Here for information. No DM's.

Joined November 2023

- Tweets 39,078

- Following 7,216

- Followers 531

- Likes 5,013

116 Photos and videos

Taxation Is Theft. retweeted

Police “Twist” handcuffs to cause more Pain to 17 year old boy 😳👮♀️😡

Sheffield 🏴

The 17 year old boy who hit his head on a metal bollard after being “violently” arrested is on the ground explaining he is in a lot of Pain after hitting his head…an officer “Twists” his handcuffs to cause more pain and tells him to “relax” this is police brutality 😡

#police @TRobinsonNewEra @syptweet

281

2,818

7,578

110,898

Taxation Is Theft. retweeted

What the heck?

Grok claims that these prices are legit due to "production scarcity". Hmmmm....Jon might be onto something here.

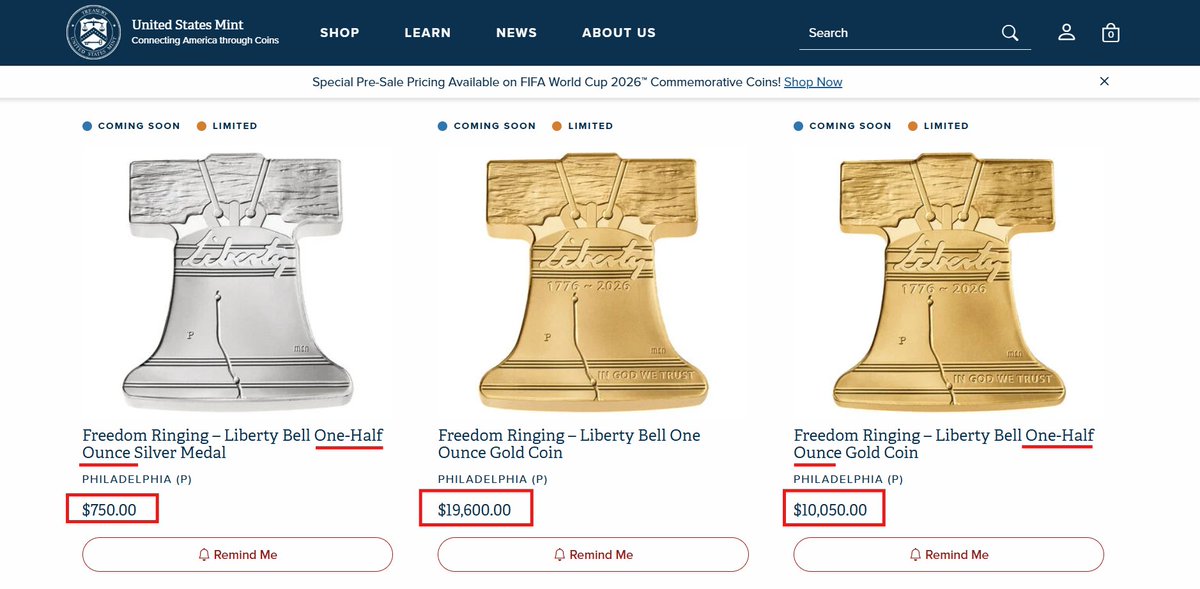

🔥$20,100 GOLD, $1,500 SILVER:

DID THE US MINT JUST REVEAL TRUMP'S JULY 4 GOLD REVALUATION⁉️

The US Mint has just posted limited edition (Mintage of 2,026) Gold & Silver Liberty Bell Medals on the US Mint's website:

🚨1 oz Gold Coin: $19,600

🚨1/2 oz Gold Coin: $10,050

🚨1/2 oz Silver Coin: $750

Yes, these are limited mintage numismatic medals, but $1,500/ oz silver & $20,100/ oz gold is FAR beyond numismatic premiums.

⚠️Did the US Mint just accidentally confirm that the Trump Administration is preparing a MASSIVE GOLD REVALUATION ON AMERICA'S 250th BIRTHDAY⁉️

Suddenly those $20,000 Dec '26 gold calls look like a sure thing...

silvertrade.com/news/preciou…

43

129

655

45,621

Taxation Is Theft. retweeted

12h

Trump’s press conference was INSANE:

He confirmed that:

• Iran gets $300B $100B unfrozen

• Iran has the RIGHT to ballistic missiles

• The U.S. was running out of oil

• A worldwide depression was coming

I was predicting all of this from the first week including that REPARATIONS were coming and got a lot of hate for it.

