CIO @arca - digital assets investing | Former COO of Harvest Exchange | Former Lehman, Merrill, Citadel | Huge Cleveland Sports Fan | CFA charterholder

Joined December 2010

- Tweets 11,239

- Following 1,637

- Followers 48,088

- Likes 8,328

695 Photos and videos

Pinned Tweet

27 Feb 2025

There are a few Crypto hills that I will die on.

I've been writing about these topics, and debating people for years.

Today I'm laying them all out in one place. I will happily debate any of these topics with anyone at anytime.

A thread👇

79

45

434

137,394

Jun 12

Directionally agree with this. We think timeline is longer, the IB is probably worth a little less, and overall multiple will have crypto drag, but $GLXY is still wildly undervalued by all measures based on the data center business alone.

@Crypto_Alex17 nailed the $IREN $WULF and $CIFR thesis for us last year... has nailed GLXY thus far too. He's your guy for understanding crypto companies that have pivoted to AI

Some napkin math on $GLXY.

It's market cap is around $12B.

$GLXY has three core businesses:

> its crypto balance sheet, currently around $3-4b;

> its crypto Investment Banking type business;

> its data centre business.

Essentially, $GLXY already has 800MW approved and leased to $CRWV and has another 800MW approved (@novogratz said we'll learn of the tenant by July hopefully).

If you apply the same margins as their $CRWV deal, that is 2.4B in revenue and 2.16B in EBITDA (90% EBITDA margins). Say you slap a 15x P/ EBITDA, that's $32B on its data centre business alone. Say 1.6GW comes online 2028? So since market is forward looking, that's a FY 2027 price.

It also seems very likely that $GLXY can have 3.5GW come fully online by 2031/2032. Applying the same metrics, that's $5.25b in revenue and 4.725b in EBITDA in 2031/2032 just from the data centre business alone. At15x P/EBITDA that's $70b ($170 per share) in 7 years.

It's crypto IB business is another beast altogether, but I think it can conservatively be valued at $5B (bull $20B).

Conservatively, $GLXY should at least be $5B (IB Business), $30B (data centre, accounting also for 1.9GW more in study), and $3B crypto balance sheet.

That adds up to $38B. $GLXY is trading at $12B now.

I am long $GLXY.

9

10

125

34,222

Jeff Dorman retweeted

Some napkin math on $GLXY.

It's market cap is around $12B.

$GLXY has three core businesses:

> its crypto balance sheet, currently around $3-4b;

> its crypto Investment Banking type business;

> its data centre business.

Essentially, $GLXY already has 800MW approved and leased to $CRWV and has another 800MW approved (@novogratz said we'll learn of the tenant by July hopefully).

If you apply the same margins as their $CRWV deal, that is 2.4B in revenue and 2.16B in EBITDA (90% EBITDA margins). Say you slap a 15x P/ EBITDA, that's $32B on its data centre business alone. Say 1.6GW comes online 2028? So since market is forward looking, that's a FY 2027 price.

It also seems very likely that $GLXY can have 3.5GW come fully online by 2031/2032. Applying the same metrics, that's $5.25b in revenue and 4.725b in EBITDA in 2031/2032 just from the data centre business alone. At15x P/EBITDA that's $70b ($170 per share) in 7 years.

It's crypto IB business is another beast altogether, but I think it can conservatively be valued at $5B (bull $20B).

Conservatively, $GLXY should at least be $5B (IB Business), $30B (data centre, accounting also for 1.9GW more in study), and $3B crypto balance sheet.

That adds up to $38B. $GLXY is trading at $12B now.

I am long $GLXY.

14

28

215

54,549

Jun 12

Switching gears from my usual posts for a sec.

My 5-year-old son and I wrote a children's book together (years ago, but just now published it).

Fun little side project with my kid. Check it out if you have young kids🌼 amazon.com/dp/B0H3YN8SXS

or visit whenwillmarciabehere.com

5

20

1,455

Jun 9

Prediction markets are supposed to be about truth discovery. Last week showed what happens when incentives, capital structures, and market design collide with reality.

In this week’s That’s Our Two Satoshis, I cover two very different stories that both revolve around a simple question:

What happens when markets stop functioning the way participants expect?

