Senior fellow at the Atlantic Council GeoEconomics Center. Former IMF, former WSJ/AWSJ.

Joined April 2009

- Tweets 2,525

- Following 317

- Followers 648

- Likes 1,002

26 Photos and videos

Jeremy Mark retweeted

It is harder than ever to find good news in China's data release today. The economy continues to be structurally locked into increasing production at the expense of consumption, even though China suffers from many years of growing excess capacity.

China's industrial output, for example, increased by 5.4% year on year in the first five months of 2026, with a 4.5% year on year increase in the month of May. This was a little higher than April’s 4.1% increase, although lower than the 5.7% increase in March.

The uglier numbers were (as always) on the consumption side. For the first five months of 2026, total retail sales grew 2.8%, just over half the pace of industrial output. Although they were barely expected to grow in May, in fact they actually fell by 0.6%, well below the disappointing 0.2% increase in April and the first decline since the end of the Covid lockdown in 2022.

For all the excited claims about consumption spending during the important May holiday, in other words, it was more than offset by the decline in spending over the rest of the month, proving, once again, that what limits household consumption is the household budget, not spending opportunities.

Meanwhile China's fixed-asset investment declined 4.1% year on year in the first five months of 2026.

Last week's trade and debt numbers reinforce the claim that China is finding it harder than ever to restructure its economy. It is expending huge resources in growing output, especially manufacturing output, but Chinese producers rely more than ever on soaring exports to offset weak domestic demand.

So far this year's numbers show that China's economy has further increased its already-excessive dependence on surging debt and soaring trade surpluses to keep GDP growth from slowing. It is not clear how much longer this growth model can be sustained before China is forced into a very difficult economic adjustment, but it is almost impossible for China to exit this model without a sharp slowdown in near-term growth, which is why, for all its promises, Beijing has been unable to adjust.

The problem, of course, is that as long as this process continues, it will increase the final adjustment costs for the Chinese economy and will further undermine manufacturing in the rest of the world.

english.news.cn/20260616/dbe…

26

76

277

33,949

Jun 10

Oh, the irony of this response: A spokesperson for the Chinese embassy in Washington said the Pentagon was “overstretching the concept of national security and making discriminatory lists to go after Chinese companies.” @ACGeoEcon @ACGlobalChina

wsj.com/politics/national-se… via @WSJ

17

Jeremy Mark retweeted

Apr 23

Thanks to @jedmark888 and the @ACGeoEcon for a conversation about my new book "Emerged Markets - The Global Economy's Better Half", published by @routledgebooks. In a nutshell, we spoke about the rise of the rest!

🎗️ What are “emerged market countries”?

“You’ve got 25-40 nations, all of them middle income or on the doorstep of fully developed. These nations, in my view, deserve a little bit more respect and recognition,” @vshastry tells @jedmark888. ⬇️

youtube.com/watch?v=pNQ-9mD6…

1

101

Jeremy Mark retweeted

Apr 22

Understanding China !

