참여

4. 향후 전망

지정학적 불안정성이 고조되고 기존 GPS 내비게이션 체계의 취약성이 지속해서 노출됨에 따라, 양자 기반 RF 센싱 시장은 국방 및 통신 분야에서 폭발적으로 성장할 것으로 전망

*** 경쟁하지 말고 독점하라🚀🚀🚀

1

4

34

9,741

Directed Energy High Energy Laser Weapon System (HELWS) adoption across the US Joint Force has been slow, and the usual explanation is technology. Scaling and ruggedization above 50-100 kW remain real challenges, but the bigger obstacle is structural.

HELWS cannot replace any current air defense system 1-for-1. Not for small quadcopters, where guns and EW already exist and can be purchased in numbers. Not larger missiles or across AAW roles. They may never. That makes them complementary add-ons, lowering the cost to defend fixed assets and maneuvering troops while creating a significantly deeper magazine and a more resilient CUAS and CMD force. But at a significant upfront cost to procure, sustain and actually industrialize production capacity.

Lawmakers and budget pundits therefore read HELWS and HPM as added investment with uncertain returns against proven kinetic and EW options. The math only closes when the threat picture demands composite Kinetic and Non-Kinetic defenses at scale. The DoW now seems to be getting 'there', starting with the Enduring High Energy Laser (E-HEL) effort. Hopefully, 300 kW systems follow. (📸US Army)

May 14

Directed energy is no longer experimental — it’s operational.

Built for the next phase of modern warfare, AV’s LOCUST® reflects years of progress from prototype to real-world validation, including successful testing at White Sands and a 100% live-fire demonstration aboard USS George H.W. Bush (CVN 77).

As @SecWar recently emphasized, directed energy is reshaping the future of the counter-UAS fight and driving the need for scalable, rapidly fielded solutions that adapt to an evolving battlefield. The future of scalable, cost-effective counter-UAS defense is here — and LOCUST® is leading the way.

1

23

107

9,270

May 16

$OUST

"Our customers really care about the capability of the LiDAR, but they never want to think about it breaking. [...] So the requirements and ruggedization of these devices is like insane compared to most of the products you would ever purchase as a consumer."

— Angus Pacala, CEO of Ouster

Here's more footage of Ouster's OS1 MAX being tested for functional safety and 24/7 reliability:

2

8

67

4,370

May 14

5 questions before you migrate from LTE Cat-4:

1. Real throughput needs?

2. Deployment lifespan?

3. Power requirements?

4. Ruggedization?

5. OTA remote mgmt?

Full 10-question framework in @SemtechCorp's new RedCap white paper: info.sierrawireless.com/how-…

1

3

8

184

Aimtron is the outlier in this coverage universe an SME-board listed company that has nearly doubled revenue in a single year, maintains EBITDA margins above 20%, and is targeting a 40–50% CAGR over 3–5 years toward a ₹1,000 crore revenue target. The profile is fundamentally different from the other four companies: ODM-led, design-driven, with a strong box-build orientation (69% of revenue) and PAT margins of 15.3%.

The ICS Acquisition

The defining event of FY26 was the acquisition of International Control Services (ICS) in Decatur, Illinois, rebranded as Aimtron International Controls (AIC). This 58,000 sq ft facility specializes in product ruggedization — electronics designed for harsh environments like agriculture, mining, fire and safety. It gives Aimtron immediate access to the US Midwest industrial ecosystem (proximity to Caterpillar, John Deere, CNH, BUNN).

The Order Book Explosion

The order book nearly tripled from ₹189 crores to ₹521 crores 1.7x FY26 revenue. Telecom leads at 32%, followed by Power & Data Center at 22%, IoT & Robotics at 21%, and Industrial at 17%. The RFQ pipeline stands at ₹900–950 crores.

Major order wins include an ODM contract worth 975 million from a leading US infrastructure firm, a 460 million AI/IIoT box-build domestic order for 50,000 units, and a significant order from a Navratna PSU in electronic communication. Post-quarter, another 577 crore order was received for Industrial (IoT) and AI Surveillance sectors.

Margin Profile is differentiated here

At 21.8% EBITDA and 15.3% PAT margins, Aimtron operates at multiples of the margin profile of larger EMS players. This is structurally driven by three factors: the ODM/design-led model (they don't just assemble they design from concept to production), the focus on complex, high-mix products (UPS systems for data centres, AI dashboard cameras, drone PCBAs), and a lean cost structure

When an analyst pressed on whether consolidated margins would sustain at 22%, Sneh Shah responded: "EBITDA in the 20–22% range will be maintained on a consolidated basis." And on the PAT margin: "We are eyeing 15% PAT margins, with small variations."

