Joined December 2024

- Tweets 34

- Following 1

- Followers 222

- Likes 81

9 Photos and videos

Shaper retweeted

Jun 3

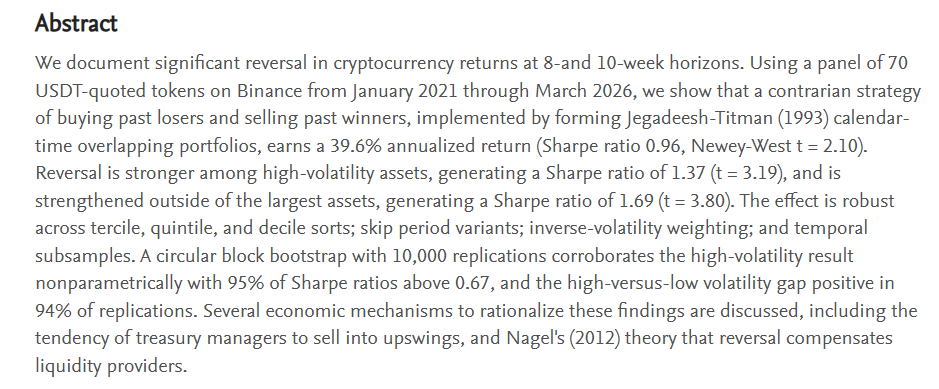

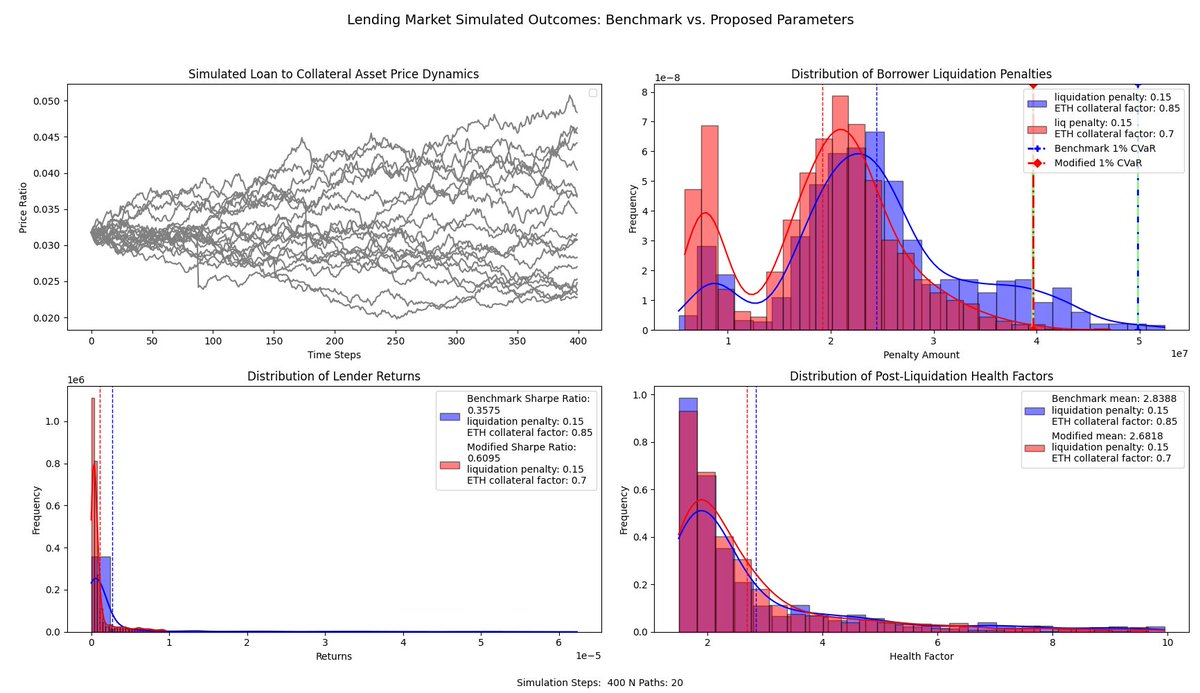

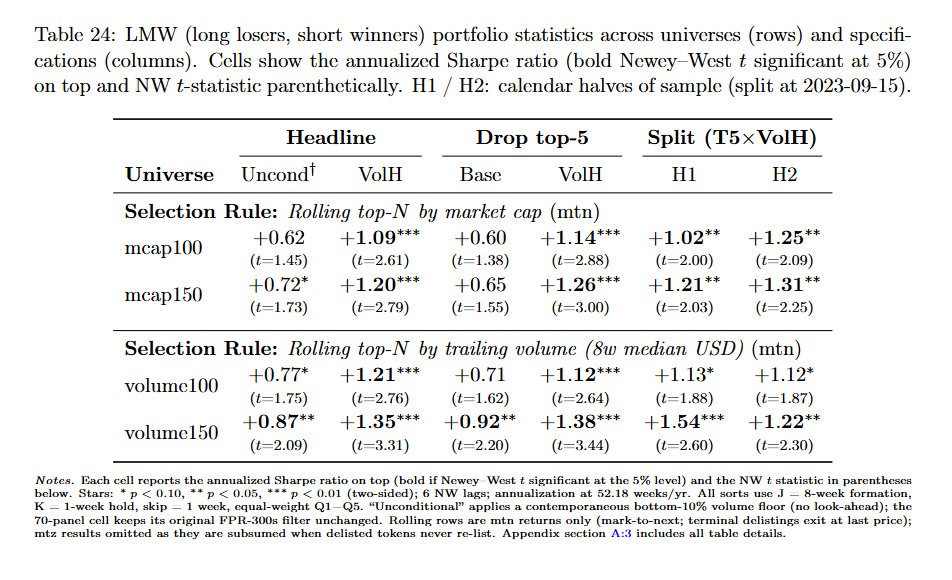

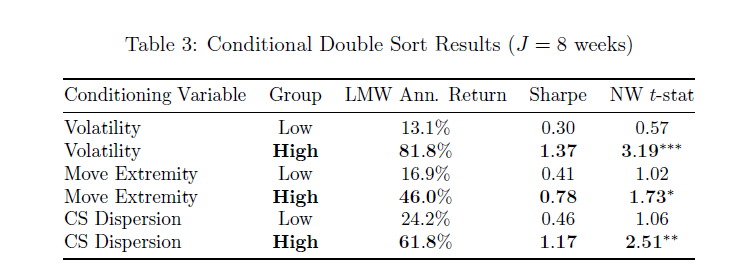

Cross-sectional reversal in cryptocurrency returns is substantial. We extended our 70-name panel to a universe of 500 symbols and applied real-time selection criteria. Long-short (LMW) portfolios sorted on past returns and volatility generate high mean returns and high Sharpe ratios. Past winners sell off on average, and past losers rebound episodically. The effect is concentrated in projects with discretionary treasury management - a point we are continuing to investigate.

1

2

4

598

Shaper retweeted

May 4

Reversal is systematic in crypto returns. Portfolios that long losers and short winners (LMW), based on 8-12 week horizons, generate high Sharpe ratios and are almost orthogonal to the market. The effect is concentrated in relatively volatile, midsize assets.

Joint with @MichaelCNowotny

2

3

10

949

18 Dec 2025

Full article including additional tables and data appendix available here: shapeshifterbuilders.notion.…

1

1,085

Shaper retweeted

5 Dec 2025

Kinetic is expanding to @StellarOrg's Soroban!

