Joined April 2009

- Tweets 11,658

- Following 14

- Followers 14,361

- Likes 2,411

26 Photos and videos

Pinned Tweet

16 Mar 2025

Why I’m Bullish on $ALLR:

1) The Science is Solid

Allarity ($ALLR) has delivered compelling clinical results. Their precision oncology approach, utilizing the PARP inhibitor Stenoparib, which targets the WNT pathway, is showing remarkable promise. A Phase 2 trial was concluded early after demonstrating clear clinical benefit, with one patient achieving a full response and several others experiencing significantly prolonged survival—an extraordinary outcome considering Stenoparib is administered as a last-line treatment when all other therapies have failed.

2) Addressing Market Concerns: Dilution & Reverse Splits

Investor concerns over dilution and reverse splits have been prevalent due to past filings. However, these fears should now be largely alleviated. CEO Thomas Jensen has committed to increasing shareholder value without engaging in toxic financing. Furthermore, the company has officially canceled their S-1 filing, reducing dilution risk. The only remaining ATM (At-the-Market offering) is according to my calculations approximately $10M, but it’s unlikely to be utilized given their recent $5 million share buyback announcement—a clear signal of confidence in the company’s future(I don't think SEC looks favorably at share buyback simultaneous with companies tapping ATM). Furthermore there is only one class of shares and no longer any debt conversions or warrants as far as I can see.

2b) another outstanding concern till now was Legal/SEC related to missteps by previous management. They are long gone but there were remaining lawsuits and SEC charges. However, over the past 2 weeks, Allarity announced that the class action was dismissed and they settled with the SEC to quote: "Allarity has now resolved all regulatory and legal challenges related to these issues and all other previously outstanding legal matters."

3) The March 6th Game-Changer: Government-Backed Trial

Perhaps the most overlooked yet groundbreaking development was $ALLR’s March 6th announcement that a Phase 2 trial for Stenoparib in lung cancer (SCLC) will be fully funded by the U.S. Department of Veterans Affairs (VA). This is highly significant for two reasons:

It underscores the government's confidence in the drug's efficacy.

It marks the first expansion of Stenoparib into lung cancer, a previously untapped indication.

Presumably, this level of government backing would not have materialized unless Stenoparib was demonstrating exceptional results in late-stage ovarian cancer trials.

4) The Market Hasn’t Caught Up Yet

Despite these pivotal developments, the market continues to price $ALLR as if dilution remains a major overhang—which is simply outdated thinking. With that concern effectively neutralized, the potential upside is enormous. If the market wakes up to the company’s strong science, promising clinical data, and improved financial structure, we could see a dramatic re-rating of the stock.

5) Conclusion: A Misunderstood Turnaround Play

$ALLR represents a highly asymmetric risk/reward opportunity. The market has mispriced the stock based on past concerns that are no longer relevant. If upcoming conference abstracts confirm the strength of Stenoparib’s data, the valuation could shift rapidly. Given its current market cap and historical price levels, the potential for a significant revaluation is very real.

Shorts who have been leaning on this company for years, may not be feeling so comfortable in the weeks ahead and months ahead.

7

18

78

15,166

Weedhoppa retweeted

Jun 8

President Trump and Commie Mamdani plan on attending tomorrow night's Knicks game at MSG. While both profess to be lifelong Knick fans, in reality Trump is the one who knows what a jump ball is while Mamdani is very familiar with those that jump bail.

2

2

489

May 8

$NUS just another dreadful eps report..

