Playing infinite games. $85m raised across startups — sold my fintech to a YC company. Microcap & equities trader.

Joined May 2020

- Tweets 549

- Following 471

- Followers 382

- Likes 1,168

14 Photos and videos

Frontrun Capital retweeted

Jun 11

As micro watcher pointed out, look at what the market happily pays for hyped small-caps.

$ALMU trades around 80x sales.

$AMPX many times higher than this name.

Meanwhile $AMPG sits at ~6x trailing and ~4x forward.

So let me tell you the complete story of what you're actually getting at that price.

📡 THE RADIO. AMPG is the only American company to design and commercialize a 64T64R Massive MIMO O-RAN radio, the only one of its configuration certified by the DoD-backed Open6G OTIC, and the only 64T64R vendor at the latest O-RAN PlugFest.

🇨🇦 TELUS. ALREADY PRINTING. Per Telus's own VP: every Open RAN site runs AmpliTech antennas, 2 of the 5 radios per sector, live, alongside Samsung, on a Tier-1 carrier. Only ~15% of sites are Open RAN today. Starting line, not ceiling.

🤖 NVIDIA. AMPG's radio ran hand-in-hand with NVIDIA's Aerial in the world's first open-source AI-RAN demo, inside the DoD-funded Open6G hub. NVIDIA is now on its customer wall. (A collaboration/demo, not a signed supply deal, but the direction is loud.)

🛰️ AMAZON / KUIPER. Dec 2024: AMPG shipped space-qualified amplifiers to a "Fortune 50 satellite provider," LEO constellation, tens of thousands of units expected. The only Fortune 50 building its own LEO network is Amazon. Now on the customer wall too. (Still a deduction, still a prototype, but the dots keep landing.)

⚛️ QUANTUM. The only US maker of the cryogenic amplifiers superconducting qubits need, Google and IBM named as proof-of-concept recipients. (Optionality, not revenue yet, but real.)

🏛️ THE CUSTOMER WALL. This isn't a no-name. Straight from amplitechgroup.com, the logos AMPG puts under "Customers": NVIDIA, IBM, Amazon, Boeing, Lockheed Martin, Northrop Grumman, L3Harris, CPI, Fujitsu, HTC, Globecomm, C2Tech, Greins, Northeastern, Georgia Tech, University of Edinburgh, Digital Catapult, Paramount, DiscoveryPlus, Disney Channel, and more. (Honest framing: it's the company's own wall, spanning all divisions and years, including its distribution arm, so it shows who they've worked with, not the size of each deal. But you don't put Lockheed, NVIDIA and Amazon up on a whim as a public company.)

💰 THE FUNDAMENTALS. Debt-free. Gross margins 33% → 48%. $118M in LOIs across multiple carriers. A founder who started with $2 in his pocket, still owns ~10% , and hasn't sold a share.

🇺🇸 NOW THE BIG ONE. WHY THIS IS NATIONAL SECURITY?

Look at who builds the world's wireless radios:

Nokia (Finnish).

Ericsson (Swedish).

Huawei and ZTE (Chinese — banned in the US).

Read that again.

The backbone of America's communications, the same networks its military, its first responders, its critical infrastructure run on, is supplied almost entirely by foreign companies.

That's not a convenience problem.

It's a strategic vulnerability.

Whoever builds the radios sits inside the nation's nervous system, which is exactly why the US ripped Huawei out of its networks over espionage and backdoor fears.

You cannot have a trusted network on untrusted, foreign-controlled hardware.

So the US government's answer is Open RAN, an open, multi-vendor architecture that lets American companies supply trusted, individual pieces (a radio here, software there) instead of depending on a single foreign empire.

And the tip of that spear is Open6G: the DoD-funded (OUSD R&E, via an Army Research Laboratory agreement) research hub at Northeastern, built to create a domestic, secure foundation.

That's the whole point.

Washington is funding an entire architecture to get foreign hardware out of the nation's networks, and at the radio layer, where it matters most, there is exactly one American company at that spec.

Already defense-qualified (Lockheed, Northrop, L3Harris, Boeing).

Already inside the DoD-backed hub.

Already certified.

Already deployed at a Tier-1 carrier.

When the government decides trusted, domestic, open infrastructure is a national priority, and there's only one US company that makes the radio, that company stops being "a micro-cap" and starts being strategic.

So step all the way back and look at the asymmetry:

The market pays 40–80x sales for hyped names with tiny revenue and no story like this.

AMPG, real revenue, real customers, a debt-free balance sheet, NVIDIA and Amazon on its wall, designed into Telus, and sitting at the center of a national-security strategy, trades at single-digit sales.

That's the story.

That's the gap.

And the market is only starting to close it.

Not financial advice. I'm long $AMPG. DYOR. 📡

Jun 11

5

11

78

8,458

Jun 12

We need to think harder before selling.

Spend as much time thinking about an exit as we would with buying.

Don't sell just because something is painful TODAY.