By bringing our lending and borrowing platform to a network built for global financial innovation, we’re adding new ways for individuals, institutions, and developers to utilize and grow their assets.

kinetic.market

19

59

198

13,173

25 Nov 2025

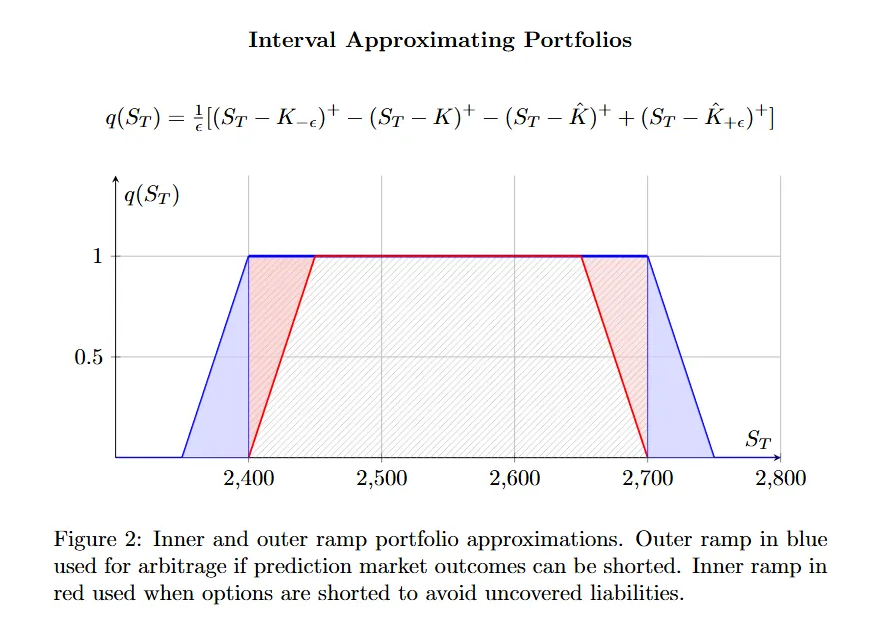

Prediction markets and options are similar in interesting ways.

Price prediction market payouts can be approximated by portfolios of options. In the attached plot, the payoff of a prediction market contract on ETH landing between 2400 and 2700 is approximated by combinations of call spreads.

In practice, whether the payoff is approximated from above or below depends on whether the option portfolio or the prediction market contract is short when constructing an arbitrage.

Full article here: x.com/hexshapeshifter/status…

20 Jun 2025

1

3

1,888

10 Oct 2025

PSA for @FlareNetworks community to revoke approvals:

We recommend revoking any approvals made to the following contract addresses, possibly associated with the now defunct lending protocol Teralend on Flare:

0x0AbcA7776D419dBC1E5548DF25748B7463f6428e

0x5213a4843626107342e26E630CC80F979805087a

If you need to revoke approvals to these addresses, revoke.cash is one easy way.

Background:

While working with @HypernativeLabs to optimize risk monitoring for @Kinetic_Markets, Hypernative's alert system flagged an unusual transaction involving the sFLR token. We dug deeper and found a pattern of exploits involving sFLR and USDT0 approvals to the above addresses.

Linked is a more detailed report including the attack pattern, attempts, and revoking approvals:

shapeshifterbuilders.notion.…

1

6

17

7,268

Shaper retweeted

11 Aug 2025

State of @coredao_org Q2

Key Update: Core's Theseus Hardfork activates fee sharing and smart contract hooks, boosting developer incentives and DApp flexibility.

QoQ Metrics 📊

• CORE and BTC Staked (USD) ⬆️ 30%

• BTC stakers also staking CORE ⬆️ 60%

• Average daily DEX volume ⬆️ 132%

Read the full report 👇

11 Aug 2025

1/ @Coredao_Org dual staking continues to grow, with $706M staked in BTC CORE at the end of Q2, up 30% QoQ.