The sellout MAGA frauds are now going to change their entire life-philosophy and deeply held “principles” over night.

Trump is on his knees. This was ALWASY the ONLY way it was going to end. Even if he thinks he can start the war again. Iran will always win.

It’s check mate. Always has been.

748

3,804

17,993

729,446

Taxation Is Theft. retweeted

Jun 1

Ok, new CAGR is dropping:

63.5% over a span of 12 years.

35,900% total growth.

All my subs are super happy! Subscribe today!

Oh wait, I don’t run a subscription.

It’s all free!

Oooops I forgot. 😂🤣😏

Let’s keep winning guys!!!

50

7

548

115,772

Taxation Is Theft. retweeted

⚡🇨🇳 China has unveiled an upgraded version of its HJ-73 anti tank missile, showcasing the HJ-73D during live fire drills.

The missile features a tandem warhead designed to penetrate modern armored vehicles, while new footage highlights the PLA's continued push to strengthen its anti armor capabilities.

8

33

197

21,750

Taxation Is Theft. retweeted

A clip of a UK refugee council using girls as young as 12 years old to encourage migrant men to come to the United Kingdom is resurfacing amid the release of the grooming gang inquiry report.

Jail isn’t enough.

1,016

8,250

27,083

609,391

Taxation Is Theft. retweeted

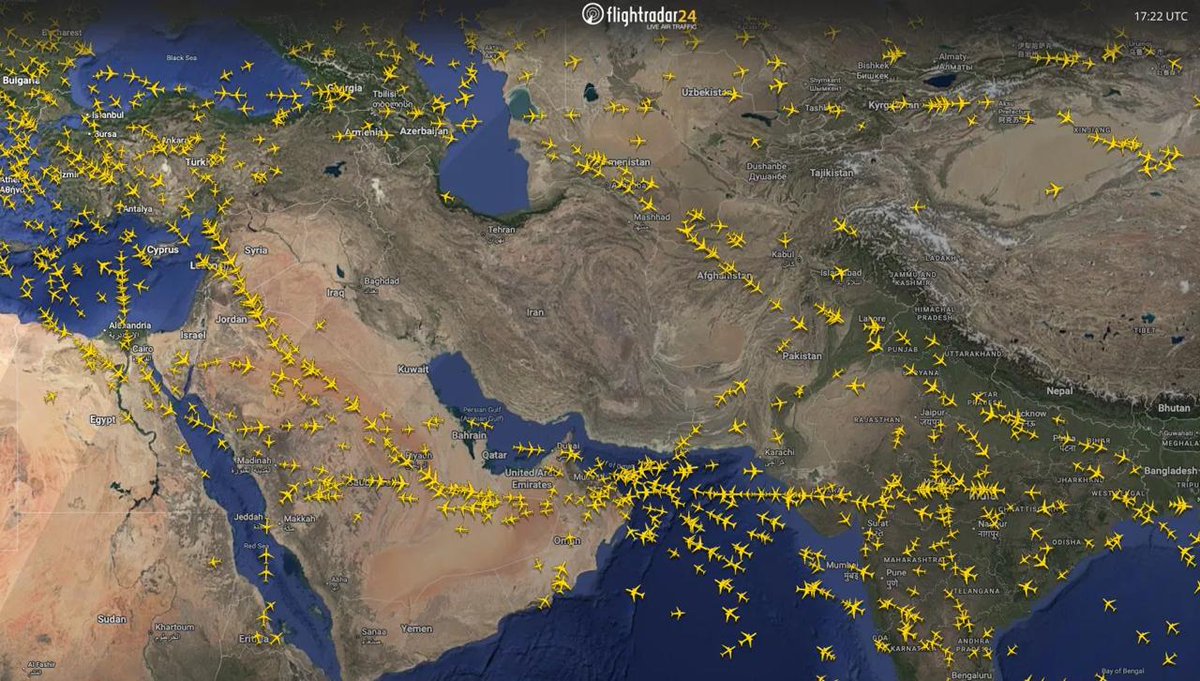

🇮🇷 Iranian airspace is effectively empty.