First, I revisit the fallout from Strategy ($MSTR )’s first Bitcoin sale in four years. The sale itself was tiny (just 32 bitcoin:native ) but that wasn’t the point. The market reaction reflected growing concern that Strategy may eventually need to sell significantly more Bitcoin to satisfy its preferred dividend obligations or sell significantly more MSTR at non-accretive levels. My argument for the past three months has been that the risk is in the cash dividends. Once the market realizes the world’s largest Bitcoin buyer could become a forced seller, the narrative changes dramatically.

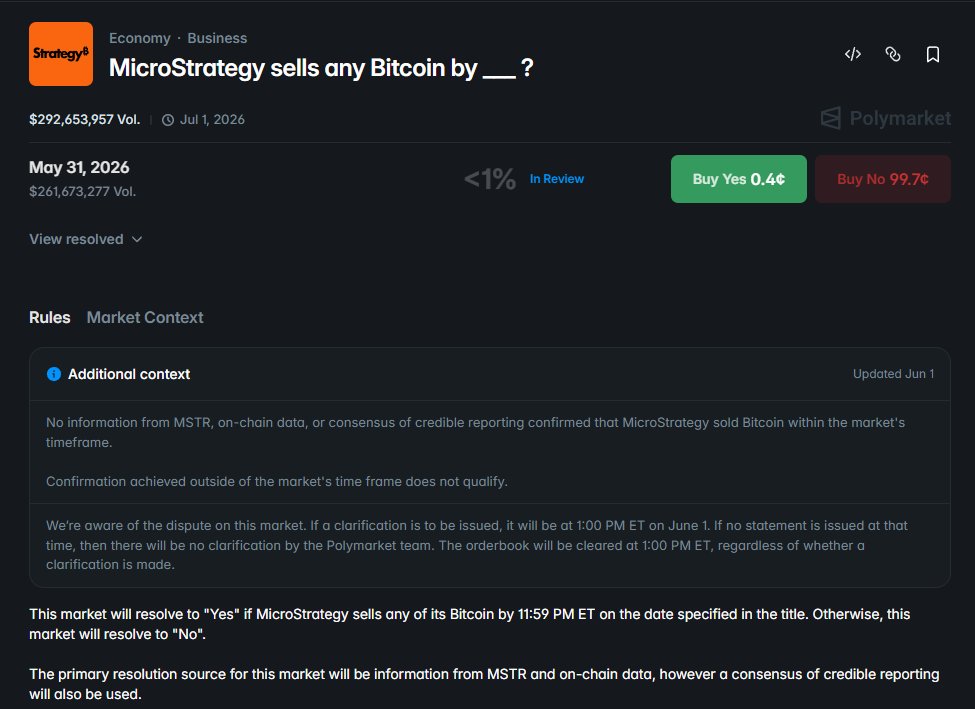

Second, I dive into what may become one of the most damaging events in prediction market history. A @Polymarket contract asked whether MicroStrategy would sell Bitcoin by May 31. Strategy later confirmed it had sold Bitcoin during that period. Yet the contract resolved NO, wiping out traders who correctly predicted the outcome. Nearly $400 million was wagered on the market, and the controversy raises a much bigger question: if prediction markets can resolve against reality because of technicalities and oracle mechanics, are participants actually betting on future events, or just on how a platform will interpret its own rules?

Prediction markets have enormous potential, and I’m a believer in the sector’s future. But credibility is everything. Markets can survive being wrong. They can’t survive losing trust.

9

3

40

5,251

Jun 8

Just about any company can raise money at 11.5% if they wanted to... they simply don't, because that's an incredibly high hurdle rate to overcome, no matter what you do with the money.

Just because $MSTR calls this innovative doesn't make it smart. Sure, BTC could go up more than 11.5% per year. It also may not.

But every company COULD do this. They could buy assets with the proceeds, or they could reinvest in their business, or they could even buy back their own stock. Many of these investments would outperform BTC. But again, no one does this, because 11.5% is a massive hurdle rate.

114

24

384

131,001

Jun 8

Yes. Let’s purposefully lose $16 bn in equity market cap so we can buy $180mm BTC on the cheap.