May 7

$NUS Q1 2026 earnings: Core Network Collapses as Management Sells the Future

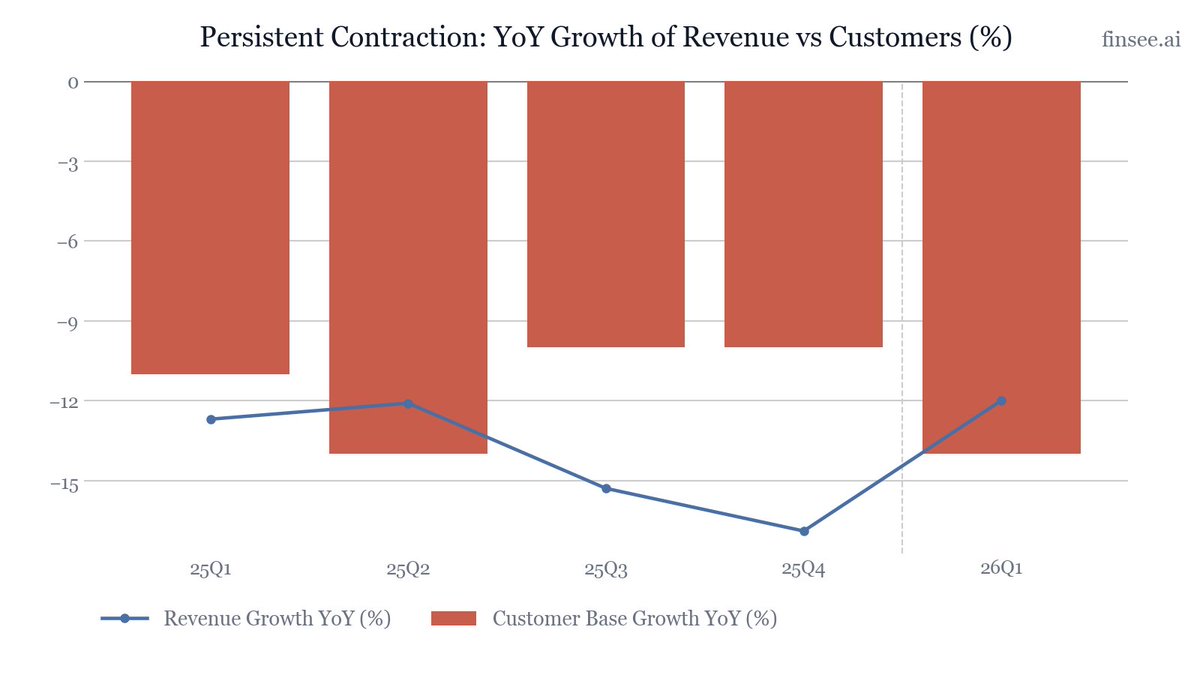

Nu Skin's first quarter delivered a brutal reality check against management's optimistic transition narrative. Revenue fell 12% YoY to $320.6M, marking the fifth consecutive quarter of double-digit contraction. More alarmingly, the underlying sales engine is eroding fast: total customers dropped 14% to a multi-year low of 669K, and the sales leader count fell 13%. While management continues to hype the upcoming H2 consumer rollout of the Prysm iO intelligent wellness platform and a late-2026 India expansion, the core business lacks stability. With adjusted operating margins compressing to 3.6% and guidance pointing to continued top- and bottom-line erosion, the company is racing against the clock to pivot before its distribution network hollows out entirely.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐏𝐫𝐲𝐬𝐦 𝐢𝐎 𝐓𝐫𝐨𝐮𝐠𝐡 𝐀𝐩𝐩𝐫𝐨𝐚𝐜𝐡𝐢𝐧𝐠 — The company is actively flushing out low-margin, legacy beauty revenue in favor of high-LTV wellness subscriptions. The planned H2 2026 full consumer rollout of the Prysm iO AI platform could reignite distributor excitement.

• 𝐂𝐥𝐞𝐚𝐧 𝐁𝐚𝐥𝐚𝐧𝐜𝐞 𝐒𝐡𝐞𝐞𝐭 𝐏𝐫𝐨𝐯𝐢𝐝𝐞𝐬 𝐑𝐮𝐧𝐰𝐚𝐲 — Despite operational weakness, the company has successfully deleveraged over the past year (reducing debt significantly since early 2025) and maintained a net cash positive position, ensuring they can fund the India and Prysm iO initiatives without distress.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐒𝐚𝐥𝐞𝐬 𝐍𝐞𝐭𝐰𝐨𝐫𝐤 𝐄𝐯𝐚𝐩𝐨𝐫𝐚𝐭𝐢𝐧𝐠 — A direct-selling model cannot function without sellers. The continued 13% YoY loss in Sales Leaders and 8% loss in Paid Affiliates limits the funnel for any new product launches, making a back-half recovery highly questionable.

