Honteux!

Piège fielleux tendu en fin d'émission exigeant une réponse rapide en posant une question sur base de faits tronqués.

Fuite du "journaliste" passant directement à autre chose quand @MLP_officiel explique la laïcité à géométrie variable défendue par le maire d'Ivry.

3

There’s a cost to everything you do and don’t do.

Every choice forecloses something, and the man who pretends otherwise is just hiding his sacrifices from himself. The cost is always there and the only variable is whether you're conscious of it.

21h

Evlenirsen pişman olursun. Evlenmezsen de pişman olursun. Çocuk yapsan da yapmasan da pişman olursun. Kierkegaard bunu 200 yıl önce şöyle söylemiştir:

"Neyi seçersen seç pişman olursun. Çünkü sorun tercihlerinde değil yaşanmamış bir hayatı romantize etmendir. İnsan her daim gidilmemiş bir yolu cazibeli ve gizemli bulur. Bu yüzden mesele en doğru seçimi yapman değil. Hangi pişmanlıkla yaşayacağını seçip karar vermendir."

Sen neye karar verdin?

4

Il est étonnant que vous ne parliez de ce qui a précédé et motivé cette réaction ! Laïcité à géométrie très variable…

1

The one thing we do know… they can’t arrest everyone. Their policing and court systems are already overwhelmed.

Want real action. Stop using your phone for all things. Delete all your apps. Use your home computer for email and apps. There a way to bring it all down… because we as the people are the variable

2

C’est a hurler de rire comment vous vous embourbez tous dans votre laïcité a géométrie variable. Il vous a bien eu cet élu Rn.

Le RN sous son vrai jour : un ennemi et un danger pour la République , bafouant sans vergogne le principe constitutionnel de laïcité : honteux !

it's also an SEP meeting so you get the dot plot alongside the rate decision. warsh's first presser plus updated projections makes june 17 a two-variable event for BTC, not just the rate call.

5

Not all #fruits and #vegetables are equal when it comes to heart #health, our research shows theconversation.com/not-all-… the study my colleagues and I conducted, we specifically investigated flavanols. This group of bioactive compounds are found in many plant-based foods, including tea, apples and berries. Flavanols have been shown to reduce the risk of heart disease. About 500mg of flavanols per day are enough for most people to see #health benefits from flavanols. We wanted to find how many people eat at least 500mg of flavanols per day – and whether these are the people who eat their five-a-day and follow dietary recommendations. To do this, we did not rely on food diaries or dietary questionnaires – methods that are known to be unreliable. People often forget what they’ve eaten, and the flavanol content in food is very variable.

7

I never see a Mr.Beast video ever. But it is worth nothing it's view count and like/dislike ratio as well as comments

Because I'm pretty sure the data for a healthy video is out there that uses like/dislike, viewers, and comments as a variable

