Look for value where value can be found. posts NFA. please challenge any of my posts/ideas Check out my Substack: substack.com/@hayncapital

Joined May 2024

- Tweets 627

- Following 470

- Followers 609

- Likes 2,681

49 Photos and videos

Jun 12

Great article behind the complexity of the software capabilities needed to extract adequate compute (MFU) from AI hardware.

Then combine this with $IREN and their recent acquisition of Mirantis who works closely with Nvidia on exactly the complexities required to increase MFU from the hardware

$IREN GW pipeline access to hardware and capital direct collaboration with Nvidia in deploying DSX architecture to improve maximum compute per data center through rack architecture and the thesis gets even stronger.

I honestly was not knowledgable about this when I first researched $IREN in 2025 and if I had known I would have probably been more skeptical but now that they have these capabilities in house the value of their MW get's a lot more interesting.

It is a lot easier to acquire a software team to increase MFU then it is to acquire GWs of grid connected power.

Side Note: $CRWV MFU numbers are impressive

open.substack.com/pub/chiplo…

1

319

Jun 10

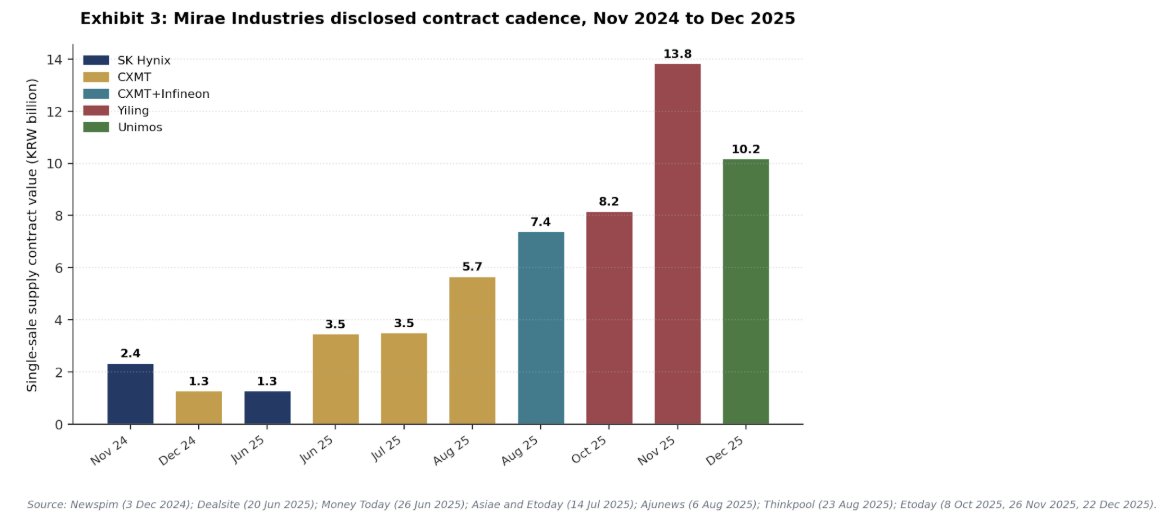

China Memory Capex go brrr

Another 15B won order on June 1 for $025560.KS Mirae Corp Test handlers

Q2 Started March 31st

Since then they have announced 37B KRW in contracts so far in Q2

06/01 15.4B KRW (Yiling)

5/27/26 3.6B KRW (direct order from YMTC)

5/20/26 2.6B KRW (SK hynix)

5/20/26 4B KRW (SK hynix)

5/13/26 8B KRW (Unimos)

4/29/26 3.8B KRW (Yiling)

*Unimos is assembly and test arm for YMTC

*Yiling inferred to be a trading intermediary for YMTC and CXMT

To put this into context

- Full Year 2025 revenue was 50B KRW they have almost met that in one quarter

Q126

- revenues were 21B KRW

- EBIT was 4.9B KRW ~24% ebit margins

They are about to hit 100% QoQ revenue growth

Applying a 25% ebit margin to the 37B KRW in orders so far gets us 9.25B KRW in ebit in Q2 alone

