May 28

昨天新上的港股:深演智能(02723.HK)

上市首日收涨265%

深演智能(DeepZero)

是港股首家以“企业决策AI智能体”为主打概念的上市公司,公司专注于企业营销与销售决策的AI应用。

对标企业

The Trade Desk( $TTD ),美股AdTech龙头

两家是独立程序化广告投放平台(DSP),核心依靠AI驱动广告决策,服务大品牌客户,并保持对Google、Meta等巨头的中立性。

关键差异

规模与全球化:TTD是全球领先独立DSP,营收规模超DeepZero十倍以上,业务覆盖欧美等多地。DeepZero目前高度依赖中国市场,国际化尚处于早期阶段。

产品侧重:DeepZero在本土数据优势和企业决策AI

Agent(Deep Agent)上有特色延伸,TTD则在CTV、零售媒体和UID2等全球技术标准上更成熟。

成熟度:TTD已证明长期商业模式,DeepZero仍处于快速成长期,但营收和利润波动较大。

TTD当前股价较历史高点下跌超70%,估值已回归合理区间,DeepZero则因上市首日大涨265%,AI 新股极高情绪溢价

走势判断

短期(1-4周)

回调概率较大,港股流动性相对有限,关注成交量和换手率,回调20-40%并非不可能

中期(1-6个月)

若业绩稳定增长,有望维持较高估值,反之,可能跟随TTD路径——增长放缓即被市场杀估值

长期

无法评价,如果推进国际化还好,否则大概率e....

总之,但估值已充分甚至过度反映AI概念,优势在于本土大客户护城河和新兴AI叙事,劣势在于规模、稳定性和全球化程度。

港已有A的迹象

最后,好歹是“首位”,你敢跟风吗?

DYOR

我是好人,谢谢

#港股 #美股 #AI

14

7

1,722

May 22

Start your holiday weekend off with THE BEST coverage of the recent Publicis / LiveRamp deal and how it impacts the industry:

Signal Break: The Real Take on the LiveRamp Acquisition by Publicis Groupe

The independent infrastructure era may be ending. In this "Signal Break," we unpack one of the most consequential AdTech deals in years: Publicis Groupeacquiring LiveRamp.

Joined by Bob Walczak and Krish Raja, we break down what this deal really means for identity, clean rooms, publishers, UID2, systems integrators, and the future of the open internet.

* Is this the end of “neutral” identity infrastructure?

* Are HoldCos becoming walled gardens?

* Does agentic AI accelerate consolidation—or make it obsolete?

We get into all of it. This is the first official Signal Break: rapid-response episodes covering the biggest shifts happening across AdTech, AI, media, and infrastructure in real time. Enjoy!

Links below!

1

3

283

May 18

Publicis buying LiveRamp is one of those acquisitions that the strategy is perfect in every way. But that doesn’t mean it’ll work.

As Rich says, “Own the identity layer, the data stack, and the targeting decisions, and the open internet becomes just the pipes.”

This is the strategy behind the deal and he is spot on. The distribution tax of The Trade Desk is to identity and the supply. If you’re Publicis, you have control enough budget to get access to supply, so acquiring for identity is the missing gap to vertically integrate their offerings and expand margin.

But not so fast. This is no different than Informa buying TechTarget or Under Armour buying all the fitness apps. Both data plays that on the surface were a no brainer. But the execution of these deals is way harder than people realize. Integrating the teams, the data, and the different models make it a huge uphill battle.

If they pull it off, it’s bad news for The Trade Desk. Not only questions their network effects, but they’ll pay an additional tax to Ramp to support their UID2.

I still think this will work and the deal makes sense. I dont know what agentic offerings this helps Publicis with… but maybe that’s just PR BS. We’ll see in ~2 years how it turns out.

⚡️ Why Pay The Trade Desk’s Premium Take Rate, When Publicis Now Owns the Data? ⚡️ $RAMP $TTD

Publicis is building a data and intelligence walled garden on the buy side...Own the identity layer, the data stack, and the targeting decisions, and the open internet becomes just the pipes.

lightshedtmt.com/lightning/w…

1

8

5,147

May 18

If TTD is successful going direct to the pubs that matter they won't even need UID2. They can just transact on a direct supply path on HEMs of logged in users for CTV and mobile app. There is some loss on web, but for brands you're probably better off doing ID-less buys on web anyway.

1

2

358

May 17

Publicis acquiring LiveRamp is interesting because the majority of Trade Desks UID2 coverage was captured through the RAMP ID. The leverage they just captured will be interesting here.

4

45

5,529

Ezoic integrates UID2, ID5, and major identity providers natively.

Identity isn't a checkbox. It's a stack — deterministic IDs, alt IDs, clean rooms, PMPs. Each layer covers traffic the others can't.

ezoic.com/blog

ALT IDENTITY = STACK Not a checkbox. A layered system.

2

194

May 8

Budování ekosystému okolo UID2, kokai, ctv, třeba se uchytí Ventura OS? Kdo ví?

Jeff Green mi přijde sympatický CEO a to, že si nakoupil zpátky svůj podíl na 25 za 150M mi přijde jako hodně vote of confidence, buybacky konečně přebily dilution. Valuace už je taky fajn.

1

3

259

May 8

$TTD I think this is one of the most important underappreciated bull arguments for TTD, especially after all the agency drama.

The key point is this:

TTD’s direct advertiser relationships reduce agency dependency and create switching costs.

That matters a lot.

