Investing in the bottlenecks: power, data centers, land, oil, semis, and DRAM. The physical constraints behind the AI age. FAANG AI Engineer. $025560.KS

Joined October 2023

- Tweets 4,831

- Following 2,176

- Followers 1,903

- Likes 13,799

272 Photos and videos

Pinned Tweet

Jun 11

025560.KS has recently become unfrozen for foreign investment. Just made it my largest position by far. Still trades at like 1/4th the valuation of its nearest comp TechWing. Mirae is now 1/3rd of my IBKR allocation, 1/6th of my liquid allocation and 1/10th of my total NW.

Jun 10

China Memory Capex go brrr

Another 15B won order on June 1 for $025560.KS Mirae Corp Test handlers

Q2 Started March 31st

Since then they have announced 37B KRW in contracts so far in Q2

06/01 15.4B KRW (Yiling)

5/27/26 3.6B KRW (direct order from YMTC)

5/20/26 2.6B KRW (SK hynix)

5/20/26 4B KRW (SK hynix)

5/13/26 8B KRW (Unimos)

4/29/26 3.8B KRW (Yiling)

*Unimos is assembly and test arm for YMTC

*Yiling inferred to be a trading intermediary for YMTC and CXMT

To put this into context

- Full Year 2025 revenue was 50B KRW they have almost met that in one quarter

Q126

- revenues were 21B KRW

- EBIT was 4.9B KRW ~24% ebit margins

They are about to hit 100% QoQ revenue growth

Applying a 25% ebit margin to the 37B KRW in orders so far gets us 9.25B KRW in ebit in Q2 alone

You are getting all of this profitability and growth for only ~160B KRW market cap with the current share price at 36,000 KRW

If we take

Q1 ebit 5B KRW

Q2 ebit 9.25B KRW

Assume Q3 and Q4 ebit stays the same as Q2 (18.5B KRW)

= 33B KRW EBIT

5x forward ebit multiple for a company whose Q2 revenue growth was 100% QoQ

Is this cycle peak profitability or durable revenue/earnings growth?

Everything related to memory is cyclical we know this. But is the market pricing the reality of the current cycle.

I don't think so.

CXMT

CXMT recently filed for an IPO in December last year, seeking to raise 29.5 billion yuan (approx. $4.2 billion)

CXMT is expanding its Shanghai fab, aiming for two to three times the capacity of Hefei headquarters. With equipment installation in late 2026 and mass production starting in 2027.

Longer term, the company plans to expand capacity to 300,000 wafers/month by year-end and beyond 400,000 thereafter using IPO proceeds.

YMTC investing in expanding NAND manufacturing

Its Wuhan campus plans include a new facility where an estimated half of production will target DRAM.

YMTC is fast-tracking the Wuhan Phase III NAND fab, bringing its mass production target forward to the second half of 2026, roughly a year ahead of the original 2027 schedule.

The Phase III project broke ground in September 2025 under an operating entity established with registered capital of CNY 20.72 billion (~US$2.98 billion)

Phase III will reach 50,000 wafers/month by 2027 and 100,000 wafers/month at full capacity.

Beyond Phase III, three sources told Reuters the company aims to add two more fabs of equivalent scale.

SK HYNIX planning to double wafer capacity by 2030

Memory Capex is expected to go on for another 3 years minimum.

With Mirae at 5x forward ev/ebit they will earn almost the entire market cap in cash flow over the next handful of years.

8x forward ev/ebit = 260B KRW / 4.5 m = 58K/shr

10x forward ev/ebit = 330B KRW / 4.5m = 70K/shr

12x forward ev/ebit = 360B KRW / 4.5m = 80k/shr

I AM LONG MIRAE. NFA.

5

2

16

4,123

Well that confirms it: Mythos is Agent-1.

Jun 13

The US government, citing national security authorities, has issued an export control directive to suspend all access to Fable 5 and Mythos 5 by any foreign national, whether inside or outside the United States, including foreign national Anthropic employees.

The net effect of this order is that we must abruptly disable Fable 5 and Mythos 5 for all our customers to ensure compliance.

Access to all other Claude models is not affected.

