Sharing my personal views, not investment advice. Please do your own work.

Joined November 2022

- Tweets 2,333

- Following 119

- Followers 7,432

- Likes 4,406

151 Photos and videos

Pinned Tweet

This year I present a handful of my top ideas for 2026 (in alphabetical order of tickers). Some of these names are fairly uncorrelated with the market (and a few definitely are not). As a reminder please do your own work and be mindful of the low trading liquidity in many of these.

$BWEL JG Boswell at $459/share (LOW RISK / HIGH REWARD)

JG Boswell has been the deep value stock that even the most disciplined investors have lost patience with (including yours truly!). Despite the last year being horrible for both tomatoes and cotton, $BWEL put up ~$40mm of adj. EBITDA. It is extremely rare for both of its core crops to be bad at the same time (i.e., something good should happen with one of them this year) and their pistachio crop will generate increasingly material cash flow for the next 10 years as it matures. Creation value per acre is around ~$3k (or lower) depending on your assumptions which compares to FMV of $15k/acre. There's a lot of room for the stock to appreciate and still trade poorly!

$MLP Maui Land & Pineapple at $17 (LOW RISK / HIGH REWARD)

This name has seen a recent cluster of insider buying by the CEO (Race Randle), Chairman (Scot Sellers) and controling shareholder (Steve Case). The company's undiscounted land value is ridiuclously high relative to its stock price (like 8-15x) but the open question is the time to monetize. In a frothy stock market, this seems like an interesting, low risk place to deploy capital.

$PLAY Dave & Buster's at $16 (MEDIUM RISK / VERY HIGH REWARD)

Dave & Buster's is in the midst of a turnaround, with tangible signs of progress, but an exasperated investor base. Valuation is ~4.5x EBITDA which compares to its long history of 6-10x EBITDA. It's also worth pointing out that within this business is a bowling business called Main Event which is ~half of the company's TEV and worth ~8-10x if sold separately. $PLAY is going through a capital intensive remodel phase (with mixed results). The company recently put in a new CEO and results are turning, but the street is rightly worried about the staying power of the improvement. 2026 could be disappointing on the topline, but my gut is that there is a lot of low hanging fruit that will result in nicely improving results in 2026. There are no near-term liquidity issues and this is a nice multi-year option. I think it's highly asymmetric, wherein downside should be limited given b/s duration low hanging fruit on costs with colossal upside on any real turnaround (every ~1x EV/EBITDA revaluation upward is around 100% on the stock). Don't waste your time on this one if you can't handle the volatility.