Smart move 🙃

"If I'm sitting in Strategy's c-suite, I now know I can acquire Bitcoin cheaper if I sell every once in a while and spook the market when I do it"

Dave on why Strategy will keep selling Bitcoin to drive the price down

"They're gonna do it again and again and again until the market is fully inoculated against it. You can't do that kind of legal manipulation more than a few times before people catch on that they're gonna get their faces ripped off by shorting against it"

"I learned something and they learned something last week. They probably also regret paying back the convert, but that's a different thing"

16

10

130

29,418

Jun 7

I think we’ve all learned that @Polymarket odds now mean absolutely nothing.

Could rewrite this as “90% chance that UMA voters and poorly written polymarket contracts will yield YES on something arbitrarily, and UMA holders and Polymarket whales likely also own YES”.

Jun 7

90% chance that Strategy has bought BTC last week according to Polymarket...

18

4

173

16,449

Jeff Dorman retweeted

Jun 6

Through the 2008 financial crisis was always the hardest thing for companies under stress to get their heads around: once the market smells blood you need to move fast - and typically bigger than expected - or your options rapidly disappear. It's the only way to stop the spiral. There are no half measures.

Surely Saylor has been advised exactly this, so after the 32 BTC sale debacle I'm hopeful he's taken that advice over the last few days and added $2bn to the treasury.

For bitcoin:native would expect a relief rally. Under any scenario I can't see $MSTR being a material buyer of BTC any time soon, but the price has already retraced (and then some imo) to price-in that change in demand/flows.

Jun 5

Only one scenario saves bitcoin:native and $MSTR in the short-term.

Saylor has to come out and say (via Monday's 8K, or next Monday's 8K):

"I sold $4 bn of MSTR and BTC... we now have 2.5 years before we have to raise money again... dividends are covered for 2 years, debt doesn't mature til sept 2028 (puttable in 2027) and that's easy to refinance via more converts".

If he does that, the market rips, and might even rip 20-30%. It once again makes MSTR uninteresting for years, but that's a good thing. STRC probably goes back close to $100, but he won't be able to sell more. And while capital markets might be closed to MSTR for awhile, it at least buys a ton of time, and in that time who knows what other catalysts might pop up.

He should have done this last week instead of that misguided $2.5mm teaser sale.

If he doesn't, and he continues to just wait it out (only has 5 months), or he sells tiny amounts as he goes (just enough to pay each monthly dividend), this selling won't stop

3

3

29

11,589

Jun 5

Only one scenario saves bitcoin:native and $MSTR in the short-term.

Saylor has to come out and say (via Monday's 8K, or next Monday's 8K):

"I sold $4 bn of MSTR and BTC... we now have 2.5 years before we have to raise money again... dividends are covered for 2 years, debt doesn't mature til sept 2028 (puttable in 2027) and that's easy to refinance via more converts".

If he does that, the market rips, and might even rip 20-30%. It once again makes MSTR uninteresting for years, but that's a good thing. STRC probably goes back close to $100, but he won't be able to sell more. And while capital markets might be closed to MSTR for awhile, it at least buys a ton of time, and in that time who knows what other catalysts might pop up.

He should have done this last week instead of that misguided $2.5mm teaser sale.

If he doesn't, and he continues to just wait it out (only has 5 months), or he sells tiny amounts as he goes (just enough to pay each monthly dividend), this selling won't stop

May 28

i'm not in Saylor's inner circle, but this $MSTR story has gotten so out of hand, my only guess is this:

- MSTR could have sat and done nothing before they started pumping out $billons of prefs... it would have made MSTR boring (little buys, no sells), but it would have been stable x.com/jdorman81/status/19959…

- But the push into these prefs was based on him clearly thinking $BTC was about to moon — not sure what he saw to think that (4 year cycle, flows, ???) but that's the only reason to take that sort of miscalculated risk to screw up his balance sheet so badly -- he must have thought BTC was about to fly and he could easily pay the pref dividends with future BTC sales.