Over half of BTC stakers now also stake CORE, with most of that in the top-yield Satoshi tier.

messari.co/4m5l3ix

16

45

116

27,775

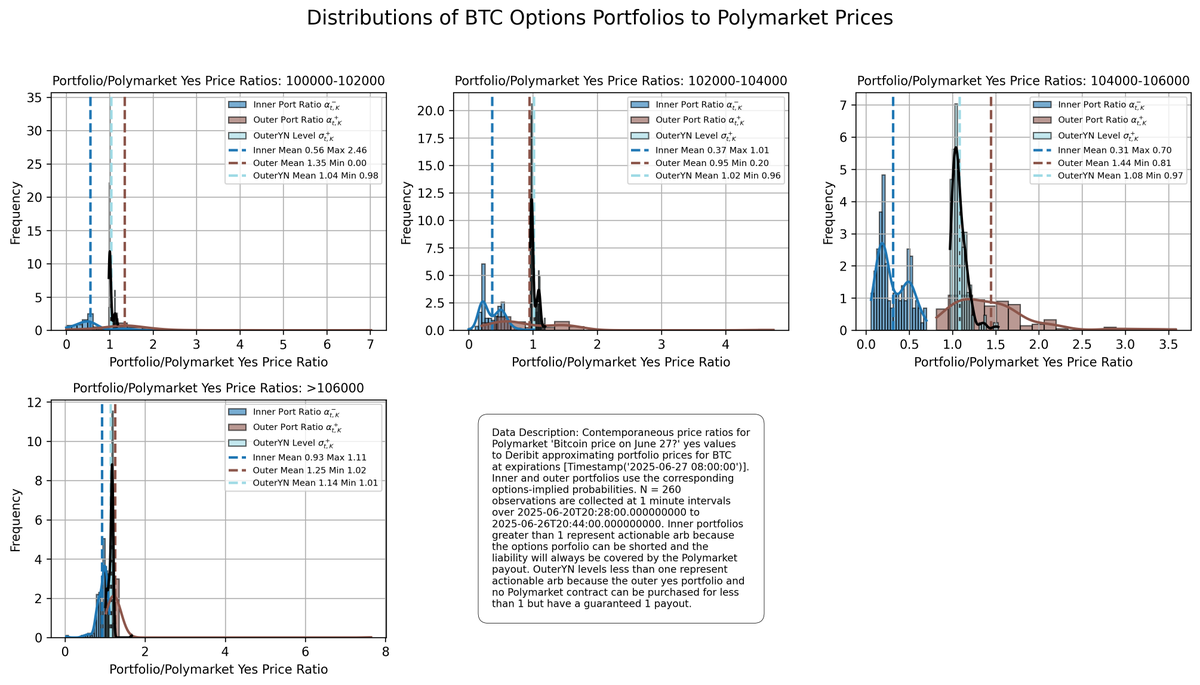

17 Jul 2025

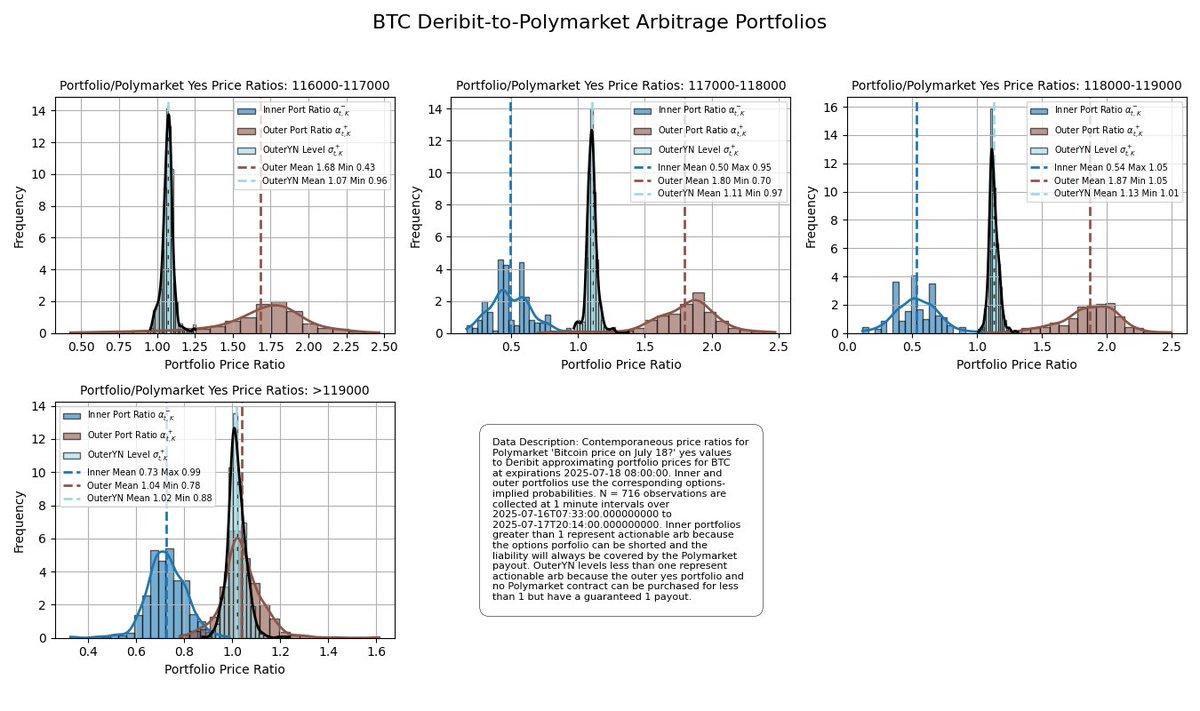

A few flashes of arb this week between @DeribitOfficial and @Polymarket but overall these venues are consistently priced.

