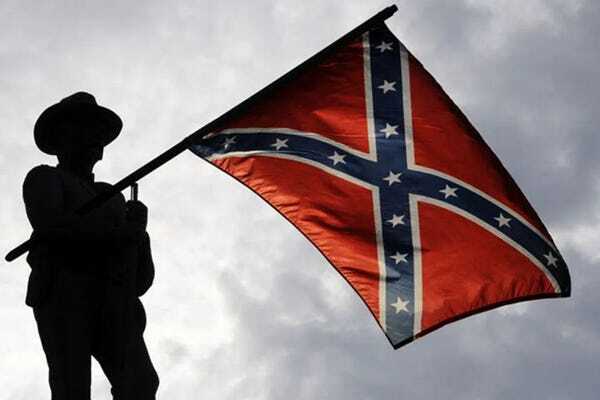

Visit Southern Nation News

In Dixie, We Fly Our Colors Proudly!

Why I Fly The Confederate Battle Flag

(An absolutely outstanding article. well worth the follow-through - DD)

(TJ, SwiftStack) - The first thing visitors to Shady Grove may notice, besi… southernnation.org/p/in-dixi…

7

13

89

833

Jan 1

$IREN: Market Dynamics and GPU Pricing

These concepts together were pretty important for me to visualize Neocloud market dynamics so I will aggregate and expand on ideas from various people. Original post from @MarkosAAIG's post (1). Strong contributions from @pepe_maltese (2). Important points on short term deviations from long term dynamics from @FransBakker9812 (3). Observation on higher GPU prices from @Umbisam (4).

Who's the Supplier to Whom?

Although Nvidia is physically supplying GPUs to IREN via Dell, intellectual property wise, everyone is a supplier for Nvidia. Nvidia defines the specifications for the rack, cooling, and more or less the datacenter. Nvidia defines more of the roadmap for the AI than anyone else.

DRAM suppliers make HBM to meet Nvidia's memory controller's clock speeds, voltage, and signaling. $CRDO tunes their retimers for Nvidia NVSwitches. AI platforms write all of their software on top of CUDA, cuDNN, NCCL, etc. IREN is actually the power DC operations supplier for GPUs.

How Nvidia Leverages It's Position

The battle is not Nvidia raising prices on Neoclouds but Nvidia taking margin share from Microsoft and upper software layer.

An example, although over simplified, would be Microsoft buys 100k Blackwells for $3/hr, now buys 50k Vera Rubins for $6/hr. The Vera Rubins have more than 2x more efficient token generation so Microsoft and the end consumer still sees savings per tokens. The big difference is that while Intel market cap stagnated despite CPU performance improvements, Nvidia on the other hand is in a more dominant position that allows it bear the fruits of it's engineering.

Nvidia's Dominant Position

Obvious to most but its worth re-iterating that Nvidia is not just GPUs. Nvidia owns a large part of the networking hardware with their acquisition of Mellanox which became their BlueField DPUs and InfiniBand scale out networking. Nvidia has developed scale up networking in house with NVLink and NVSwitch. All the networking gear run software from Nvidia's acquisition of Cumulus Networks. NCCL is the networking library that coordinates all of Nvidia networking portfolio at a AI infrastructure level.

Nvidia acquired Bright Computing for GPU cluster orchestration in 2022. Although no where near as successful as their networking stack, Nvidia is trying again with talks to acquire AI21, an Israel based Neocloud (5). Nvidia acquired RunAI for GPU scheduling in 2024 but is pending jurisdiction and. Nvidia acquired Deci for model optimization in 2024 as well.

Nvidia has also acquired SwiftStack for storage integration and Omniverse for simulation. Nvidia routinely publishes frontier research for models and robotics to expand it's TAM but underneath the research is the the software libraries that expand it's moat.

Nvidia vs Microsoft with Neoclouds Between

Microsoft already blinked on their AI buildout in 2025 and OpenAI and potentially other customers just went to $ORCL, $CRWV. To catch up Microsoft went to $NBIS, $IREN.