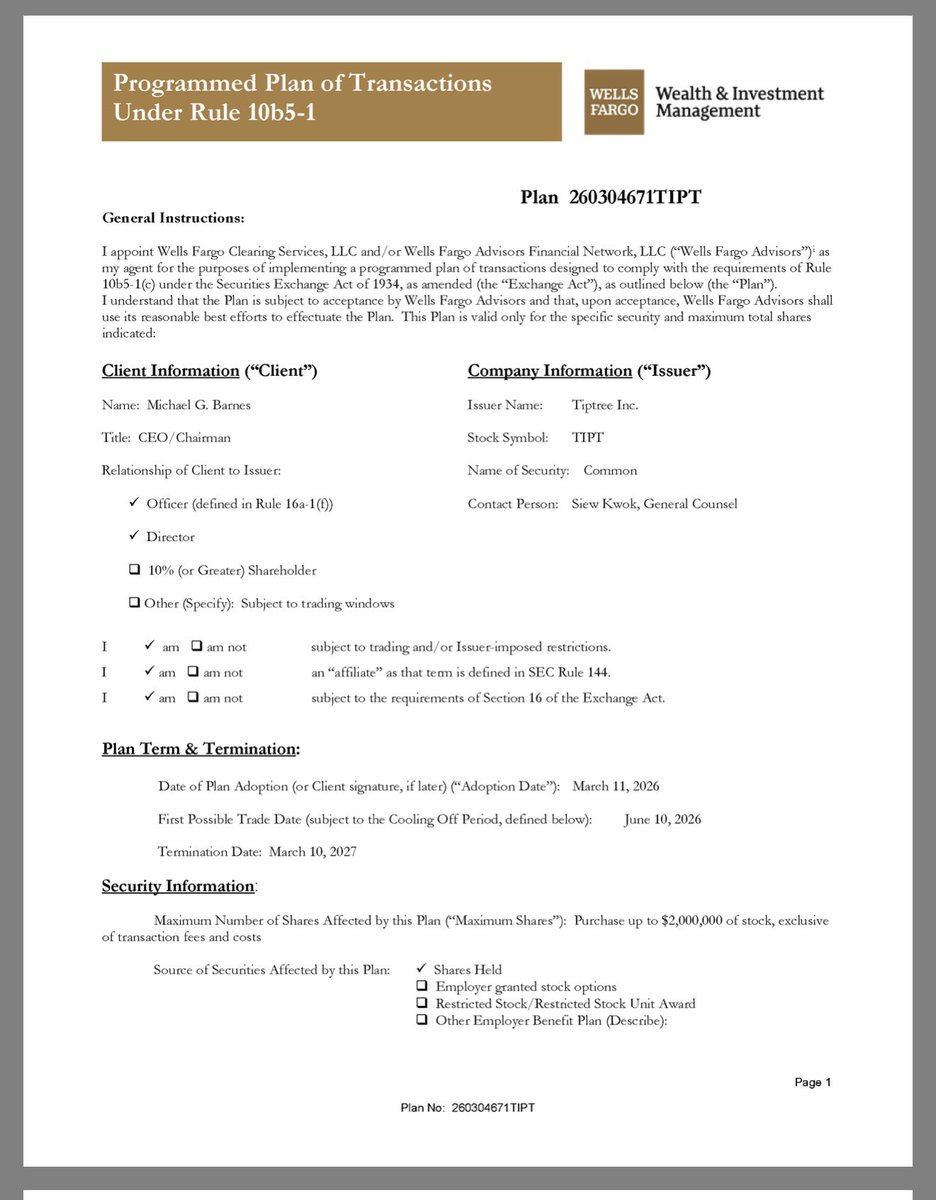

$TIPT Tiptree at $18.27 (SAFE PLACE TO PARK CASH)

This is by far my lowest beta pick. $TIPT is essentially doing the opposite of a de-SPAC. It is morphing from an operating company to a cash shell. It has agreements to sell its assets and will have $24.60/share in net tangible book value upon closing of Fortegra in 1H26. Post closing, the company will return the cash, make a large acquisition or a combination thereof. One of $TIPT's directors recently bought stock at $18.21/share and most importantly insiders own ~35% of the company. Upon completion of the Fortegra divestiture, I expect this to pull toward 85-95% of TBV ($20.91-23.37/share) representing a 14-28% return. Further upside potential when they announce an acquisition. If this were a true SPAC (with a 24 month put) I think this management team would trade at a premium.

$WEBC Webco at $218 (warning: VERY ILLIQUID)

Webco ended the year near its ATH, however, it is incredibly cheap at ~0.5x TBV and ~4x EBITDA. About a year ago, the company did a privately negotiated buyback of ~15% of its stock at $200, which was a premium to the prevailing $185/share trading price. No surprise, but in the last few quarters, the results have turned and the company should generate meaningful FCF in 2026. I believe the take private valuation for this company is ~$350-400/share.

And a few other old favorites that I'll throw in here:

$CBBI CBB Bancorp at $11 (LOW RISK HIGH REWARD)

This name has been discussed on FinX extensively and I'm not going to break new ground here. But I will say that the new board member gives me some hope that something will happen in the name in the short-term.

$FMBL at $8,349 $QUCT at $2,100. (LOW RISK)

Both of these names had an amazing 2025 due to the company taking shareholder friendly actions (for FMBL, raising a $200mm pref, for QUCT signalling asset sales and having improved results). Both of these names continue to very cheap relative to their take private valuations. And, due to conservatively positioned balance sheets they both have little downside.

$FPH at $5.59 (LOW RISK HIGH REWARD)

It feels like hubris to re-recommend $FPH as a top pick for the upcoming year and I do think that at this price it's not as interesting (obviously). However, there are a lot of good catalysts coming with this name, including the announcement of JV partners in both Valencia and SF and the potential favorable resolution of the litigation against $TTEK (in addition to continued high value land sales in Irvine). $10-15/share continues to be where I think this goes to over time.