Then we'd really know

975

Muro retweeted

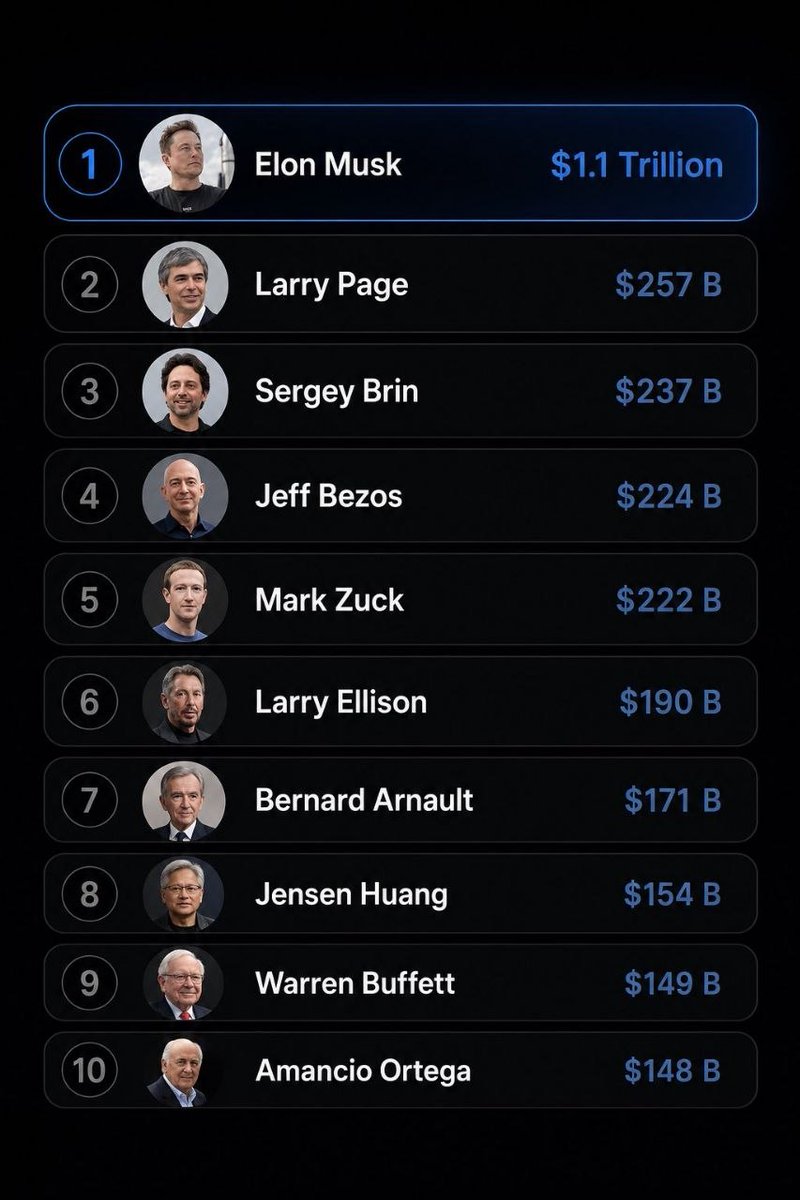

Almost 0 women work 60 hours a week which is required to be in this list.

Women’s IQ is not as variable as men’s and is centered around the mean. Which means the 140 IQ required to be in this list is 47:1 men.

Women focus on people. Men focus on things. As a result a woman doing her job can affect a few dozen people an hour. A man focusing on things can build something that benefits a billion people an hour.

Of course this will offend leftists and feminists but it is none the less true and explains exactly why there are 0 and everything that powers civilization was invented, brought to market and made successful by men and that won’t change any time soon if ever.

133

372

4,480

319,003

The more interesting TermMax update is not just fixed rates

It is the shift in what can sit underneath fixed-rate credit

With @TermMaxFi expanding from crypto collateral into tokenized stock collateral via Ondo Global Markets on BNB Chain, the product starts moving closer to onchain securities financing

That matters because fixed borrowing cost becomes more valuable when the collateral itself starts looking less like pure crypto beta

Variable-rate lending works fine for reactive capital

But tokenized equities, curated vaults, fixed maturities, and predictable borrow costs point toward a different market structure

One where DeFi credit is less about chasing utilization spikes and more about pricing duration, collateral quality, and balance sheet efficiency

The overlooked insight is that fixed-rate lending becomes more important as onchain collateral becomes more institutional

7

7m

Depends. Cannabis tolerances are much more variable than alcohol tolerances, and there are some people that wouldn’t even feel one of these. But we do have 5, 10, 25, and 50mg options available for lower tolerances, too! 💚 3chi.com/product-category/dr…

6

The histamine response on cagrilintide is documented and the fact it resolved by dose 3 without antihistamines tracks with what others report, likely mast cell adaptation rather than the TA1 or KPV, though isolating the variable when you changed three things the same week is impossible.

