Scientist; in Tokyo.

Joined November 2025

- Tweets 146

- Following 107

- Followers 477

- Likes 1,534

14 Photos and videos

Jun 12

Many here desperately want you to believe that rare earth solvent extraction chemistry requires a ton of skill. As someone who has actually run multi-circuit solvent extraction processes I can tell you it doesn’t! Metallurgy is 1000X harder—which Japan still dominates.

1

114

Jaraxle retweeted

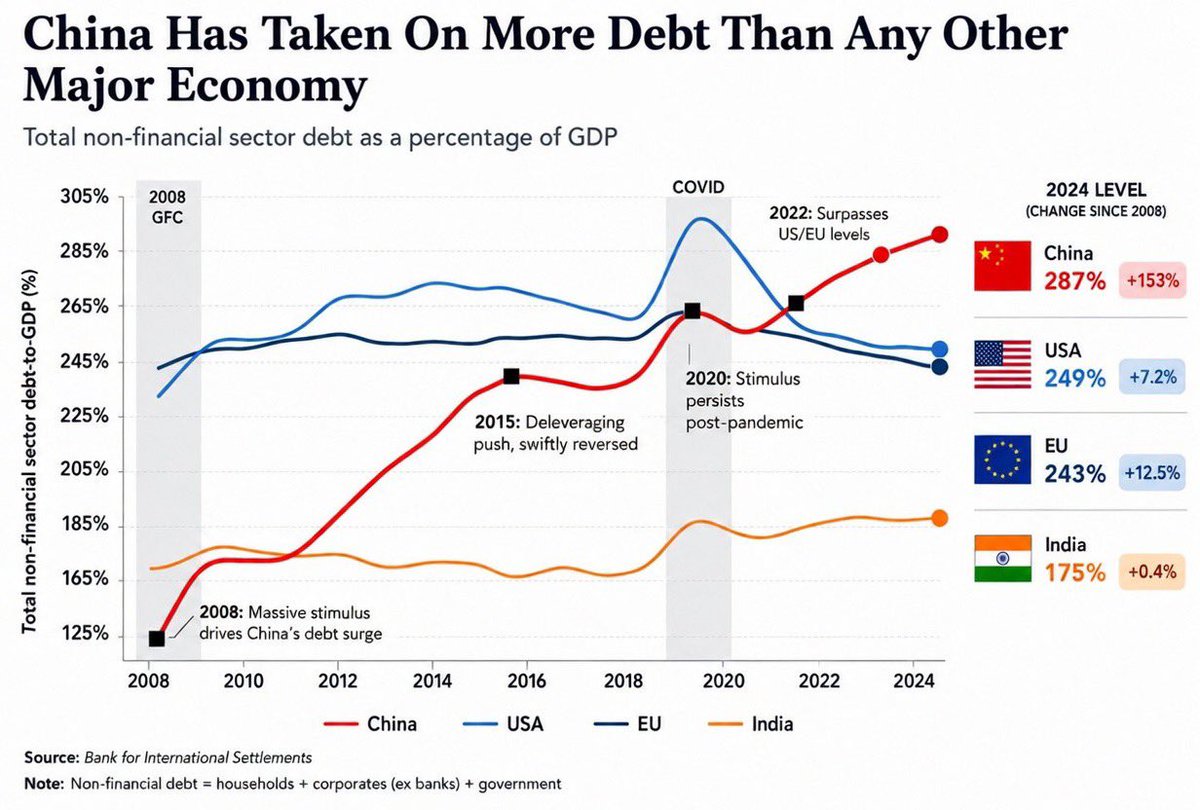

China didn’t build an economic miracle. It built the world’s biggest debt experiment. And experiments don’t last forever

When growth is fueled by borrowing, every vacant illuminated skyscraper, highway, and ghost city comes with a bill. How long can they keep the illusion alive?