- Then BTC started falling, and the market got spooked because the $15 bn in prefs have a $1.5 bn/year annual dividend, so he raised $2 bn in cash via stock just to alleviate any near-term default concerns — that bought him almost 2 years of runway to pay dividends. Smart move

At that point, he could have chilled for a little, and even though he now has every stakeholder pinned against each other, there was at least no near term risk x.com/jdorman81/status/20342…

- But then for some unknown reason, he decides to take that cash buffer and buyback 2029 maturity bonds instead of using it to fund the annual dividends (at a discount, so it's at least mildly accretive to MSTR). This is a baffling decision for a company with cash flow problems. Why pay off 0% coupon debt with the only cash you have?

The only bull case is that underestimating Saylor's capital markets chicanery has been a losing proposition for years. Maybe there was a plan?

That plan may just be selling BTC, which he will have to do eventually, but if he does this while BTC is in a death spriral it's going to crush BTC and MSTR. So again, why buyback the debt now and force your hand sooner than you have to?

Maybe he is going to refinance those converts with new longer-dated converts? He has sworn off converts, so I doubt it, but that would at least logically make sense.

But TLDR -- this is the first time that MSTR, BTC and Pref holders are really in bind. Someone is going to lose badly here, and it will happen in the next 4 months.

131

69

848

387,061

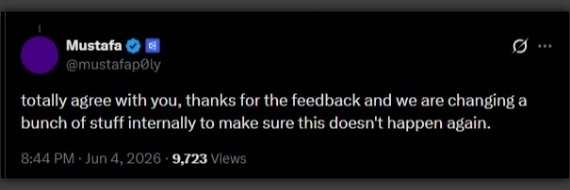

So after all the MicroStrategy resolution drama, Polymarket says '' we're changing things internally so it doesn't happen again. ''

Total trash talk from them again, exact same vague promise after the last big failure (the Ukraine minerals market). Nothing actually changed and problems got worse.

@Polymarket keeps making the same empty promises after every scandal, but their root problems (weak rules, UMA manipulation, lack of transparency) never get fixed.

genuinely insane to me Polymarket has no shame for a company valued at Billions dollars.

35

6

99

3,337

Jeff Dorman retweeted

Jun 5

😬 @jdorman81 on Strategy's capital structure crisis: no matter which stakeholder class you own, the risks are higher than nine months ago.

Every option Saylor has damages at least one class of holder. 🎧

Timestamps:

🐦 01:18 How MSTR was sitting pretty until it complicated its capital structure and put itself in a bind

🎾 04:49 How MSTR committed an unforced error, giving itself only 5 months of cash left

🔀 08:43 Four options, four stakeholder classes, at least one loser each

💼 20:23 Fidelity: Explore opportunities at crypto.fidelitycareers.com

📊 21:23 Jeff ranks the capital structure positions by probability

🎲 27:00 Polymarket: a confirmed Bitcoin sale is resolving 'no.' How did that happen?

7

8

40

17,674

Jeff Dorman retweeted

Jun 4

I want to talk about the mNAV that everyone refers to on here for $MSTR

The thing I see is people saying something like “mNAV is 1.2 so relax”

Let me show you what that number quietly leaves out or hides. I want everyone to follow so I’m going to explain it simply, because it can be confusing.

Think of the company as a house made out of Bitcoin. Worth about $54bn right now, call it 843,000 coins.

But theres a mortgage on the house. They owe roughly $22bn to people who get paid before the owner or the house (ordinary shareholders). Say $7bn to bondholders and $15bn to the preferred holders, STRC and its cousins.

So what do shareholders actually own?

House minus the mortgage. About $32bn. Just that part.

Now there’s two ways people measure the shares against the Bitcoin (2 ways to measure mNAV)

The one everyone uses and makes you feel good takes the whole mortgage, adds it back on top of the shares, divides by the house. Comes out near 1.2. Above one, all fine, all looks good.

The simpler one just compares the value of shares against the house. Near 0.84 currently.

Here’s the trick. By adding the mortgage back in, the 1.2 cancels out the borrowing.

The thing that makes things difficult to see, the debt, which is added back into the sum so you cant see it. Fine for comparing two companies on a quiet day. No use for the way this hurts you.

The part nobody wants to talk about is what happens to your Bitcoin per share when they print more shares.

In a bull market it works. Sell shares for more than the value of the Bitcoin, buy more coins, everyone’s BTC per share nudges up. In a bull market.