5

5

122

22,537

Jun 11

Really interesting how $GO had truly massive insider buying and the stock barely reacted, allowing the investor to accumulate a sizable position. This one has worked quite nicely.

x.com/marginofdanger/status/…

Grocery Outlet $GO has had a very large amount of very recent insider buying around the current share price. Interestingly the lead director’s (former Hellman and Friedman partner who has been involved forever) and CEO’s form 4s caused the stock to bounce, and then they kept on buying it higher despite the bounce. $GO is an extreme discount grocer that has faced some growing pains and has experienced sharp multiple contraction. Valuation is very reasonable and my gut is that you may see the trifecta: 1) sales growth, 2) margin expansion and 3) multiple expansion. Balance sheet is in fine shape. Cc: @CapitalFang

10

3,464

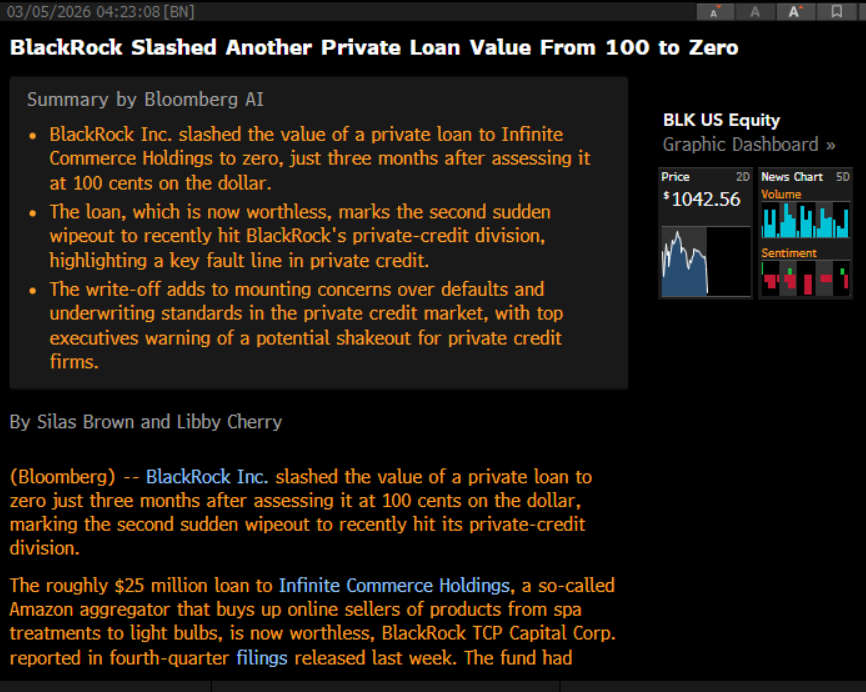

Wild to me that when $MAPS was trading 2x higher, it was a seemingly beloved consensus long on here, and now due to STRATEGIC delisting it's traded off massively, sits at net cash, all while generating $40 mm of EBITDA.

3

19

5,307

Sometimes pattern recognition works $WEBC

x.com/marginofdanger/status/…

14 Feb 2025

$WEBC, a very illiquid OTC name, is worth attention. $181/$195 right now. One month ago when $WEBC was $160-170, the company paid a sizable premium to buy back 17% of the company's stock at $200/share (in a block trade), bringing the Weber family's ownership from 65% to 79%.

One analogous situation I can think of is $MCEM. Several years ago $MCEM was trading in the 60s, and the company did a dutch tender at a premium to acquire shares. We all know what happened after that.

While $MCEM was in retrospect incredibly cheap, $WEBC is by no means expensive. Additionally, I am struggling to find a counterexample of an OTC company buying back stock at a premium, and then not doing very well.

Maybe the Weber family knows something we don't. Given they already control this thing, I don't see a non-economic reason to further consolidate their ownership.