Why this is important

Historically, the bear case was:

“TTD depends too much on agencies. If Publicis/Omnicom/WPP push back, TTD is vulnerable.”

But this quote is saying TTD has been quietly reducing that fragility by working directly with large advertisers through:

JBPs / direct brand agreements

measurement projects

data integrations

global campaign optimization

technical workflows

custom implementation projects

Those are not simple “click a button and move budget” relationships.

Once a major brand has spent months integrating its data, measurement, reporting, identity, and optimization workflows into TTD, switching becomes painful.

This connects directly to the Q1 call

Jeff said:

March was their biggest month ever for JBP signings

they signed 45 JBPs in March alone

total JBP count grew 55% YoY

new JBP deal spend grew 40% YoY

one large pharma client signed a JBP aiming to increase spend 114% YoY

That supports exactly what this former executive is saying.

The market is focused on agency conflict, but TTD is saying:

“Our relationship is increasingly with the brand itself, not just the agency middle layer.”

That is very important.

Why it creates stickiness

A normal media buying relationship can be switched because it’s mostly budget allocation.

But a direct advertiser relationship can include:

first-party data activation

retail data usage

UID2 identity setup

CTV measurement frameworks

custom reporting

AI/Kokai workflows

global campaign architecture

That makes TTD harder to replace.

So the more TTD shifts from “DSP vendor” to “strategic advertising infrastructure,” the stronger its moat becomes.

My take

I agree with the statement.

This is probably one of the biggest reasons the bear case may be overstated. Agencies can create noise and friction, but if the end advertiser is deeply integrated with TTD and believes TTD drives outcomes, agencies can’t simply move that spend away without harming the client.

The key risk is still execution: TTD must prove those JBPs convert into actual spend growth. But strategically, this is very bullish.

Bottom line:

The market is treating TTD like an agency-dependent ad-tech vendor. TTD is trying to become embedded infrastructure for large global advertisers. That difference matters a lot.

1

11

1,832

May 7

$TTD I went through the Q1’26 investor presentation

My overall view:

1. The main message: TTD is positioning itself as the “objective AI buying layer”

The presentation repeatedly hammers one core idea:

TTD is buy-side only, does not own inventory, and therefore has no bias toward specific publishers or platforms.

That is the foundation of their entire thesis. They argue advertisers and agencies need a trusted technology partner that is not conflicted like Google, Amazon, Meta, or other platforms that own their own inventory. This is clearly shown early in the deck where they describe themselves as objective, omnichannel, measurement-driven, and technology-led.

This matters because it directly addresses the biggest bear arguments right now:

Amazon DSP competition

OpenAI possibly building its own ads stack

agency disputes

questions around transparency

AI disrupting software/adtech

TTD’s answer is basically:

“AI makes objectivity and data-driven decisioning more valuable, not less.”

I think that is a credible strategic argument.

2. The financial history still looks strong — but the slowdown is obvious

The deck shows revenue growing from $114M in 2015 to $2.896B in 2025. That long-term growth is impressive.

But the growth trend is clearly slowing:

2021: strong post-COVID acceleration

2022: still strong

2023: slower

2024: 26%

2025: 18%

Q1 2026: 12%

So the business is not broken, but it is no longer showing the old hypergrowth profile.

That is why the stock is getting punished. The market is not saying “TTD is bad.” It is saying:

“TTD may deserve a lower multiple if growth is now low/mid-teens.”

3. The agency conflict is addressed indirectly — and very intentionally

One slide says:

“We provide agencies a software platform. We create room for their proprietary advantages. We are an enabler, not a disruptor.”

That is not random. That is clearly included because of the Publicis / Omnicom / agency audit drama.

TTD is trying to say:

“We are not trying to kill agencies.”

But the reality is more nuanced. Even if TTD does not want to replace agencies, its tools do reduce agency control over parts of the value chain:

more direct brand relationships

more transparent reporting

OpenPath

OpenAds

JBPs / JBAs

AI automation through Koa Agents

So I would say the slide is defensive but important. It tells us TTD knows this is now a key investor concern.

4. The “buyer’s market” argument is very important

The deck says this is the single greatest buyer’s market in history.

This ties directly to what Jeff Green said on the earnings call: there is more digital supply than ever, especially in CTV and streaming. When there is more supply than demand, buyers need better tools to sort quality from junk.

TTD’s argument:

not all inventory is equal

some inventory has fraud, low viewability, excessive ad load, invalid traffic, made-for-advertising content

buyers need objective decisioning to avoid waste

This is a strong argument for why TTD still matters even if ad inventory explodes. More supply does not reduce TTD’s relevance — it may increase the need for a better filter.

5. CTV remains the strongest structural growth driver

The CTV section is one of the most bullish parts of the deck.

TTD argues:

TV is converging with the internet

subscription costs are too high for consumers

the future of TV is ad-funded

programmatic CTV allows better targeting and measurement

publishers can earn higher CPMs with decisioned buying

One slide compares traditional TV buying at $10 CPM versus connected TV buying at $20 CPM, arguing that data-driven targeting and measurement can increase publisher monetization.

This is very aligned with the Paramount live sports announcement in the Q1 release. If sports, streaming, and premium video become more biddable/programmatic, TTD benefits.

This remains one of the strongest parts of the bull thesis.

6. International expansion is a major underappreciated lever 🚨🚨🚨

This part stood out

The deck says:

about 86% of TTD revenue comes from North America

but only about 40% of global ad spend is in North America

about 60% of global ad dollars are outside North America

That means TTD is still heavily underpenetrated internationally.