We apologize for this disruption to our customers. We believe this is a misunderstanding and are working to restore access as soon as possible.

Read our full statement: anthropic.com/news/fable-myt…

14

29

1,556

169,470

Jun 12

Ended up 20% today and still under 10x forward PE for an HBM/DRAM testing company.

Jun 11

025560.KS has recently become unfrozen for foreign investment. Just made it my largest position by far. Still trades at like 1/4th the valuation of its nearest comp TechWing. Mirae is now 1/3rd of my IBKR allocation, 1/6th of my liquid allocation and 1/10th of my total NW.

2

10

860

The Scarcity Trade retweeted

Jun 12

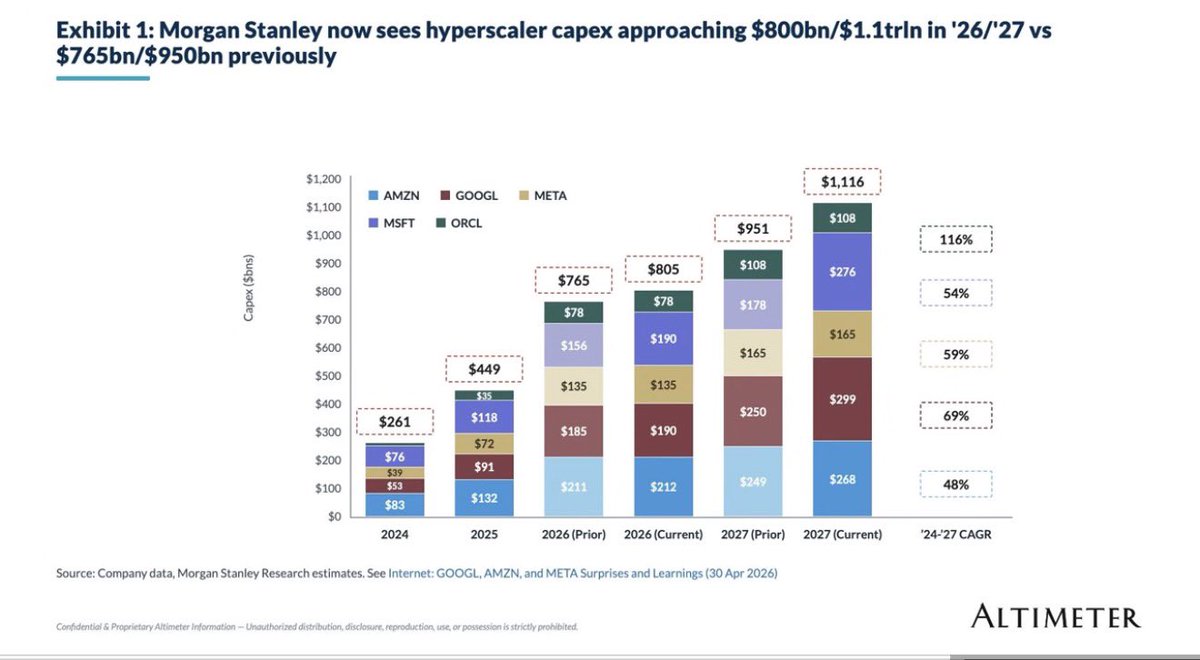

Data from Altimeter:

Morgan Stanley now projecting $GOOG to spend $299B on CapEx next year up 57% from $190B this year

The biggest revision to previous estimates by a country mile.. $MSFT. CapEx est. revised from $178B to $276B in 2027 🤯

Hyperscaler CapEx now est. >$1.1T

28

94

574

80,713

still extremely cheap

stock split in few weeks btw

Jun 12

안녕하세요 Korea!

The only that rhymes with Mirae is 100K

Kind regards,

- The Foreigner 🇰🇷 x 🇬🇧

2

8

916

The Scarcity Trade retweeted

Jun 12

I will share my research on this.

“the heavy dilution phase (2023 convertibles, 2024 rights offerings at ₩767) appears finished”

They just got 17% of their entire market cap in the last 2 weeks from prepayments from Hynix,CXMT, YMTC.

They don’t need to dilute to survive anymore. The only possible dilution is bullish in nature.