You are getting all of this profitability and growth for only ~160B KRW market cap with the current share price at 36,000 KRW

If we take

Q1 ebit 5B KRW

Q2 ebit 9.25B KRW

Assume Q3 and Q4 ebit stays the same as Q2 (18.5B KRW)

= 33B KRW EBIT

5x forward ebit multiple for a company whose Q2 revenue growth was 100% QoQ

Is this cycle peak profitability or durable revenue/earnings growth?

Everything related to memory is cyclical we know this. But is the market pricing the reality of the current cycle.

I don't think so.

CXMT

CXMT recently filed for an IPO in December last year, seeking to raise 29.5 billion yuan (approx. $4.2 billion)

CXMT is expanding its Shanghai fab, aiming for two to three times the capacity of Hefei headquarters. With equipment installation in late 2026 and mass production starting in 2027.

Longer term, the company plans to expand capacity to 300,000 wafers/month by year-end and beyond 400,000 thereafter using IPO proceeds.

YMTC investing in expanding NAND manufacturing

Its Wuhan campus plans include a new facility where an estimated half of production will target DRAM.

YMTC is fast-tracking the Wuhan Phase III NAND fab, bringing its mass production target forward to the second half of 2026, roughly a year ahead of the original 2027 schedule.

The Phase III project broke ground in September 2025 under an operating entity established with registered capital of CNY 20.72 billion (~US$2.98 billion)

Phase III will reach 50,000 wafers/month by 2027 and 100,000 wafers/month at full capacity.

Beyond Phase III, three sources told Reuters the company aims to add two more fabs of equivalent scale.

SK HYNIX planning to double wafer capacity by 2030

Memory Capex is expected to go on for another 3 years minimum.

With Mirae at 5x forward ev/ebit they will earn almost the entire market cap in cash flow over the next handful of years.

8x forward ev/ebit = 260B KRW / 4.5 m = 58K/shr

10x forward ev/ebit = 330B KRW / 4.5m = 70K/shr

12x forward ev/ebit = 360B KRW / 4.5m = 80k/shr

I AM LONG MIRAE. NFA.

1

9

3,393

Jun 5

I love when hedges actually workout. Had a decent amount of $SPY puts as well.

Funded the QQQ hedge with selling $IREN calls and closed a lot of my position right before this drawdown

