Opinionated finance commenter mostly posting on the 400 earnings calls I listen to a Q. I don't give advice. It's your $, do your DD.

Joined December 2022

- Tweets 39,413

- Following 361

- Followers 11,079

- Likes 28,518

4,842 Photos and videos

Pinned Tweet

May 29

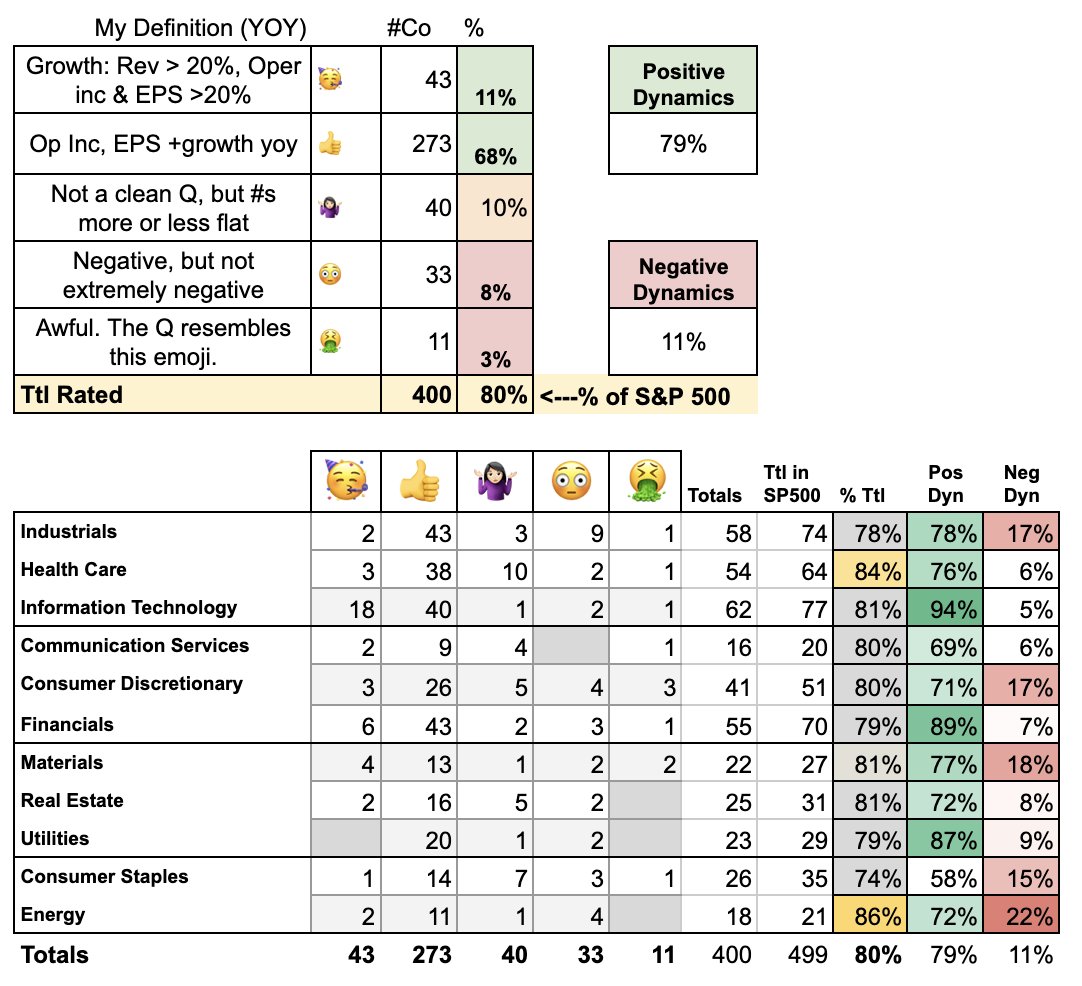

$SPY... comments on my quarterly 400 company review for Q1 or for non-standard FY, the Period Covering Mar 15th through May 30th. Why Mar 15? B/c Q4 starts a little later and takes longer.

I finished the 80% earlier this week and then began rebalancing my own stuff. Then $GS put out a piece and beat me to the punch with a few of my highlights (i'll like below).

The first has to do with how strong this earnings report was. I do not use street estimates, particularly in this very weird period of time where uncertainty is distorting things, AND ALSO, the street is not really doing what it historically did to estimate thoughtfully (*sorry, not sorry, do better).

1) The AI build is very real. This is discussed in the $GS piece but what is remarkable is that a few companies hinted that it is no longer the hyperscalers. There are very real use cases for many industries that result in immediate monitizable outcomes.