See the article for a breakdown of the portfolios.

1

2

875

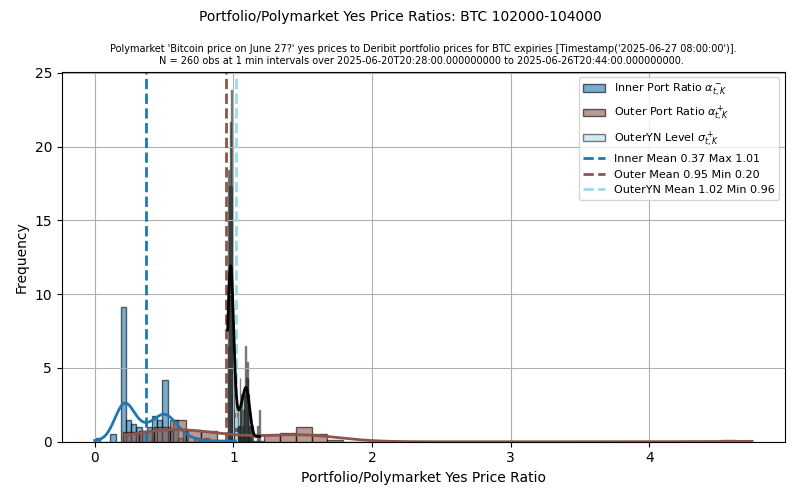

17 Jul 2025

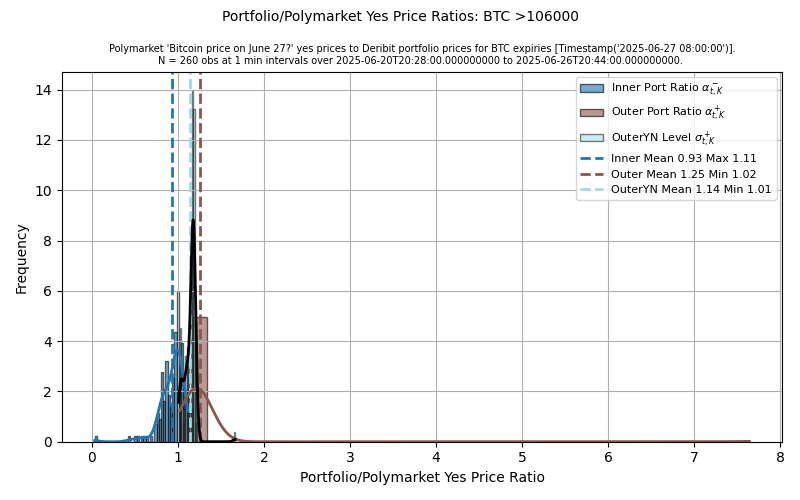

How to read the plots:

Inner portfolios (blue) greater than 1 flag arb because the options portfolio can be shorted and the liability will always be covered by the Polymarket payout.