Trouble is the shares now trade below the Bitcoin sitting behind them. So printing shares to buy coins today actually drags your Bitcoin per share down. The number they publish themselves.

And worse than that, when they print shares not to buy Bitcoin but just to pay bills, thats not clever, it’s just pure dilution. More shares, same coins, thinner slice.

Before anyone says I’m making it up: last week of May. They sold about $128m of new shares and bought zero Bitcoin with it. Nothing. Same week they sold 32 coins to help pay the preferred dividend. More shares knocking about, fewer coins in the pot, everyone holding it left with less Bitcoin per share. Thats not a flywheel.

The preferred’s pull the same stunt to cover the dividend. Sell more STRC just to pay this months bill and the mortgage gets bigger while the house stays the same size. Its remortgaging the house to pay the mortgage. Debt up, house flat, your slice bleeding. And Bitcoin hasnt even dropped yet.

Now let’s see what happens if the house price (Bitcoin) drops.

The mortgage doesnt move. $22bn whether Bitcoin’s at 64 grand or 20. Doesnt shrink because the house did. So when the house falls, who takes it on the chin? The owner of the house. First, and all of it. Bitcoin falls 15% and your slice doesnt fall 15, it falls nearer 25. Debt sits still, house sinks, the whole lot lands on the equity. Leverage in reverse.

Real numbers. Bitcoin’s about 64k. It only has to fall around 60%, to about 26k, and the owners has nothing left. Gone. Fall to about 8k and even the “safe, senior, stable” preferred has nothing under it.

And heres the bit that I want you to notice. What do the two numbers do while thats happening?

The comforting 1.2 doesnt fall as the owner gets wiped out. Using today’s figures it actually goes up. 1.25 now, about 1.61 by the time the owners slice hits zero. Looks healthier the worse it gets, cause the fixed amounts are now a bigger chunk of a smaller house.

The 0.84 simpler one falls (basic mNAV) on the other hand falls to 0.71, then 0.61. Moves with the damage.

So when someone says 1.2, relax, have a think about what that really means. Thats the version of mNAV that moves the wrong way when it all goes south, by design.

Want to know what’s actually happening when Bitcoin drops, watch the simple one (basic mNAV)

22

26

142

23,680

Jun 4

The Polymarket PR team probably banking on the hopes that this egregious mistake/fraud/scam will just fade away with time. And they are probably right. The reality is, most people are selfish, and only really care about things that directly affect themselves... so they are right to assume that this will have a short shelf life since very few were actually negatively affected.

But this will be an interesting case study in the persistence of public opinion that is almost unanimously against the outcome vs a company that went from $1 bn market cap to $20 bn market cap almost overnight and easily has the means to do the right thing should they choose to.

20

6

191

8,519

Jeff Dorman retweeted

Jun 4

Most annoying part with the @Polymarket situation is not the money they scammed from me in a market I clearly won based on rules.

It is all the little weasels with their badges coming out of the woodwork doing gaslighting and "acktually" posts while in reality every single one of them knows how full of shit they are...

despicable behaviour truly

13

11

179

5,658

Jeff Dorman retweeted

Jun 4

Let me be clear, because softening it helps no one: this resolution was wrong.

The market asked whether Strategy SOLD any Bitcoin by May 31. It did. Strategy’s own 8-K, the primary resolution source @Polymarket named, dates the sale inside the window. The only way to reach NO was to bolt on an “Additional context” after the deadline that quietly swapped “did they sell” for “was it announced,” which is the exact move @Polymarket’s own rules say a clarification cannot make. The standard was broken, and real people paid for it.

But I am not here just to point at the problem. There is a solution, and it is one where both @Polymarket and the YES holders come out ahead.

Make every YES holder whole at $1, and pair it with a platform-wide review that cleanly separates two things the rulebook currently blurs: did the event happen by the deadline, versus was it confirmed by the deadline.

Why this is a win for @Polymarket, not a concession. The disputed amount is a rounding error against the volume you handle. The goodwill of being the platform that trades truth, not technicalities, is something marketing cannot buy at any price. Framed as a rules reform rather than a reversal, it kills the precedent worry: you are not caving to noise, you are fixing a genuine structural ambiguity and making the people caught by it whole. It slots directly into the integrity overhaul you have already announced.