2) Healthcare Labs (Example of item 1). $LH and $DGX for example, finally caught a break with single-digit revenue growth and low teens net income growth. This after spending most of the decade in a nasty spot due to both COVID and medicare medicaid "stuff." What's intriguing about what they had to say about AI is the types of tests that are now possible that weren't before. The drive, therefore, is to then move ALL collections into a digital format, such as X-rays. What is possibly by doing this in the way of AI is tremendous, and it will create real tangible benefits to Drs, diagnoses, and - ultimately the inherent liability hospital networks carry. That same sort of thought process (very tangible, immediately cost-improving or revenue-generating) in decision-making is driving HC equipment as well.

3) The speed of monetization is faster than folks understand. Item 2 illustrates a point that is lost in the naysayers of AI right now. Namely, that the speed between new product and monetization has meaningfully changed in many industries. This is faster than what happened when the world moved to even more agile forms of internal innovation. And this implies that the second wave of AI spend (one that is NOT driven by the hyperscalers alone) has already begun.

4) Energy Beverages. I have no idea what is driving this passion toward energy beverages, and no one has an explanation. If I had to guess, it contrasts with what I'm seeing in Alcohol. Nonetheless, $MNST $KO $PEP all reported that thematically, and I have subsequently taken a position in $CELH, which had a blowout quarter

5) Consumer Discretionary. More than one industry reported that consumers are hanging in there but that it is a tail of 2 worlds. The card companies all said that the hit to gas was not changing overall behaviors meaningfully. And for the most significant weakness in Discretionary Staples was all consolidated toward the most fragile parts of the economy. That said, the consumer is far more picky.

6) Staples. Recently, poor renamed Consumer Defensive was anything but though. Food-related staples were an awkward story. This is not a GLP1 thing as some might argue. Really, it's just that they can't catch a break. In some cases, it was a particular ingredient's rising cost. In others, it was the packaging that did them in. In a third mix, it was folks just not wanting what they were selling. Energy drinks were in demand. And IMO there isn't a great theme here that flips the switch.

7) Industrials. Largely speaking, did great. Because of the earlier part of this decade, most were able to pass through fairly well. In some cases, there is a lag, and you do have some weakness in leveraged end markets. But because energy and construction, particularly for data warehousing, were so strong, the industrials did fine, EVEN without the Residential housing pick-up.

8) REITs. This was a mixed bag, but mostly good. CRE is really benefiting from the 5-year lack of additional supply and a reconstitution into the Sunbelt, aka Red states. (Sorry, the picture in blue vs red is pretty significant.) Resi is mixed depending on geography as well. But again, you have such a limited build occurring. And I see people arguing that it's not the rates that are doing it, it's the uncertainty. But to me, that's a red herring. If rates were lower, you'd take the uncertainty risk in most cases.

9) Utilities. 100% are demonstrating the need to build. And it's not just built to generate energy. It's also built to enhance the grid. As a result, the parts of Industrials and tech that deal with power storage both showed great numbers this quarter, in line with a demand that was willing to offer margin to get things done faster.

10) Materials. Very strong b/c of the dynamics also driving energy and industrials. Chemicals were obviously going to a few awkward players due to SOH. But those guys were already struggling before this scenario. Mostly, they benefited from tariffs, anything that hit non-US competitors, and the massive Industrial, Utility, and Energy demand.

11) Capacity. For all of the strong areas, it's worth mentioning that there is a slow thoughtfulness to building capacity. This is why I still argue for rates, though I get that the SOH makes it harder. For a lot of these industries, little to no capacity has been built in this decade. And in some cases b/c the industry left US shores, the situation is quite tight.

12) Inventory Build. That said, b/c of the Tariffs and the many things that happened at the beginning of this decade, most are running inventories that are healthy enough to pace out the impact of Q1's geopolitics. It's really amazing given how much of the first 2 decades of this century were about just-in-time. Supply chains weren't this fragile this time around. But my impression is that this is a quarter by quarter phenomenom.

13) Food Inventory. As an example, Fertilizer, which got a lot of airtime, is mixed. In some cases - as with $MOS - it's just springloading. The farmer has a choice whether to apply or delay until next year. With $CF (nitrogen), it's also mixed. The US is the low-cost provider, and so it comes down to what will be used here vs. what we will export. And recall, if it's on US shores and falls under Ag there are unique solutions that always crop up. As for the actual plants, it's always hard to say in spring. We - unlike Central/S. America - really do have mostly 1 season for harvest.