180

374

1,223

275,187

Jaraxle retweeted

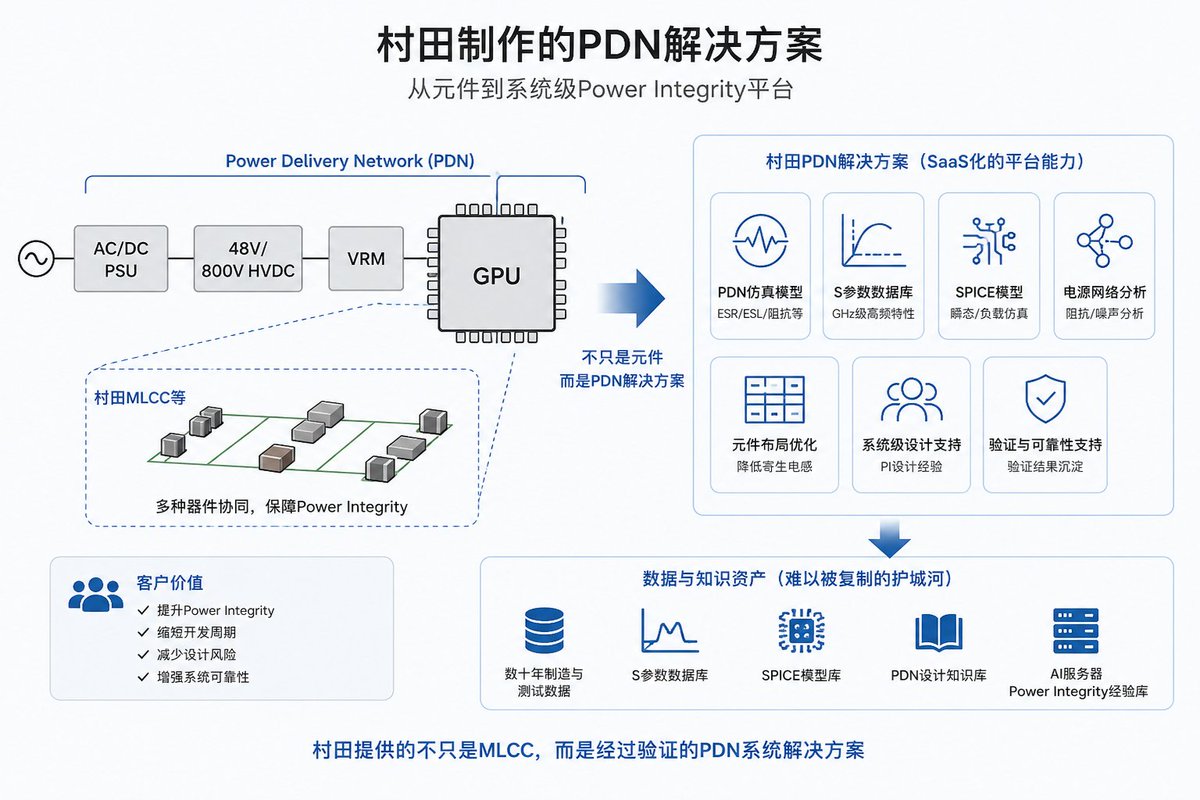

村田制作的PDN解决方案:为SaaS的未来指明方向

分析村田制作时,市场关注的是MLCC市场份额、BaTiO₃粉体、超薄介质层工艺以及100μF级高端产品。

但村田其实还在悄悄的干另一件大事:围绕MLCC建立起来的PDN(Power Delivery Network)软硬一体的解决方案。

在NVIDIA GB200、GB300等平台单颗GPU功耗已经超过1000W的情况下,AI服务器设计的核心挑战之一已经从算力本身转向Power Integrity(电源完整性),而Power Integrity的核心就是PDN设计。

传统意义上的MLCC厂商负责提供元件,客户负责设计。但今天的村田不仅提供MLCC,还提供PDN仿真模型、S参数数据库、SPICE模型、电源网络分析、元件布局优化以及系统级设计支持。客户采购的已经不再是一颗电容,而是一整套经过验证的供电解决方案。

对于每颗MLCC,村田提供的不只是容量和耐压参数,还包括ESR、ESL、阻抗曲线、自谐振频率、温度特性、DC Bias特性以及高频行为模型。工程师可以直接导入Cadence、Ansys、Keysight等EDA工具进行仿真,在PCB制造之前预测整个供电系统的行为。这意味着大量问题可以在设计阶段解决,而不是等到样机阶段。

随着AI服务器功率不断提升,供电噪声已经进入GHz频段。传统参数已经无法准确描述元件行为,S参数成为高频设计的核心工具。村田长期积累的S参数数据库,使客户能够直接获得真实器件在不同频率下的表现,而不需要重新测量和建模。对于很多客户而言,这些数据库的价值甚至超过元件本身。

更进一步,村田开始参与整个Power Integrity设计过程。例如GPU电流从200A瞬间提升到1000A时,电压会下降多少;哪些位置需要增加MLCC;哪些位置已经过度设计;如何降低阻抗峰值;如何优化瞬态响应。这些已经不是元件层面的问题,而是系统层面的问题。村田实际上正在帮助客户完成整个PDN设计。