Sources on the ground report domestic flights in Iran have been canceled.

This comes as Iran's leadership signals the ceasefire is broken and threats of retaliation mount over continued Israeli strikes on Lebanon.

40

913

3,401

106,126

Taxation Is Theft. retweeted

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

THEY ARE GOING TO BAN VPNs

525

1,644

7,465

489,488

Taxation Is Theft. retweeted

ALERT: Horse dies in Central Park after eating Japanese yew plant, and the local union is outraged.

Deniz, a 16-year-old gelding horse, died after allegedly eating Japanese yew, a “highly toxic” poisonous plant, according to TWU Local 100, which represents carriage horse drivers.

TWU is awaiting the necropsy results to determine the exact cause of death, but says Deniz was healthy and had no illness prior to their death.

TWU representative Christina Hansen said, " Toxic plants have been planted in the park where our horses, or police horses, or parks department horses, or riding horses could easily access them. When a single mouthful is enough to stop a horse's park and kill them.”

81

184

829

191,395

Taxation Is Theft. retweeted

$NOK

Nokia Expands Semiconductor Test, Packaging Operations in Pennsylvania

$NOK will expand its advanced semiconductor test and packaging facilities in Allentown, Pennsylvania, to increase the manufacturing of photonic chips for artificial intelligence networks, the

The project will expand production capabilities tenfold, with the added capacity slated to become commercially accessible by late Q3, the company said.

3

10

93

6,851

Taxation Is Theft. retweeted

Everyone talks about GPUs, memory, and lasers.

But the real bottleneck is the only one both humans and data depend on to run.

IT'S WATER.

$ERII is up 8% today since I dropped my long thesis yesterday to clients.

So here's why this $500M water tech stock down 50% in 3 months could be an asymmetrical bet.

I first spotted $ERII in March, but I was too early.

Now I think a few catalysts put this small cap gem in prime re-rating territory.

$ERII makes a special piece of tech that makes desalination plants economical. The PX Pressure Exchanger recycles the pressure inside a seawater reverse osmosis plant and cuts its energy use by up to 60%. This hero product accounts for over 90% of $ERII's revenue and commands gross margins over 60%.

I love $ERII because it feels like a high margin IP business, not a low margin industrial, despite being priced like one.

So why is the stock trading half off its February $16 price and a fraction of its comps?

The Middle East, the world's largest desalination market, is 50% of their revenue. And two huge gut punches nuked the stock across two ER's.

1) Revised 26 guidance down before the Iran War started.

2) Removed 26 guidance entirely during the War due to the massive ME concentration of business. Then the CEO and CFO both left.

But the business isn't broken. And the Iran War looks to be resolved, making more signals of sustained ME peace a real catalyst.

Q1 is their smallest quarter historically and revenue still grew 20% YoY. The ugly Q1 loss was a one time charge from killing their CO2 side project. Q4'25 was a record $66.9M at 67% gross margin.

The balance sheet is a fortress too. $77M net cash, almost no debt, a 9x current ratio, ~$27M TTM FCF, and they buy back stock at a ~9% yield. You get paid to wait and this is not a small cap where you get diluted.

The tailwinds are massive for $ERII's desalination business and I think the market may be mispricing $ERII's growth potential on 4 vectors.

1) Fast Growing Market

Water scarcity isn't a regional story anymore, it's a global one. Rivers and aquifers are drying up while population, industry, and now AI all pull harder on the same shrinking supply, and desalination is the backstop the world keeps falling back on. Reverse osmosis dominates new capacity, every RO plant needs an energy recovery device, and the PX is the standard, so $ERII's installed base scales as desal scales globally.

2) Water As Warfare

The Iran war turned water into a weapon. Plants got hit across Bahrain, Kuwait, the UAE and Iran, and with desal supplying up to 90% of water in some Gulf states, every ministry just learned a centralized, aging fleet is a strategic weak spot. The answer isn't to build less. It's to harden, decentralize, and build MORE, which means more PX sales.

3) Middle East AI

Every gigawatt of compute landing in the Gulf has to be cooled, and up to 90% of the region's water comes from desal, so water is the constraint of where you can build. PwC sees Gulf data center capacity tripling to ~3.3GW by 2030, all running through RO where $ERII sells the picks and shovels. Management isn't even telling this story yet, but when they bring in a new permanent CEO, I could see him pushing AI water scarcity angle.