• 𝐑𝐡𝐲𝐳 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐢𝐧𝐠 𝐒𝐭𝐨𝐫𝐲 𝐁𝐫𝐞𝐚𝐤𝐬 — The Rhyz segment, previously touted as a key growth driver and diversification engine ( 17% YoY in 25Q2), suddenly saw manufacturing revenues plunge 18.7% YoY in Q1, stripping the company of its only growing pillar.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴🔴

Highly Bearish. When management cites 'early signs of improving paid affiliates' while the printed data shows a 14% sequential drop in total customers and a YoY contraction in every major region, credibility is strained. The core business is shrinking faster than the new initiatives can scale.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴🔴 𝐍𝐚𝐫𝐫𝐚𝐭𝐢𝐯𝐞 𝐯𝐬. 𝐑𝐞𝐚𝐥𝐢𝐭𝐲 𝐨𝐧 𝐒𝐚𝐥𝐞𝐬 𝐅𝐨𝐫𝐜𝐞 𝐇𝐞𝐚𝐥𝐭𝐡 [NEW]

Management explicitly stated they are 'encouraged by early signs of improving paid affiliates and new sales leader development.' This directly contradicts the printed financials: Paid Affiliates dropped 8% YoY (and fell from 129,311 in 25Q4 to 120,850 in 26Q1) while Sales Leaders dropped 13% YoY. A sequential loss of roughly 8,500 affiliates and 3,100 leaders in a single quarter is a massive red flag that casts doubt on the 'improving' narrative.

🔴 𝐑𝐡𝐲𝐳 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐢𝐧𝐠 𝐆𝐫𝐨𝐰𝐭𝐡 𝐑𝐞𝐯𝐞𝐫𝐬𝐞𝐬 [NEW]

For the past year, the Rhyz Manufacturing segment was management's reliable bright spot, consistently growing ( 17.3% in 25Q2, for instance) and validating the incubator strategy. In 26Q1, that trend is Reversing violently. Rhyz Manufacturing revenue fell 18.7% YoY to $44.9M. If external partner demand is drying up, Nu Skin is left entirely reliant on its contracting direct-sales channel.

🟢 𝐏𝐫𝐲𝐬𝐦 𝐢𝐎 𝐚𝐬 𝐭𝐡𝐞 𝐌𝐚𝐤𝐞-𝐨𝐫-𝐁𝐫𝐞𝐚𝐤 𝐂𝐚𝐭𝐚𝐥𝐲𝐬𝐭

The entire strategic pivot rests on Prysm iO, an AI-powered intelligent wellness platform. Management is currently equipping sales leaders with the device to build the nutritional health biomarker database ahead of a full consumer rollout in H2 2026. The thesis: use hardware to drive high-LTV wellness product subscriptions. If successful, this could transform Nu Skin from a transactional cosmetics company to a recurring-revenue wellness platform.

🔴 𝐒𝐞𝐯𝐞𝐫𝐞 𝐃𝐞𝐭𝐞𝐫𝐢𝐨𝐫𝐚𝐭𝐢𝐨𝐧 𝐢𝐧 𝐭𝐡𝐞 𝐀𝐦𝐞𝐫𝐢𝐜𝐚𝐬 𝐚𝐧𝐝 𝐒𝐨𝐮𝐭𝐡 𝐊𝐨𝐫𝐞𝐚

Geographic performance remains bleak. South Korea was the worst laggard, plunging 22.1% YoY to $25.3M (with customers down 20%). The Americas, historically a core stronghold, dropped 16.3% to $57.8M (customers down 18%). The continued erosion of the Americas footprint suggests deep systemic issues with the compensation model or brand resonance in developed, hyper-competitive social commerce markets.

⚪ 𝐈𝐧𝐝𝐢𝐚 𝐌𝐚𝐫𝐤𝐞𝐭 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 𝐃𝐞𝐥𝐚𝐲𝐞𝐝 𝐈𝐦𝐩𝐚𝐜𝐭

Management continues to highlight India (a 1.4 billion population market) as a massive structural growth opportunity. However, they clarified that the formal launch is not anticipated until late 2026. While strategically sound, this means investors cannot expect any meaningful revenue rescue from India during the current fiscal year.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧 (𝟐𝟔𝐐𝟏): 3.6%

Decelerating sharply from 6.4% in 25Q1. While adjusted gross margins held perfectly steady (67.9% vs 67.8%), operating deleverage crushed the bottom line. Selling expenses rose to 34.3% of revenue (up from 32.5%), and adjusted G&A rose to 29.9% (up from 28.9%). The company is losing scale faster than it can cut costs.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬 (𝟐𝟔𝐐𝟏): $7.9 million

Stable. The company paid $2.9M in dividends and executed $5.0M in stock repurchases. While mathematically sound given their cash balance, buying back stock when the distributor network is actively imploding raises questions about capital allocation priorities versus investing in network stabilization.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝟐𝟔𝐐𝟐 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $330 - $360 million

Stable trajectory. The midpoint of $345M implies a YoY decline of roughly 11% (vs 25Q2's $386.1M) and roughly 0% FX impact. This indicates management does not expect any meaningful sequential rebound in the core business before the H2 launches.