1

1

14

1,815

May 14

Really strong update. This is the kind of clearer $INFQ product/category communication investors need.

Would love to hear more on the call about the commercialization roadmap for Quantum Spectrum - specifically where it sits today between field trials, ruggedization, deployment, and larger contract revenue.

2

14

1,263

Apr 22

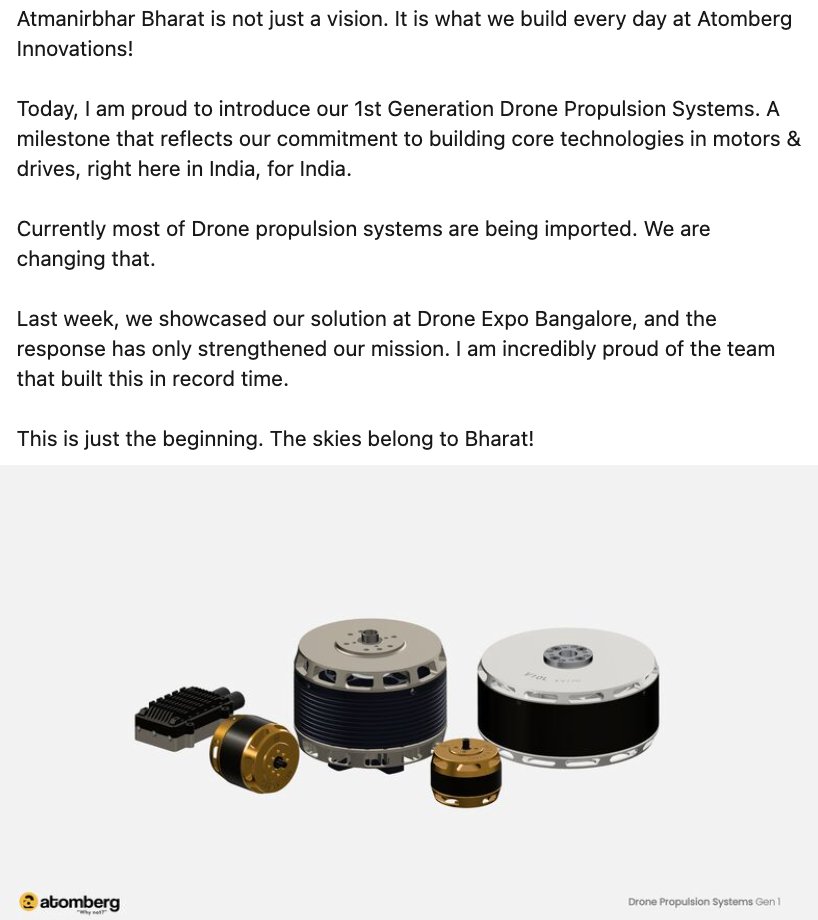

Logical progression—Atomberg has entered drone propulsion.

A drone stack = high power-density BLDC motor ESC real-time response firmware. AtomB already owns the full stack—motor design, winding, controller PCB, firmware & control algorithms. Leveraging AtomSENSE algo, this is less reinvention, more scaling ruggedization.

Its 1.5 lakh sq ft Pune facility can produce ~5M units/year, including def-grade systems. Full in-house stack enables 70% indigenous content.

If AtomSENSE evolves to multi-motor coordination, it enables swarm drones & redundancy systems. The same stack extends to robotics actuators, EV auxiliaries & industrial automation.

China-heavy motor & magnet supply chain will be bottleneck to watch out for.

Mar 16

Atomberg unveiled indigenous 1.5-ton AC rotary compressor tech at ACREX.

Mass production timelines point to ~2027; scaling rotary comp requires extensive reliability testing, BEE/ISI certification, precision mfg setup. AB targeting is B2B supply. Yet to hear about confirmed OEM orders & supply chain validation.

2

13

64

2,425

Apr 17

Can't wait for this!!

The maiden edition of Multilateral Joint Exercise Pragati-I 2026 is planned from 18 - 31 May 2026 at FTN Umroi (Shillong), Meghalaya. between India and 15 Friendly Foreign Countries (FFCs). An equipment display for the exercise is planned on 30 – 31 May 2026.

List of countries participating for the Multilateral Exercise includes Countries of Indian Ocean Region (IOR) Cambodia, Indonesia, Laos, Malaysia, Maldives, Myanmar, Philippines, Seychelles, Singapore, Sri Lanka, Thailand, Vietnam and 3 neighboring countries Bangladesh, Bhutan and Nepal.