Once $CRWV runs out ability to dump supply on the market as Nvidia's designated commoditization beachhead, Neoclouds will raise prices because eventually the price of the GPU is just the aggregate of the depreciation residual values minus a financing and operational premium. Nvidia cannot indefinitely sell GPUs above their lifetime value.

Contrary to popular belief, ORCL is not dumping on the market and is getting 13.3m/MW-yr for IaaS (6) compared to 11.6m/MW-yr for NBIS and 9.7m/MW-yr for IREN. I expect IREN to improve their topline as 9.7m/MW-yr was not just anchor tenant pricing for Childress site but anchor tenant for the whole company.

If anything higher GPU prices show up as both higher cost and higher topline revenue for Neoclouds. Suppose fixed operational margins, higher topline is good. High cost is higher risk which will be embedded in top line as risk premium or derived from less new Neoclouds being able to afford the capital risk.

Neoclouds are Essential

Just as DRAM is an essential component, powered DCs are essential to Nvidia as they are a bottleneck for where Nvidia's customers can deploy their GPUs which is in turn a bottleneck for Nvidia's sales. From a market perspective, Neoclouds are essential for Nvidia as negotiation leverage against the hyperscalers.

Although Nvidia would like to minimize Neocloud margins, it's imperative for Nvidia to keep the industry alive.

Like any supplier industry, there is additional margin from differentiation. HS, IREN, NBIS all have good uptime, from Frans research, IREN is expecting 99.99% uptime. Differentiation will be operational and cost structure. Grid connected power has the best cost structure and best time to power which has differentiating value. With MSFT contract and H1-4 buildout, now IREN has credibilty and certainty behind it's timelines which will be a differentiator with higher GPU prices upping the stakes.

MSFT and hyperscalers will sign IaaS contracts with $IREN because they need time to power and can benefit from pass through advantages of IREN's grid connected capex cost structure. Although BTM gas turbines are becoming popular, @ShanuMathew93 talks about their higher cost structure here: (8). @ShanuMathew93 has good insights on value of grid connected power in the important details of Google's Intersect acquisition: (7).

Light at the End of the Drawdown

From above you can see that powered DCs are just as essential as DRAM to GPUs and AI. All the doubt that @hkuppy and @RealJimChanos have counter balancing forces.

@pepe_maltese says it more eloquently than I can so I will just quote him: "The market will stop punishing capex when it can underwrite utilization, price pass-through, and funding certainly in next deal."

For those fearing dilution, @pepe_maltese insightfully says "The market cap isn't the covenant. Credit is underwritten on assets contracts, not the spot share price. If H5-10 is staged with committed offtake, leverage can rise without "dstroying the capital base. If it's speculative MW, even a higher stock price won't save it."

@pepe_maltese's experience in the credit market clearly shows when he writes to not "anchor on D/E like IREN is an asset-light software co. For infra, lenders mostly underwrite collateral contracted cashflows ( DSCR/LTV, coverage)".

At these prices IREN may have to look at JVs or regular debt but there will be a way to fund H5-10, SW1, Oklahoma as long as money is funneling from the top at the frontier lab, hyperscaler level. I don't think IREN will do colocation but some form of GPU leasing is possible.

Colocation vs CSP

Power is T3 supply, DC is T2 supply, GPU operations is T1 supply. Colocation is T3 T2 supply. CSP is T3 T2 T1 supply. Having more of the stack is more capital risk but higher topline to capture margin from.

Nvidia holds the foundation layer of software but even the AI Cloud Platform can be seen as a supplier with zero distribution cost for Databricks/FireworksAI. $NBIS is also trying to capture IaaS margins can have zero distribution cost once a software component is worth running on any cloud like Clickhouse.

I invest in $IREN over $NBIS because Nvidia is unlikely to assail the powered DC layer as hard as the software layer because powered DCs are hard assets with grid interconnects already entrenched while software is zero cost distribution with networking effects. The latter is moat worthy and margins are high but too intense of a battle with Databricks/FireworksAI as direct competitiors, Nvidia from below, and Frontier Labs/AI Natives/Software Enterprises from above, and X-factor commoditization like coding agents.