The food noise observation on top of 3.5mg reta is the interesting part. That's a high reta dose to still be feeling hunger through, and cagri hitting a different mechanism explains why the combo is getting attention.

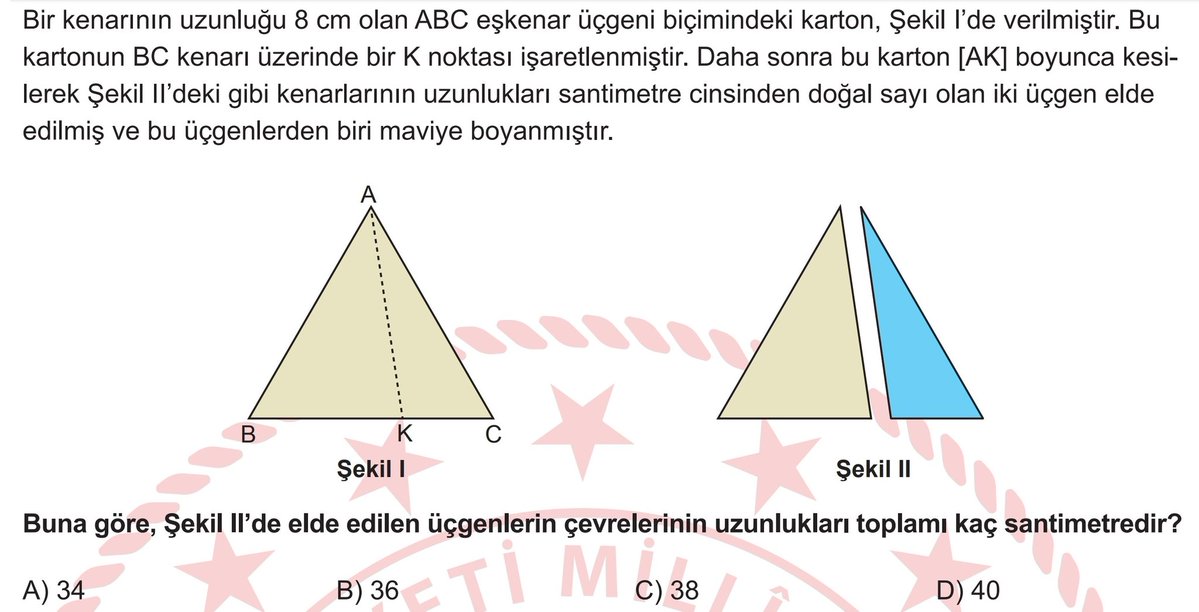

One question from Saturday’s LGS exam (Türkiye’s nationwide high school entrance exam) struck me as a perfect illustration of the gap between procedural skill and true mathematical thinking.

There’s a long, safe way to solve it: define a variable, apply relevant theorems or properties, check cases one by one, and grind toward the answer. It’s fully correct, but calculation-heavy.

There’s also a shorter path: truly understand what the question is asking. Instead of computing every intermediate length, isolate the single critical length that determines the outcome. Then use its possible range (together with the fact that it must be a natural number) to reach the answer far faster.

In the first approach, procedural skill leads. In the second, mathematical thinking takes center stage.

I shared the question with advanced models on both Claude and ChatGPT. Initially, both defaulted to the zero-risk, calculation-heavy path. Only when I noted the 2-minute time limit did they pivot toward the more efficient, insight-driven method.

Of course, this isn’t a rigorous scientific test. But it was telling.

The AI’s first response felt less like a deliberate decision and more like a reflex. Calculation is fast and cheap for them, the long route costs almost nothing. For students under real time pressure, though, those extra minutes are everything.

So I get why questions like this appear in high-stakes exams. They don’t just test calculation fluency; they test whether students can think.

But that leads to the bigger question: If we expect middle schoolers to reason abstractly and choose optimal approaches under pressure, are we systematically teaching those skills?

