18 Photos and videos

With $5k you can buy ~5 shares of $MU… or put it to work in a defined-risk bull call spread.

Long the $900 call, short the $950 call.

Example: ~$25 net debit ($2,500 total).

• Max loss: Limited to the $2.5k debit paid.

• Max profit: Strike width minus debit if $MU closes at or above $950 at expiration (roughly doubles the risk capital on this setup).

• Breakeven: $900 net debit.

Lower capital requirement than stock, leveraged bullish exposure with capped downside ahead of the June 24 earnings catalyst.

Not financial advice. Options involve substantial risk of loss and can expire worthless. Greeks (theta decay, vega) matter. Do your own research and size responsibly.

64

NipSh 13 retweeted

Jun 13

Iran peace deal could be FINALIZED in the next 24 hours per the Pakistani PM.🚨

92

41

303

7,457

📊 $AGI — Gold leverage with the cost curve already turning in your favor.

At ~$34.5 (38% off the $55 high), you’re getting a mid-tier producer guiding for meaningfully lower AISC through 2026 as low-cost ounces ramp at Island Gold. Q1’s temporary cost overrun is explicitly flagged as reversing — not a structural problem.

The real engine: Mineral reserves up 32% YoY to 15.9M oz (7th straight year of growth, grades also rising). Production scaling from current levels toward 570-650k oz in 2026 and 755-835k oz by 2028.

Net cash balance very low leverage gives real downside cushion while gold’s structural bid (central banks geopolitics) does the heavy lifting on the upside.

This is operating leverage to gold with improving unit economics already in motion — not just riding the metal price.

Not financial advice. Do your own research. Size for volatility.

41

📊 $MU — The AI memory name with actual sold-out visibility.

At ~$982 (still only ~10% off the $1,089 high), forward P/E sits at just ~9.9x while earnings are exploding toward ~$57 for FY26. PEG around 0.34. ROIC at 37% . Q2 revenue hit $23.86B (nearly 3x YoY) with gross margins already ~75% and guiding ~81% next quarter.

The real edge most people are missing: Micron’s entire 2026 HBM output is already sold out under multi-year contracts. Tight supply massive hyperscaler AI spending = real pricing power and revenue visibility that typical semis don’t have.

Q3 earnings drop June 24 — high-asymmetry catalyst. Strong beat/raise = serious melt-up fuel. Miss = sharp reset (size for it).

Downside has a floor most growth names lack because of those contracted HBM volumes. This isn’t just another AI memory story — the numbers actually back the structural shift.

Not financial advice. Do your own research. Size responsibly.

1

69

📊 $CME — The quiet infrastructure play nobody’s talking about.

Trading ~$269–270, still ~18% off its $329 high. Every spike in rate volatility, equity swings, macro uncertainty, or geopolitical noise drives futures/options volume straight to their bottom line.

The chaos is literally the product.

Q1 delivered record revenue on exactly that dynamic — higher hedging demand across rates, equities, and commodities. Vertically integrated model (trading own clearinghouse) creates a real moat: deepest liquidity, capital efficiencies for clients, and sticky institutional flow.

Not the flashiest AI or commodity name, but one of the cleanest ways to own “uncertainty as a tailwind” with quality compounding, ~1.9% dividend, and reasonable ~22x forward P/E.

Next catalyst: Q2 earnings July 22.

High-conviction infrastructure bet heading into a noisy macro summer.

Not financial advice. Do your own research. Position sizing > thesis.

1

45

📊 Top 3 picks heading into next week:

$CME — Financial infrastructure nobody talks about. Trading at $262, 18% off its 52-week high of $321. Every rate volatility, futures volume surge, and macro uncertainty event drives their revenue. The chaos is the product. Jan’28 $200C already 26%.

$MU — Memory is back. $993/sh, ~9% off all-time high of $1,089. Q3 earnings June 24 — HBM demand is structural, not cyclical. AI data centers need more memory than anyone modeled. 137 hedge funds holding. This is the next leg, not the last one.

$AGI — Best-run mid-cap gold miner, period. At $34.49, sitting 38% off its 52-week high of $55. If you believe gold goes higher, this is where you want to be — not the metal itself. AGI has the cost discipline to convert gold’s move into actual margin. When gold runs, AGI runs harder.

Not financial advice. Do your own research. Will be sharing some details on each

23

🚀 SpaceX (SPCX) IPO this week — record ~$75B raise incoming.

