~Your Jack of All Trades~ “Great minds discuss ideas; Average minds discuss events; Small minds discuss people” ~Eleanor Roosevelt

Joined January 2011

- Tweets 9,231

- Following 286

- Followers 578

- Likes 70,696

306 Photos and videos

Mel retweeted

Jan 10

Happy belated New Year! I just hit send on Ripple’s quarterly shareholder email. To say that 2025 (and Q4) were successful for Ripple feels like saying @TomBrady was just a great quarterback!! (#theGOAT)

Our two major acquisitions - Ripple Prime and GTreasury - greatly accelerate and expand our ability to deliver on our vision, enabling the Internet of Value. XRP has been (and will continue to be) the heartbeat of that vision.

With truly the most comprehensive licensing portfolio (and now today UK’s EMI license added) we are poised to make 2026 even more consequential.

Building and using crypto infrastructure, updating our global financial plumbing, and rethinking legacy systems – none of this happens overnight. At Ripple, we’re going to continue taking the long view of what crypto-based assets – like XRP and RLUSD – can do, rather than chasing cycles and hype.

Bring on 2026. We are firing on all cylinders. It’s happening!

1,074

3,152

15,405

1,337,962

Mel retweeted

26 Nov 2025

This is what you get when you mix the best selling single of the king of pop with the lately departed queen of MAGA: "MTG Has Broken Cover" 🎶🕺

- with a shout out to @awzurcher & colleagues for helpful coverage (despite, ya know, BBC awkward situation)

312

2,751

8,678

550,342

Mel retweeted

25 Nov 2025

Last month, @Ripple completed the acquisition of Hidden Road (now Ripple Prime) who serve 300 institutional customers, clearing $3 trillion across all markets annually 🚀

@Ripple is now the first crypto native company to own a global, multi-asset prime broker (FX, digital assets, derivatives, fixed income more)

We have already seen significant growth since the announcement, and XRP & RLUSD will be used as collateral for institutional clients 🚀

The institutional era just leveled up

#RLUSD #XRP

67

483

2,374

180,735

Mel retweeted

6 Nov 2025

These arguments that ripple is only worth their XRP holdings and therefore is worthless because xrp is worthless and all the people who own xrp have been duped and lack agency requires fairly stunning amounts of cognitive dissonance to pull off.

5 Nov 2025

Ripple just raised $500 million from a group of marquee investors.

But here’s how outside VCs see it:

“[The company] is not worth anything outside of XRP holdings. No one uses their tech. No usage on the network/blockchain.”

@steven_ehrlich investigates

unchainedcrypto.com/are-inve…

121

198

1,305

160,709

Mel retweeted

31 Oct 2025

It was a late afternoon in London, inside a private boardroom overlooking Canary Wharf. Around the table sat senior executives from three of the world’s largest banks, along with representatives from Ripple. I was there as one of the directors overseeing cross-border settlement strategy.

The discussion was clinical, not speculative. Spreadsheets, cost models, and projected efficiencies were all laid out in front of us. The data was irrefutable.

One XRP equals one million drops.

An average transaction consumes around ten drops, or 0.00001 XRP.

As long as those ten drops remain valued below one dollar, the cost efficiency is unmatched. Every executive in that room understood what it meant. Profit margins could be widened, client fees reduced, and settlement times reduced from days to seconds.

The only challenge left on the table was compliance — KYC, AML, and identity verification frameworks. Once those are fully synchronized with the XRP Ledger, it will deliver what every global banker has pursued for decades: instant settlement, institutional transparency, and scalable profitability across borders.

That afternoon in London, it was clear to everyone present. The future of global payments had already been engineered.

90

314

1,830

394,805

Mel retweeted

28 Oct 2025

This should be run as TV ads NOW‼️ SHARE‼️ REPOST‼️

926

8,601

19,714

384,215

Mel retweeted

27 Oct 2025

NewsMax talking about the USGOVT buying XRP to pay off the national debt. That's all!