The alternative only looks cheaper. Quietly clarifying the rules “going forward” with no payout leaves your users carrying the cost of your ambiguity, and it becomes the case study every regulator and competitor points to when they ask whether a Polymarket resolution can be trusted when money is on the line.

You wrote the rule that a clarification cannot change a question’s fundamental intent. Honor it. Make YES whole, fix the rulebook for everyone who comes next, and this stops being the week you lost trust and becomes the moment you earned it.

The right thing here is also the profitable one.

#Polymarket #PredictionMarkets #StopPolyScam @0xDinoCrypto @willo2_Poly

Jun 3

Don't take my word for it. Take @Polymarket 's.

There is only one thing a prediction market actually sells. Not odds, not liquidity, not volume. Those are commodities. The product is a single promise: that once your capital is committed, the question you bet on cannot be quietly rewritten underneath you. Everything else is built on top of that promise, and when it breaks, nothing else the platform offers means anything.

@Polymarket is about to break it on one of the largest disputed market of its year, a contract that has now traded roughly $292 million and is still climbing, and it is doing so in direct contradiction of its own published rules.

The facts are not in dispute. The market asked one event-based question: “MicroStrategy sells any Bitcoin by May 31, 2026?” The rules resolve it YES if Strategy sold any bitcoin by 11:59 PM ET on that date, and they name the primary resolution source in plain text: information from MSTR. This was never a question about disclosure timing or filing schedules. It asked whether an event happened.

It happened. Strategy’s own 8-K reports 32 BTC sold between May 26 and May 31, presented “as of May 31, 2026, 4:00 p.m. Eastern Time,” squarely inside the window. That is not a rumor, an inference, or a hostile reading. It is the exact primary source @Polymarket chose, confirming the exact event the market was written to track. Under the rules as written, this resolves YES.

So how does it resolve NO? Only by rewriting the question after the outcome was already known. After the deadline had passed, after the filing was public, and while the market was still open, @Polymarket appended an “Additional context” note that quietly converted “did Strategy SELL by May 31” into “was the sale ANNOUNCED by May 31.” That condition appears nowhere in the original rules. It surfaced only after the outcome was already public.

And understand who did that. @Polymarket is not a bystander to this outcome. It proposed the “No” resolution, and it authored the very context now being used to defend it. This is not a neutral referee reporting what token holders decided. It is the house writing new rules in the middle of the hand.

Here is the problem, in their own words. @Polymarket’s documentation states that a clarification “cannot change the fundamental intent of the question.” That is not my standard. It is theirs. Turning an event-based question into an announcement-based one is the textbook example of changing the fundamental intent. The rule exists specifically to stop this maneuver. By their own published standard, this is a breach.

There is no honest “No” reading that survives the design, either. Strategy reports its bitcoin activity on a weekly cadence, usually on Mondays. A sale executed in the final days of any month can never be publicly confirmed before a month-end deadline. So a “No” here is not a finding about whether Strategy sold. It is a wager on SEC filing calendars, which is not the question anyone was offered when they put their money down.

This is where integrity stops being an abstraction. A platform’s character is never revealed when following its own rules is free. It is revealed when following them is expensive, when the rules point one way and the largest holders of @UMAprotocol’s voting tokens point the other. Independent reporting has already documented how concentrated that voting power is, and how a system that punishes minority voters quietly pushes everyone toward whatever the biggest wallets want, regardless of what actually happened. If that machinery is allowed to override a platform’s own written rule and its own chosen source, the resolution process is not arbitration. It is theater with a settlement layer.

Anyone who takes @Polymarket’s mainstream ambitions seriously should sit with this. A platform pursuing the legitimacy that regulators like @CFTC exist to confer cannot, in the same breath, demonstrate that its outcomes answer to token weight rather than to its own rulebook. If it will rewrite its own rule to steer a market approaching $300 million, the only fair question is what any registration it holds or seeks is actually meant to guarantee. Integrity rules abandoned the moment they become inconvenient are not integrity. They are marketing.