1

8

895

The Scarcity Trade retweeted

Jun 12

안녕하세요 Korea!

The only that rhymes with Mirae is 100K

Kind regards,

- The Foreigner 🇰🇷 x 🇬🇧

May 21

I just found the CRAZIEST Korean proxy to CXMT YMTC (THE CHINESE MICRON/SANDISK)

$025560.KS - Mirae Corporation

> 80M Market cap

> 6x annualized ebit (q1 26 ebit annualized)

> Revenue is up 336% YoY

> Op profit: 15x YoY

> biggest customers: CXMT / YMTC SK HYNIX chinese semis

"Samsung adviser warns the AI-driven memory super-cycle may lose momentum by 2028 as Chinese chipmakers aggressively expand DRAM and NAND production"

Chinese memory ram nand capex will flow into this small cap

Mirae: 4.7x annualized Q1 earnings.

Closest comps trade at rich forward multiples:

- Techwing 21x P/E / 15x EV/EBITDA

- DI 21x / 8x

- UniTest 13x / 9x

- Exicon 26x P/E

- YC 49x P/E

Sourced: @jimcx0 @DheerajNam @killapabkai

11

6

81

114,672

Jun 12

Up 24% today! (and just getting started) $025560.KS

Jun 11

025560.KS has recently become unfrozen for foreign investment. Just made it my largest position by far. Still trades at like 1/4th the valuation of its nearest comp TechWing. Mirae is now 1/3rd of my IBKR allocation, 1/6th of my liquid allocation and 1/10th of my total NW.

2

4

590

The Scarcity Trade retweeted

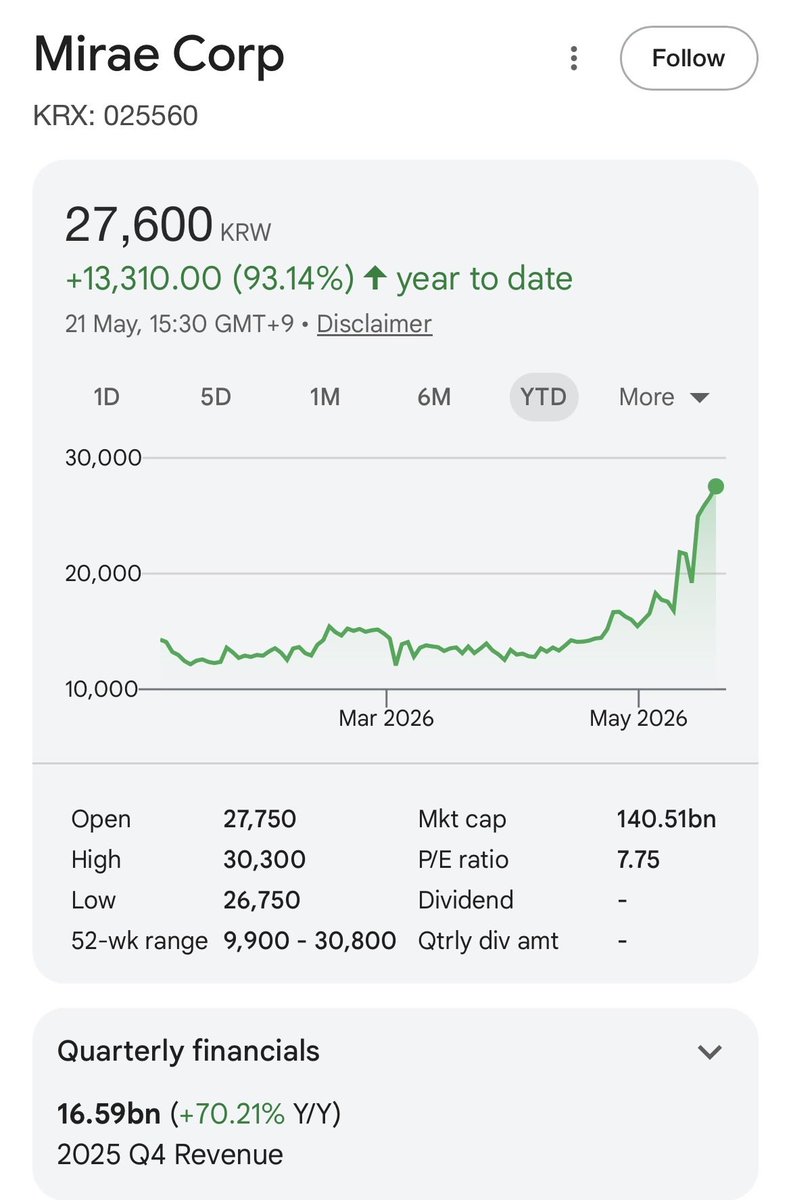

May 14

Mirae Corp $025560.KS is wild.