Lock in. 😎👇

27 Oct 2025

🚨 HUGE NEWS:

NEWSMAX IS DISCUSSING THE POTENTIAL USE OF #XRP TO ELIMINATE THE NATIONAL DEBT! 📺

Video credit: @JOLLY__R0GER

20

119

628

41,652

Mel retweeted

24 Oct 2025

With today’s close of Hidden Road (now Ripple Prime), Ripple has announced 5 major acquisitions in ~2 years (GTreasury last week, Rail in August, Standard Custody in 2024, Metaco in 2023). As we continue to build solutions towards enabling an Internet of Value – I’m reminding you all that XRP sits at the center of everything Ripple does. Lock in.

Introducing Ripple Prime: We’re pleased to share that our acquisition of Hidden Road is officially complete, making Ripple the first crypto company to own and operate a global, multi-asset prime broker – bringing the promise of digital assets to institutional customers at scale. ripple.com/insights/ripple-c…

1,739

5,981

22,729

3,490,994

Mel retweeted

24 Oct 2025

“XRP sits at the center of everything Ripple does. Lock in.”

you heard it.

from the man himself.

it’s happening 👇

24 Oct 2025

With today’s close of Hidden Road (now Ripple Prime), Ripple has announced 5 major acquisitions in ~2 years (GTreasury last week, Rail in August, Standard Custody in 2024, Metaco in 2023). As we continue to build solutions towards enabling an Internet of Value – I’m reminding you all that XRP sits at the center of everything Ripple does. Lock in.

148

539

4,472

173,853

Mel retweeted

6 Oct 2025

XRPL’s new Multi-Purpose Token standard is built for institutions.

✅ Compliance baked in

✅ RWA-ready

✅ Every move burns $XRP

3 Oct 2025

🔗💰 The XRP Ledger (XRPL) is making a strategic leap into institutional finance with the activation of its Multi-Purpose Token (MPT) Standard (MPTokensV1 amendment). This new, protocol-native fungible token is specifically designed to meet the rigorous compliance needs of major financial institutions, streamlining the tokenization of Real-World Assets (RWA) and institutional-grade instruments.

The MPT standard's main innovation is integrating critical compliance and control features directly into the XRPL's core protocol. This architectural choice is a direct response to a major pain point on other platforms: the high operational risk and complexity associated with custom smart contracts (like those on EVM-based platforms).

For regulated entities, the MPT offers an essential compliance toolkit:

🥶 MPTs provide built-in mechanisms for granular asset freezing (equivalent to Deep Freeze) and necessary fund clawback capabilities. These non-negotiable features allow issuers to comply immediately with sanctions, mitigate fraud, or recover assets lost due to operational failures.

🪪 The standard supports sophisticated access control using an integrated identity framework (DIDs and Credentials). This allows issuers to restrict token transfers only to explicitly authorized, KYC-verified holders.

⏳ By baking core functionality into the highly secure, battle-tested XRPL protocol, MPT significantly reduces the need for expensive, bespoke smart contract development and auditing. This can translate directly into lower development timelines and a potential reduction in regulatory capital allocated for operational risk.

The MPT architecture is engineered for high-volume, regulated settlement:

🚄 It leverages the XRPL's core strengths, offering 3-5 second transaction finality and extremely low, fixed transaction fees (paid in XRP). This efficiency is a massive operational cost benefit compared to the variable, often high gas fees of other networks.

👮The standard enforces a clear separation between the token issuer and the holder, automatically burning any tokens sent back to the issuer. This ensures a transparent, auditable circulating supply—essential for regulatory reporting.

💻 MPT includes a native metadata field that supports standardized data structures like XLS-0089d and integration with the Actus Standard. This enables MPT to function as a "true digital contract" by housing essential, machine-readable terms (like maturity dates) alongside the asset, facilitating seamless integration with external financial risk and valuation systems.

Strategic Implications for XRP Utility

The successful adoption of MPT for RWA tokenization—a market forecasted to reach trillions of dollars—is intrinsically linked to the utility and value of XRP.