I don’t know.

I don’t have the answer.

Yet this question reinforced something important for me: In a world where technology advances relentlessly, one of the most vital skills may no longer be solving problems, but knowing how to approach them wisely before you even begin.

(Disclaimer: I’m not an educator, nor do I have formal expertise in mathematics. I’m writing simply as someone curious about math.)

#LGS2026 #LGS

27

Wen the variable we aren’t allowed to talk with Chainlink adjusts accordingly, SmartCon will be off the rails. I’m hoping it’s finally this year. $LINK

1

6

El furor por invertir se dispara entre los jóvenes y la mayoría se decanta por la renta variable salamancahoy.es/economia/mer…

23

Dear Olayinka,

Why Islamic Banking is Interest Banking, in a Different Dress:

Having seen the back and forth between yourself and the Chief, I've been instructed to give an extensive answer as this is a topic he is extremely knowledgeable about.

Per [ZE's Economic Analysis and Research Outfit Zero Equilibrium's] (@0Equilibrium ) estimate for 2025–2026, “profit sharing” averaged between 15% and 30%, depending on; scale, risk, duration, volume, sector and company specific risk assessment (inflation, liquidity, insolvency and exchange rate risks). Fidelity Bank (and other conventional interest-based banks) “interest rates” ranged from 20%-35%.

[ZE's estimate is inferred from the Banks financial statement, we derived the average profit rates from the Banks Income Statement - it's publicly available- First we subtracted the cost of funds from financing income (Revenue) to get the net finance margin. Feel free to challenge me this methodically, I always concedde to data or superior data analysis.]

Same Objectives and Outcomes, Different Contractual Language/Formating:

Now, since the resulting pricing often almost converge, (ormore accurately are within inches of each other) cause again, they have to price in the same risks. Whilst Fidelity is looking for your deposit to pay you an interest lower than TBills and bonds, Jaiz is also raising a variant of Musharakah financing to invest in FG Sukuk Bonds then sharing the "profit" with the customer just like fidelity.

[Fun fact, for over almost half a decade, FG Sukuk Bond Yields have been fixed (please fact check me. Meaning the only difference between FGN Sukuk and NTBs and Interest Bonds is the name, liquidity, duration and flexibility. What business did the FG and Islamic Insitituional, Retail and Individual Investors/Customers who's funds were used. Surely you must now concede to superior knowledge]

Identical (Outcome) Foundational Mechanics:

With the average lower and higher band in the past 360 days for both banks are literally just 5% apart, and with similar risk assessments made to arrive at that rate (profit sharing or interest rates), Jaiz Bank is basically not too foundationally dissimilar from fidelity.

One has a standardized process, the other am variable one, but the share of your income paid either as interest or profit sharing are not only close on average but also determined in similar ways. But the Methodology differs only in the contract language and structure.

Same Risks to Evaluate and Price Money(Loans):

Both Fidelity and Jaiz Bank bear the same risk. And have the same goal, with similar rules applied in both instances where a borrower is softening.

No Islamic Bank is forgiving a loan entirely except the company goes bankrupt. Same with commercial banks. If you don't a make profit, and go bankrupt, you're covered by law.

If you're just having a downtime both institutions (Jaiz and Fidelity) would provide ext nations, or even take concessions.

So tell me again, how are they different in essence again? For they are foundationally similar in outcome, despite the contractual divergence.

Irrefutable Fact:

Islamic and conventional banking are structurally different, but very much more economically similar, if not identical, than many proponents of either system are willing to admit.

— Zero Equilibrium® Economics.

You have no simple idea of Islamic economics and finance just sit it out with the grandstanding

1

7

Bits from our kayak expedition in Barkley Sound🦭

The pictures hardly do this place justice. Absolutely stunninggggg views everywhere you look, and we lucked out with amazing weather too. This time of year can be so variable so I was definitely grate...

2