🙌

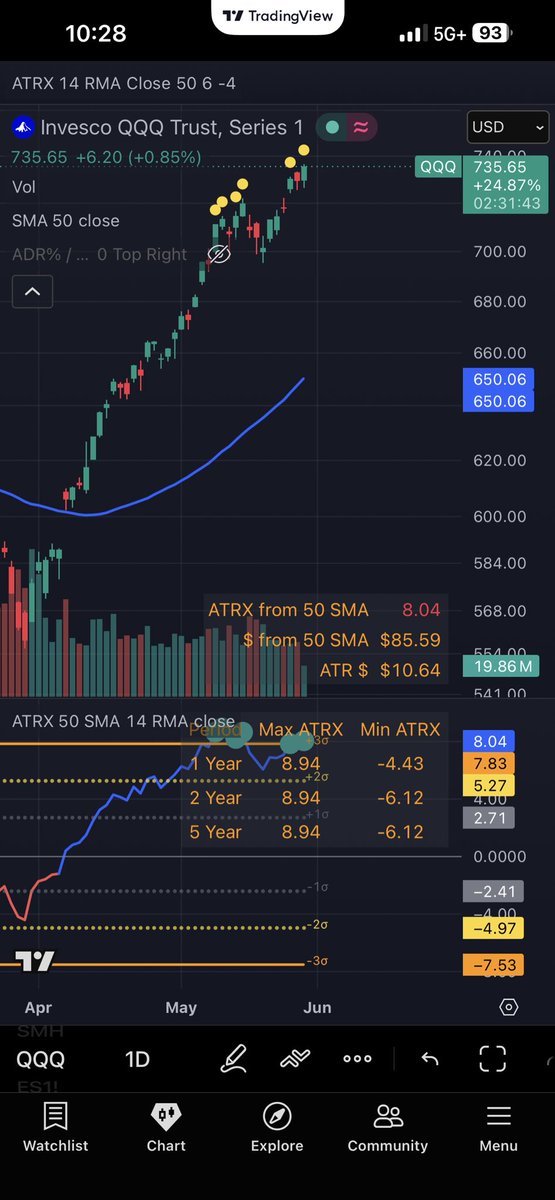

May 28

DSPX - single stock vol near peak levels

COR1M - index level vol near trough levels

QQQ at 3 sigma levels of extension - measured by ATR from 50-D MA

= Perfect time to fund some QQQ hedges by selling calls on elevated single stock vol

3

442

Jun 1

Great source for finding trades. Give him a follow.

I found Mirae Corp $025560.KQ bc of him then it doubled in 2 weeks

My largest position is $2316.TW, WUS Printed Circuit Co Ltd: an AI PCB maker trading at ~11x look-through P/E and only ~23% of its listed $002463.SZ stake NAV.

The stock is ~NT$168. Its listed $002463.SZ stake alone is worth ~NT$733/share gross.

That is a ~77% discount to listed stake NAV before giving any value to the Taiwan PCB business.

This is not a trapped holdco. They’ve already monetized part of the stake.

Why cheap?

Holdco discount. China exposure. PCB cyclicality. Low coverage. Monetization risk. No clean “AI” label.

But the setup is changing.

AI servers need more complex, high-layer PCBs. Capacity is tightening. Q1 net income was up ~141% YoY. $2316.TW hit/closed at limit-up 5 times in May alone.

This hits exactly what I look for:

Hidden NAV. Downside protection. Positive momentum. AI bottleneck exposure. Inflecting fundamentals. A monetization catalyst. Dirt-cheap Valuation.

The market sees a forgotten PCB holdco.

I see a discounted tollbooth in the AI supply chain, backed by a listed stake worth over 4x the current share price.

Just reaching listed stake NAV implies ~336% upside.

That is The Scarcity Trade.

1

1

3

1,002

May 28

DSPX - single stock vol near peak levels

COR1M - index level vol near trough levels

QQQ at 3 sigma levels of extension - measured by ATR from 50-D MA

= Perfect time to fund some QQQ hedges by selling calls on elevated single stock vol

1

2

623

May 27

SK hynix trading at 11x forward P/E now

Just a reminder you can buy it for 5.5x forward P/E through owning SK Square $402340.KS

With management actively targeting to reduce the discount to 30%

2

353

May 20

Are you a memory bag holder?

Are you looking for a hedge against china building out memory production?

Boy do I have the trade for you.

$025560.KQ Mirae Corp

With Mirae corp you make $ off the chinese memory fab buildout

Mirae corp provides back-end equipment in the form of test handlers for memory fabs.

Their biggest customers are CXMT & YMTC

Even Sk Hynix

But the best thing yet is its on sale for 6x annualized ebit (q1 26 ebit annualized)

Get it while the deal last theres only ~2.5m shares in free float

May 20

“Samsung adviser warns the AI-driven memory super-cycle may lose momentum by 2028 as Chinese chipmakers aggressively expand DRAM and NAND production. “

scmp.com/tech/tech-trends/ar…

3

15

3,381

May 20

“Samsung adviser warns the AI-driven memory super-cycle may lose momentum by 2028 as Chinese chipmakers aggressively expand DRAM and NAND production. “

scmp.com/tech/tech-trends/ar…

3,187

May 19

Just some Macro Perspective

2026 AI Capex from Hyperscalers is $725B

= to ~38% of the US fiscal deficit in 2026 currently $1.9tr

Together this equals to ~$2.6tr of spend into the economy = ~8% of GDP

We have ~8% of GDP being pushed into the economy in 2026, pro-cyclically

I get that Inflation is a problem and bonds are repricing and the FED may hike earlier than the forward curve is pricing right now.