The system is designed to amplify XRP's role as the essential utility layer:

🔥 Every MPT operation (issuance, transfer, management) requires a small fee paid in XRP, which is then permanently burned. High-frequency RWA trading will exponentially increase this burn rate.

Every new MPT issuance and the corresponding ledger objects needed to track holder balances require a small, fixed amount of XRP to be locked as a reserve, taking it out of circulation.

This utility model is a key strategic pivot, shifting the XRP valuation narrative away from pure speculation and toward a mathematically quantifiable model based on verifiable, high-throughput global financial activity. The MPT standard strategically positions the XRPL as the leading secure and compliant institutional blockchain for the future of tokenized finance.

31

186

952

73,097

Mel retweeted

4 Oct 2025

After a week of meetings with lots of partners in Singapore I’m more convinced of the utility of what Flare is building that at any point in the past. 🐂

61

191

1,009

89,091

Mel retweeted

13 Sep 2025

Texas pastor @jamestalarico flips the script on anti-trans attacks: “we’re focused on the wrong 1%.”

763

12,332

48,460

989,080

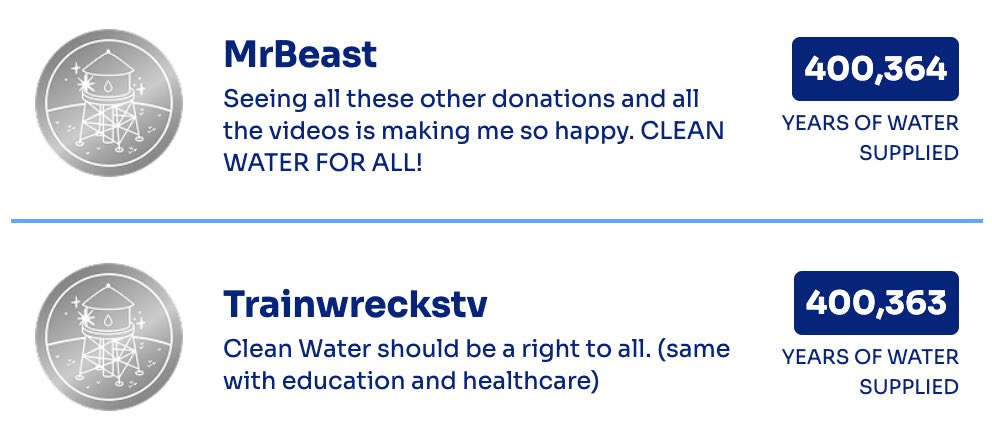

I just donated $400,364 to TeamWater!!

($1 more than @Trainwreckstv so I could be above him 🤪)