6

12

108

20,327

29 Oct 2025

NVIDIA and Oracle are joining forces with the U.S. Department of Energy (DOE) to build the nation’s largest AI supercomputer.

The Solstice System

The Solstice system will feature a record-breaking 100,000 NVIDIA Blackwell GPUs, while a companion machine, Equinox, will pack 10,000 GPUs. Both will be located at Argonne National Laboratory and interconnected through NVIDIA’s high-speed networking, delivering a combined 2,200 exaflops of AI performance , the most powerful AI infrastructure ever developed for the DOE.

The new supercomputers will enable researchers to train frontier AI and reasoning models using the NVIDIA Megatron-Core library and TensorRT™ inference software, creating what the company calls “agentic AI workflows” for open science.

“The Equinox and Solstice systems are designed to accelerate a broad set of scientific AI workflows,” added Paul K. Kearns, director of Argonne National Laboratory.

energy.gov/articles/energy-d…

Quantum Processors Powered by GPU’s; NVQLink™

Developed with input from leading DOE laboratories, including Brookhaven, Los Alamos, Berkeley, and Oak Ridge, NVQLink™,nvidia.com/en-us/solutions/q… a new open system architecture that connects GPU supercomputers with quantum processors to build accelerated quantum supercomputers for next-generation hybrid computing.

NVQLink™ enables ultra-fast, low-latency data exchange between GPUs and quantum units and the technology is being adopted by 17 quantum hardware builders and 9 U.S.national labs,nvidianews.nvidia.com/news/n… marking the next step toward scalable quantum-GPU hybrid systems.

interestingengineering.com/e…

Megatron-Core Library

Megatron-Core is an open-source PyTorch-based library that contains GPU-optimized techniques and cutting-edge system-level optimizations. It abstracts them into composable and modular APIs, allowing full flexibility for developers and model researchers to train custom transformers at-scale on NVIDIA accelerated computing infrastructure.

This library is compatible with all NVIDIA Tensor Core GPUs, including FP8 acceleration support for NVIDIA Hopper architectures.

docs.nvidia.com/megatron-cor…

Multi-Storage Client (MSC) Integration

The Multi-Storage Client (MSC) nvidia.github.io/multi-stora… provides a unified interface for reading datasets and storing checkpoints from both filesystems (e.g., local disk, NFS, Lustre) and object storage providers such as S3, GCS, OCI, Azure, AIStore, and SwiftStack.

The base client supports POSIX file systems by default, but there are extras for each storage service which provide the necessary package dependencies for its corresponding storage provider.

MSC uses a YAML configuration file to define how it connects to object storage systems. This design allows you to specify one or more storage profiles, each representing a different storage backend or bucket. To tell MSC where to find this file, set the following environment variable before running your Megatron-LM script.

MSC uses a custom URL scheme to identify and access files across different object storage providers.

To train with datasets stored in object storage, use an MSC URL with the --data-path argument. In addition, Megatron-LM requires the --object-storage-cache-path argument when reading from object storage.

docs.nvidia.com/megatron-cor…

NVIDIA Hopper Architecture

nvidia.com/en-us/data-center…

PyTorch

PyTorch is a GPU accelerated tensor computational framework. Functionality can be extended with common Python libraries such as NumPy Numpy.org and SciPy.scipy.org/ Automatic differentiation is done with a tape-based system at the functional and neural network layer levels.

pytorch.org/

PyTorch Project

github.com/pytorch/pytorch

TensorRT™

Software Development Kit (SDK) for high-performance deep learning inference.

nvidia.github.io/Torch-Tenso…

Torch-TensorRT™

Operates as a PyTorch extension and compiles modules that integrate into the JIT runtime seamlessly.