Annualize the last three quarters and it looks like the stock is trading at ~5x earnings, despite being a semiconductor back-end equipment supplier whose core products include ATE test handlers used in final inspection for NAND and DRAM memory chips.

It also has direct SK Hynix validation, including a recently announced ~₩4.4B semiconductor inspection-equipment order package.

Comps are trading ~50-200x earnings.

Already a huge position for me.

2

1

25

1,911

Jun 11

I can't believe $IONQ is a 20 BLN dollar company. This is why I never short only psychological shorts.

4

471

The Scarcity Trade retweeted

Boy do I love some memory polygamy ! Look at mirae @ScarcityTrade has a great article on it

1

1

3

294

Jun 11

Geez a tripling is insane

Jun 11

Tripling capacity will surely not keep

up with AI-driven momory demand (not even close) but should do wonders for SKHynix revenues/profits.

4

459

Jun 11

Small Cap korean stocks bought with fundamentals in mind.

every good outcome I’ve seen has been from finding a secret and doubling, tripling down on it in a way that compounds over time. not necessary that it even remains a secret because nobody ever believes you anyways; if it was something easy to accept it wouldn’t be available

3

687

Jun 11

025560.KS has recently become unfrozen for foreign investment. Just made it my largest position by far. Still trades at like 1/4th the valuation of its nearest comp TechWing. Mirae is now 1/3rd of my IBKR allocation, 1/6th of my liquid allocation and 1/10th of my total NW.

Jun 10

China Memory Capex go brrr

Another 15B won order on June 1 for $025560.KS Mirae Corp Test handlers

Q2 Started March 31st

Since then they have announced 37B KRW in contracts so far in Q2

06/01 15.4B KRW (Yiling)

5/27/26 3.6B KRW (direct order from YMTC)

5/20/26 2.6B KRW (SK hynix)

5/20/26 4B KRW (SK hynix)

5/13/26 8B KRW (Unimos)

4/29/26 3.8B KRW (Yiling)

*Unimos is assembly and test arm for YMTC

*Yiling inferred to be a trading intermediary for YMTC and CXMT

To put this into context

- Full Year 2025 revenue was 50B KRW they have almost met that in one quarter

Q126

- revenues were 21B KRW

- EBIT was 4.9B KRW ~24% ebit margins

They are about to hit 100% QoQ revenue growth

Applying a 25% ebit margin to the 37B KRW in orders so far gets us 9.25B KRW in ebit in Q2 alone

You are getting all of this profitability and growth for only ~160B KRW market cap with the current share price at 36,000 KRW

If we take

Q1 ebit 5B KRW

Q2 ebit 9.25B KRW

Assume Q3 and Q4 ebit stays the same as Q2 (18.5B KRW)

= 33B KRW EBIT

5x forward ebit multiple for a company whose Q2 revenue growth was 100% QoQ

Is this cycle peak profitability or durable revenue/earnings growth?

Everything related to memory is cyclical we know this. But is the market pricing the reality of the current cycle.

I don't think so.

CXMT

CXMT recently filed for an IPO in December last year, seeking to raise 29.5 billion yuan (approx. $4.2 billion)

CXMT is expanding its Shanghai fab, aiming for two to three times the capacity of Hefei headquarters. With equipment installation in late 2026 and mass production starting in 2027.

Longer term, the company plans to expand capacity to 300,000 wafers/month by year-end and beyond 400,000 thereafter using IPO proceeds.

YMTC investing in expanding NAND manufacturing

Its Wuhan campus plans include a new facility where an estimated half of production will target DRAM.