Equipment on display to include:

Defence grade UAVs: ISR (surveillance), combat/ strikes, loitering munitions/ kamikaze, swarm operations, logistic support etc.

Counter UAVs systems: detection (radar, radio, acoustic, optical) and mitigation (jamming, spoofing, directed energy, kinetic) – fixed, vehicle mount, handheld.

Personal protection gears (BPJ/ helmets), thermal / night vision devices, multispectral camouflage net, portable/ inflatable tent.

Land based, naval and aerial surveillance, spatial intelligence, smart surveillance, perimeter security / access control.

Secure Messaging & Voice, Software-Defined Radios (SDR), Satellite Communication (SATCOM), ruggedization and cyber hardening of connectivity, supporting air, naval, and land operations.

1/2

2

4

27

1,781

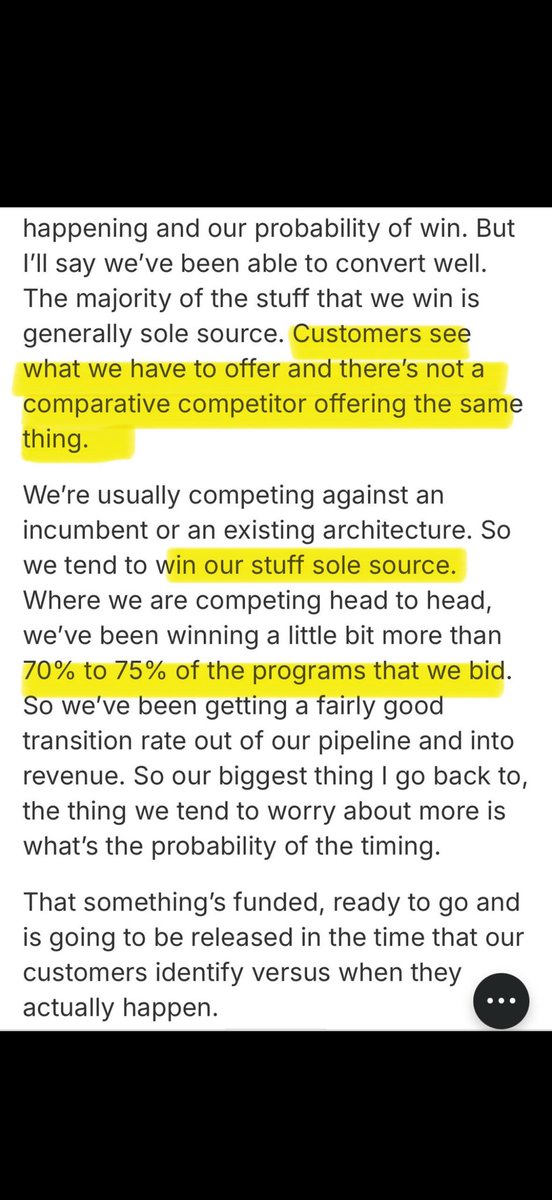

This is just wrong. Did you even spend 10 minutes doing DD on One Stop Systems?

They are not “just an integrator.” OSS designs and manufactures rugged high-performance compute systems for AI/ML at the edge integrating GPUs, storage, PCIe/NVLink fabrics, thermal systems, power, and software into deployable platforms for defense, autonomous systems, and industrial AI.

And the “no moat” argument completely misses where the moat actually is:

•Ruggedization edge AI is hard

Anyone can rack GPUs in a datacenter. Very few can make them work in tanks, ships, aircraft, or autonomous vehicles under shock, heat, and power constraints.

•Proprietary cooling (this matters more than you think)

OSS has its own advanced liquid cooling architectures, purpose-built for dense GPU deployments in extreme environments not just standard datacenter liquid loops.

This is a huge differentiator vs Vertiv-style solutions, which are primarily optimized for stationary hyperscale environments, not mobile or rugged edge deployments.

•Deep defense integration = sticky revenue

They’re embedded in multi-year defense and aerospace programs, which creates long lifecycle revenue and high switching costs.

•Engineering IP (PCIe/NVLink scaling, thermal, power)

Their value isn’t the GPU it’s making massively parallel compute systems actually function reliably in the field.

•Program-based revenue transition

Moving from one-off sales to design wins → production contracts, which is exactly how durable defense suppliers scale.

And the TAM argument is just misframed:

If you think OSS TAM = “server integrators,” you’re missing it entirely. Their TAM sits in:

•Edge AI / edge compute

•Defense AI autonomy

•Rugged industrial AI

All of which are large, fast-growing, and structurally different from hyperscale datacenters.