OuterYN (turquoise) less than 1 flag arb because the outer yes portfolio and no Polymarket contract can be purchased for less than 1 but have a guaranteed 1 payout.

2

529

17 Jul 2025

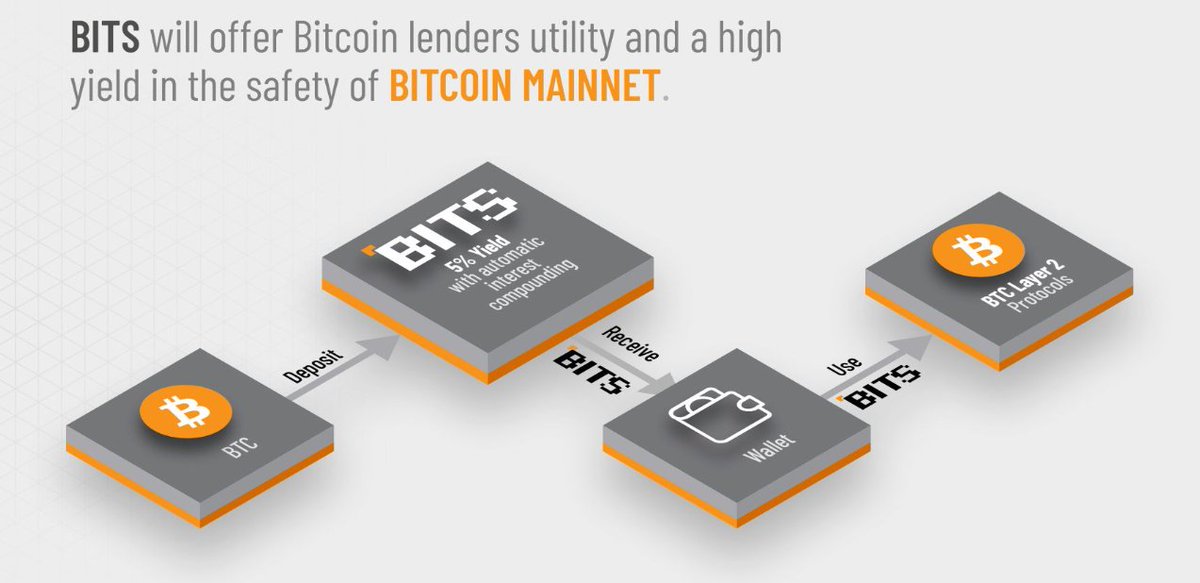

We're excited to be pushing the frontiers of on-chain Bitcoin yield with the visionaries at @bits_financial!

1

2

389

26 Jun 2025

Based on approximating portfolio prices, we see occasional but nontrivial arbitrage opportunities between @Polymarket and @DeribitOfficial.

Most prediction markets and options replicating portfolio prices we checked are consistent with no-arbitrage. We're keeping an eye on them and looking at additional markets and venues.

These data are from the week of June 22. OuterYN less than one and inner portfolio greater than one are arbitrage opportunities. Full description: x.com/hexshapeshifter/status…

20 Jun 2025

2

5

1,304

Shaper retweeted

6 Jun 2025

why we backed/ BITS

@bits_financial brings institutional-grade yield to Bitcoin without compromising custody or compliance. It's a clear path to unlocking BTC utility.

corechain.ventures/post/core…

3

16

58

3,901