14) Software. This is the most confused area of Tech and it's player by player because of AI. In some cases, AI offers fundamentally different approaches to doing things such that strategies are undergoing very meaningful changes that the organization are still trying to absorb. In other cases, this software was right into the sweet spot. This quarter has been about figuring out who is in which strategic position.

11) Data. Unambigiously, the data providers both in Tech and Finance were doing great.

12) Computer Hardware/Semi/Semi-Equipment. We all saw $DELL. The demand is there, and it is very real. But I really have to express how much that demand is also showing up in Real Estate, Industrials, & Materials. And recall, this is the S&P 500, and these companies are global.

13) Finally, Energy & Mining, there's no real need to comment on, given SOH has demonstrated what the US can do with its natural resources. I would mention that a lot of folks are only just learning about the beautiful geology of America. And as a result, they are not aware that for the US, it's not about not having resources, but which federal lands we are comfortable contributing to this effort. I do hope anyone with a thesis here just takes a moment to look at the US map of federally owned land and then juxtapose it to the hundreds of US geological surveys that exist.

Final Remarks

Overall, scale of 1 to 10, this mix of positive vs negative is around an 8.5/9 healthy level relative to this decade.

It feels like these companies are "chomping at the bit." Whether they need more less staff is hard to say despite the newsflow from specific industries.

My gut feel is that a rate cut would be applied to building capacity rather than just the share buybacks we saw in previous centuries. THOUGH, in some very specific cases, you'll get the buy-backs. This is particularly true if you cannot get the uncertainty down in certain very specific end markets (Consumer Discretionary, media, Energy, Financials, etc).

I think most are trying to figure it all out on headcount in a very changing, transforming environment. The image below is a chart summary I use to keep up with my progress.

I begin the new quarter on June 1st, regardless of what Fiscal quarter it is for the companies. Have an excellent weekend.

GS piece I mentioned. goldmansachs.com/insights/ar…

1

11

3,665

I was sent me this on Conservative ladies giving up their right to vote.

Ya’ll just b/c I think the extreme left is bonkers doesn’t mean I think extreme right is sane.

Stupidity knows no political party. If you don’t want to vote. Just don’t vote.

instagram.com/reel/DZds8LcDR…

3

393

Wow... that's really cool.