But... I think it's gonna take a lot more than 25bps to stop this train.

2

271

May 14

They also just announced a 8b won purchase order from Unimos electronics on the same day.

100b won market cap btw

One purchase order = revenues of 8% of market cap

May 14

$025560.KS Mirae just reported a monster Q1:

Revenue: ₩20.7B, 336% YoY

Op profit: ₩4.9B, ~15x YoY

Net income: ₩5.9B

At ~₩111B mkt cap, that’s ~7x LTM earnings, ~5-6x blended 2026, and ~4.7x if Q1 annualizes.

Korean semi equipment comps trade far richer.

2

365

May 13

Mirae corp 025650.KS limit up 30% today

No new POs or fundamental news officially filed by them.

Just a news article "CEO Lee Changjae has received the Deputy Prime Minister and Minister of Science and ICT Commendation as part of the 2026 Science Day Science and Technology Promotion Merit Awards."

Maybe this article put the stock on the radar of South Korean retail traders that can cause some heavy movements with a ~2.3m float

asiae.co.kr/en/article/stock…

2

334

May 12

$Q looks great here. One of those companies in the AI era that wins no matter what. Being a leader in supplying all the chemicals like CMP, photoresists, copper RDL; Etc that continue to be used in higher volumes as vertical stacking of high-end chips continues in memory and logic.

Combine this with management putting out conservative guidance and recent capacity expansions in Delaware and Taiwan there's a long runway here for consistent beats on revenue growth and margin growth.

TSMC Intel and memory makers expand Fab utilization capacity vertical stacking/etchijng steps -> Strong Revenue growth for Qnity

2

7

1,615

May 8

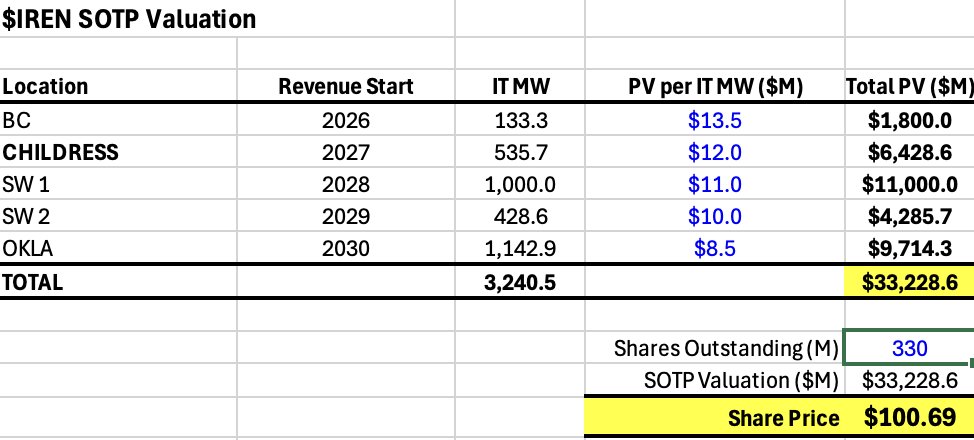

Some bits from $IREN Q3 that may be overlooked

$3.4bn AI Cloud contract with NVIDIA 5-year contract for air-cooled Blackwell GPUs Deploying within 60MW of existing data centers at Childress.

$3.4b / 5 years = $680m arr

$680m arr / 60mw = $11.33m per MW ARR

2027 Expansion to 1,200 MW at $11.33m/MW = potential for ~$13.6B ARR 2027

5 GW = ~$55B ARR

"When you look at the GPU financing, which is the lion's share of that CapEx, the Microsoft contract is a great template. We financed 95% of that CapEx at an average interest rate of about 3% through prepayments and GPU financing."