元件布局优化同样是PDN方案的重要组成部分。很多时候增加电容数量并不能解决问题,布局反而更加重要。同样100颗MLCC,由于寄生电感,不同摆放位置产生的效果可能相差数倍。

因此真正优秀的PDN设计更多的是优化布局。而村田长期积累的大量设计经验,可以帮助客户找到最优方案。

村田进行中的从“元件数字化”到“PDN设计支持”的转型,并正在向“系统级Power Integrity平台”演进。

其最重要的资产已经不仅是制造能力,还包括数十万个器件数字模型、数十年的参数数据库、AI服务器PDN经验库以及客户项目设计知识库。这些资产共同构成了新的竞争壁垒。

这种模式带来的最大价值,是极强的客户粘性。过去客户采购的是电容,今天客户采购的是经过验证的PDN架构。如果一台AI服务器已经基于村田模型完成仿真验证、EMC认证、热设计验证以及可靠性测试,那么更换供应商将意味着重新仿真、重新打板、重新测试以及重新认证。即使替代产品规格接近,也可能因为ESR、ESL、阻抗曲线或谐振频率变化而影响整个PDN性能。因此客户最终锁定的并不是MLCC,而是整个供电设计体系。

这也是村田PDN方案最有价值的地方。很多公司销售产品,村田正在销售“设计确定性”;很多公司销售元件,村田正在销售“验证结果”;很多公司销售硬件,村田正在销售“经过验证的Power Integrity平台”。

更重要的是,村田的PDN方案或许揭示了未来SaaS真正的发展方向。过去的软件公司依靠代码和功能建立护城河,而AI正在不断降低代码的价值。但无法降低真实世界的数据的价值。

村田制作的PDN解决方案拥有制造业的物理壁垒、EDA行业的工作流壁垒以及数据平台的数据飞轮。随着AI服务器功耗持续提升,Power Integrity的重要性只会越来越高,而村田积累的PDN数据库、设计经验和验证体系也会越来越难以复制。

这或许才是村田制作在AI数据中心时代最核心、也最容易被市场低估的竞争优势:未来最难被AI取代的SaaS形态。

免责声明:本人持有文章中提及资产,观点充满偏见,非投资建议,dyor

18

48

313

81,205

May 28

They could probably make the extra 6X or more if Japanese vendors were stupid enough to telegraph their internal plans. There is little upside to transparency when China is squeezing material supply chains.

May 28

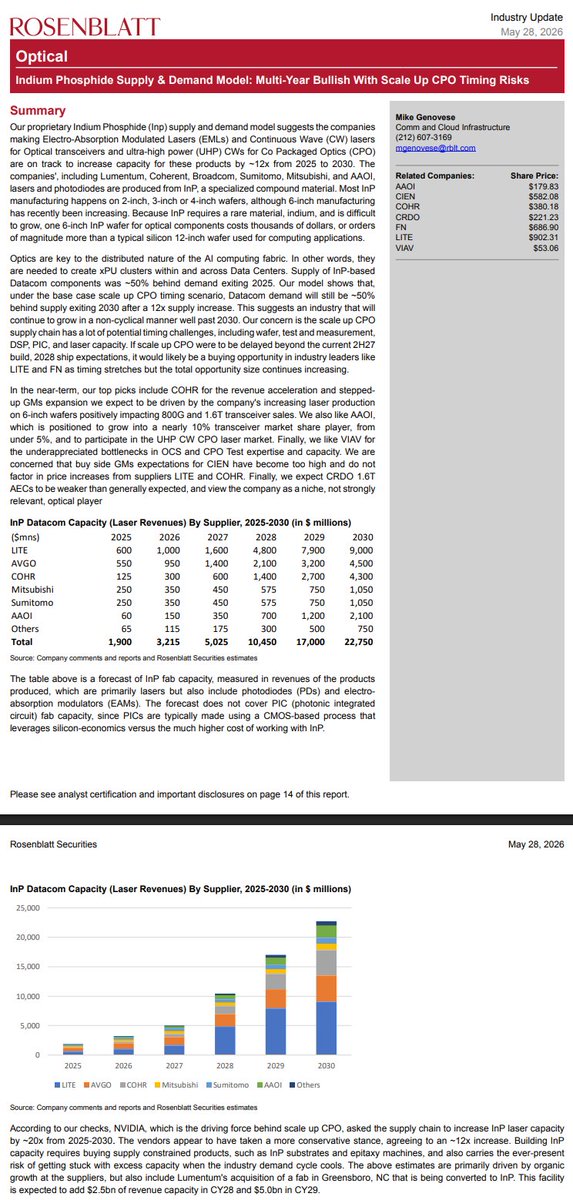

Rosenblatt InP lasers checks:

According to our checks, NVIDIA, which is the driving force behind scale up CPO, asked the supply chain to increase InP laser capacity by ~20x from 2025-2030. The vendors appear to have taken a more conservative stance, agreeing to an ~12x increase ( $AAOI / $LITE etc)

2

317

May 16

If Kioxia (285A.T) executives are going to co-opt the shareholder dividend, they had better share it with the regular employees.

1

318

Apr 27

THine Electronics volume up 2,000% today. ザインエレクトロニクス (6769.T)

Mar 12

THine Electronics (6769.T) finally seems to be catching a bid, likely tied to its work on DSP-free PCIe optical fabrics for vertically scaled AI clusters.

The pitch: cut power and latency in the short-reach links that move data inside AI servers. (1/9)

803

Mar 12

THine Electronics (6769.T) finally seems to be catching a bid, likely tied to its work on DSP-free PCIe optical fabrics for vertically scaled AI clusters.

The pitch: cut power and latency in the short-reach links that move data inside AI servers. (1/9)

1

2

9

3,344

Mar 12

The bigger question is where AI architectures ultimately go.

If clusters continue scaling vertically (more GPUs per node), efficient short-reach fabrics matter a lot.

If inference becomes more distributed and scale-out, the opportunity narrows. (8/9)

1

295

Mar 12

Either way, it’s an interesting attempt by THine to apply classic signal-integrity engineering to one of the more painful constraints in AI hardware: moving massive amounts of data without burning watts just cleaning up the signal. (9/9)

255

Mar 1

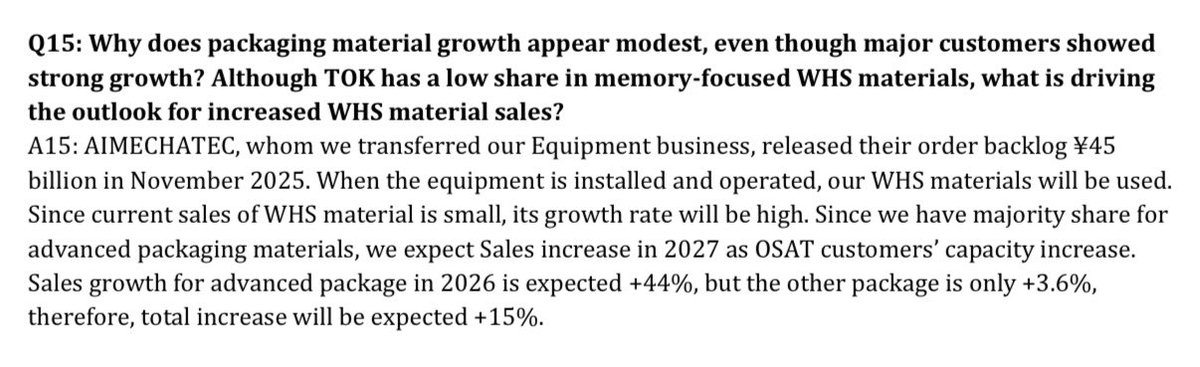

AI Mechatec (AiM; 6227.T) is up ~300% since this tweet, mainly due to expected demand for wafer handling systems via their collaboration with TOK (4186.T). It’s spelled out in their earnings and also in TOK’s recent Q&A:

17 Nov 2025

AI Mechatec (6227.T) has an order backlog of $284M, exceeding its entire market cap ($187M) by roughly 50%. 🧐🤏

1

8

1,673

Mar 1

Optorun and AiM also seem to be positioning for CPO and SiPh. Optorun’s earnings haven’t been great but recent guidance is strong. Optorun is 23%, 8% and 17% the last three Fridays. Is someone is sending a signal?

2

1

414

Mar 2

Looking at 6235.T earnings: revenue held up in FY25 ( 4.5%) but trough in margins (ALD, FX, inventory write down, equity-method swings). Net cash 3X cash flow (¥31B;¥8.5B). FY26 guide 86% OP on 13% sales from AI/datacenter optics tailwind. Possible 2025 was a reset, not a peak.

230