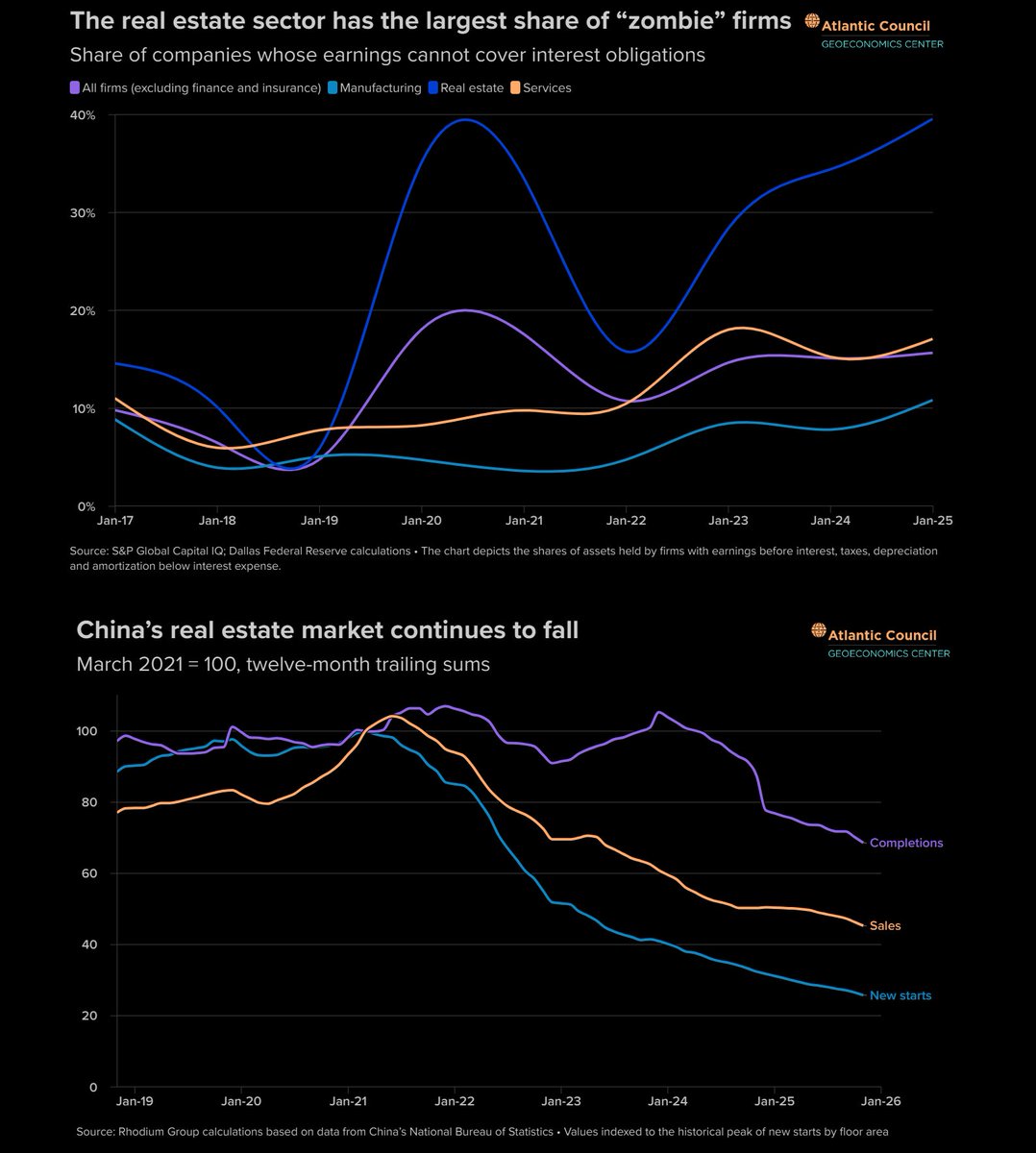

Should the World be worried about China’s current economic path? (4)

In this fourth post of the series, we focus on China’s real estate market.

The data point to a clear structural strain. The share of “zombie firms” , companies whose earnings cannot cover interest payments , is highest in the real estate sector, reaching nearly 40%, significantly above manufacturing and services. This indicates rising financial stress and declining profitability within the sector.

At the same time, real activity continues to weaken. Since the 2021 peak, new housing starts have collapsed to around 25–30% of peak levels, while property sales have fallen to nearly half, and completions are also trending downward. The simultaneous decline across construction, sales, and completions suggests not just a cyclical slowdown but a deeper adjustment process.

Taken together, these trends highlight the central role of real estate in China’s current economic trajectory. Given the sector’s strong linkages to construction, local government revenues, and household wealth, prolonged weakness could have broader spillover effects across the economy.

Note: These posts are not intended to be critical of China. As one of the world’s largest economies, developments in China inevitably have global implications. The objective is simply to understand the direction of the Chinese economy.