This is important because if North America growth slows, international can still become a long-term growth lever. Management also said international grew faster than North America in prior remarks.

The issue: this is a long-term opportunity, not an immediate fix for Q2/Q3 sentiment.

7. Retail data is a very serious part of the bull case

The retail media slides are strong.

TTD says its retail data marketplace provides access to over 80% of sales from top U.S. retailers. The deck also positions retail data as deterministic, future-proof, useful for customer lifetime data, market share growth, and holistic frequency control.

This directly counters the “TTD doesn’t own data” bear argument.

TTD’s response is:

“We don’t need to own the data. We are the trusted platform that activates data from many retailers and advertisers.”

That is actually powerful if brands trust TTD more than conflicted platforms.

This also ties into the Amazon debate. Amazon has great closed-loop purchase data, but TTD is trying to aggregate retail signals across Walmart, Target, Kroger, Walgreens, Albertsons, CVS, Costco, Home Depot, and others.

If this scales, it meaningfully strengthens TTD’s moat.

8. The technology section is basically their AI/data moat argument

The deck emphasizes:

TTD built a data management platform first

“the buyer with the most data can make the most intelligent bid”

expressiveness is central to their advantage

bid factors are better than line-item structures

reporting covers 200 performance measures across 300 variables

This is important because it explains why Jeff Green keeps saying AI helps TTD.

Their argument is:

AI is only useful if you have scaled data, granular decisioning, and trusted workflows.

That is a stronger argument than just “we use AI.”

9. The financial appendix explains part of the market concern

Free cash flow remains strong:

Q1’26 operating cash flow: $391.8M, up 34% YoY

Q1’26 free cash flow: $276.0M, up 20% YoY

That is very good.

But there is a catch: Q1 capex jumped to $112.7M, up 91% YoY. That may be one reason investors are worried about margin pressure and investment intensity.

So the company is still highly cash generative, but the market may be asking:

“How much do they need to spend to keep growth going?”

My overall interpretation

Bullish points from the presentation

TTD still has a very strong strategic story:

objective buy-side platform

strong CTV positioning

strong retail data marketplace

international underpenetration

AI/data-driven decisioning

UID2 / identity infrastructure

OpenPath / OpenAds / OpenSincera transparency push

strong free cash flow

customer retention above 95%

This is not a broken company.

3

1

30

7,132

May 7

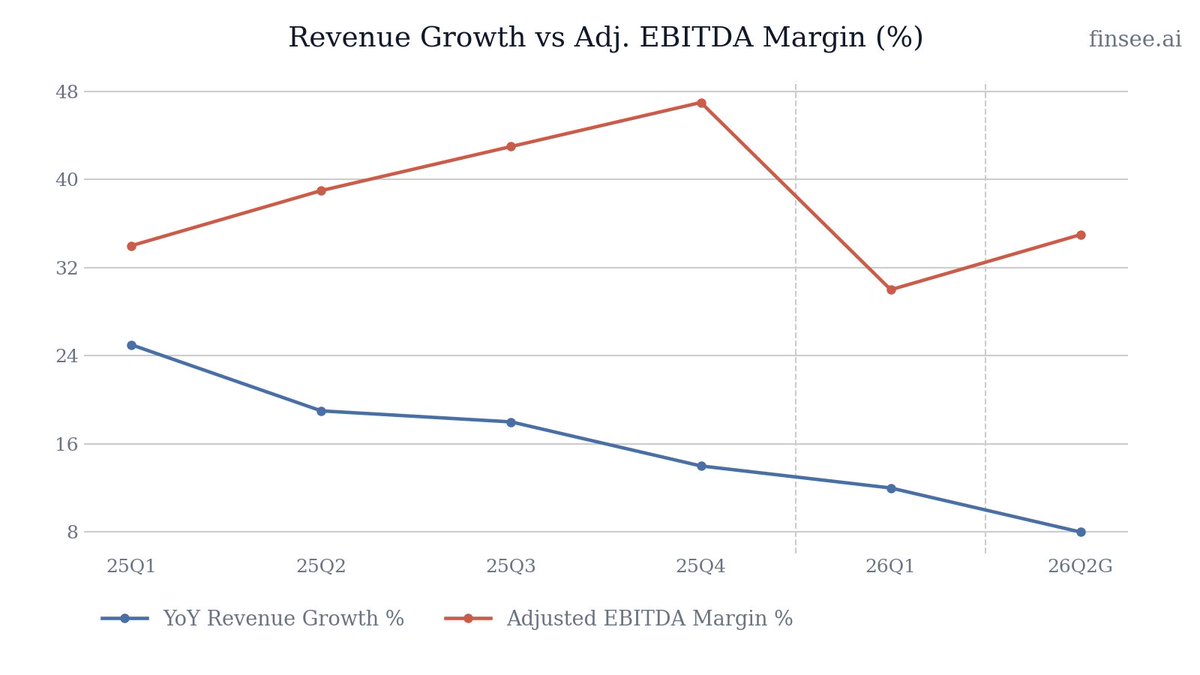

$TTD Q1 2026 earnings: Growth Decelerates as AI Narrative Outpaces Financial Reality

The Trade Desk delivered a sobering Q1. While management praised strategic upgrades and AI innovations, the numbers paint a picture of a business rapidly cooling off. Revenue grew 12% YoY to $689 million, marking the fifth consecutive quarter of top-line deceleration. More concerning is the Q2 guidance: 'at least $750 million' implies a drop to just 8% YoY growth. Profitability is also reversing: Adjusted EBITDA margin shrank to 30% from 34%, and a spike in the tax rate drove Net Income down 21% YoY. The gap between the company's visionary AI rhetoric and its decelerating financial engine is becoming impossible to ignore.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐒𝐭𝐢𝐜𝐤𝐲 𝐄𝐜𝐨𝐬𝐲𝐬𝐭𝐞𝐦 — Customer retention remained over 95% for over a decade. Advertisers aren't leaving; they are simply slowing their spend growth in a challenging macro environment.

