Joined August 2025

- Tweets 106

- Following 30

- Followers 7,654

- Likes 648

21 Photos and videos

Jun 12

[Alpha Test Log 003] In this sprint, we’re making deposits and withdrawals effortless.

We know that moving money on and off exchanges can be onerous. Regional limits, hidden complexity, and too many platforms overcomplicate the process.

We’re putting an end to the friction:

🔸Deposit and withdraw fiat by debit card, credit card, bank transfer, Apple Pay, or from an exchange. Options vary by region.

🔸Deposit and withdraw crypto from any wallet, on any chain.

Pressure testing for global release continues.

5

3

32

2,120

Jun 8

A couple of news heavy weeks ahead. Here's a few things we've got our eyes on.

5

3

36

3,524

Jun 2

HelloTrade is moving to @monad.

We remain focused on our mission to make global capital markets more accessible to everyone around the world. We’re excited to build alongside the Monad team, who share our vision of bringing this future to life at global scale.

Stay tuned for further updates as we continue progressing through Alpha testing.

267

79

654

287,565

May 29

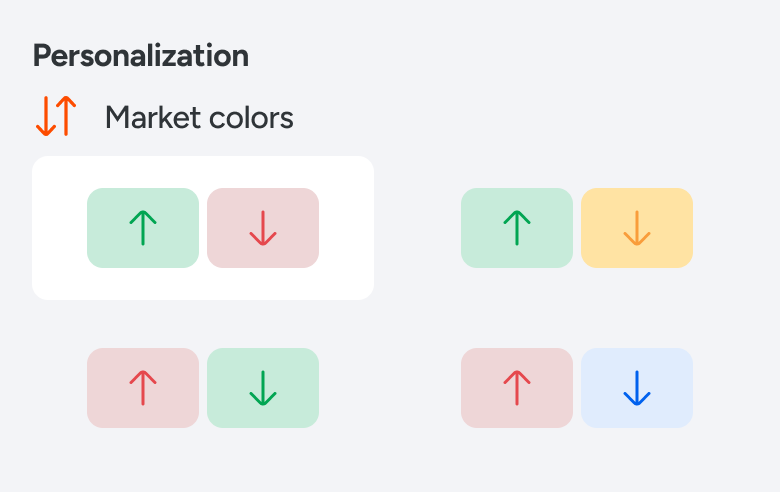

Allowing users to customize trading chart colors is one underrated detail we’ve added.

Did you know in some countries colors have different meanings?

Green ⬆ / Red ⬇ is the Western (US/Europe) standard

Red ⬆ / Blue ⬇ is the East Asian standard (China/Japan/Korea)

May 28

[Alpha Test Log 002] We continue to release more spots in our Alpha testing experience. With this sprint, we focused on user preferences and accessibility.

🔸Languages: Added support for 10 new languages.

🔸Market Colors: market colors adapted to regional preferences.

🔸Trade Screen Preferences: We’ve learned traders in certain regions want simplicity and ease of trading while others want sophistication with depth and data-rich experiences. We're building for both.

More coming as we adapt and pressure test our app for a global release.

12

3

49

6,614

May 28

[Alpha Test Log 002] We continue to release more spots in our Alpha testing experience. With this sprint, we focused on user preferences and accessibility.

🔸Languages: Added support for 10 new languages.

🔸Market Colors: market colors adapted to regional preferences.

🔸Trade Screen Preferences: We’ve learned traders in certain regions want simplicity and ease of trading while others want sophistication with depth and data-rich experiences. We're building for both.

More coming as we adapt and pressure test our app for a global release.

