Joined March 2023

- Tweets 6

- Following 426

- Followers 36

- Likes 586

4 Photos and videos

May 19

Built a desktop app to visualize trading backtests.

PyQt6 matplotlib. Loads a CSV of trades, shows 50 metrics, equity curves, Monte Carlo simulations, rolling analytics.

Nothing revolutionary : just a clean tool I wanted to exist. Open source.

-> github.com/Wilfrid-art/backt…

2

42

May 18

Open-sourced options-quant-toolkit :

a Python library for options pricing, Greeks, and volatility modeling.

Black-Scholes, Monte Carlo, binomial trees, implied vol, strategy backtesting.

Built for quants, traders, and students. Free and open.

-> github.com/Wilfrid-art/optio…

1

48

Jan 28

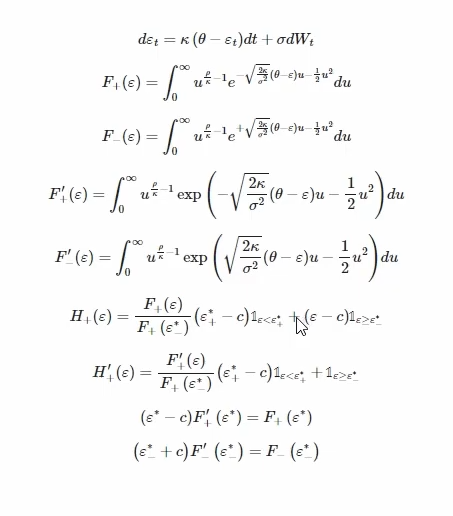

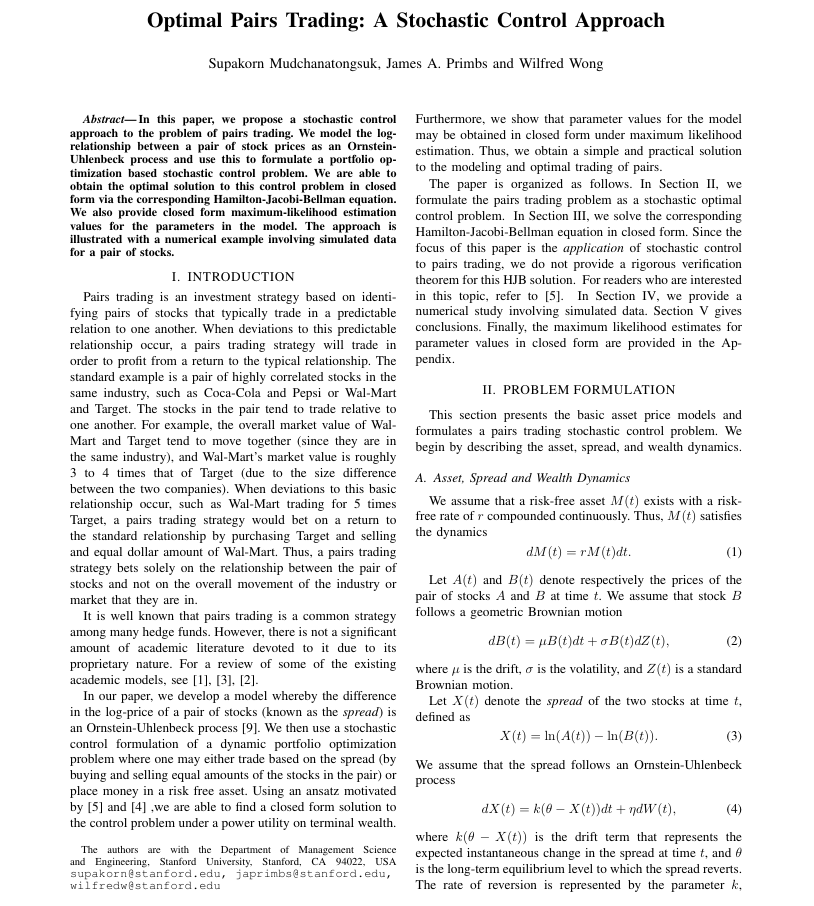

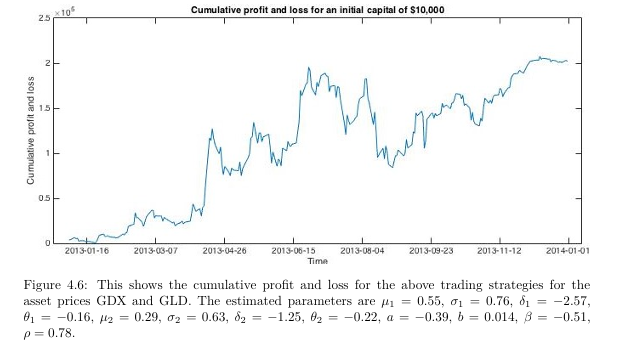

"Optimal Pairs Trading with Time-Varying Volatility" by Li & Tourin.