1

8

3,379

May 29

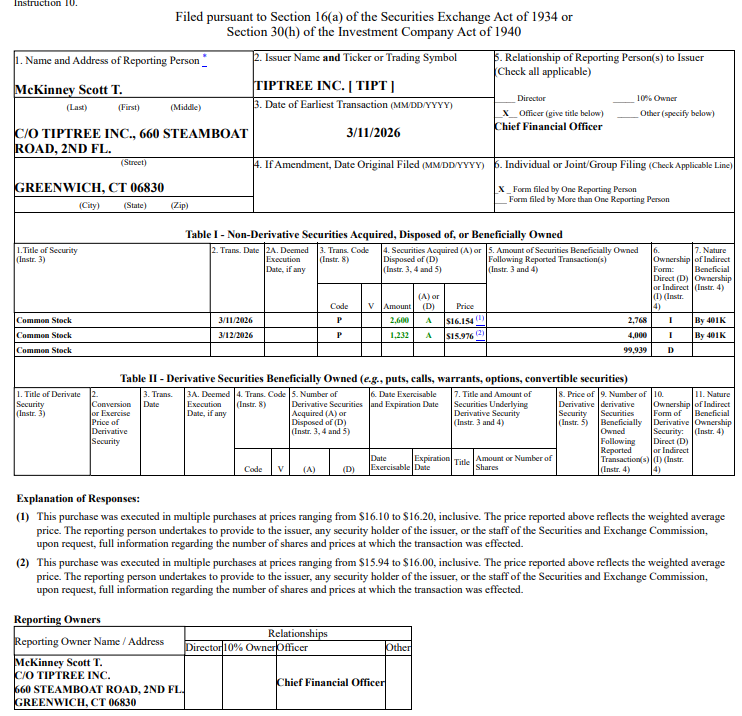

$TIPT director buys ~1k shares at 17.45 on Wednesday and Fortegra deal should close today

x.com/marginofdanger/status/…

May 22

$TIPT filed an 8-K this morning where they said they expected the Fortegra deal to close by Friday 5/29. Pro forma TBV is ~$24/share, stock last 17.17.

7

1,738

May 28

Another great quarter from $WEBC with accelerating top line and gross margin expansion. Company continues to buy back and refresh buyback.

x.com/marginofdanger/status/…

$WEBC reports continued improvement in results, with large yoy increases in revenues, gross margin and earnings. They stepped up buybacks again in the quarter, repurchasing 15k shares (~2% O/S).

1

5

1,605

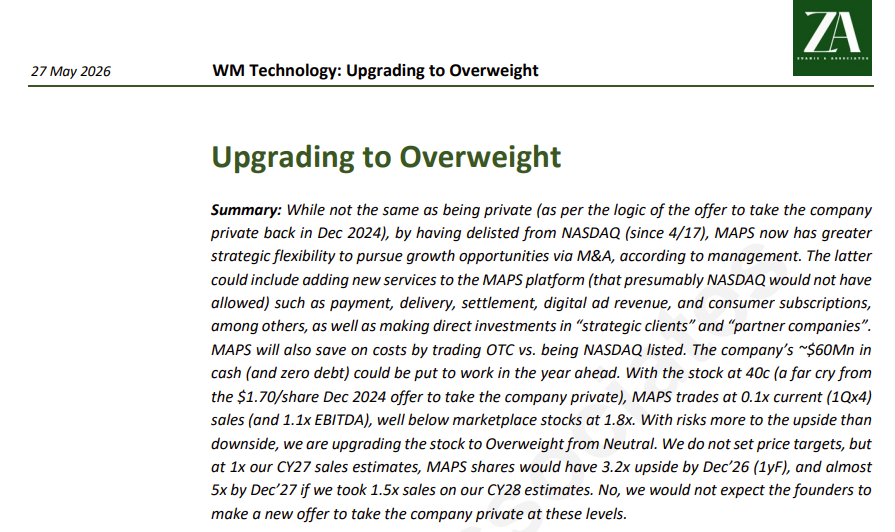

May 27

Don't normally focus on sellside notes but in this instance Pablo Zuanic is on point re: $MAPS

4

24

5,862

May 22

$TIPT filed an 8-K this morning where they said they expected the Fortegra deal to close by Friday 5/29. Pro forma TBV is ~$24/share, stock last 17.17.