Source: @AtlanticCouncil by @jedmark888

Apr 21

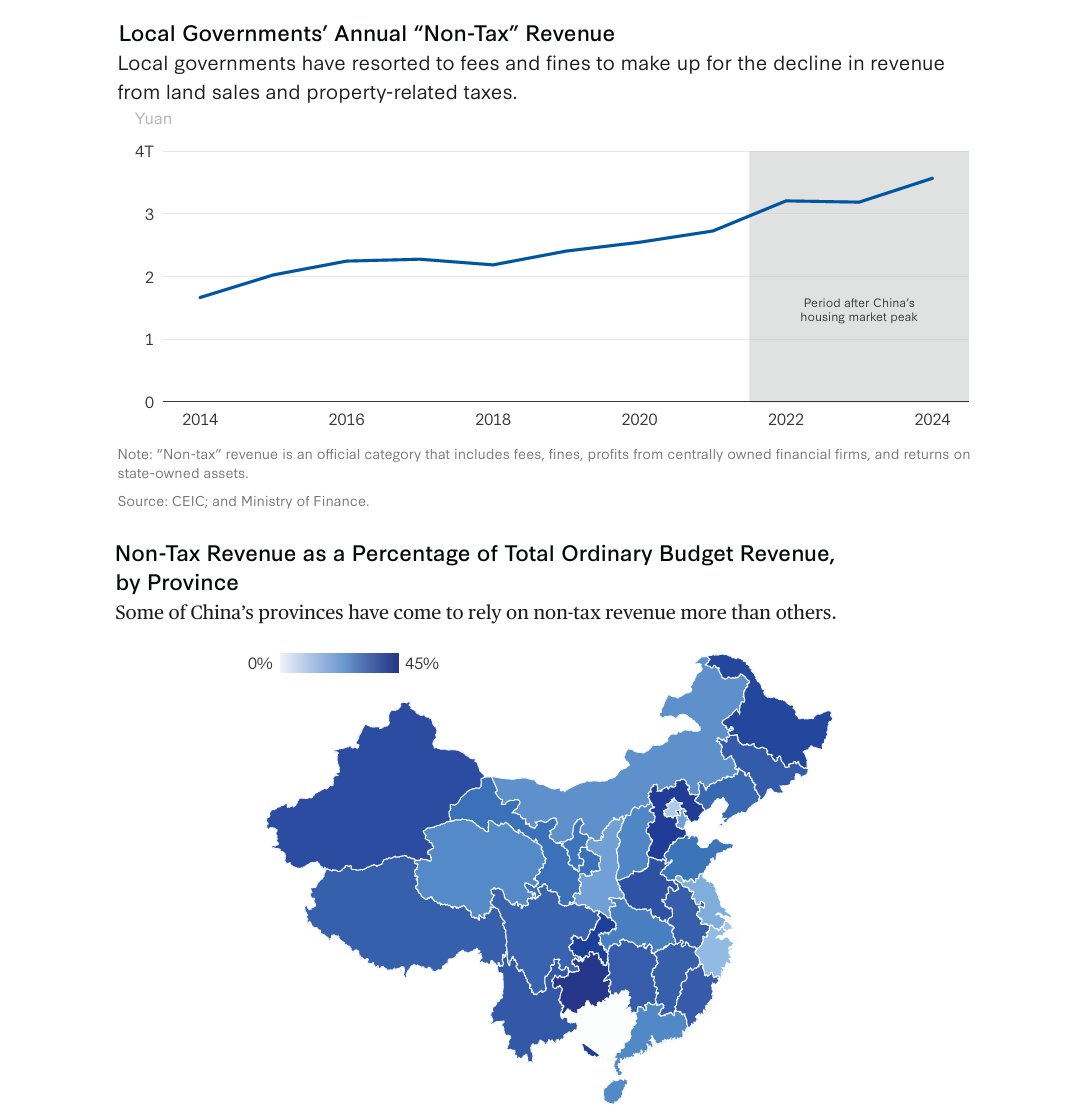

Understanding China !

Should the World be worried about China’s current economic path? (3)

Local governments, shifting revenues, and a silent transformation

China’s local government revenue model is changing fast. Property-related income and property tax income are weakening, while alternative revenues and central support are rising.

The data below shows how deep this shift is.

Is this stabilizing… or a growing risk? You decide.

1) Non-tax revenues are rising sharply

Local non-tax revenues increased from ~1.7T yuan (2014) to ~3.5T yuan (2024)

Growth accelerates after 2021

As property revenues fall, fees, fines, and other non-tax income are being scaled up

2) Some regions are highly dependent

In several provinces, non-tax revenues exceed 40% of total income

Strong regional divergence: This is no longer temporary, in some areas, it has become structural

Sources:

@csis by Dinny McMahon and Andrew Polk

zhuoyongliang .blog.caixin

3

19

1,962

Apr 16

Buried in the IMF World Economic Outlook is a disquieting projection: The commodities team expects food prices to rise by 6 percent this year. That has serious implications for global food security. My take for @ACGeoEcon @AtlanticCouncil

atlanticcouncil.org/blogs/ec…

2

3

10

1,495

Jeremy Mark retweeted

“The US has to recognize that we have a competitor in China,” says @ACGlobalChina’s Melanie Hart at the Global Prosperity Forum.