13

10

63

14,285

May 22

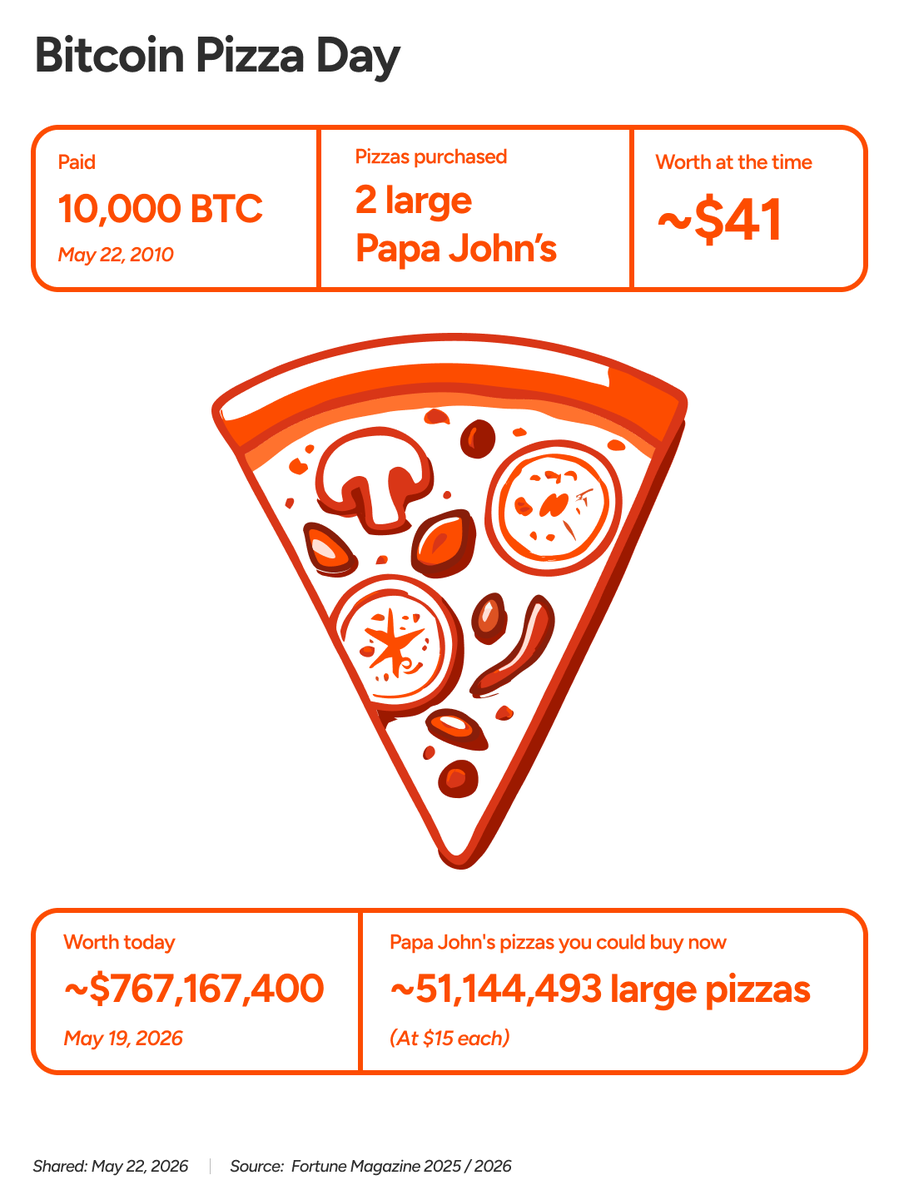

2010: Trading crypto required a forum, patience, and a stranger's goodwill 🍕

2026: It takes 2 taps on HelloTrade.

18

16

106

16,501

HelloTrade retweeted

May 21

I do not understand the debate between orderbooks, RFQ and AMM trading models for broad RWA perps.

Orderbooks are great for realtime liquidity and price discovery, this has been proven by weekend volumes on closed underlying markets. They are however very capital intensive to bootstrap when there is not natural demand in a market.

RFQs are better suited for large block trades to optimize for slippage, especially on less liquid markets. BlackRock's trading desk for example routes legs of large orders across many different algos on orderbooks and direct to counterparties via RFQ to reduce price impact. In crypto, daily RFQ volume on majors is massive, and on alts they are often used to preserve privacy and limit price impact.

AMMs and bonding curves are especially effective at bootstrapping liquidity as it is simple for anyone to market make (LP), but often comes at the expense of capital and market efficiency for both sides of a trade.

There is no one size fits all for any asset class or market. As a result, we will be supporting a multitude of trading models to address user's needs for breadth, depth, and 24/7 trading. This is only possible by owning the underlying infrastructure and allocating liquidity on books to the highest demand pairs.

Ideally an end retail user should end up with the best possible execution for the exposure vehicle and order of their choice.

May 20

CLOBs are not going to take us to the RWA promised land.

Today Hyperliquid owns the liquidity for a handful of RWA macro names. But outside the top 10 traded assets (which are ~90% of volume) liquidity falls off a cliff. When there's enough retail demand, order books can work. But "perps on everything" is a different problem, and TradFi solved it decades ago.