1

2

8

3,027

May 19

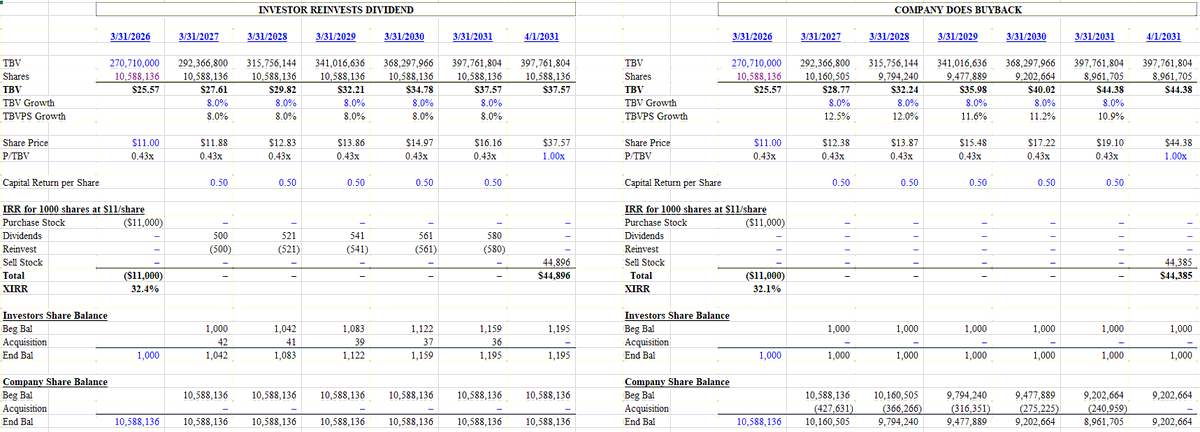

$CBBI followers- the tables below show two scenarios assuming a sale in 5 years at 100% of TBV:

1) Investor reinvests the .50/yr dividend into more shares

2) CBBI suspends dividend and instead does a share repurchase

The analysis shows that the results are roughly the same (BEFORE TAXES). The point here is to show that if you reinvest your dividend you can somewhat replicate the economics of a buyback. One assumption that is likely optimistic in the company buyback scenario is that they'd continue to be able to buy back at 0.4x TBV. If you tinker with that, the buyback is less valuable.