• 𝐔𝐧𝐥𝐨𝐜𝐤𝐢𝐧𝐠 𝐍𝐞𝐰 𝐁𝐮𝐝𝐠𝐞𝐭𝐬 — Integrations with LinkedIn for B2B Connected TV (CTV) activation and Dollar General for retail media show TTD is successfully expanding its addressable market beyond traditional consumer brands.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐮𝐬𝐭𝐚𝐢𝐧𝐞𝐝 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐨𝐧 — Growth has stepped down sequentially for five straight quarters (25% to 8% implied). The hyper-growth narrative is breaking as the company approaches single-digit expansion.

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧 — Adjusted EBITDA and Net Income margins are both contracting. Operating expenses, particularly direct platform costs, are rising faster than revenue, destroying operating leverage.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴

Bearish. The persistent deceleration in revenue growth combined with shrinking margins fundamentally challenges The Trade Desk's premium valuation. AI product launches are encouraging but are not currently translating into top-line acceleration.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴🔴 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐢𝐬 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐑𝐚𝐩𝐢𝐝𝐥𝐲 [NEW]

The most critical metric for TTD—revenue growth—is failing to hold up. After printing 25% growth a year ago, the rate has decelerated in every subsequent quarter: 19% -> 18% -> 14% -> 12% today. The Q2 guidance implies a further drop to roughly 8%. Management previously cited macro headwinds in CPG and Auto verticals, but a drop to single digits suggests deeper structural friction or market saturation.

🔴 𝐂𝐨𝐬𝐭 𝐨𝐟 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐢𝐬 𝐎𝐮𝐭𝐩𝐚𝐜𝐢𝐧𝐠 𝐒𝐚𝐥𝐞𝐬 [NEW]

Platform operations (Cost of Revenue) surged 27% YoY to $182M. Because this grew more than twice as fast as revenue ( 12%), gross margins are compressing. TTD is paying significantly more to operate its platform per dollar of revenue generated, which inherently limits bottom-line expansion.

🟢 𝐀𝐠𝐞𝐧𝐭𝐢𝐜 𝐀𝐈 𝐑𝐨𝐥𝐥𝐨𝐮𝐭 𝐆𝐚𝐢𝐧𝐢𝐧𝐠 𝐓𝐫𝐚𝐜𝐭𝐢𝐨𝐧

The rollout of 'Koa Agents' marks a shift toward agentic AI capabilities for media planning and optimization. Stagwell signing on as the first partner validates the demand for automated, objective tools that reduce the manual workload for agency buyers.

🟢 𝐂𝐫𝐚𝐜𝐤𝐢𝐧𝐠 𝐭𝐡𝐞 𝐁𝟐𝐁 𝐚𝐧𝐝 𝐋𝐢𝐯𝐞 𝐒𝐩𝐨𝐫𝐭𝐬 𝐌𝐚𝐫𝐤𝐞𝐭𝐬 [NEW]

TTD secured two major strategic wins: LinkedIn selected TTD as its first DSP partner for B2B data activation on Connected TV, and Paramount announced live, in-game programmatic buying for marquee sporting events. These are premium, high-CPM environments that competitors struggle to access objectively.

⚪ 𝐔𝐧𝐢𝐟𝐢𝐞𝐝 𝐈𝐃 𝟐.𝟎 (𝐔𝐈𝐃𝟐) 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐑𝐞𝐚𝐜𝐡𝐢𝐧𝐠 𝐂𝐫𝐢𝐭𝐢𝐜𝐚𝐥 𝐌𝐚𝐬𝐬

The industry's shift away from third-party cookies continues to benefit TTD. The integration of MetaRouter to synchronize UID2 and conversion events in real-time strengthens the connection between consented identity and activation, preserving ad relevance.

🔴 𝐁𝐞𝐥𝐨𝐰-𝐭𝐡𝐞-𝐋𝐢𝐧𝐞 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬 𝐂𝐫𝐮𝐬𝐡 𝐍𝐞𝐭 𝐈𝐧𝐜𝐨𝐦𝐞 [NEW]

Despite a 22% increase in Operating Income, GAAP Net Income reversed, falling 21% YoY to $40M. This was driven by two major non-operating items: Interest income dropped by $9M as cash yields normalized, and the provision for income taxes spiked 55% to $39M. The effective tax rate nearly reached 50% in the quarter.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐒𝐭𝐨𝐜𝐤-𝐁𝐚𝐬𝐞𝐝 𝐂𝐨𝐦𝐩𝐞𝐧𝐬𝐚𝐭𝐢𝐨𝐧 (𝟐𝟔𝐐𝟏): $109.0 million

SBC remains a massive expense, consuming 15.8% of total revenue. While it appears to have declined from $128.3M last year, the entirety of the drop is due to a scheduled reduction in the CEO's long-term performance grant (down from $24M to $5M). Core employee SBC actually increased.