There is a clean precedent for doing the right thing. @Polymarket has overruled its own oracle before and refunded the affected side when an outcome was indefensible. That option is on the table right now. The event happened inside the window. The primary source confirms it. The original rules require YES.

So the platform faces a choice it cannot escape, and both doors are open to the public. Resolve it YES, and the rulebook means something. Resolve it NO, and you will have answered, permanently and on the record, that your rules hold only until they cost you. On a market that has moved nearly $300 million, that single decision is the most honest disclosure @Polymarket will ever make about its own integrity.

$MSTR #Polymarket #PredictionMarkets #DeFi

24

6

34

4,218

Jun 2

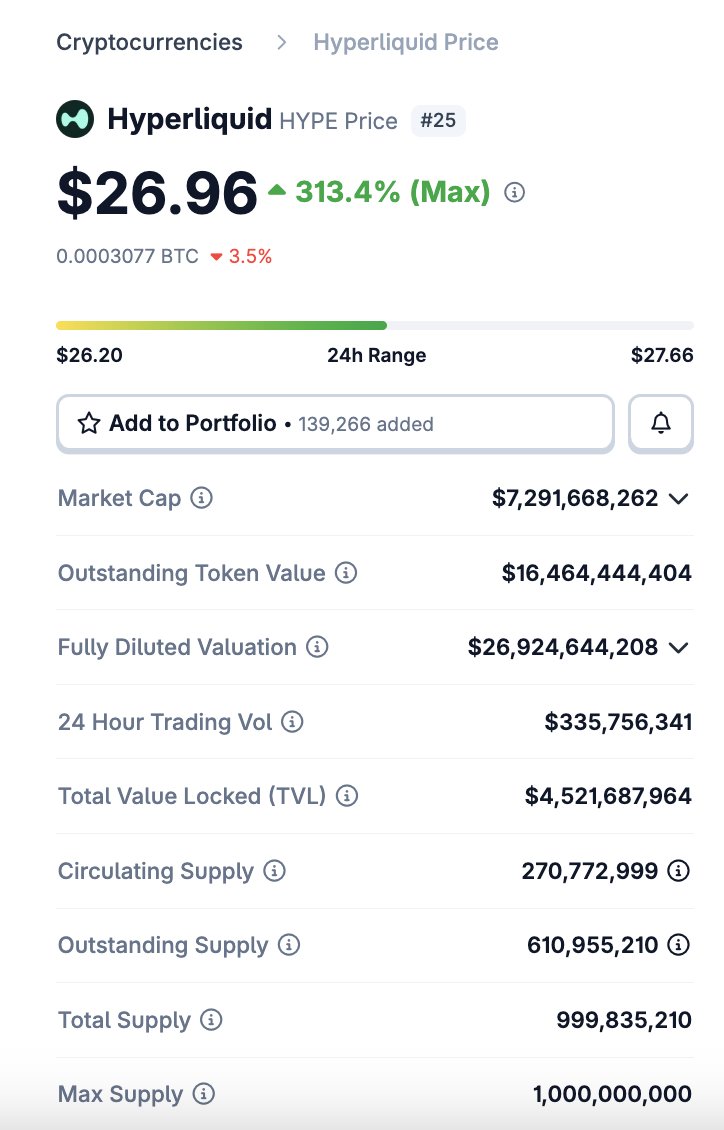

Wrote this about $HYPE success and $MSTR failure on Sunday night... a lot of it already playing out, but still worth a read as the stories are far from over

ar.ca/blog/hypes-success-mst…

3

2

10

3,236

Jun 2

While I'm not cheering for bitcoin:native to go lower, I am cheering that BTC is going lower while many other crypto assets are not, and others are outperforming BTC. This underperformance is clearly due to the Saylor / $MSTR selling news, which is an idiosyncratic downside risk for only BTC.

If this holds, and BTC doesn't take down the whole market, it is yet another sign that digital asset market participants are becoming more sophisticated. This industry was historically held hostage by misinformation from the large exchanges and influencers, and uninformed media coverage, who failed to educate investors on the nuances and differences between different sectors and types of crypto assets.

If investors are now able to properly assign individual risks to assets rather than blindly buying/selling the whole market, then this becomes a much more investable asset class for the masses and institutions.

35

8

116

21,245