cc: @mwphnh

6

1,615

May 16

Seems like $MLP may be selling its water assets to Maui for $30 million

mauinow.com/2026/05/16/maui-…

1

23

2,926

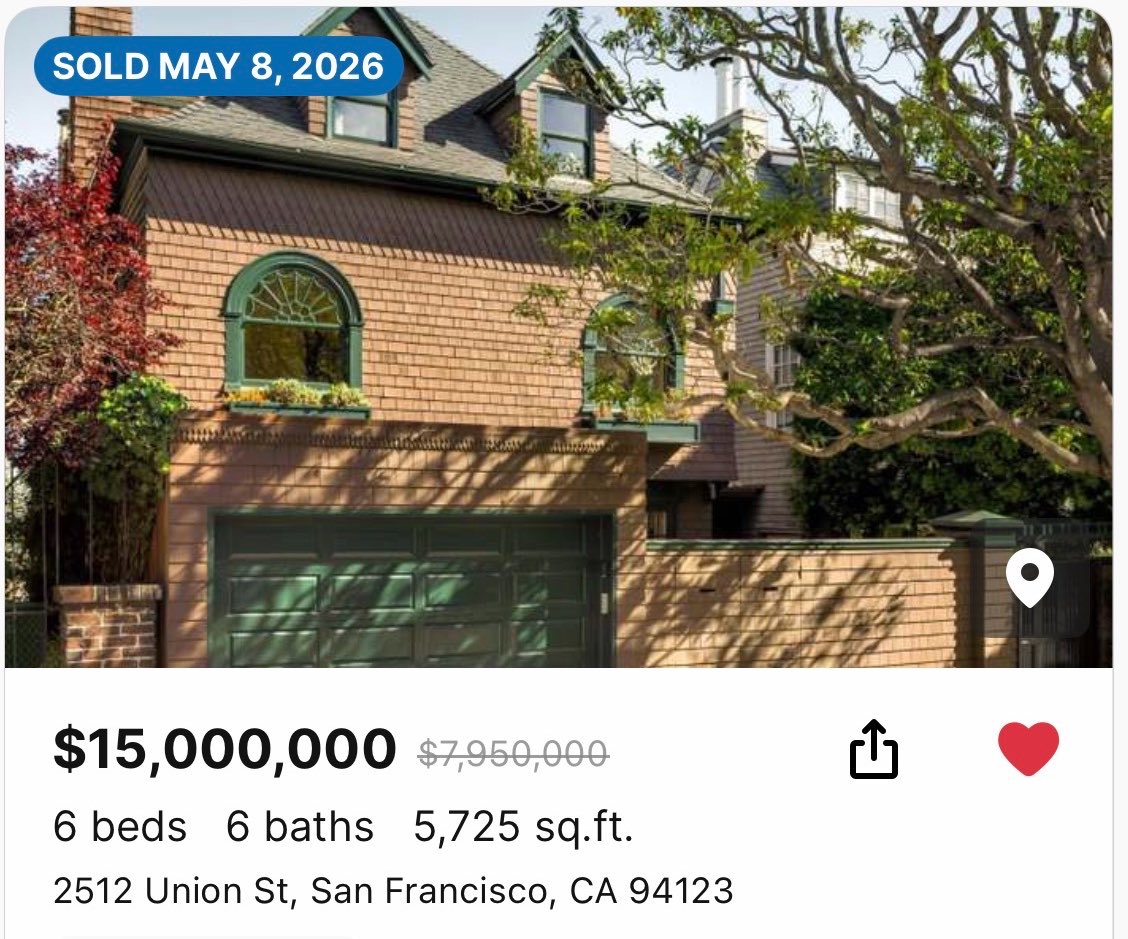

The SF housing market is on fire. Should bode very well for $FPH's Candlestick project, including finding financing partners.

x.com/rohindhar/status/20528…

May 8

San Francisco home sale in the cow hollow neighborhood at $7 MM over asking price