Institutions will need to free up serious capital. Watch these names for potential rotation selling pressure:

$AMD | $AVGO | $MU | $TSLA | $NVDA

(sell Elon’s car, buy Elon’s rocket 👀)

This isn’t macro. It’s the largest IPO in history sucking liquidity.

$SPCX on deck.

Positioned how?

205

$AGI is the pick-and-shovel play nobody’s talking about.

Gold corrects. Sentiment tanks. Miners sell off harder. That’s the entry. 🧵

1/ What AGI actually is

Alamos Gold. Mid-tier North American producer. Not a leveraged junior gambling on a discovery — a real operating business with real cash flow, expanding high-grade mines in Canada and Mexico. No political risk. No currency disasters. Just gold in the ground and the people who know how to get it out.

2/ The numbers are genuinely good

→ Forward P/E: ~12x

→ PEG: 0.77 (you’re paying less than 1x growth)

→ Debt/Equity: 4.5% — basically debt-free

→ Reserves up 32% to 15.9Moz with rising grades

→ 2026 production 12% (570–650k oz)

→ AISC dropping to $1,500–$1,600/oz

At $4,325 gold they’re printing ~$2,700/oz margin. That’s not thin. That’s a machine.

3/ The leverage is the point

$GLD gives you 1:1 gold exposure. Clean, no drama.

AGI gives you operating leverage. Gold up 20% = AGI FCF up 40% . Margins expand faster than the metal moves. That’s why miners exist in a portfolio — they amplify the thesis when it works.

4/ The risk is real, name it

Gold drops to $3,800–$4,200 = margin squeeze. AGI’s balance sheet survives it. 4.5% debt/equity means no refinancing crisis, no dilution, no emergency equity raise. They weather the cycle. Most juniors don’t.

5/ The setup

AGI is currently down with the gold correction. You’re buying a growing, low-debt, high-margin producer at 12x forward earnings with a PEG under 1 — during a 23% pullback in the underlying commodity that institutions are still calling a structural bull market.

The base case: gold recovers to $5k . AGI re-rates hard.

Don’t chase. Scale in on dips. Pair with $GLD as the foundation.

$AGI $GLD

109

Gold just corrected 23% from its Jan ATH of $5,595.

Half of fintwit is calling the bull run dead.

Here’s why they’re wrong 🧵

1/ This correction was inevitable

Gold gained 60% in 2025 — best year since 1979. Parabolic moves get sold. Hot US jobs data pushed back rate cut expectations. Dollar strengthened. Classic short-term headwind. The reason gold ran — CB de-dollarization, geopolitics, monetary debasement — none of that changed.

2/ Central banks don’t panic-sell

863 tonnes bought in 2025. Q1 2026: 244 tonnes — up 3% YoY, above the 5-year average. Poland, China, emerging markets all still adding. This is de-dollarization, not a trade. These buyers absorb every dip.

3/ The bear case requires a miracle

For gold to genuinely reverse you need ALL of this at once:

→ Fed hiking again

→ Inflation below 2%

→ Middle East peace deal

→ Central banks stopping purchases

→ USD 20% sustained

Zero of those are happening.

4/ What the numbers say

Goldman: $5,400 YE2026

JPMorgan: $5,000–$6,300

Wells Fargo: $6,100–$6,300

Reuters poll, 31 analysts: $4,916 median

$4,325 today. Consensus sees $5,000 by December. You’re being handed a 15-18% setup that was 23% more expensive in January.

5/ The cleanest way to play it

$GLD — allocated physical gold, no mining risk, no leverage, pure price exposure. Direct line to every structural driver. DCA on weakness, hold through the noise.

The structural gold bull market is one of the clearest macro trades of the decade.

You’re not late. You got a second entry.

115

$GLD – The simplest, most conservative way to own physical gold. Holds allocated gold bullion; tracks spot XAU/USD closely (minus modest expense ratio). No mining/operational risk, no leverage, pure price exposure.

Current environment: Gold correcting ~23% from Jan ATH to ~$4,325. GLD moves in line (recently ~$397–$410 area). Benefits directly from the same structural drivers (CB buying, geopolitics, monetary backdrop) without company-specific issues.

12-month outlook (mid-2027):

• Bull case (gold moves back to $5,000–$6,000 ): Clean 15–40% upside in line with spot. Lowest friction way to capture the move.