𝟐𝟔𝐐𝟐 𝐄𝐏𝐒: $0.15 - $0.25

Decelerating. Compared to 25Q2's adjusted EPS of $0.43, this represents a severe YoY profit contraction. It reflects the ongoing deleverage from lower sales volumes and the absence of margin support from the Rhyz Manufacturing segment.

𝐅𝐘𝟐𝟔 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $1.35 - $1.50 billion

Stable. Management maintained their full-year guide, which implies a range of -9% to 1% YoY growth. Achieving the higher end of this range mathematically requires a massive, unprecedented revenue acceleration in the second half of the year. Given current run-rates, reaching the midpoint relies heavily on Prysm iO execution.

𝐅𝐘𝟐𝟔 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐄𝐏𝐒: $0.80 - $1.20

Reiterated, but requires a steep back-half ramp. In prior quarters, management noted that 2026 EPS will be heavily pressured by an effective tax rate spike to roughly 35% (compared to 2025's tax-advantaged ~19%).

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐀𝐟𝐟𝐢𝐥𝐢𝐚𝐭𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐃𝐢𝐬𝐜𝐫𝐞𝐩𝐚𝐧𝐜𝐲

You noted 'early signs of improving paid affiliates' in your prepared remarks, yet the reported data shows Paid Affiliates are down 8% YoY and dropped sequentially by over 8,000. In which specific markets are you seeing these improvements, and why aren't they offsetting the broader collapse?

𝐑𝐡𝐲𝐳 𝐌𝐚𝐧𝐮𝐟𝐚𝐜𝐭𝐮𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐫𝐬𝐚𝐥

Rhyz Manufacturing went from a double-digit growth engine last year to an 18.7% YoY decline this quarter. Did you lose a major third-party customer, or is this a broader slowdown in the external beauty manufacturing space?

𝐇𝟐 𝐄𝐱𝐞𝐜𝐮𝐭𝐢𝐨𝐧 𝐑𝐢𝐬𝐤

Your FY26 revenue guidance relies entirely on a second-half inflection driven by Prysm iO. With total customers and sales leaders at multi-year lows, how will you effectively distribute and scale a new hardware platform through a rapidly shrinking network?

1

2

1,233

May 6

Let me say this. In terms of a baseball analogy, we haven't even thrown out the ceremonial first pitch.

Just saying..

16 Mar 2025

Why I’m Bullish on $ALLR:

1) The Science is Solid

Allarity ($ALLR) has delivered compelling clinical results. Their precision oncology approach, utilizing the PARP inhibitor Stenoparib, which targets the WNT pathway, is showing remarkable promise. A Phase 2 trial was concluded early after demonstrating clear clinical benefit, with one patient achieving a full response and several others experiencing significantly prolonged survival—an extraordinary outcome considering Stenoparib is administered as a last-line treatment when all other therapies have failed.

2) Addressing Market Concerns: Dilution & Reverse Splits

Investor concerns over dilution and reverse splits have been prevalent due to past filings. However, these fears should now be largely alleviated. CEO Thomas Jensen has committed to increasing shareholder value without engaging in toxic financing. Furthermore, the company has officially canceled their S-1 filing, reducing dilution risk. The only remaining ATM (At-the-Market offering) is according to my calculations approximately $10M, but it’s unlikely to be utilized given their recent $5 million share buyback announcement—a clear signal of confidence in the company’s future(I don't think SEC looks favorably at share buyback simultaneous with companies tapping ATM). Furthermore there is only one class of shares and no longer any debt conversions or warrants as far as I can see.

2b) another outstanding concern till now was Legal/SEC related to missteps by previous management. They are long gone but there were remaining lawsuits and SEC charges. However, over the past 2 weeks, Allarity announced that the class action was dismissed and they settled with the SEC to quote: "Allarity has now resolved all regulatory and legal challenges related to these issues and all other previously outstanding legal matters."