nvidia.github.io/Torch-Tenso…

12

89

144

12,250

10 Jun 2025

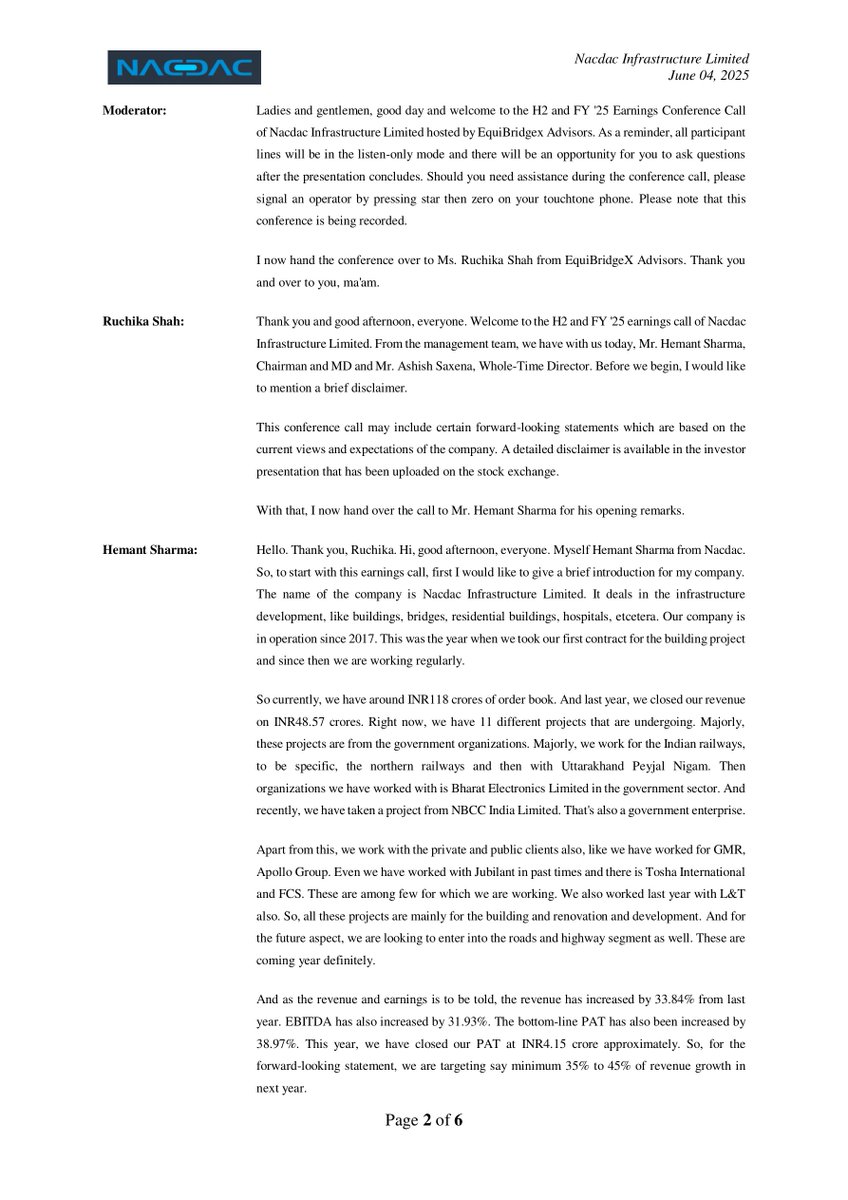

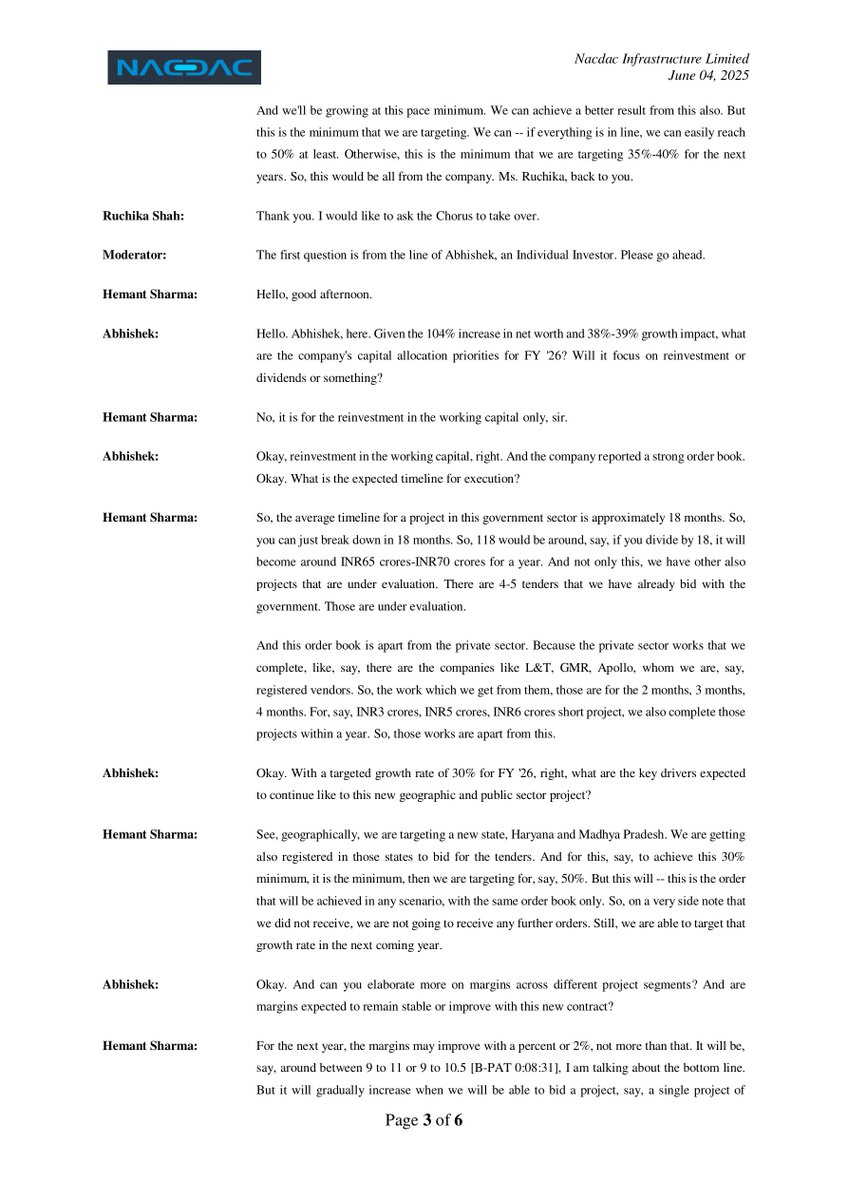

🚀 NACDAC Infrastructure Ltd: Strong Growth, Expansion Plans & Solid Order Book | MCap 43.26 Cr

- Order book at INR118 crores with 11 ongoing projects (major clients: Indian Railways, NBCC India Limited).

- Revenue grew 33.84% in FY '25; EBITDA up 31.93%, PAT at INR4.15 crore ( 38.97%).

- FY '26 revenue growth target: 35%-45%, potential to hit 50%.

- Expanding into roads & highways segment next year.

- Margins expected to improve to 9%-11%.

- Avg. project timeline: 18 months (aiming to reduce to 16 months).

- New clients: NBCC, Swiftstack Warehousing; potential deals with Bharat Electronics Limited.

- INR1 crore capex planned for machinery (JCBs, excavators, concrete plants) to boost margins.

- Reinvesting in working capital to sustain growth.

Complete Source: bseindia.com/xml-data/corpfi…

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

Preview 👇 (First 4 out of 7 pages)