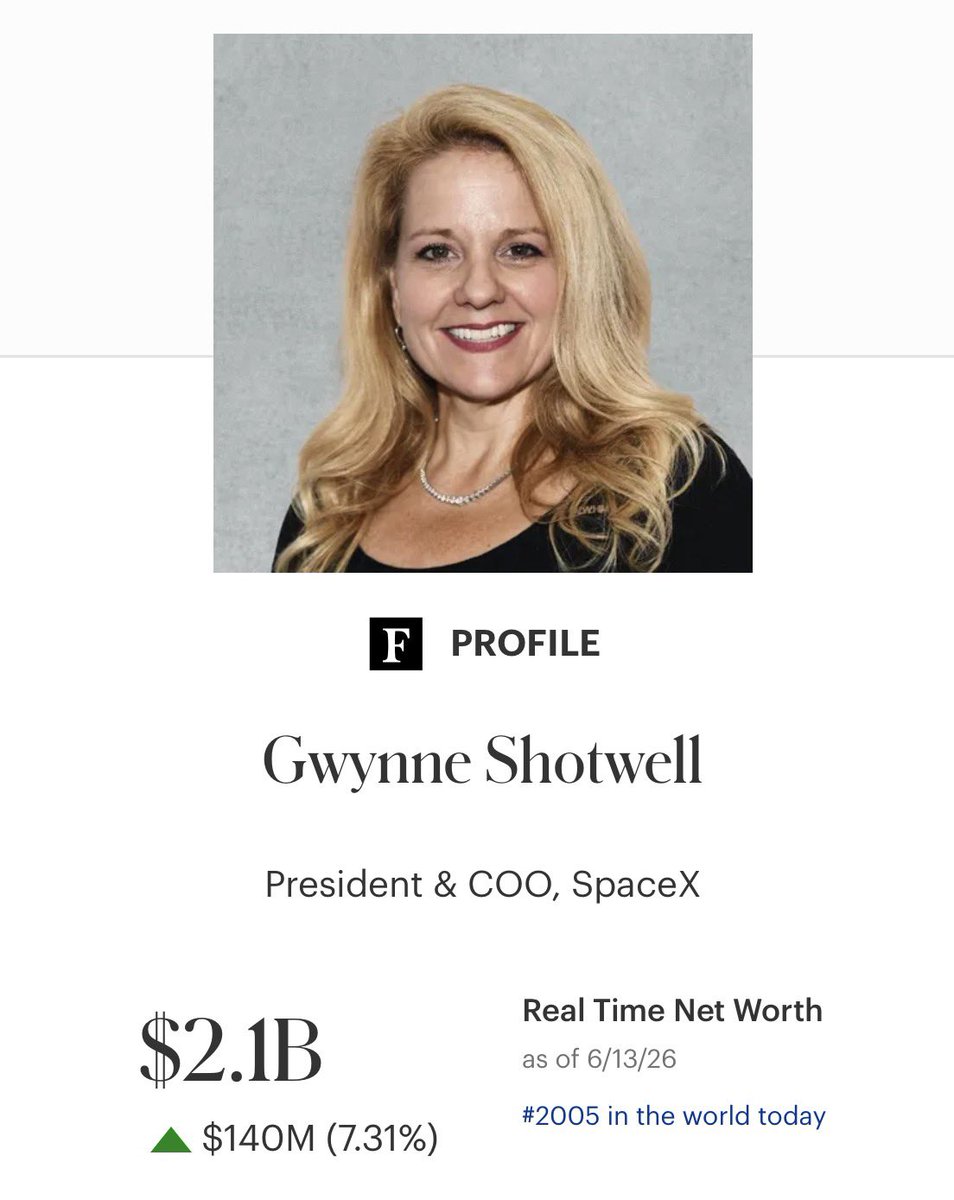

If she wasn’t working for Elon Gwynne Shotwell would be hailed as an incredible success story and the most powerful woman in aerospace.

Instead it’s radio silence from the media

2

16

2,219

$spcx … wow

1

1

830

Elon Musk becoming a trillionaire proves even after you’ve accomplished a lot there can always be more to accomplish. There isn’t really a concept of having done everything in a lifetime.

Idk … for me…as you age, it’s wonderful to be reminded of it.

2

15

851

Jun 13

Jaeger La-Coultre… was watching some social media pronouncing it “Jae” instead of “Yay” and was so confused. It seems the brand has recently anglicized for the English markets. Idk how I feel about that…

On the one hand, it’s a bit like Hearing Hermes will now be her-mees. On the other hand, I prefer pronouncing Target, tar-jay….

3

5

1,229

Jun 12

Regarding the 2x per year reporting change....I'd be cool if it was tri-annually? I mean 12 divides by 3 just as easily as by 4 and 2...

SEC Rule S7-2026-15 would let public companies stop filing quarterly reports and hide financials for six months. Your savings are in those stocks. Comment is open right now.

1

196

Jun 12

$TKO is in the S&P 500. It's newer, and I'm just learning them. If someone from TKO IR is on X and could help me understand the economics, that would be amazing... like, are you paying the White House (the US taxpayers) a rental fee?

TBH, if that's what's going down, given how much they make on the fights, I'm kinda ok on this... I think.... without hearing more discussion...

776

Jun 12

$SPCX.... funny how much value is created by capitalism... you'd almost think it's not a bad thing...

1

8

647

Jun 12

$SPCX... not gonna lie, the argument for why this should trade up to $175 on just mechanics is pretty strong...

I am long btw...

3

6

703

Jun 12

$LEN.... -2.3%

Rev -5%, Net Inc -36%

I'm still long a bit of this one b/c I wanted the $MRP and have sold a bunch since the allocation of those shares.

This one is tough b/c - as mentioned on the call - home prices have stayed stable, outpacing wage growth, but it's not easy for buyers.

In case there is confusion, this is what happens when you are undersupplying the market. Housing - b/c of the leverage component - is NOT the same as all other goods and services.

He then talks about Private Equity and how he does not agree with the legislation that reduces their purchases. This is b/c this will only lead to the builders building even less to support a rental market that is already very tight.

Ultimately, this call was a little bit of a capitulation that the structure of housing will have to meaningfully change... though not in the way most folks are talking about it.

Most are discussing how home values are too high. They are talking about how to reconfigure what needs to be built to make a price situation that entry-level home builders can have a shot at.

It kinda sounds to me like you'll have a very different mix of what's produced, not less produced in general. But a little bit hard to say. Given this major shift - which incidentally comes from the rate issue, not the other stuff - I really want to listen to a manufactured housing call to understand what precisely is going on.