3) The March 6th Game-Changer: Government-Backed Trial

Perhaps the most overlooked yet groundbreaking development was $ALLR’s March 6th announcement that a Phase 2 trial for Stenoparib in lung cancer (SCLC) will be fully funded by the U.S. Department of Veterans Affairs (VA). This is highly significant for two reasons:

It underscores the government's confidence in the drug's efficacy.

It marks the first expansion of Stenoparib into lung cancer, a previously untapped indication.

Presumably, this level of government backing would not have materialized unless Stenoparib was demonstrating exceptional results in late-stage ovarian cancer trials.

4) The Market Hasn’t Caught Up Yet

Despite these pivotal developments, the market continues to price $ALLR as if dilution remains a major overhang—which is simply outdated thinking. With that concern effectively neutralized, the potential upside is enormous. If the market wakes up to the company’s strong science, promising clinical data, and improved financial structure, we could see a dramatic re-rating of the stock.

5) Conclusion: A Misunderstood Turnaround Play

$ALLR represents a highly asymmetric risk/reward opportunity. The market has mispriced the stock based on past concerns that are no longer relevant. If upcoming conference abstracts confirm the strength of Stenoparib’s data, the valuation could shift rapidly. Given its current market cap and historical price levels, the potential for a significant revaluation is very real.

Shorts who have been leaning on this company for years, may not be feeling so comfortable in the weeks ahead and months ahead.

1

13

2,632

Weedhoppa retweeted

May 5

$HCKT Q1 2026 earnings: Gen AI Pivot Derails Legacy Business; Massive Guidance Miss

The Hackett Group is suffering a severe transition shock. Management's aggressive pivot to Generative AI platforms has stalled its legacy consulting business far faster than new software models can replace it. Q1 revenue before reimbursements fell 11% YoY to $67.8M, disastrously missing management's own $70.5M-$72.0M guidance. While GAAP Net Income rose, this was heavily distorted by a non-cash stock compensation reversal and aggressive headcount cuts. Adjusted EPS plunged 17% to $0.34. The Oracle and Global S&BT segments are in freefall, and a sudden reversal in operating cash flow to negative $5.1M contradicts the narrative of an 'Agentic enterprise era' boom.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐒𝐀𝐏 𝐒𝐨𝐥𝐮𝐭𝐢𝐨𝐧𝐬 𝐁𝐨𝐨𝐦 — SAP Solutions is the lone bright spot, accelerating 21% YoY in Q1 to $16.0M. S/4HANA cloud migrations continue to provide a reliable implementation pipeline.

• 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐥 𝐌𝐚𝐫𝐠𝐢𝐧 𝐏𝐫𝐨𝐭𝐞𝐜𝐭𝐢𝐨𝐧 — Management is aggressively cutting costs to protect margins. A $1.96M restructuring charge signals swift action to align headcount with reduced traditional consulting demand, leveraging internal AI tools to boost productivity.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐂𝐫𝐞𝐝𝐢𝐛𝐢𝐥𝐢𝐭𝐲 𝐃𝐞𝐬𝐭𝐫𝐨𝐲𝐞𝐝 — Management missed their Q1 revenue guidance midpoint by nearly $3.5M. The aggressive hyping of new channel partnerships in Q4 failed to materialize into Q1 financial results.

• 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰 𝐑𝐞𝐯𝐞𝐫𝐬𝐚𝐥 — Operating cash flow suddenly flipped from a positive $19.1M in Q4 (and $4.2M last year) to a negative $5.1M cash burn, highlighting severe working capital deterioration.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🔴

Bearish. The strategic pivot to Gen AI may be visionary, but execution is deeply flawed. Cannibalizing the core consulting business before software revenues scale is resulting in shrinking top-line revenue, declining adjusted earnings, and cash burn.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🔴🔴 𝐒𝐞𝐯𝐞𝐫𝐞 𝐓𝐨𝐩-𝐋𝐢𝐧𝐞 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐌𝐢𝐬𝐬 [NEW]

The most alarming takeaway is the sheer magnitude of the Q1 revenue miss. Management guided for $70.5M-$72.0M, but delivered only $67.8M. This indicates a profound disconnect between management's pipeline visibility and actual client behavior. The Gen AI 'halo effect' touted in previous quarters has morphed into a freeze on legacy spending.