𝐂𝐚𝐬𝐡 𝐔𝐬𝐞𝐝 𝐢𝐧 𝐒𝐡𝐚𝐫𝐞 𝐑𝐞𝐩𝐮𝐫𝐜𝐡𝐚𝐬𝐞𝐬 (𝟐𝟔𝐐𝟏): $164 million

The company continues to use cash to offset heavy dilution from SBC. They have $327 million remaining on their authorization. However, with free cash flow generation historically tight relative to SBC levels, the ability to meaningfully shrink the float remains constrained.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: At least $750 million

Decelerating. The implied YoY growth rate is just 8.1% (compared to $694M in 25Q2). This is a severe step down from the 12% growth achieved in 26Q1 and suggests the macro weakness in verticals like CPG and Auto is intensifying, or competitive pressures are mounting.

𝐐𝟐 𝟐𝟎𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀: Approximately $260 million

Reversing. This figure is lower than the $271 million generated in the same quarter last year, implying a YoY contraction of roughly 4%. The implied EBITDA margin of 34.7% marks a nearly 450-basis-point compression versus 25Q2's 39.0% margin. The company is sacrificing profitability to chase slowing growth.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐂𝐨𝐬𝐭 𝐨𝐟 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧

Platform operations expense grew 27% YoY, significantly outpacing the 12% revenue growth. What specific infrastructure or data costs are driving this margin compression, and when will we see operating leverage return?

𝐒𝐢𝐧𝐠𝐥𝐞-𝐃𝐢𝐠𝐢𝐭 𝐆𝐫𝐨𝐰𝐭𝐡 𝐇𝐨𝐫𝐢𝐳𝐨𝐧

Q2 guidance implies growth slowing to 8%. How much of this is driven by the previously mentioned macro weakness in CPG/Auto versus structural market saturation or increased competitive discounting from walled gardens?

𝐓𝐚𝐱 𝐑𝐚𝐭𝐞 𝐍𝐨𝐫𝐦𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧

The provision for income taxes jumped 55% despite lower net income, resulting in an effective tax rate near 50%. What drove this spike, and what is the expected normalized tax rate for the remainder of FY26?

2

1,713

Apr 27

sharing my alt cupcakes #今週の創造物 #이번주_떡냥이 #thisweekscreation #honkaistarrail

UID1: 841522585 (anaxa, aventurine, sunday)

UID2: 841475854 (castorice, aventurine, phainon)

3

3

4,024

Mar 25

5. There is no universal ID (plan for many)

The "one ID to replace cookies" didn't happen.

Instead:

– Multiple frameworks (UID2, RampID, ID5, etc.)

– Limited interoperability

1

33

Mar 6

Let me guess, Jeff.

They’re using UID2’ and believe in ‘OpenPath as the best direct connection to Advertisers’…

Sighhh

2

89

$TTD: Evercore sees Gen-AI boosting ad spend as Trade Desk jumps on OpenAI reports

Evercore ISI notes Trade Desk's shares are trading up about 18% intraday, likely driven by reports the company has held ad partnership discussions with OpenAI, and CEO Jeff Green's recent purchases of stock totaling $150M. Relative to Trade Desk's 2025 gross spend of $13.4B, the firm believes Generative AI engines could be a significant source of incremental gross spend. Early structural features of OpenAI's ad offering such as CPM pricing appear to play to the company's strength in inventory valuation, though Evercore believes its decisions on whether to partner with publishers generally hinge on data availability and Trade Desk's ability to add value via fully decisioned bidding. While the firm would anticipate that a partnership featuring UID2 integration in the near term might be relatively unlikely given user privacy/data concerns, it thinks some level of audience matching could be on the table. Evercore has an Outperform rating on Trade Desk with a price target of $35.

1

4

941

Mar 5

트레이드 데스크 급등 이유

TTD 오늘 급등 핵심은 OpenAI와의 광고 파트너십 보도입니다.

The Information이 3월 4일 보도한 바에 따르면, OpenAI가 ChatGPT에 광고를 판매하기 위해 The Trade Desk와 초기 협의를 진행 중이며, 이를 통해 올해 소비자용 ChatGPT 매출을 170억 달러로 두 배 늘릴 수 있을 것으로 전망했습니다. 이 소식에 TTD 주가가 시간외 거래에서 9.3% 급등했고, 오늘 정규장에서도 19.19% 상승으로 이어진 겁니다.

추가 촉매도 있었는데, 같은 날 TTD가 OpenTTD라는 새 플랫폼을 공개했습니다. UID2, OpenPath 등 자사 데이터 솔루션을 광고주에게 통합 제공하는 인프라입니다.

차트 맥락에서 보면 상당히 의미 있는 반등입니다. 고점 $91.45(08/07)에서 최저 $21.08(02/26)까지 약 77% 폭락한 상태에서, RSI가 25 부근 극심한 과매도 구간이었고, 숏 이자율이 약 10%에 달해 숏스퀴즈 가능성도 겹친 상황입니다.

다만 리스크도 명확합니다. 시총이 약 122억 달러로, S&P 500 잔류 기준인 227억 달러를 크게 하회해서 인덱스 제외 리스크가 상존하고, OpenAI 협의는 아직 초기 단계라 실제 매출 기여까지는 불확실성이 큽니다. 기술적으로는 $30 부근이 이전 지지/저항 전환선이라 여기서 안착 여부가 관건입니다.

32

436

Mar 1

The real kicker is the first-party data. Unlike competitors like $TTD that rely on third-party frameworks and industry adoption of UID2, $ZETA owns its entire data ecosystem.