2

397

Jun 12

Fun habit I've added is listening to books of wisdom while doing my daily walks (1-2hrs). They build resistance to the inundation of negative propaganda. Even though from the early 1920s, most discuss how continuous negativity enslaves, dis-empowers, and dis-empowers.

Here are 2 from today:

youtube.com/watch?v=gVr4sbNG…

youtube.com/watch?v=o0Exu8S7…

573

Jun 12

I think people who have "investor" in their bio are so weird. In 2026... who isn't an investor?

I mean...Why not put "human" in your bio? That would actually be more helpful to me in 2026.

2

8

642

Jun 12

$ADBE... -7.8%

Rev 13%, Net Inc 1% (Op Inc 10%).

The lower margin was tax provisions (corp action stuff). Yes, the CFO is done. Yes. That's weird in some ways, not in others.

I think everyone wants to find the bottom in $ADBE. Since 2023, the chart looks like the green slopes in Colorado, nice and even, but down the mountain nonetheless.

So how do we think about this in the context of AI, which is massively changing creator workflows?

IDK, tbh. You have to bet that they will use the balance sheet and actually be allowed to consolidate some of the tech. It's not an insignificant issue to believe this, given it was the UK, not the US, that blocked $FIG.

My position size was small on the off chance they would have said something or done something inspiring this Q.

I think they are on it. It's just a little hard to see easily. They do have the money, though. They're throwing off over $1b in FCF (even with recent corp actions) with less than $5b in debt.

Have to think about this a bit...

6

596

Jun 12

$SPCX …. Love this guy calling out the many folks who are posting their allocation before desks have allocated. 🤣🤣🤣

2,236

Jun 12

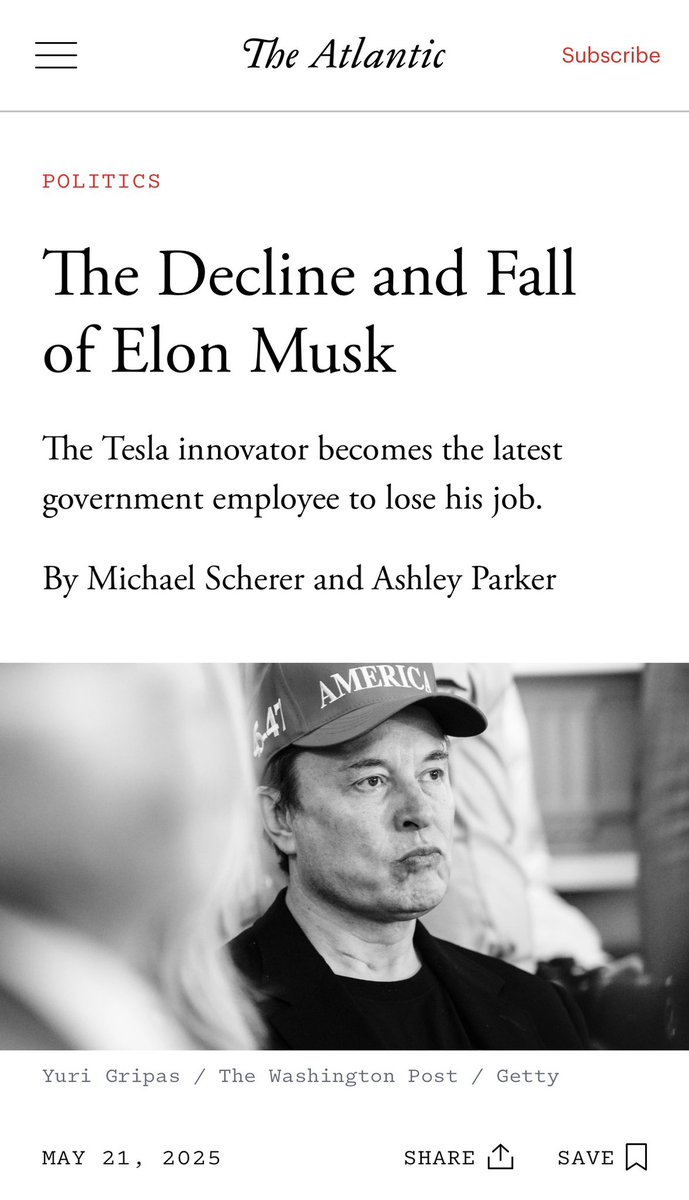

$SPCX @michaelscherer @AshleyRParker …. Thoughts…

Maybe your next article can be on bias at media companies or weaponizing reporting?

386 days after Elon’s decline and fall…

He’s the World’s first trillionaire.

The Media truly does suck.

5

846