🔴 𝐒𝐞𝐠𝐦𝐞𝐧𝐭 𝐃𝐢𝐯𝐞𝐫𝐠𝐞𝐧𝐜𝐞: 𝐎𝐫𝐚𝐜𝐥𝐞 𝐚𝐧𝐝 𝐒&𝐁𝐓 𝐢𝐧 𝐅𝐫𝐞𝐞𝐟𝐚𝐥𝐥

The core business segments are deteriorating rapidly. Global S&BT (which accounts for over half of total revenue) decelerated further, dropping 14.7% YoY. Oracle Solutions cratered by 24.3% YoY. Clients appear to be engaging in 'thoughtful decision making' (macroeconomic hesitation) or are simply pausing large Oracle upgrades to evaluate AI alternatives.

🔴 𝐖𝐨𝐫𝐤𝐢𝐧𝐠 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐭𝐞𝐫𝐢𝐨𝐫𝐚𝐭𝐢𝐨𝐧 𝐂𝐨𝐧𝐭𝐫𝐚𝐝𝐢𝐜𝐭𝐬 𝐆𝐀𝐀𝐏 𝐈𝐧𝐜𝐨𝐦𝐞 [NEW]

A massive red flag is present in the cash flow statement. Despite reporting GAAP Net Income of $4.3M, Operating Cash Flow was heavily negative, burning $5.1M. This is a severe reversal from the $19.1M generated in Q4 and $4.2M in the prior year. This implies significant collections issues, extended payment terms, or milestone delays on legacy projects.

🟢 𝐆𝐞𝐧 𝐀𝐈 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 (𝐀𝐈 𝐗𝐏𝐋𝐑 & 𝐙𝐁𝐫𝐚𝐢𝐧)

Management continues to position its proprietary AI XPLR and ZBrain platforms as the cornerstone of its turnaround. The strategy relies on shifting clients toward an 'Agentic enterprise era.' If the company can successfully transition to a SaaS-like licensing model with its recently discussed channel partners, this remains a potent long-term growth driver.

🟢 𝐈𝐧𝐭𝐞𝐫𝐧𝐚𝐥 𝐑𝐞𝐬𝐭𝐫𝐮𝐜𝐭𝐮𝐫𝐢𝐧𝐠 𝐚𝐧𝐝 𝐀𝐮𝐭𝐨𝐦𝐚𝐭𝐢𝐨𝐧 [NEW]

Hackett recorded $1.96M in restructuring costs in Q1, cutting headcount to right-size against falling demand. By utilizing their own Gen AI delivery platforms (like XT and AIXelerator), they are forcing internal productivity gains. This aggressive cost management shielded GAAP operating margins, which improved to 13% despite the revenue collapse.

🟢 𝐒𝐀𝐏 𝐌𝐢𝐠𝐫𝐚𝐭𝐢𝐨𝐧𝐬 𝐏𝐫𝐨𝐯𝐢𝐝𝐢𝐧𝐠 𝐚 𝐅𝐥𝐨𝐨𝐫

While Oracle implementation stalls, SAP S/4HANA cloud migrations continue to thrive. The SAP segment has posted two consecutive quarters of 20% growth, effectively acting as the sole load-bearing pillar for the company's top line.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐆𝐀𝐀𝐏 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐈𝐧𝐜𝐨𝐦𝐞: $8.94 million

Accelerating significantly from $4.40M a year ago. However, investors must look under the hood: this was entirely driven by a massive $5.5M YoY swing in non-cash stock-based compensation (moving from a $4.9M expense last year to a $0.6M reversal this year). The underlying core profitability, as measured by Adjusted EPS, actually declined.

𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰: -$5.07 million

Reversing violently from positive cash generation. The company utilized $5.1M in operations compared to generating $4.2M in Q1 of last year. This is the first quarter of operating cash burn in the past year, requiring the company to draw down its cash balance to $6.1M while keeping $79.0M outstanding on its credit facility.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝟐𝟔𝐐𝟐 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐁𝐞𝐟𝐨𝐫𝐞 𝐑𝐞𝐢𝐦𝐛𝐮𝐫𝐬𝐞𝐦𝐞𝐧𝐭𝐬: $68.5M - $70.0M

Decelerating. The midpoint of $69.25M implies an 11% YoY decline compared to $77.6M in 25Q2. More concerning, this range is even lower than the already-missed Q1 guidance, signaling that the company expects no immediate relief from the current demand freeze.