By controlling the data cloud and the activation layer, Zeta is immune to the 'cookie-less' headwinds that are currently stalling the rest of the SaaS ad-tech sector. It’s a closed-loop advantage that the market is still deeply underestimating.

Mar 1

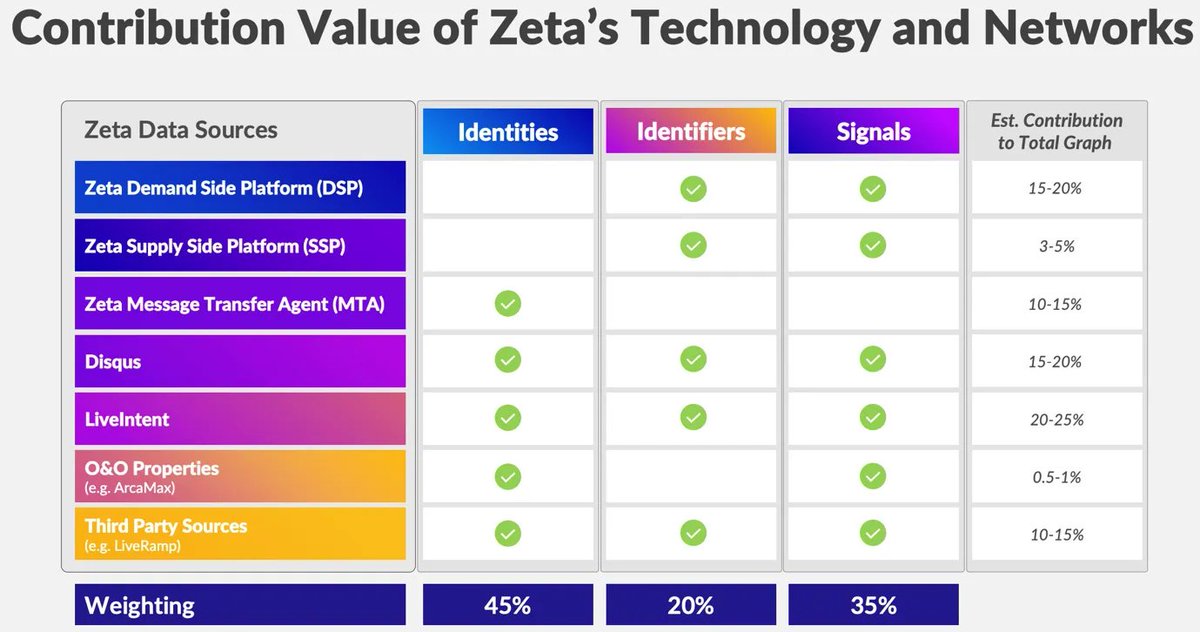

$ZETA has a huge Data Advantage!

- Demand Side Platform

- Supply Side Platform

- Marketing Activations

- Publisher Monitazation Platform

From these sources, $ZETA gets data on:

- 500M people globally

- 200M people in the US

- 1.5B emails

- 1 trillion signals per month

- 850 audience categories

- 10B transactions a year

1

2

270

Feb 26

But seriously, it might be. If you are a CTV OS and vibe to OpenPath and UID2 - are you “on Ventura”?