Regarding TAM:

Again you are just plain wrong

TAM of $VRT Data Center Infrastructure market; 150B

Marketcap of $VRT; 115B

TAM of $OSS Rugged Edge Compute; 17B

Marketcap of $OSS: 220M with s 70-75% win rate of contracts they bid on.

Did it finally click?

1

4

140

$OSS just released a new blog post detailing the key takeaways from this year's $NVDA GTC 2026, and the message is clear:

#AI is moving out of the cloud and into the real world.

For investors, this confirms that OSS is positioned exactly where the industry is heading. 👇🏻

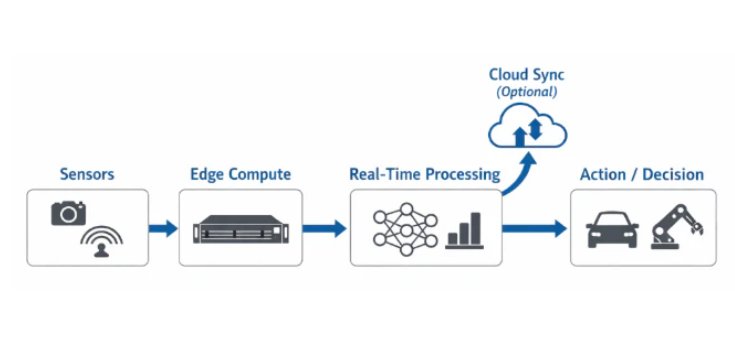

1️⃣ The Shift to "System-Level" AI

NVIDIA GTC 2026 highlighted that AI is evolving from simple inference to continuous, autonomous systems (Agentic AI). These systems can’t rely on the cloud; they need to live locally. $OSS provides the rugged, persistent compute required for this level of autonomy in the field.

2️⃣ The "AI Factory" at the Edge

NVIDIA’s "AI Factory" concept is moving to distributed nodes. OSS is ahead of the curve with platforms like the Torrey 2U Short Depth Server, built on NVIDIA MGX architectures. This allows high-performance GPU compute to be deployed in environments where traditional data centers can't go.

3️⃣ Liquid Cooling: The New Performance Frontier

As GPU power increases, thermal management is the #1 constraint. OSS is solving this with the 3U SDS-LC—a liquid-cooled, rugged system that enables enterprise-grade GPU performance in high-heat, noise-sensitive, or space-constrained areas.

4️⃣ Convergence of Industries

GTC 2026 showed a massive convergence between Defense, Energy, Healthcare, and Robotics. They all need the same thing: low-latency, deterministic, and rugged AI infrastructure. This significantly expands $OSS’s total addressable market (TAM) beyond its traditional base.

📈 The Investor Takeaway:

The edge is no longer an "endpoint"—it is where the decision-making resides. As AI workloads become more sensor-driven and real-time, the hardware requirements (ruggedization, specialized cooling, and power efficiency) become the primary differentiators.

$OSS isn't just following the AI trend; they are building the physical foundation for its next phase of growth.

3

6

43

2,998

#Quantum sensors offer unmatched precision, but environmental noise often limits their performance in the field.

We stabilize these systems against environmental and platform noise through software-ruggedization in the most demanding environments.

buff.ly/UWbtX3m

1

2

32

1,233

Apr 6

FPVs are actually disposable, they are one way muntions. UGVs are in fact attritable, you expect to lose and replace them over time. But my point is, off-the-shelf solutions often barely work, they often need ruggedization and specialisation to become militarily viable.

2

21

$OSS customer GigaIO has announced the sale of its Datacenter assets (SuperNODE™ & FabreX™) to inference pioneer d-Matrix. GigaIO is now pivotally focusing on Gryf, their "suitcase-sized" AI supercomputer for the Edge.

Why this matters for One Stop Systems:

🔹Market Validation: GigaIO going all-in on the Edge confirms that "Edge AI" is the next massive frontier—OSS’s home turf.

🔹New Synergies: With d-Matrix scaling up rack-level inference, the demand for high-performance PCIe Gen 5/6 hardware (OSS specialty) could see a new heavyweight customer.

🔹The "Gryf" Factor: As GigaIO pushes mobile datacenter-class hardware, will they partner with OSS for ruggedization, or become a friendly rival?

Slightly bullish on the sector as the Edge AI story expands, but it will be fascinating to see how the partner ecosystem reshuffles. One to watch closely! 👀

2

31

1,694