2,050

1,236

61,822

3,964,284

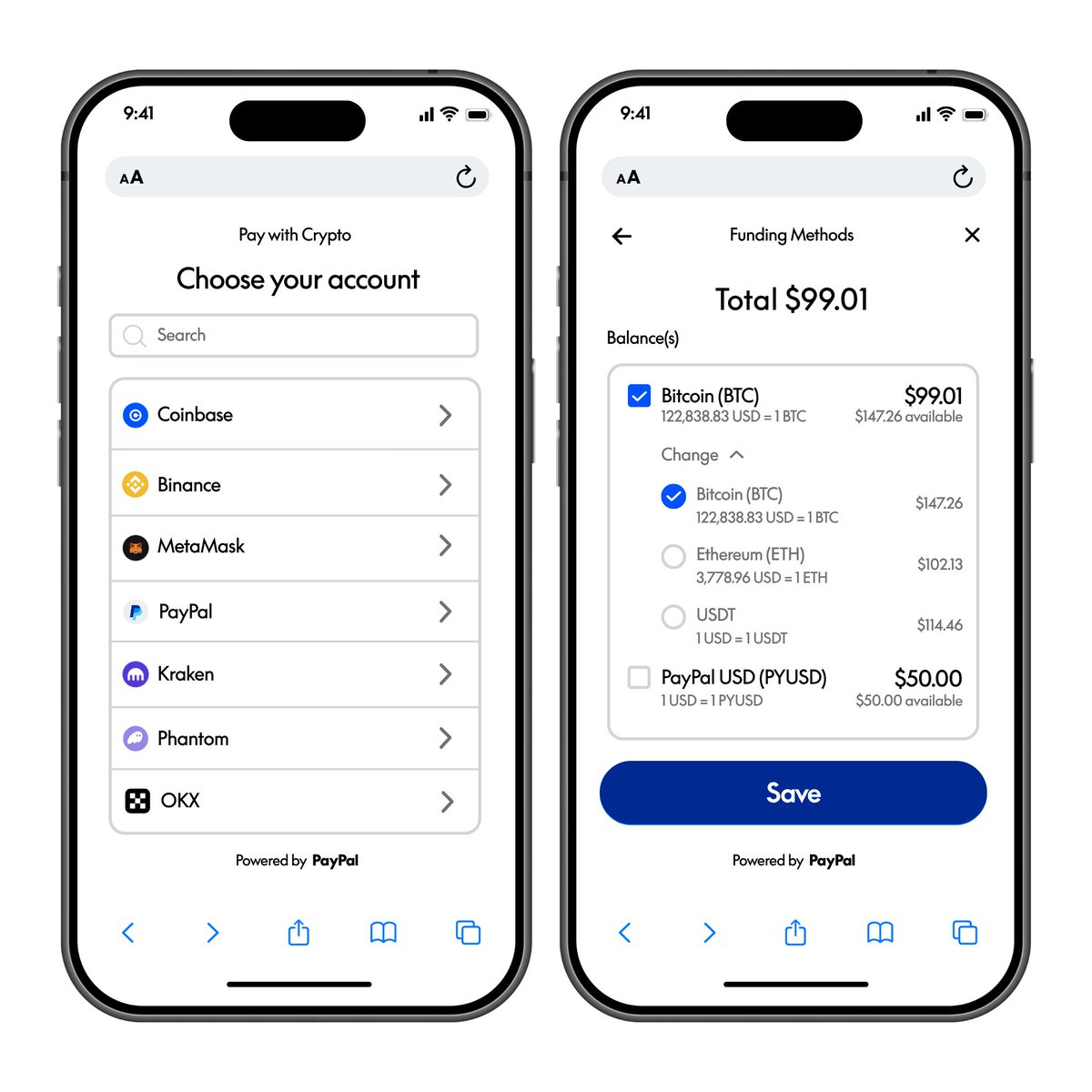

Tired: Paying high transaction fees for international payments.

Wired: Reducing costs up to 90% by offering pay with crypto for payments.

✅ Reduce international transaction fees by up to 90%

✅ Offer 100 cryptocurrencies and eligible wallets at checkout

✅ Get immediate access to funds

We’re making all of this, and more, easily accessible and available through Pay with Crypto, a new payment method that allows merchants to reach more than 650 million crypto users and allow them to pay using any of hundreds of eligible wallets and cryptocurrencies: newsroom.paypal-corp.com/202…

535

1,381

5,529

1,330,742

Mel retweeted

15 Jul 2025

💯So #XRP is FAST!

We GET that already! 👌

BUT the FUTURE of #blockchains are NOT solely about SPEED..

It is: AMENDMENT XLS-81d

IDENTITY

Compliance

And LEIs 😎😎

#iso20022 #cryptonews #ripple

11

109

450

19,959

Mel retweeted

17 May 2025

Miguel Vias (former Ripple employee) telling us the difference between what Ripple the company is trying to do (in accordance with cross-border payments) and how Ripple is using XRP.

There seems to be some confusion in this area. Ripple the company is trying to replace SWIFT, while XRP facilitates instant settlement as a bridge asset by Ripple.

XRP(L) is not competing with SWIFT.

In order words, other payments systems could in theory use XRP for instant settlement as well, it doesn't have to be Ripple. It's open source software.

Theoretically SWIFT could use XRP as a bridge asset, as an example, if they really wanted to.

23

91

347

44,915