1

3

179

Feb 25

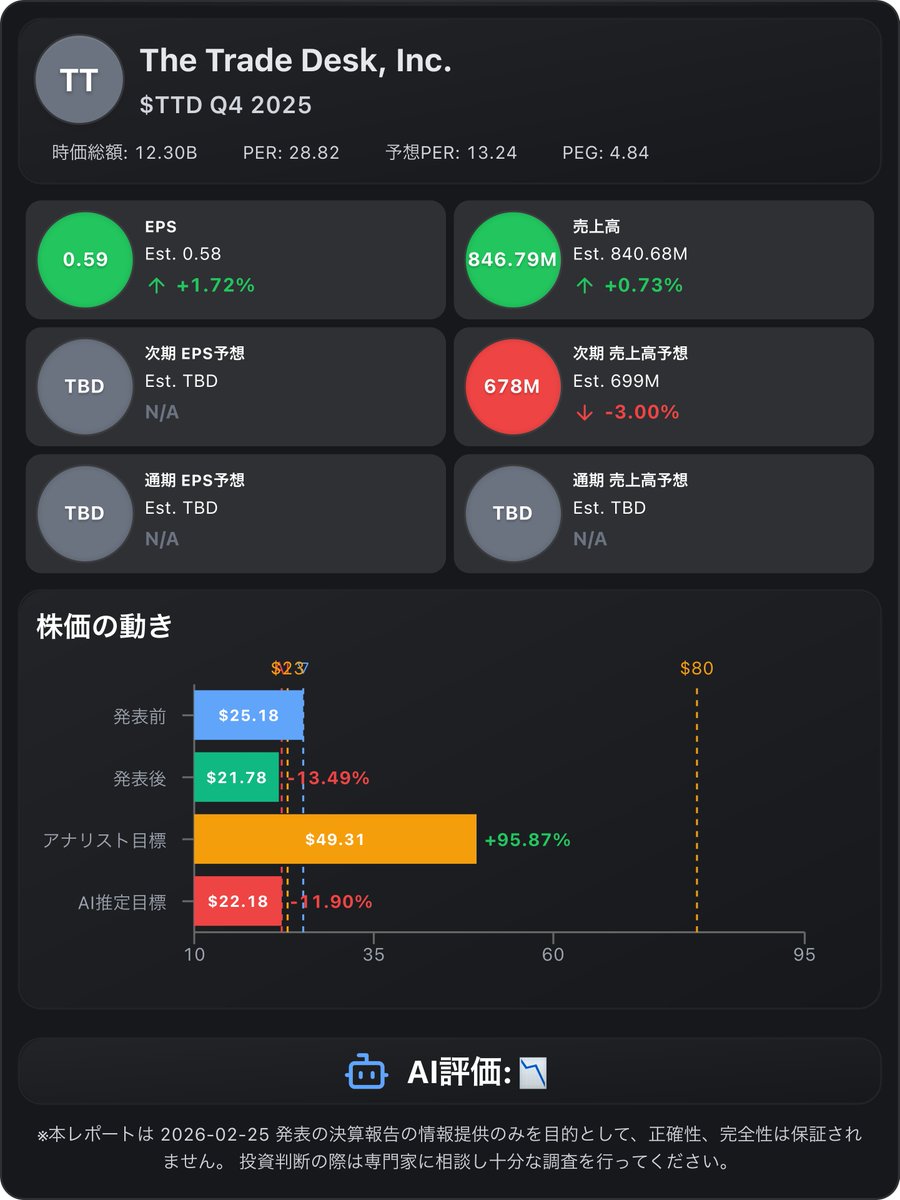

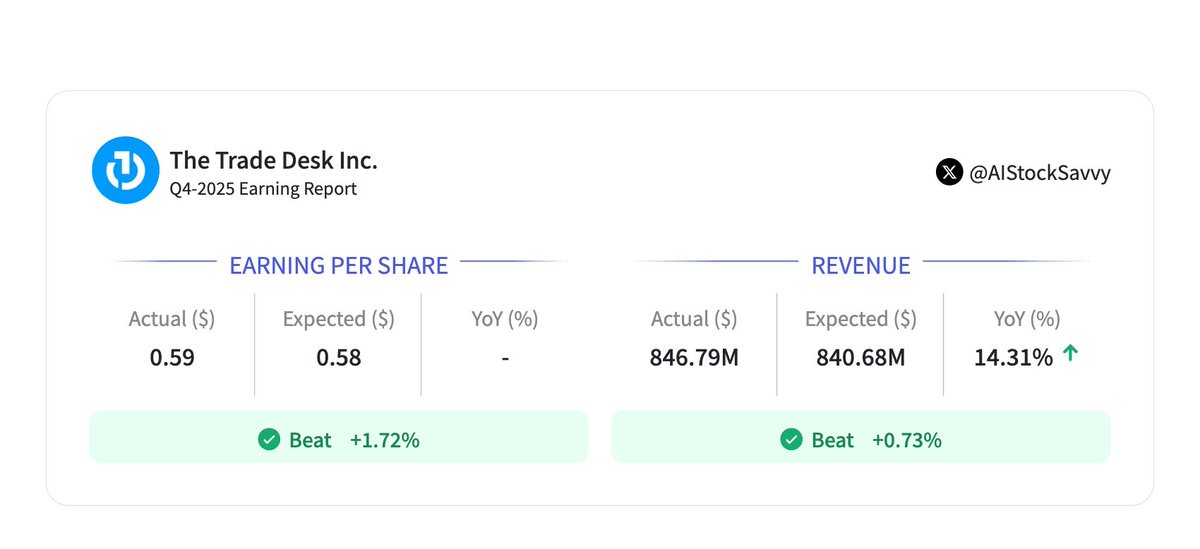

💡 The Trade Desk, Inc. $TTD Q4 2025決算 2026-02-25

💰 今四半期業績

- 🟢 EPS:$0.59 (予想$0.58)

- 🟢 売上高:$846.79M (予想$840.68M)

📊 重要指標

- 🟢 Adjusted EBITDA:$400M (マージン47%, 前年同期47%横ばい)

- 🟢 通期売上高 (FY2025):$2.90B (YoY 18.5%)

- 🔴 Non-GAAP純利益 (Q4):$284M (前年同期$297M, YoY-4.2%)

- 🟢 営業キャッシュフロー (FY2025):$993M (前年$739M, YoY 34.3%)

- 🟢 顧客継続率:95%超 (12年連続)

- 🟢 自社株買い (FY2025):$1.4B (平均取得価格$52.60), 追加$350M承認 (残枠$500M)

- 🔴 Q1 2026売上高ガイダンス:$678M以上 (Est. $699M) — コンセンサス大幅下回る

📊 次四半期ガイダンス

- 🔴 売上高:$678M (予想$699M)

📍決算内容の注目ポイント

- FY2025通期売上高$2.9Bを達成し、YoY 18.5%の成長を記録。Adjusted EBITDA $1.20Bでマージン41%を維持

- 自社株買いを積極化し、FY2025で$1.4B(平均$52.60)を買戻し。取締役会が追加$350Mを承認し、残枠$500Mに拡大

- Kokai(次世代AI広告プラットフォーム)、リテールデータ、サプライチェーン領域での革新を推進。PubDeskやIntuit SMB MediaLabとの連携を発表

- NBCUniversalが2026年冬季五輪のプログラマティック広告アクセスをThe Trade Desk経由で提供。CTV領域の拡大が継続

- Q1 2026売上高ガイダンスが$678M以上とコンセンサス$699Mを約3%下回り、Adjusted EBITDAガイダンス$195Mもコンセンサス$224Mを大幅に下回る