Classic OU model fails because volatility isn't constant. This paper layers a realistic time-varying vol structure onto the mean-reverting OU process, using stochastic control to find the optimal strategy

3

147

Jan 27

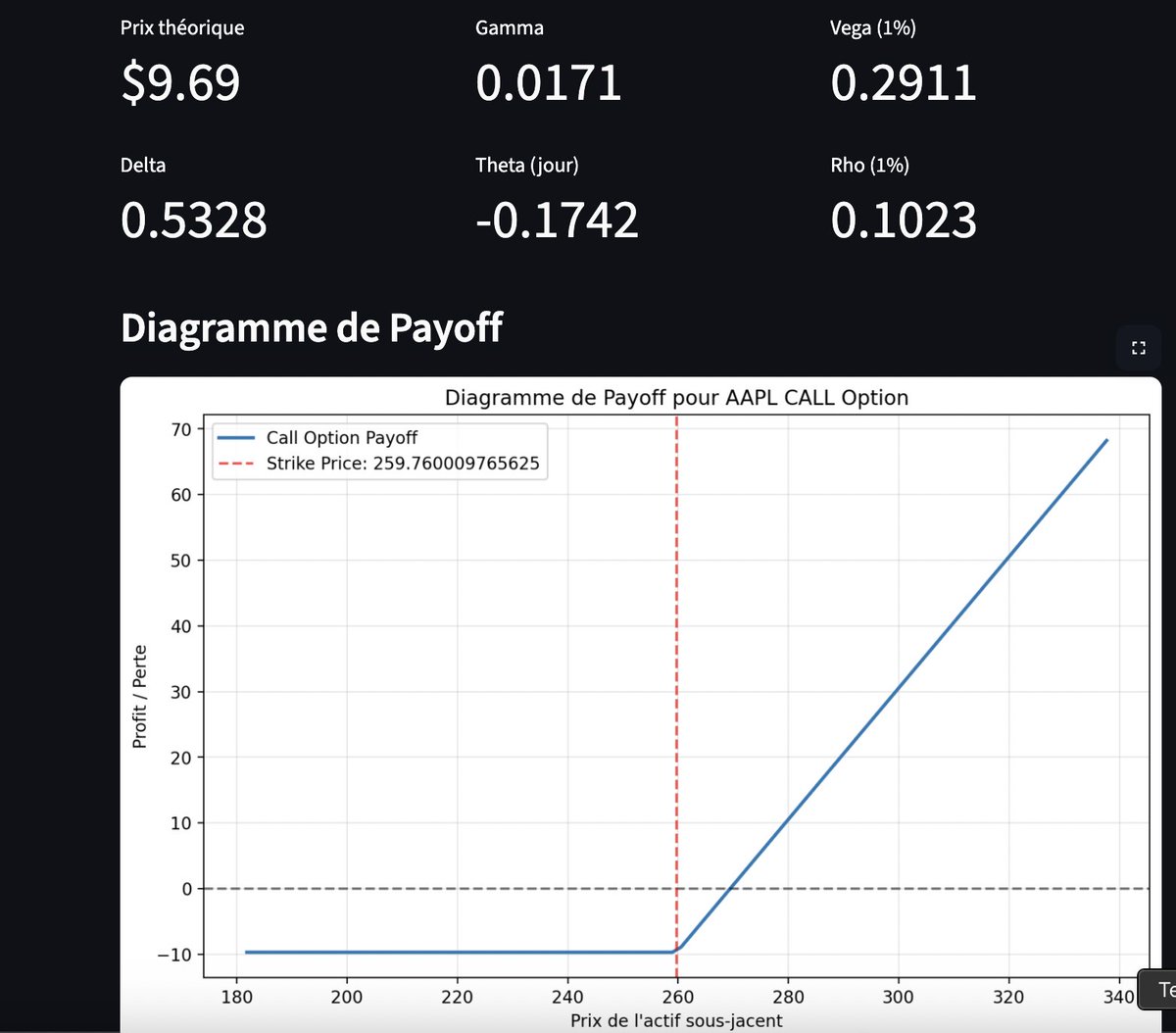

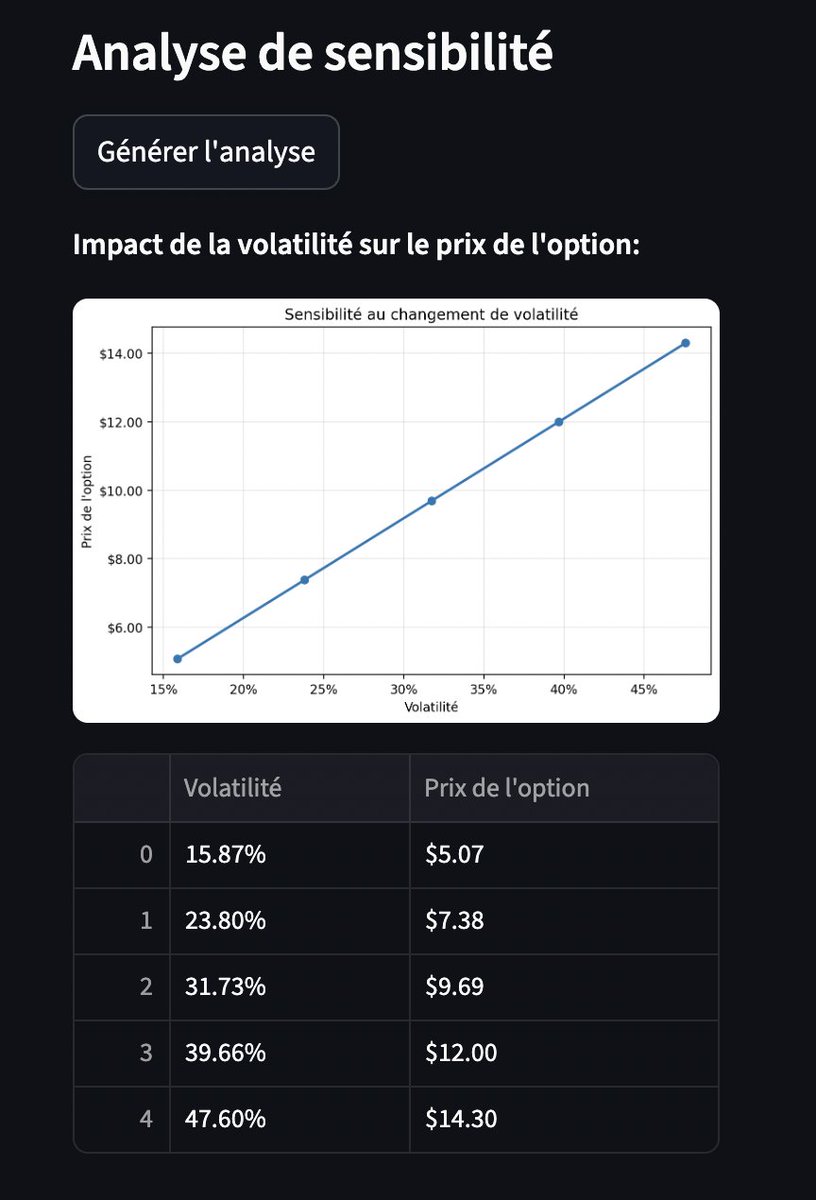

open-sourced my options pricing engine with implied vol surface (vol smile), educational notebooks & interactive dashboards.

README in English, app interface in French.

github.com/Wilfrid-art/Prici…

#QuantDev #OptionPricing #QuantFinance #Python

2

171

Jan 23

Optimal trading bands > arbitrary z-score rules.

Using stochastic control / optimal stopping to derive optimal entry & exit levels for mean-reverting spreads (Cartea–Jaimungal).

#QuantFinance #StatArb #AlgoTrading #SystematicTrading

2

119

Jan 22

Exploring statistical arbitrage across the SP500.

Pairs trading with OU-modeled spreads and Cartéa-optimized bands to capture mean-reversion efficiently.

(Based on key research papers 📄)

#QuantTrading #AlgoTrading #SP500 #PairsTrading

5

204