29

Jun 9

$BRUN has real revenues backed by a massive and growing backlog

Boost Run Investor update here: boostrun.com/investors/

1

211

Jun 3

Started a challenge account.

Full ported $XFAB

Can we full port our way to 1m from 30k?

2x incoming 🚀

3

340

Frontrun Capital retweeted

Jun 2

$XFAB - 10 REASONS why INVEST

1. High-Growth Megatrends

Focus on Key Markets

No Consumer Risks

Stable Long-Term Growth

2. Strong Customer Loyalty

Unique Manufacturing Processes

Sole-Source Supplier

High Switching Costs

3. Electric Vehicle (EV) Boom

More Chips Needed

Automotive Certified

Critical Component Supplier

4. Next-Gen Power Materials

Silicon Carbide Pioneer

Gallium Nitride Expertise

Green Energy Leader

5. Secure Financial Agreements

Long-Term Contracts

Take-or-Pay Clauses

Pre-Funded Expansion

6. Advanced Medical Technology

Medical Chip Demand

Lab-on-a-Chip Solutions

Life-Saving Electronics

7. Safe Global Footprint

Six Global Factories

No Geopolitical Trap

Local Supply Chains

8. Long Product Lifecycles

Decades of Revenue

Low Upgrade Costs

Reliable Cash Flows

9. Leadership in MEMS Sensors

Micro-System Pioneers

Heterogeneous Integration

Smart Device Futures

10. Direct Research Connections

Lab-in-Fab Concept

Fast Market Entry

Cost-Efficient Innovation

Not financial advice.

5

13

84

13,866

Jun 3

Time in the market is teaching us an important lesson.

Don't let price action change your thesis.

58

Jun 2

The stock market is such a gift.

There are multiple companies that we can full port and go to sleep.

Wake up richer on the other side.

103

Jun 2

$HPE just CRUSHED IT.

Biggest EPS beat since 2018. Stock surging 30% after hours.

Q2 FY2026 results:

- Revenue: $10.68B vs $9.79B est

- Adj EPS: $0.79 vs $0.53 est

- Server Revenue: $5.45B vs $4.66B est

- Free Cash Flow: $915M (record Q2)

- AI Systems Orders: $1.8B (record backlog)

1

244

May 29

Listened to the $SIVE earnings call today.

I have a 7% position in $SIVE

When the CEO talks about the 'opportunity pipeline', I can read between the lines.

I was also a CEO/founder.

It's usually a sum of the 'potential value' of 'customer engagements' from the CRM app the company uses.

Note that these aren't LOIs or contracts, and sales people usually exaggerate these numbers to 'look good' infront of management.

Venture building has taught me a lot, and knowing how organizations are built tells you what might be happening under the hood.

$SIVE is still very early.

If you have to be bullish, then be so with knowledge and a dose of skepticism.

2

736

May 29

The more I pick stocks/companies, the more I learn that I am price sensitive.

(1) I don't like overpriced companies no matter how rosy the future is

(2) I love a re-rate story. Being able to front-run the price discovery ahead of everyone else = satisfaction

(3) Commercial inflection points backed by patents/IP = treasure hunting

Know thyself.

205

May 28

Probable $DELL $IQE connection?

$IQE makes InP epiwafers

▼

MACOM uses epiwafers to make laser drivers, TIAs, EMLs

▼

Transceiver OEMs $LITE $AAOI use MACOM components to build 800G/1.6T modules

▼

Transceiver modules installed by $TSSI in server racks

▼

$DELL buys those specific transceivers which are made from $IQE InP epiwafers

▼

Dell PowerEdge AI server ships to customer like $CRWV

3

500

May 28

Wild idea I was discussing with @Ren_aramb

The idea is to create a sub-portfolio of 30-50 microcaps and then double down on winners.. could turn 50k into 1m...

Margin is a bad idea on this one but otherwise not too different from how VCs do pre-seed investments 😅

1

2

126

May 28

Fantastic write up on $IQE vs $SOI by @AlmaCap114204

I had already trimmed our position in $SOI as we feel the price reflects the business of tomorrow I don't have clarity on TAM, so unless the conviction develops - I will sit it out. I do like the monopoly but not at this valuation.

I continued to hold $IQE through the ER today. It's a much better company today than it was 3 months ago.

May 28

$SOI (SOITEC) earnings yesterday and $IQE earnings this morning are a window into what we can expect across the photonics industry.

We're still very early to the photonics / CPO shift, it hasn't happened yet. In many cases products are still being tested and integrated into wider system designs, so mass orders could be 6–12 months away. We may not get real visibility until Q3 prints at year-end, if not early 2027.

> $IQE is what we are hoping for: trailing numbers soft (revenue down ~18%, EBITDA down 60%), but the lead story is multiple Tier 1 InP photonics design wins for AI / hyperscale data-centre lasers and detectors, plus a 20% FY26 growth guide.