2

3

5

761

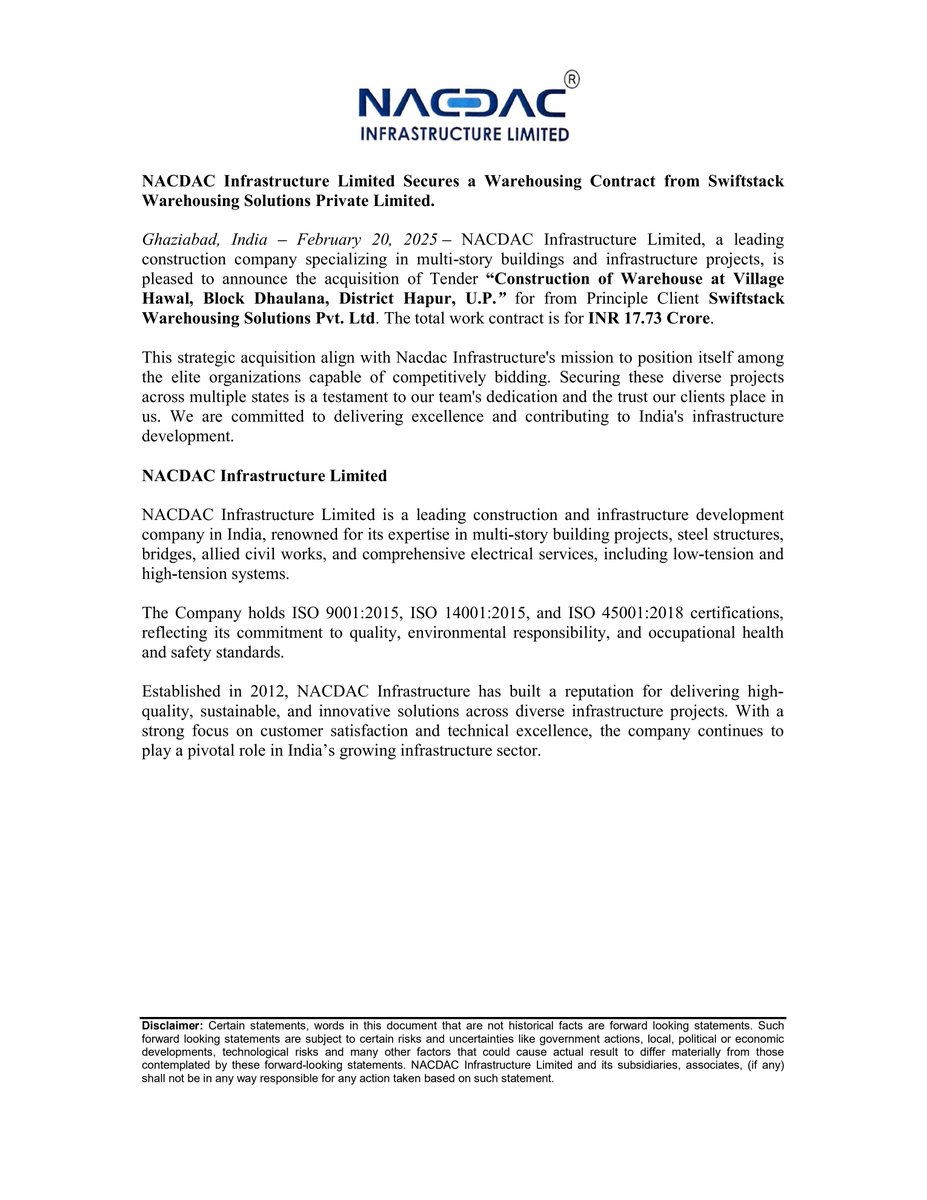

20 Feb 2025

🚀BIG NEWS from NACDAC INFRASTRUCTURE LIMITED!

NACDAC Infrastructure Limited secures warehousing contract from Swiftstack Warehousing Solutions Pvt. Ltd.!

🏗 Project : Construction of a state-of-the-art warehouse

📍 Location : Village Hawal, Block Dhaulana, Hapur, U.P.

💰 Contract Value : ₹17.73 Crore

This achievement is a testament to NACDAC expertise, dedication, and commitment to building India’s future! 🌟

More details are available at :

tinyurl.com/y3yt2rpa

1

1

3

751

20 Feb 2025

NACDAC Infrastructure Ltd

NACDAC secures a INR 17.73 crore warehousing contract from Swiftstack to build a warehouse in Hapur, U.P.