4) AI Factory Wastewater Upside

This one is early but $ERII just carved wastewater out as its own segment, it's ~6% of revenue today. It's the OTHER end of the AI water story: data centers and the chip fabs feeding them discharge dirty water and the laws require treatment before it leaves. ERII uses the same PX tech here with same 60% margin profile, and management expects this to get bigger in 2027.

The comps do a ton of the work to feel good about the valuation here.

$ERII has the smallest market cap and the highest gross margin in water tech (63%) while trading at the LOWEST 24x TTM PE multiple. ~25x vs $XYL 28x, $BMI 30x, $FELE 31x.

The catalysts?

- Iran War peace deal finalized

- $300B Iran investment would boost any stocks with strong ME geography exposure

- Company re-affirms guidance for 2026 in Q2 or Q3 call

- New CEO joins replacing interim CEO and maybe introduces AI angle to boost narrative

The risks.

Re-escalation. If Israel and Iran flare back up, the momentum dies and this might retests the lows. Projects will get even more delayed.

Guidance. The reinstatement they flagged for Q2/Q3 could be pushed to Q3/Q4 and come later than we hope.

Leadership. The CEO retired and the CFO resigned in the same quarter, and the permanent CEO search is still open.

Lumpy revenue. This is a project driven, back half-weighted business where big orders slip without warning. February proved it.

But the floor is real. ~$77M net cash (nearly 1/5 MC), no debt, a 9% buyback. A $500M company growing 20% retiring its own shares is not the kind that drops to 0.

DYOR. NFA.

Make sure to join my VIP discord through my Substack at the link in my bio to chat with me and our analysts about this name.

$ERII - Oil isn't the Middle East's most critical resource.

It's drinking water. And Iran just declared war on it.

Yesterday a drone strike on a Bahrain desalination put 90% of the population at risk.

And no one is talking about $ERII, a $500M micro cap with a monopoly on the key component every desalination plant on earth uses.

$ERII makes a ceramic pressure exchanger that recycles 98% of the energy in reverse osmosis desalination.

35,000 units installed worldwide. Zero competition. 65% gross margins.

CEO on Q4 earnings call confirmed this: "No other pressure exchanger competition that we see today."

Here's why this company deserves a massive re-rating.

Qatar's PM admitted the country could run out of drinking water in 3 days if plants are hit.

Kuwait gets 90% of its drinking water from desalination

UAE - 90%

Saudi Arabia - 70%

A leaked US diplomatic message warned Riyadh "would have to evacuate within a week" if its main desal plant was destroyed.

Over 60% of ERII's revenue comes from the Middle East.

These are literally their customers getting bombed right now.

And the stock is at 52-week lows.

Down 35% after a Feb 25 earnings miss.

ERII issued guidance on Feb 25. The war started Feb 28. Three days later.

This changes the entire calculus.

Forward P/E is 17.7x. Every water sector peer trades at 20 to 30.

The name is dirt cheap and the war catalyst has done nothing for the stock.

ERII has the best moat AND best margins (65% gross) in the entire sector. It's the cheapest name with a confirmed monopoly.

Post-conflict, Gulf governments will massively overbuild desalination capacity for redundancy.

Every new plant needs ERII's tech inside it.

This stock is due for a massive re-rating.