The answer isn't every venue rebuilding its own order book. That's not what Robinhood does, it's not what Schwab does, and it's not what DeFi should be doing either.

Building your own book for every asset means bootstrapping demand ticker by ticker, renting liquidity with subsidies, and ending up with thin markets that blow out 200x the moment news hits. It's like sucking the ocean of TradFi liquidity through a straw.

Variational skips all of it via the RFQ model. RFQ is how institutions like Dragonfly actually trade. In RFQ, dealers quote just-in-time and hedge on the primary venue as orders come in. This lets Variational mainline TradFi liquidity directly and mirror it on-chain. Margin in smart contracts, settlement in stablecoins, liquidity aggregated from the people who already trade on the biggest underlying markets, like the CME and NYSE.

It makes it permissionless to access the same depth and spreads the big boys get. With the cold start problem gone, new markets can ship at the speed of software.

By next year I expect RWA perps to be the biggest contract class on-chain, bigger than BTC and ETH perps combined. That's how crypto truly becomes the market for everything.

I believe the platform that wins that won't look like a traditional exchange.

Proud to lead Variational's $50M Series A.

Watch this space.

8

5

67

8,613

HelloTrade retweeted

May 20

HelloEng shipped 164 bugs fixes and UI/UX improvements in the last two weeks.

208 users across 8 countries participated in alpha testing.

Api integrations and load testing this week. Building momentum and focusing on our customers.

8

2

20

1,839

HelloTrade retweeted

May 14

Over the last 2 weeks, we’ve had long-time friends and traders extensively test the app, including many in-person feedback sessions.

One thing that has become very clear: identifying specific personas and tailoring the trading experience is very important.

Different traders value very different things. We’re spending a lot of time thinking about this.

May 14

[Alpha Test Log 001] Last week, we gave access to the Alpha version of our app to 100 traders all over the world.

Here’s what we learned:

🔸UI/UX is increasingly important even for crypto native users. The bar for trading applications is much higher than even one year ago.

🔸Top traders are looking for more sophisticated tools to better compete with professional investors.

🔸Users are excited about the opportunity to access a wide range of assets and exposure vehicles all from one app.

We’re feeling the momentum and alignment. If you have DMed us, you’re in our queue. We’re slowly releasing more Alpha tester seats. More to come 🫡

6

10

67

10,726

May 14

[Alpha Test Log 001] Last week, we gave access to the Alpha version of our app to 100 traders all over the world.

Here’s what we learned:

🔸UI/UX is increasingly important even for crypto native users. The bar for trading applications is much higher than even one year ago.

🔸Top traders are looking for more sophisticated tools to better compete with professional investors.

🔸Users are excited about the opportunity to access a wide range of assets and exposure vehicles all from one app.

We’re feeling the momentum and alignment. If you have DMed us, you’re in our queue. We’re slowly releasing more Alpha tester seats. More to come 🫡

