Avid outside person with great inside skills. Bum and a fish. Startup/business lawyer.

- Tweets 2,034

- Following 823

- Followers 328

- Likes 4,025

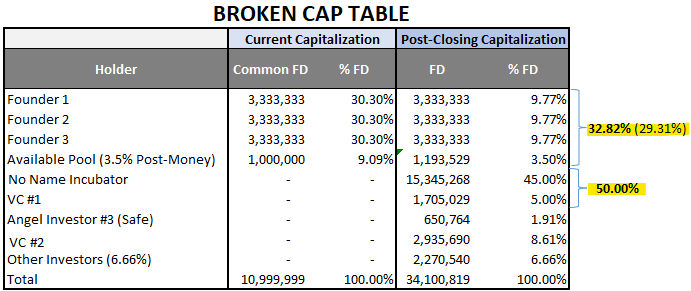

ALT This is a cap table shows a VC-backed startup that has been significantly diluted by one or more financing events. • Founders: The three founders each own 30.30% of the common stock before the funding round. However, after the funding round, their ownership is diluted to 9.77% each. This is a significant dilution. • No Name Incubator: The No Name Incubator is the lead investor in the funding round, and they will own 45.00% of the common stock after the closing. This is a very large stake for an investor, and it is likely that they will have a lot of control over the company. • Other investors: There are a number of other investors in the funding round, including VC firms, angel investors, and other companies. These venture capital investors will own a total of 21.22% of the common stock after the closing. • Available Pool: The available pool is the amount of common stock that is still available to be issued. In this case, the available pool is 3.50% of the common stock.