21

23

364

123,054

Taxation Is Theft. retweeted

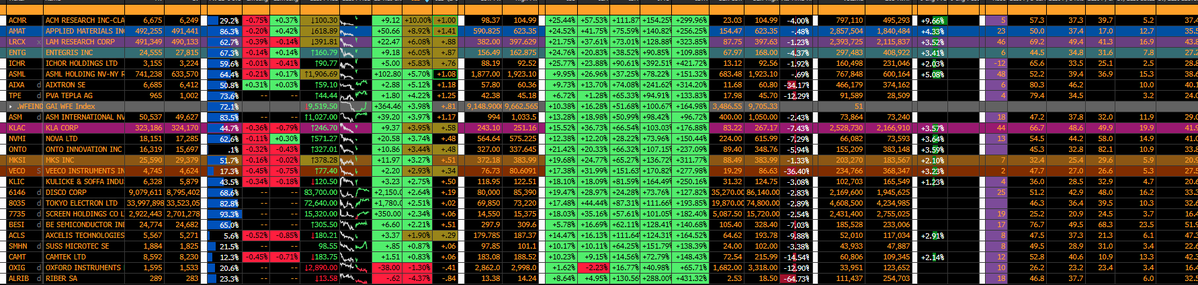

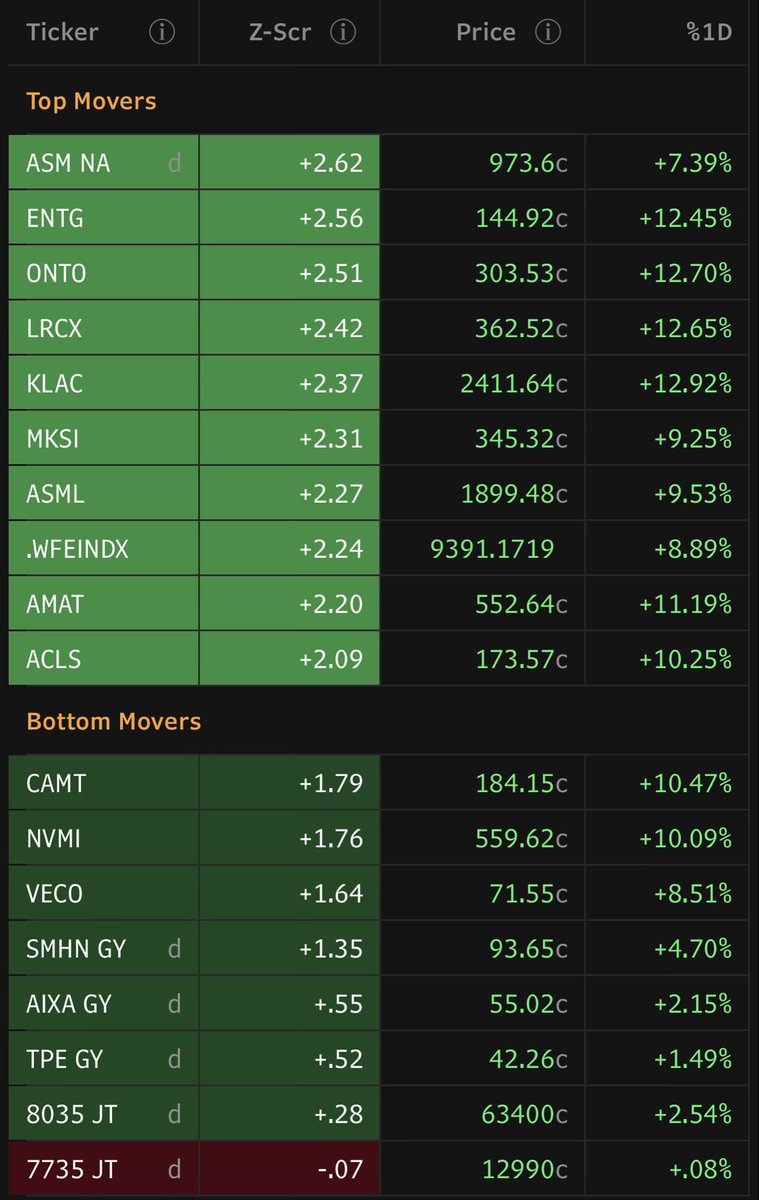

$AMAT $KLAC $LRCX $ASML Some of the WFE names going Donkey Kong today. AMAT up 9% is nuts. Still lots and lots more to go.

These are highly specialized companies within their relative niche, and once they are spec'd into a particular customer's fab generation, there is virtually no switching out. There won't be any credible new names emerging within the next 5-7 years (potentially China, and they will only serve the domestic Chinese market) - these existing companies will carve up all of the TAM between them.

Jun 11

$AMAT $KLAC $LRCX $ASML I can feel the momentum building even greater in the WFE names. Many at all time highs and many with 2z moves today. Looks like big money is chasing this trade. On my list is to build a detailed landscape map of all new fabs under construction.

1

2

20

4,034

Not a coincidence.

four companies supplying the backbone of the semiconductor industry are setting up to break multi-year bases.

$ENTG - Semi materials & filtration

$ALGM - Power & motion sensing

$APH - Connectors & interconnects

$DIOD - Analog & discrete semis

bigger the base, higher in space.