2

14

3,289

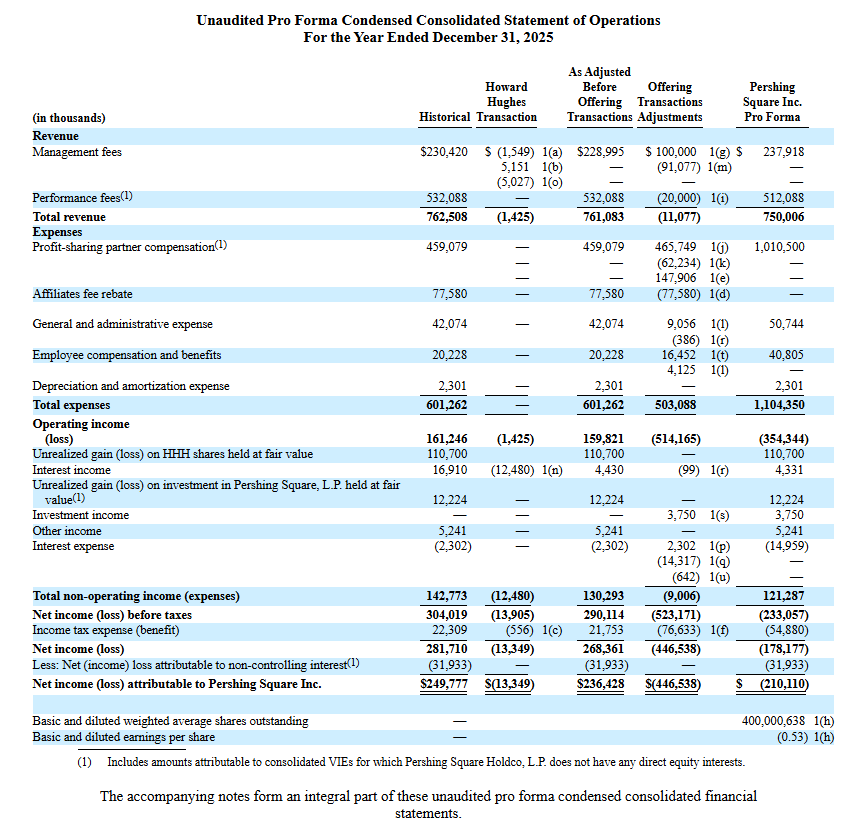

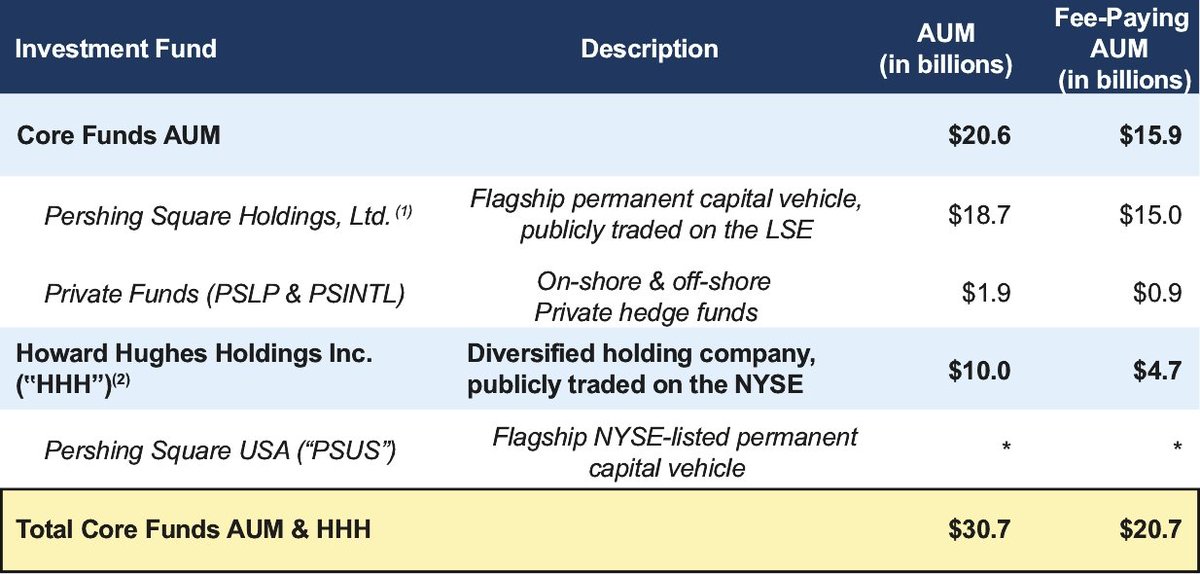

I pasted two screenshots from $PS's 424B4. If you look at fee paying AUM, it's $16 bn excl HHH which has a de minimis mgmt fee/carry. Add in $PSUS and you are at $21 bn of fee paying AUM.

$PS discloses pro forma mgmt fees of $238 mm but that is net of $91 mm of non-cash amort related to the IPO. So I'm going to give them credit for $329 mm of mgmt fees. Assuming a 65% operating margin and a 20% tax rate, that gives me effective fee paying earnings of $171 mm.

$PSH.LN has a 16% incentive fee and $PS is entitled to the performance fees on the first 5% (the team gets beyond that). On $15 bn, this is $15 bn * 5% * 16% = $120 mm or $96 mm after tax.

Add up the mgmt fee and performance fee share, and I get $267 mm of expected earnings or $0.67/share. Implies $PS is trading at around ~50x EPS vs. $KKR at 17x, $ARES at 20x, $BX at 21x. Of course you can layer in some minor $HHH economics and it takes down the multiple a couple of turns. But you could also layer in a few years of sub 5% returns and that takes away the performance fee too.

Certainly a 50x EPS valuation is pretty common for a fast growing higher ROIC biz. But it's by no means cheap. The question is, how will Ackman raise any money from here? $PSH.LN is at a discount to NAV, $PSUS is at a discount to NAV and $HHH is at a discount to NAV. One thing that will allow $PS to grow into its valuation is great results as that will 1) scale up the earnings (as it's based on % of AUM) and 2) facilitate new investors.

Another way to contextualize the valuation is to simply look at fee paying AUM of $21 bn and compare that to the equity value of $13 bn. That is pretty unprecedented in the land of asset managers but reflects in part the permanent capital and the limited float (I think its just the 20mm shares given in the IPO). Could easily see a lot of price pressure once the 380mm non-IPO related investors are free to sell.

10

2

51

16,864

Apr 29

$PSUS opening delayed until Ackman pulls his last few relationship cards. Going to be UGLY!