3% is an insanely good wacc

"you don't need a sales team in this market, particularly when you've got NVIDIA. They see the whole ecosystem, the introductions, the referrals, putting us in touch with anyone that needs capacity."

qualitative benefits of the Nvidia partnership

"It certainly plays a role in a number of those conversations and, you know, we are still seeing prepayments being on the table in a large number of instances. That obviously factors in as part of the overall equation. It's not, you know, the single factor that you're looking at. Everything has to go together with a combination of term length, prepayment, credit worthiness, price. Prepayments are certainly very much on the table in the current environment."

Prepayments still being on the table gives them potential to finance further Capex at that insanely good 3% level seen in the MSFT deal

"Revenues from Microsoft contract and additional 50k GPUs procured during the quarter expected to begin ramping in Q3 CY26 (Q1 FY27)"

For anyone wondering why revenues numbers don't look good now they will start showing up in Q1 27 and beyond

1

328

May 8

Just entered a position in Mirae Corp 025560.KS 🧵

TLDR; Strong theme tight float cheap valuation strong korean market

They make “test handlers” robotic machines that take the packaged chips (mostly memory), put them into the tester and then sort them after.

Memory fab expansions have lead to increased demand for their products.

$35m in revenues FY 25

~87% revenue growth from $18.6m in FY 24

FY25 ebit of $6.3m ~18% ebit margin.

Market cap $55m.

~1.5x sales/9x ebit.

I have literally looked 50 AI related companies in Korea since IBKR opened access and I have not seen a company with valuation metrics this cheap.

Float is also tight with ~4.5m s/o and estimated free float at ~2.3m shares (53% of shares).

1

1

11

1,039

May 8

Durability of Revenue Growth

TLDR: Test handler industry is fragmented and Mirae is not a market leader but they have carved out a niche growth opportunity in Chinese memory fabs.

Likely due to export controls blocking other test handlers (Advantest/Teradyne) from selling to china and mirae being cheaper than competitors.

I personally believe the scale of China’s memory expansion is a rising tide lifts all boats situation and I expect revenue growth to continue to be strong which the current valuation does not reflect.

CXMT alone accounts for roughly KRW 19.9 billion of disclosed direct contracts in calendar 2025, plus an additional KRW 22 billion via Yiling Trading and KRW 10.2 billion via Unimos Microelectronics, both of which are Chinese trading-house intermediaries that the Korean financial press has linked to Chinese memory and OSAT capacity ramps.

We also see purchase orders from SK Hynix as well which establishes a relationship and path to potential further orders from SK Hynix.

1

1

338

May 8

Governance Risk

Nexturn N Roll Korea: The direct parent of Mirae, owns 40.4%. They make precision CNC machine tools and construction equipment parts. Created in October 2025 by merging Nexturn Bio Sciences (which originally bought Mirae in 2023) with Roll Korea (the heavy machinery affiliate). It's listed itself.

Roa & Co Holdings: Owns the other 7.4%. This is a related-party financing entity within the same group — same ultimate controller, separate legal vehicle.

Both ultimately roll up to Roa Holdings Company, the family holdco wholly owned by chairman Onn Sung-jun's wife.

Now this is where the key risk for the investment here is. Onn Sung-Jun has a lot of influence over the board with 47% ownership and has a shady legal and corporate governance background.

I personally am sizing this small just in case of a governance tail risk but I am willing to accept this governance risk for the upside potential in this stock.

2

269

haYN Capital retweeted

May 7

$NVDA and $IREN announced a strategic partnership to deploy up to 5 GW of AI infrastructure across IREN’s global data center pipeline.

Sweetwater in Texas is planned as the flagship NVIDIA DSX deployment.

NVIDIA also gets the right to invest up to $2.1B in IREN

26

114

695

255,669