3

1

64

25,880

Taxation Is Theft. retweeted

POV: You realize this account tracks every move Jensen Huang makes.

Definitely worth a follow

Jensen Huang has been saying it for months:

AI is going to strain every power grid on the planet.

Here are 3 stocks worth watching:

2

7

365

211,989

Taxation Is Theft. retweeted

Jensen Huang has been saying it for months:

AI is going to strain every power grid on the planet.

Here are 3 stocks worth watching:

20

52

1,018

1,035,796

Taxation Is Theft. retweeted

13h

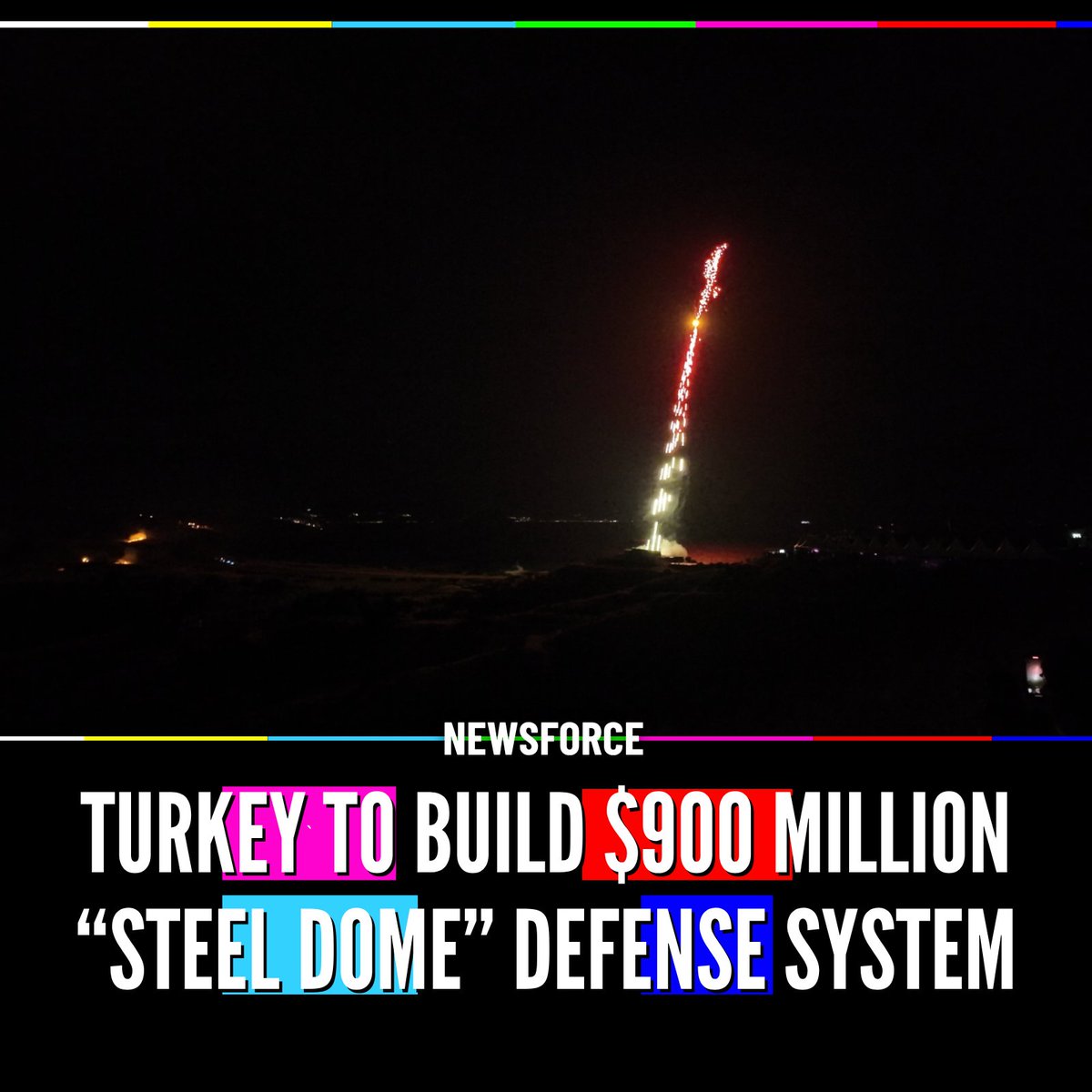

🇹🇷 Turkish defense giant Aselsan has secured a $900 million contract to provide key technologies for Turkey’s “Steel Dome” layered air defense system.