12

1

12

5,014

Apr 29

Seems like $PSUS and $PS going to trade worse than I expected. Looks like PSUS could open at a 20% discount to NAV and PS to trade below the $10 bn valuation from the latest 3rd party pre-IPO raise.

x.com/marginofdanger/status/…

Apr 28

Ackman's closed end fund $PSUS will begin trading on Wednesday. For every 5 shares of PSUS, IPO investors (only) will get 1 share of $PS (the GP). It sounds like the PSUS offering will be 100mm shares at $50/share or $5 bn. Ackman thought this was going to be a $10 bn offering and he previously was targeting $25 bn or some ridiculous amount. The PSUS IPO investors will end up owning 20mm shares or 5% of PS (based on 400mm pf s/o).

I expect that PSUS, like many closed end funds, will settle at a 5-10% discount to NAV, implying a trading price of $45-47.50/share.

PS will begin trading as well (via a direct listing) and I anticipate a valuation of $5-10bn, implying that the PSUS IPO investors will get a "bonus" of $250-500mm on the $5 bn IPO or 5-10%. Therefore their loss on the PSUS shares should be mostly offset by the free shares in PS. Given this is a direct listing, I expect WILD price movements in PS stock and would stay far away from that one. I used $10 bn as the high end valuation for PS because that is where investors invested back a year or so ago (predicated upon significant growth in AUM), but I tend to believe that was a high watermark and not realistic given that Ackman can't seem to raise $.

In terms of $PSUS, I don't see a compelling reason to own this at 90-95% of NAV. If you put a 15x on the 2% fee, that alone is a 30% drag. Also, Ackman has high volatility and there is no prospect to ever get repaid (and no incentive for Ackman to do so). Like $PSH.LN I would personally only step into $PSUS at a 25-30% discount to NAV and probably not in any real size.

6

1

27

13,204

Apr 28

Ackman's closed end fund $PSUS will begin trading on Wednesday. For every 5 shares of PSUS, IPO investors (only) will get 1 share of $PS (the GP). It sounds like the PSUS offering will be 100mm shares at $50/share or $5 bn. Ackman thought this was going to be a $10 bn offering and he previously was targeting $25 bn or some ridiculous amount. The PSUS IPO investors will end up owning 20mm shares or 5% of PS (based on 400mm pf s/o).

I expect that PSUS, like many closed end funds, will settle at a 5-10% discount to NAV, implying a trading price of $45-47.50/share.

PS will begin trading as well (via a direct listing) and I anticipate a valuation of $5-10bn, implying that the PSUS IPO investors will get a "bonus" of $250-500mm on the $5 bn IPO or 5-10%. Therefore their loss on the PSUS shares should be mostly offset by the free shares in PS. Given this is a direct listing, I expect WILD price movements in PS stock and would stay far away from that one. I used $10 bn as the high end valuation for PS because that is where investors invested back a year or so ago (predicated upon significant growth in AUM), but I tend to believe that was a high watermark and not realistic given that Ackman can't seem to raise $.

In terms of $PSUS, I don't see a compelling reason to own this at 90-95% of NAV. If you put a 15x on the 2% fee, that alone is a 30% drag. Also, Ackman has high volatility and there is no prospect to ever get repaid (and no incentive for Ackman to do so). Like $PSH.LN I would personally only step into $PSUS at a 25-30% discount to NAV and probably not in any real size.

15

7

93

40,539

Apr 24

$CBBI continues to do its thing. TBVPS up to $25.57/share. Run-rate earnings probably around $2 implying a mid 5x P/E. If you don't like the lack of buyback, reinvest the dividend into more shares. Biggest discount of its peers due to OTC listing and lack of buyback.

$OPBK raises dividend and reports slight improvement in EPS vs. last quarter. Seems to be trading in the mid 7s P/E.

$PCB reports and trading maybe in the 8s on P/E.

$HAFC trading around 10x P/E and hitting ATH. A premium vs $OPBK and $PCB for a larger balance sheet.

All very cheap.

3

1

20

2,810

Apr 22

$MAPS is trading at net cash, generates positive EBITDA and its comp set (via $MSOS) is up 20% on rescheduling news. Still suffering from a technical of selling pressure due to delisting. Big margin of safety. cc: @ragingbullcap @ClarkSquareCap

2

3

27

7,472