23

33

205

34,832

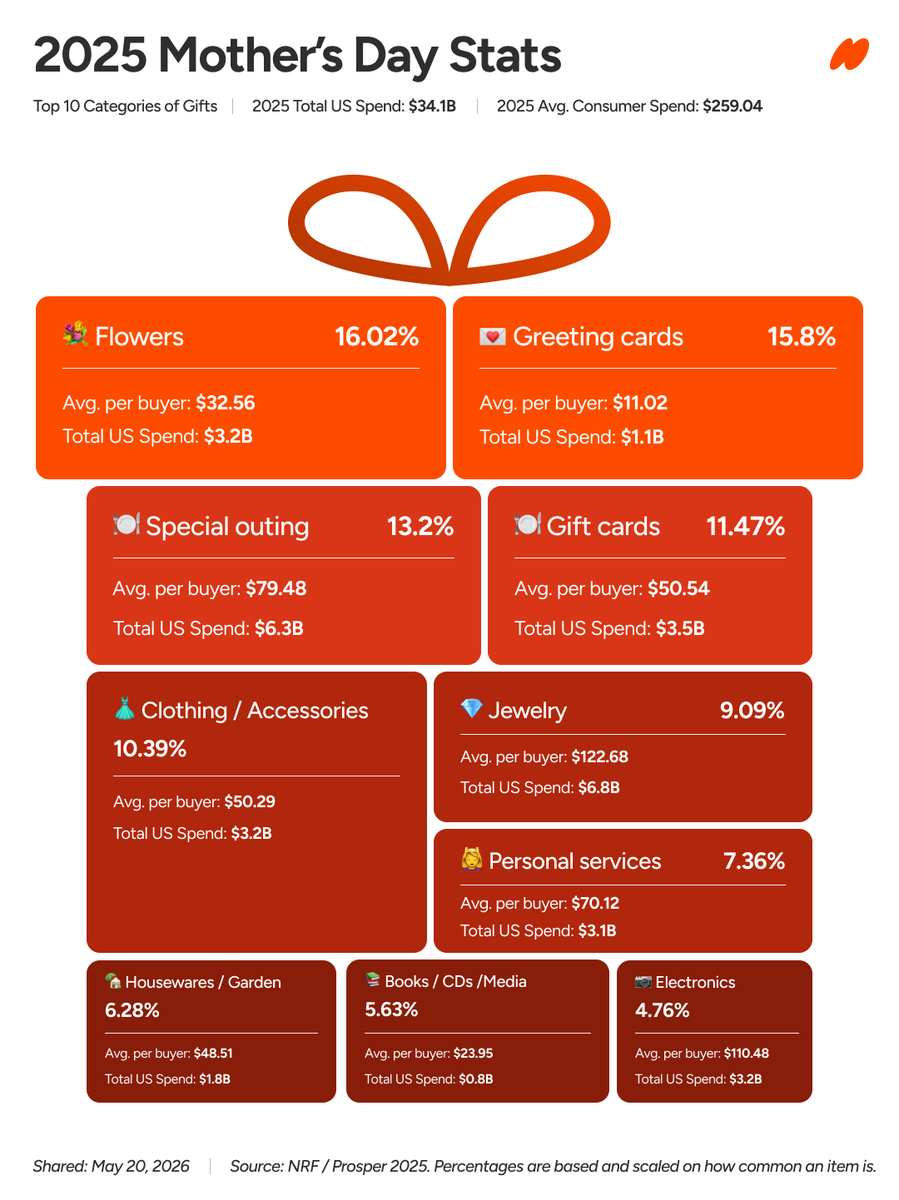

May 8

Everyone and their mothers are spending $34.1B on Mother's Day. That's $259 per person driving across flowers, jewelry, outings, cards.

Thank a mom this weekend with one of these gifts 🥰

15

28

221

34,357

May 6

Shoot us a DM if you're interested 👀

May 6

Who wants to test some stuff?

23

5

55

3,643

May 1

Apr 30

This GPT Image 2 prompt is going insanely viral right now.

“Redraw the attached image in the most clumsy, scribbly, and utterly pathetic way possible. Use a white background, and make it look like it was drawn in MS Paint with a mouse. It should be vaguely similar but also not really, kind of matching but also off in a confusing, awkward way, with that low-quality pixel-by-pixel feel that really emphasizes how ridiculously bad it is. Actually, you know what, whatever, just draw it however you want.”

3

4

43

2,915

Apr 29

April 2026 US Market Update: The Fed is leaving interest rates unchanged, maintaining the 3.50-3.75% rate. Volatility traders have clearer sight lines. Equities, crypto, commodities all moving.

4

2

23

1,332

HelloTrade retweeted

Apr 28

Markets shouldn't only be open when New York is awake.

Everyone deserves access to the same opportunities as the folks sitting in front of Bloomberg Terminals in midtown.

We're going to solve this, soon.

Apr 25

As a trader, I understand that sentiment doesn't take the weekend off. On Saturday mornings, I'm drinking my coffee and thinking about my positioning.

That weekend thinking drives markets, even if they're closed. @airlovsky and @ColinSt30481392 use calendar days for exactly this reason.

Trading infrastructure catching up with how cycles actually trade is pretty wild. NYSE announced a few months back that they're building 24/7 on-chain settlement for tokenized securities. This is a big deal. Non-futures traders will have access to #Gold, #silver, $GDX, $SPX when they're having their coffee on Saturday morning.

I'm going to have to start (slowly) updating my cycle counts.

businesswire.com/news/home/2…

5

3

18

2,584

Apr 1

Some of the biggest market moments have happened on April 1st... not even joking.