> The market may punish the "bad earnings" if it's anchored on current revenue, the real bull case is design-win progression and forward order visibility.

I expect more of the same across the board: $SIVE, $POET, $LWLG, $ALMU.

Same read for $LPK in packaging, though equipment makers tend to catch the first wave of orders.

PS: $AAOI is the one case where I'd expect significant revenue beats and guidance uplifts. They supply high-speed pluggable optical transceivers (400G/800G/1.6T modules) for AI data-center interconnect, being deployed in volume today.

PPS. I am adding on this $IQE earnings update but not on the $SOI one.

412

May 28

$IQE FY2025: headline revenue -17.6% hides the real story.

Photonics 15% to £57.1M which is now the majority segment

MACOM just bought 11.5% of the company and locked in long-term supply agreements. A customer doesn't invest £45M in their supplier unless they see accelerating demand ahead.

"Multiple Tier 1 InP design wins for data centre" volume production. FY2026 guided 20% growth.

Bank debt eliminated. Balance sheet clean.

FY2026: exceeding 20% growth guided

The smartphone drag is fading. The AI photonics inflection is here. Every optical transceiver connecting GPUs needs InP wafers. IQE makes them.

6

329

May 28

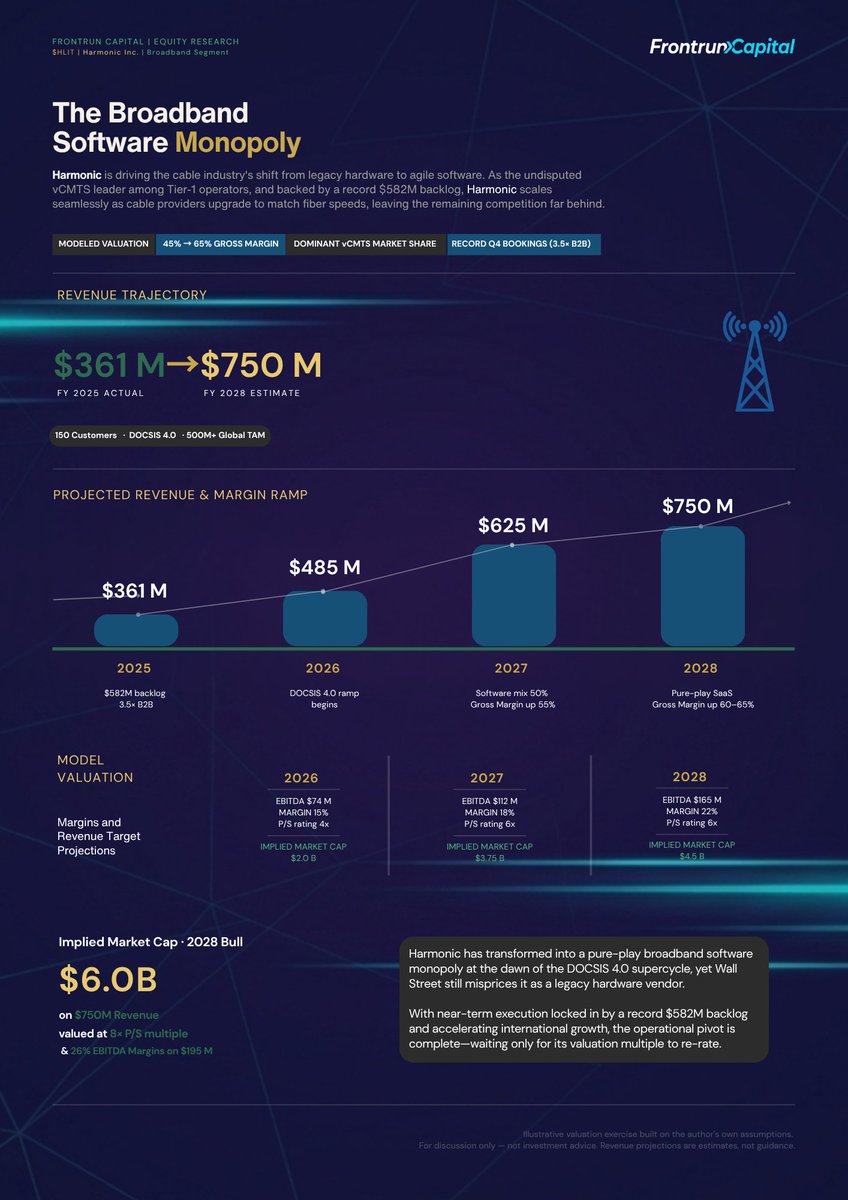

Why HLIT's TAM is the 500M global homes, not 85M US:

Every cable modem whether in Ohio, Germany, Brazil, or Japan needs DOCSIS technology to function. When cable operators upgrade to DOCSIS 4.0, the headend software (Harmonic cOS) must be upgraded regardless of geography. HLIT's 41M modems on cOS today is only 8% of the 500M global installed base. The other 92% is the multi-year runway.

$HLIT

80