YMTC is fast-tracking the Wuhan Phase III NAND fab, bringing its mass production target forward to the second half of 2026, roughly a year ahead of the original 2027 schedule.

The Phase III project broke ground in September 2025 under an operating entity established with registered capital of CNY 20.72 billion (~US$2.98 billion)

Phase III will reach 50,000 wafers/month by 2027 and 100,000 wafers/month at full capacity.

Beyond Phase III, three sources told Reuters the company aims to add two more fabs of equivalent scale.

SK HYNIX planning to double wafer capacity by 2030

Memory Capex is expected to go on for another 3 years minimum.

With Mirae at 5x forward ev/ebit they will earn almost the entire market cap in cash flow over the next handful of years.

8x forward ev/ebit = 260B KRW / 4.5 m = 58K/shr

10x forward ev/ebit = 330B KRW / 4.5m = 70K/shr

12x forward ev/ebit = 360B KRW / 4.5m = 80k/shr

I AM LONG MIRAE. NFA.

5

2

16

4,123

Jun 11

If Mirae rerates to semi equip/test-handler comps, upside is huge. Using ₩33B fwd EBIT ₩26B fwd NI, just Techwing parity gets Mirae to ₩170K-₩177K/sh, or 4.7x-4.9x from ₩36K. Not Hanmi HBM or Cohu insanity. Just closest Korean mem-handler comp on Mirae’s run-rate EPS.

At Wonik/Techwing/Advantest/ISC fwd EBIT earnings mults, Mirae can earn ₩185K-₩246K/sh, or 5x-7x. Hanmi/Cohu squeeze-case mults imply ₩450K-₩500K , but not base case. Point is simple: Mirae doesn’t need insane mult to be stupid cheap. If mkt stops treating it like tiny cyclical Korea equipco and starts treating like memory capex winner which based on order flow it is, stock can still rerate multiple times.

1

6

594

Jun 11

Mirae @ 5.0x fwd EBIT and 6.2x fwd EPS. On fwd EV/EBIT, Techwing at 24.2x Advantest at 29.2x, Wonik IPS at 27.7x, ISC at 33.0x, Teradyne at 39.2x, Hanmi at 64.5x and Cohu at 68.

On fwd P/E, same story. Mirae @ ~6.2x, Techwing at 29.5x, Wonik IPS at 32.1x, Advantest at 39.5x, ISC at 42.5x , Teradyne at 49.8x, and Hanmi at 79.6x. Can you spot the dislocation here? I certainly can.

6

379

The Scarcity Trade retweeted

Jun 10

BREAKING NEWS: Mirae $025560.KS investment warning has been LIFTED and SK Hynix are reviewing suppliers request for 3-4% price hikes.

> KRX confirmed the designation comes off as of June 11. The stock cooled enough to satisfy all three release conditions. Margin buying restrictions ease.

> New positions will be able to allocate on IBKR again.

> It drops to a 1 day investment caution on June 11 then off the alert system.

> Re-designation only triggers on a 40% move over 2 days, so theres room to run before it re-arms.

> The surveillance reset is done. Now we wait for Q2.

> 330% YoY rev growth 3-4% price hike = 9-12% more growth YoY.

May 21

I just found the CRAZIEST Korean proxy to CXMT YMTC (THE CHINESE MICRON/SANDISK)

$025560.KS - Mirae Corporation

> 80M Market cap

> 6x annualized ebit (q1 26 ebit annualized)

> Revenue is up 336% YoY

> Op profit: 15x YoY

> biggest customers: CXMT / YMTC SK HYNIX chinese semis

"Samsung adviser warns the AI-driven memory super-cycle may lose momentum by 2028 as Chinese chipmakers aggressively expand DRAM and NAND production"

Chinese memory ram nand capex will flow into this small cap

Mirae: 4.7x annualized Q1 earnings.

Closest comps trade at rich forward multiples:

- Techwing 21x P/E / 15x EV/EBITDA

- DI 21x / 8x

- UniTest 13x / 9x

- Exicon 26x P/E

- YC 49x P/E

Sourced: @jimcx0 @DheerajNam @killapabkai

5

3

40

13,549