“And if we want to be the partner of choice in Latin America, we can’t be flip-flopping policy back and forth,” she adds.

3

6

7

1,980

Jeremy Mark retweeted

In Africa, there hasn’t been a damaging effect of people’s views of China vis-à-vis support for democracy, says @afrobarometer’s @joeasunka at the Global Prosperity Forum.

But the fear is that corruption, if left unchecked, will reduce people’s commitment to democracy, he adds.

5

7

1,790

Jeremy Mark retweeted

Across 38 African countries we surveyed between 2024 and 2025, China is the country with the most positive influence on the continent, says @afrobarometer’s @joeasunka at the Global Prosperity Forum.

The US comes in at the 4th position, he tells @ACGeoEcon’s @jedmark888.

2

12

9

2,470

Jeremy Mark retweeted

We have to recognize that in some cases, what China is building overseas are projects that are needed, and we weren’t going to build them, explains @ACGlobalChina’s Melanie Hart.

But there are problems that are consistent across a lot of China’s development portfolio, she adds.

1

5

7

2,062

Jeremy Mark retweeted

What we see today is that many developing countries borrow money from China and face an indebtedness problem, says @hofunghung at the Global Prosperity Forum.

“It is not so much different from the loan performance problem in the domestic economy of China,” he explains.

2

4

15

12,561

Apr 11

An illuminating exchange on China and international debt restructuring process.

Apr 10

Am sure Yufan describes the basic view of many in Beijing --

At the same time, the world has already made enormous accommodations to China, and I am not sure China has made much effort to accommodate other creditors that also have claims ...

1/

44

Apr 2

An important analysis from @CGDev on the potential impact of the oil price spike on low-income countries facing food insecurity. Most vulnerable are poor households that spend 50% to 70% of their budgets on food. @ACGeoEcon

cgdev.org/blog/when-oil-pric…

27

Jeremy Mark retweeted

Mar 13

Now available on @routledgebooks and @amazon - my book "Emerged Markets - The Global Economy's Better Half". Looking forward to debate and dialogue on the thesis and themes of the book. Please DM me!

2

7

15

1,749

Feb 10

What to make of China's warning to its financial institutions to limit buying of US Treasuries? @joshualipsky and I examine what's behind this development. Hint: it's tied to the internationalization of the RMB. @AtlanticCouncil @ACGeoEcon @ACGlobalChina

atlanticcouncil.org/blogs/ec…

3

5

1,426

Jeremy Mark retweeted

🇨🇳 China’s property crisis continues, with no end in sight, but Beijing seems content to ignore the reality of the problem. @jedmark888 explains how this weighs on the financial system and household consumer confidence.

Read the full piece 🔽

atlanticcouncil.org/blogs/ec…

1

3

202

Jan 28

As China’s property crisis drags on, Beijing talks of a “new model” of real estate. But the problems remain: zombie firms weigh on the financial system and a generation of household wealth is lost. My latest for @AtlanticCouncil @ACGeoEcon @ACGlobalChina

atlanticcouncil.org/blogs/ec…

2

3

1,728

Jan 22

Domestic Demand Dead End: "China is developing something of a Potemkin economy. Retail sales depend to a large degree on trade-in subsidies for items ranging from white goods to mobile phones. It isn’t sustainable." @ACGeoEcon @ACGlobalChina

“China needs what President Xi Jinping is unlikely ever to grant: a freer market that unleashes the entrepreneurship of ordinary Chinese people. China could grow much faster if Beijing would let it.” @WSJopinion wsj.com/opinion/china-econom…

1

88

31 Dec 2025

Will Wonders Never Cease? "Yet investment is headed for its first annual contraction since 1998, growth for retail sales has hit the worst pace outside the pandemic and new home prices fell further in November." @ACGeoEcon @ACGlobalChina

bloomberg.com/news/articles/…

61