The ambitious project includes counter-drone tech, short-range systems like Korkut, directed energy weapons, and longer-range missiles—modeled after Israel’s Iron Dome and the U.S. Golden Dome.

Deliveries are slated for 2028–2032.

3

2

1,477

Taxation Is Theft. retweeted

Companies don’t make those investments unless demand visibility is extraordinary.

this is bullish not just for $COHR, but for the entire photonics ecosystem: $LITE, $TSEM, $ALMU, $AAOI and $AEHR

The market spent the last two years chasing compute.

The next phase may be chasing the technologies that allow compute to communicate.

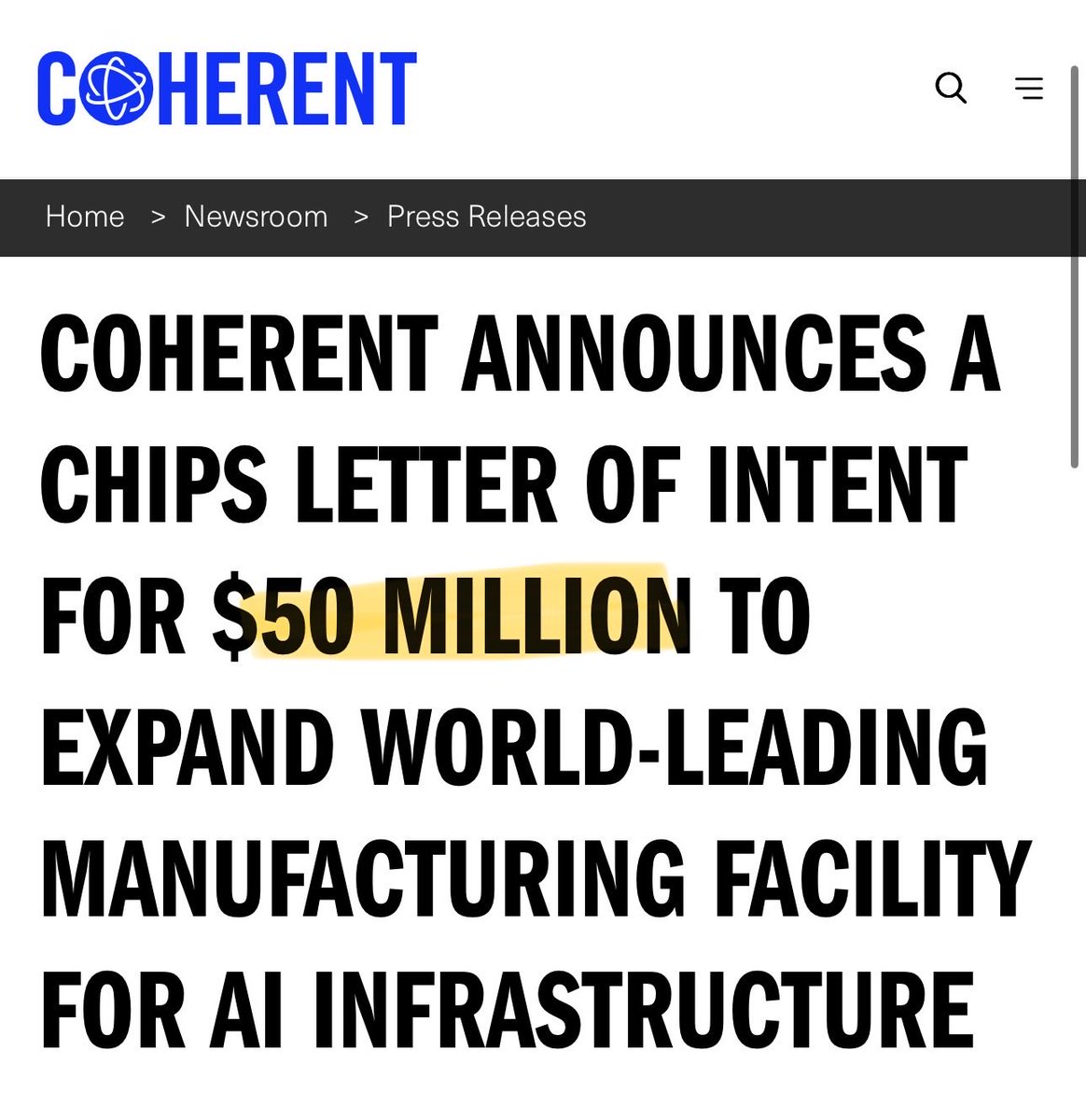

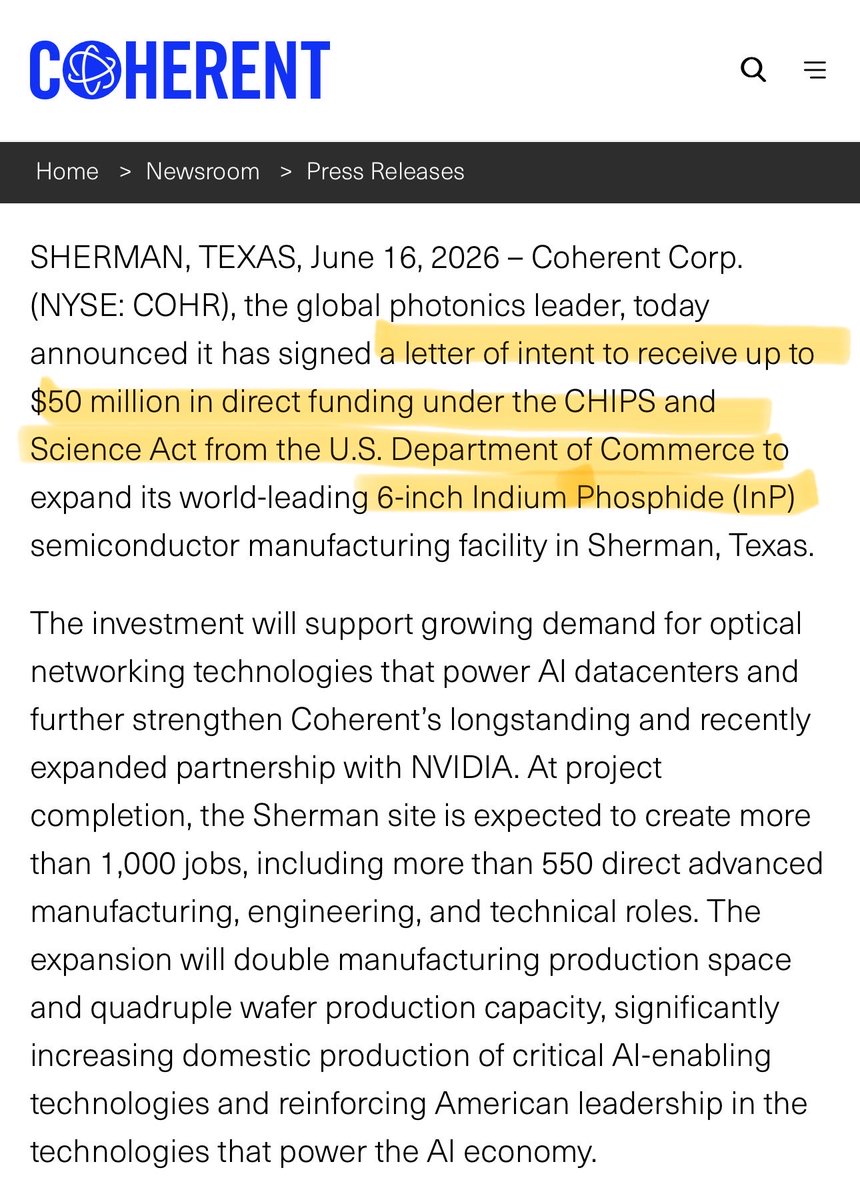

$COHR just secured up to $50M in CHIPS Act funding to expand 6-inch InP wafer production.

The headline isn’t the funding.

It’s the fact that Coherent is doubling manufacturing space and 4X wafer capacity to meet AI optical demand.

The InP shortage is real. The bottleneck is moving upstream.

4

103

215

34,054