MCap: 47.54 Cr. CMP: 45.17

#NACDAC #Breaking #FlashStox #StockMarket

1

2

192

20 Feb 2025

📌 NACDAC Infrastructure Ltd informed the exchange about securing a warehousing contract from Swiftstack Warehousing Solutions Pvt. Ltd for the "Construction of Warehouse at Village Hawal, Block Dhaulana, District Hapur, U.P." The total work contract is for INR 17.73 Crore. #SME #NACDAC 🏗️📦

2

9

2,265

2 Apr 2024

Set a reminder for my upcoming Space! x.com/i/spaces/1BRJjPyDZYaKw

Our #PitchTuesday is back again. Pitching from amazing start-ups today such as @myspacebank, swiftstack, azumablockchain, payverve, econutur etc. Brought to you by #ICP

@ICPHUBS

1

6

22

516

29 Nov 2022

So great to see so many people. Including @joearnold and @anderstj from @SwiftStack that was acquired by @nvidia just before the lockdown. Great to see everyone!

28 Nov 2022

Storm hosted two welcome back mixers earlier this month – one in Menlo Park and one in San Francisco. It was great to reconnect in person with our portfolio companies and other friends of the firm. We look forward to seeing everyone again at future Storm events!

#vc #networking

6

8 Mar 2022

Is Nvidia silently buying small assets to build a platform play.

Mellanox - high speed networking chip/adapter

object storage - SwiftStack

network sdn/mgmt - Cumulus,

HPC - Bright Computing.

1

3

7 Mar 2022

Wow. @nvidia just made its 3rd storage vendor acquisition, that of @ExceleroStorage. Nvidia's acquisition play is to make a newly acquired co's tech part of its overall platform, like it did with SwiftStack and Mellanox before.

bit.ly/3vIQsju

Details @CRN. $NVDA

3

2

12 Jan 2022

Interested in @OpenStack Swift object store? I have been working on an open source management solution using @ansible and have a basic role going. The aim is to be able to build and manage clusters inspired by @SwiftStack. See github.com/csmart/ansible-ro…

1

2

6

7 Dec 2021

אז מאז מרץ 2020 אני בפיתוח בנבידיה, הסטארטאפ הגדול בעולם. האבסורד הוא שבתור swiftstack היה לי תג של נבידיה (שגם סיבך אותי קצת, אבל זה סיפור אחר), אבל עדיין אין לי תג בתור עובד, כי היום הראשון שלי בנבידיה היה גם היום הראשון של הסגר.

<<

1

10

7 Dec 2021

אנחנו עדיין swiftstack, והמנהל שלי אומר בשיחת צוות "אני יודע שמשאבי אנוש של נבידיה דיברו אתכם על המקום החדש שלכם...".

ואיתי אף אחד לא דיבר. והייתי בטוח שזהו, תסמונת המתחזה שלי צדקה כל הזמן.

<<

1

7

7 Dec 2021

אחרי עוד קצת מים במיסיסיפי, חלקם די מלוכלכים, הגיע 2020 ונבידיה החליטה לקנות את swiftstack. הייתי מאוד גאה בחלק שלי בעניין (שאולי רק היה לא לדפוק את העסק, אבל גם זה משהו).

<<

1

6

7 Dec 2021

ואז swiftstack, שוב בתור מכירות טכני. אבל בסטארטאפ של 60 איש קל להכיר את ה-PS, ולהראות להם יכולות, ולעזור להם בכמה פרוייקטים. ואולי איזה פאץ׳ קטן לאפסטרים של Swift.

<<

1

6

23 Jun 2021

1/2 Featuring @awscloud @CaringoStorage @CloudianStorage @Cohesity @ddn_limitless @DellEMC @FujitsuAmerica @HitachiVantara @HPE @Huawei @IBM @InspurCorp @NetApp @nutanix @Pivot3Inc @PureStorage @qumulo @Rackspace @RedHat @scality @silk_us @StorageCraft @suse @SwiftStack

3

2

4

1 Apr 2021

@onehub @wasabi_cloud @Infinidat @NetApp @Seagate @Nasuni @SwiftStack @OpenDrive @actifile @Minio

Tokenised software as a service👍

An innovative product from @parsiq_net is coming soon to the #SaaS space which can be used with #dataanalytics

$PRQ 💎

newsbtc.com/press-releases/p…

4

7