4

2

39

2,795

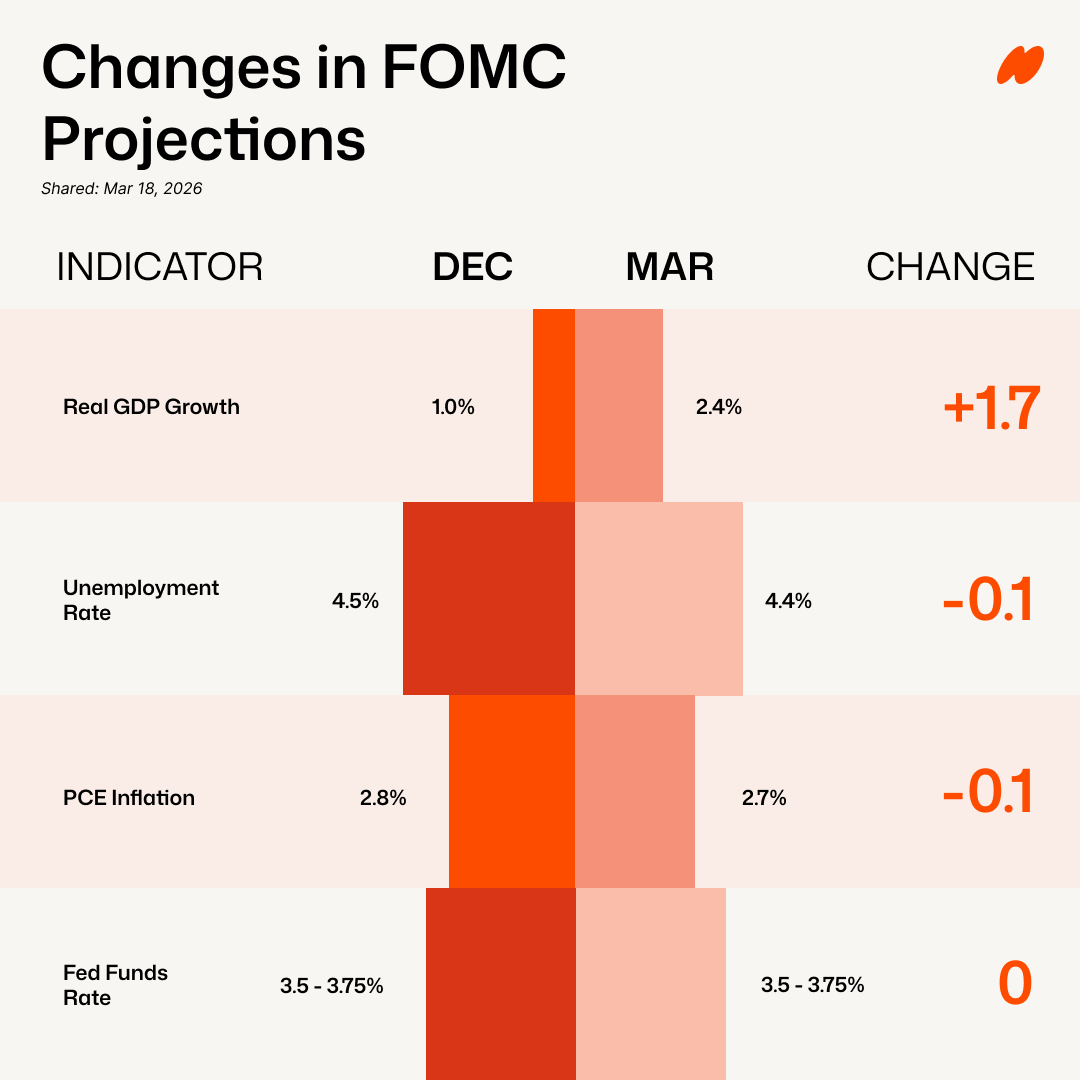

Mar 18

📰 Your FOMC Highlights:

The Fed held rates at 3.5–3.75% today. No surprise there.

What changed:

→ March projections revised GDP growth up to 2.4%, kept unemployment steady at 4.4%, and nudged inflation slightly higher to 2.7%.

→ Markets are pricing in at most one cut in 2026. Timing is unclear.

→ The Middle East conflict is the new wildcard. Oil is above $97, and the Fed is watching whether it's a short shock or a structural inflation driver.

8

4

43

4,174