🤵♂️CEO (Jeff Green) コメント

「The Trade Deskは2025年に$2.9Bの売上高を達成し、引き続き高い収益性とキャッシュフローを創出しました。マクロの不確実性の中で、当社史上最も意義のあるアップグレードを実行しました。広告主が安価なリーチよりも測定可能な成果とデータドリブンな意思決定を重視する傾向が強まる中、客観的プラットフォームとしての当社の役割はますます重要になっています。Kokai、リテールデータ、サプライチェーンにおける継続的なイノベーションにより、2026年以降もグローバル広告市場でさらなるシェア獲得に向けて好位置にあります。」

🔍 主要ファンダメンタルズ指標

- 時価総額: 12.30B

- PER: 28.82

- Forward PER: 13.24

- PEG: 4.84

🎯市場評価

- 株価 (発表前): 📈$25.175 (0.94%)

- 株価 (発表後): 📉$21.78 (-13.49%)

- 決算前アナリスト目標株価: $49.31 ($80 ~ $23) Buy

- 決算総合サプライズ率 (AI推定): 😥-4.82%

- 決算後目標株価 (AI推定): $22.18

🤖 決算まとめるくん(AI)コメント

「The Trade Deskの Q4 2025決算は、今期実績においてはEPS・売上高ともにアナリスト予想を小幅に上回り、堅調な着地を示しました。Non-GAAP EPS $0.59はコンセンサス$0.58を上回り、売上高$846.79Mも予想$840.68Mを超過。Adjusted EBITDAマージン47%は前年同期と同水準を維持し、収益性の安定が確認されます。

一方、市場が最も注目したのはQ1 2026ガイダンスの弱さです。売上高ガイダンス「$678M以上」はコンセンサス$699Mを約3%下回り、Adjusted EBITDAガイダンス$195Mもコンセンサス$224Mを約13%下回りました。これはマクロ経済の不確実性に加え、Q1が季節的に広告需要が低迷する時期であることを反映していますが、市場の期待を大きく裏切る水準です。

構造的な観点では、FY2025通期売上高$2.90B(YoY 18.5%)は堅実ですが、Q4単体のYoY成長率は 14.3%と過去の 22%(Q4 2024)から明確に減速しています。成長鈍化トレンドが鮮明になりつつある点は、PER 28.82倍、PEG 4.84倍という現在のバリュエーションに対する下方圧力となり得ます。

積極的な自社株買い(FY2025で$1.4B、追加$350M承認)は株主還元姿勢として評価できますが、平均取得価格$52.60は現在株価の約2倍であり、資本配分の効率性に疑問が残ります。Kokai、CTV、UID2等の戦略的取り組みは中長期の成長ドライバーとして有望ですが、短期的にはガイダンス未達懸念が支配的であり、決算後の時間外での大幅な株価下落はこの懸念を反映したものと考えられます。 評価は📉ポヨ」

🏢 The Trade Desk, Inc. 概要

- セクター: テクノロジー

- 特徴: 広告主向けプログラマティック広告のセルフサービス型クラウドプラットフォームを提供するアドテク企業

4

1

34

9,710

Feb 25

$TTD | 𝐓𝐡𝐞 𝐓𝐫𝐚𝐝𝐞 𝐃𝐞𝐬𝐤 𝐐𝟒 𝐄𝐚𝐫𝐧𝐢𝐧𝐠𝐬 𝐑𝐞𝐩𝐨𝐫𝐭: Revenue: $847M (↑ 14% YoY) | GAAP EPS: $0.39 | Adjusted EPS: $0.59

👉 𝐁𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐇𝐢𝐠𝐡𝐥𝐢𝐠𝐡𝐭𝐬:

➤ Delivered 𝟐𝟎𝟐𝟓 𝐫𝐞𝐯𝐞𝐧𝐮𝐞 of $2.9B with continued strong profitability.

➤ Generated 𝟐𝟎𝟐𝟓 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐁𝐈𝐓𝐃𝐀 of $1.2B, maintaining 41% margin.

➤ Achieved 𝟐𝟎𝟐𝟓 𝐠𝐫𝐨𝐬𝐬 𝐬𝐩𝐞𝐧𝐝 of $13.4B across platform.

➤ Maintained customer retention above 𝟗𝟓% for twelfth consecutive year.

➤ Launched 𝐏𝐮𝐛𝐃𝐞𝐬𝐤 to enhance publisher transparency and pricing insights.

➤ Expanded UID2 ecosystem with 𝐃𝐚𝐭𝐚𝐛𝐫𝐢𝐜𝐤𝐬, 𝐇𝐢𝐠𝐡𝐓𝐨𝐮𝐜𝐡, and Spotify integration.

➤ Strengthened CTV footprint including 𝐍𝐁𝐂𝐔 2026 Winter Olympics programmatic access.

➤ Repurchased $1.4B shares in FY25 at average price of $52.60.

➤ Approved additional $350M buyback, totaling 𝐀𝐮𝐭𝐡𝐨𝐫𝐢𝐳𝐞𝐝 $500M.

➤ Recognized in 𝐅𝐨𝐫𝐭𝐮𝐧𝐞 100 Fastest Growing Companies 2025.

👉 𝐂𝐄𝐎 𝐒𝐭𝐚𝐭𝐞𝐦𝐞𝐧𝐭:

“We delivered $2.9 billion in revenue in 2025 while continuing to generate significant profitability and cash flow,” said Jeff Green, Co-Founder and CEO of The Trade Desk. “With continued innovation across Kokai, retail data, and the supply chain, we are well positioned to capture greater share of the global advertising market in 2026 and beyond.”

8

3,020