𝟐𝟔𝐐𝟐 𝐀𝐝𝐣𝐮𝐬𝐭𝐞𝐝 𝐃𝐢𝐥𝐮𝐭𝐞𝐝 𝐄𝐏𝐒: $0.33 - $0.35

Decelerating. The midpoint of $0.34 matches the current quarter's weak result, representing a ~10.5% drop from the $0.38 achieved in 25Q2. Management assumes a 26.6% effective tax rate.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐄𝐱𝐩𝐥𝐚𝐢𝐧𝐢𝐧𝐠 𝐭𝐡𝐞 𝐌𝐚𝐬𝐬𝐢𝐯𝐞 𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞 𝐌𝐢𝐬𝐬

You guided for $70.5M-$72.0M just a few months ago but delivered $67.8M. What specifically broke down in your pipeline visibility, and why should investors trust the new Q2 guidance range?

𝐖𝐨𝐫𝐤𝐢𝐧𝐠 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐫𝐚𝐢𝐧

Operating cash flow flipped to a negative $5.1 million despite positive Net Income. Are clients delaying payments, or are you experiencing milestone delivery issues on legacy engagements?

𝐀𝐈 𝐂𝐚𝐧𝐧𝐢𝐛𝐚𝐥𝐢𝐳𝐚𝐭𝐢𝐨𝐧 𝐯𝐬 𝐌𝐨𝐧𝐞𝐭𝐢𝐳𝐚𝐭𝐢𝐨𝐧

Global S&BT and Oracle revenues are dropping by double-digits. Are clients actively pausing these legacy engagements because they are waiting to deploy your AI XPLR solutions, or are these lost deals entirely?

𝐒𝐭𝐚𝐭𝐮𝐬 𝐨𝐟 𝐭𝐡𝐞 '𝐆𝐚𝐦𝐞 𝐂𝐡𝐚𝐧𝐠𝐢𝐧𝐠' 𝐏𝐚𝐫𝐭𝐧𝐞𝐫𝐬𝐡𝐢𝐩𝐬

In Q4, you mentioned an imminent 'game changing' agreement with a global tech and consulting company, alongside a ServiceNow pilot. When will these partnerships materially inflect the revenue trajectory to offset the legacy declines?

1

1

681

Mar 8

Although $ALLR is by far my biggest swing, I largely refrained from tweeting about it over the last year, but Friday's financing is a total game changer.

You see, there were two major concerns about the company.

1)The Science

2) Adequate financing through the trials.

I doubt many had concerns about the science, based on the interim findings, the total remission and the extended longevity of many on the drug.

The bigger concern imo, was the possibility of dilution, especially given the company's track record.

Fridays fantastic non dilutive $20 million infusion should put this fear to rest .

Now it's just a waiting game for more interim data to be released and then what the proper valuation this company deserves relative to its peers.

While that can be a matter of debate, I think we can all agree that the current price of $1.24 isn't even astronomically close.

Once again I will reiterate, I've been trading for close to 35 years, and I don't believe I have ever seen a bigger disconnect between price and valuation than $ALLR.

Good luck Longs.

2026 look to be a life changer

3

1

40

3,687

Mar 6

$ALLR

This looks like the last piece to the financing puzzle!

What a deal!

All we have to do now is sit back and wait for the interim data rollout and the potential BTD designation by the FDA

Exciting times indeed!!

Mar 6

$ALLR wow this deal.. cash to 28 🔥🔥

"Financing Structured as Non-Convertible Debt Financing"

$10m 10m

I really like this..

Waiting for the SEC filing to come out but everything I've seen the PR looks amazing wow I don't know how Thomas got these terms wow

~$35m cash

1

21

1,503

Feb 26

$WRBY huge miss and warn..Not sure why it was bid up this morning..Traded as low as 18.80

1

1

1,023

Feb 4

$WNC nasty downside guide for next wtr..Expecting about $320m vs the prior $447 million expectation

Also sees about $1 loss for next qtr vs the .17 profit expected.

No guidance for FY 26 due to lack of visibility.

1

1

469

Jan 29

$IMG which does about 300k in reve announces contracts totalling 2.59ml

4m float bottom chart play..One to watch imo here

2

5

534