• Bear case (gold extends correction to $3,800–$4,200): Direct downside in line with spot (no operating leverage cushion or amplification). Still the cleanest expression of the gold thesis.

Conservative take: Core position for gold exposure right now. Use it as the foundation, then layer selective miners (like AGI) only if you want extra upside beta. DCA on weakness; hold through volatility. No operational surprises.

75

Gold at $4,325. Down 23% from January’s $5,595 ATH.

Everyone’s asking if the bull run is over.

It’s not. Here’s why 🧵

1/ What actually happened

Gold ran 60% in 2025 — its best year since 1979. Parabolic moves get corrected. This one was overdue. The pullback has nothing to do with the structural drivers that caused the rally. It’s profit-taking hot US data pushing back rate cut expectations a stronger dollar. Temporary, not structural.

2/ The floor is real

Central banks bought 863 tonnes in 2025 — nearly double the pre-2022 average. Q1 2026: 244 tonnes, up 3% YoY. Poland, China, emerging markets all adding. This isn’t a trade. It’s de-dollarization. These buyers don’t panic-sell on a bad CPI print.

3/ The thesis hasn’t broken

For gold to genuinely reverse you need ALL of this simultaneously:

•Fed hiking again

•Inflation below 2% sustained

•Middle East peace deal

•Central banks stopping purchases

•USD rallying 20%

None of that is happening. Not even close.

4/ Where we are technically

$4,319 = the yearly open. Critical level being tested right now. Below that, next real support is $4,100–$4,200. A break there opens $3,800–$3,900. That’s the bear case — painful, not terminal.

To resume the uptrend, gold needs to reclaim $4,500, then $4,800.

5/ What the big banks say

•Goldman Sachs: $5,400 year-end

•JPMorgan: $5,000–$6,300

•Wells Fargo: $6,100–$6,300

•Reuters poll of 31 analysts: $4,916 median

Even the bears see $4,500 by year-end. The disagreement is on magnitude, not direction.

6/ The setup

$4,325 today. Consensus target $5,000–5,100 by December. That’s a 16–18% move from current levels — better risk/reward than buying at $5,500 in January.

The structural bull market for gold is one of the clearest macro trades of this decade. You’re being handed a re-entry.

The only question is whether you have the patience to sit through the noise.

Gold doesn’t care about your timeline. It moves on its own schedule.

64

Still green today. Went up 0.5%

$CME just hit fresh 52-week lows while reporting record May ADV of 33.2M contracts — up 15% YoY.

Berkshire just anchored Alphabet’s $80B AI infrastructure raise with a $10B commitment. Every dollar of that capex and financing needs hedging in rates, commodities, and beyond.

CME clears the vast majority of it.

Business at all-time highs. Stock price at multi-month lows. Classic dislocation.

63

🥊 $SOFI vs $HOOD head-to-head

Forward P/E: SOFI 26x vs HOOD 36x

Revenue growth: SOFI 41% vs HOOD 15%

Debt/Equity: SOFI 0.18x vs HOOD 1.40x

Platform assets: SOFI $40B deposits (bank) vs HOOD $307B AUM (brokerage)*

More growth. Cheaper multiple. Cleaner balance sheet → $SOFI

Bigger platform, higher margins, covered call optionality → $HOOD

Different animals. Pick your thesis.

*Deposits ≠ brokerage AUM

Not financial advice. DYOR.

211

🚨 $SIVE alert — not a buy call

Stock up 37x in 12 months. Trading at 70-90x revenue. Losing money. Cash runway ~3 quarters. Analyst PTs: SEK 6-10. Stock at SEK 90 .

Largest shareholder in debt restructuring — forced seller incoming.

GlobalFoundries partnership is real. The valuation is not.

Pipeline ≠ revenue.

Not financial advice. DYOR.

409

$CME just hit fresh 52-week lows while reporting record May ADV of 33.2M contracts — up 15% YoY.

Berkshire just anchored Alphabet’s $80B AI infrastructure raise with a $10B commitment. Every dollar of that capex and financing needs hedging in rates, commodities, and beyond.

CME clears the vast majority of it.

Business at all-time highs. Stock price at multi-month lows. Classic dislocation.

252

$CEG entry here is a gift. Secondary offering flush cleared. Company bought back 2M shares at $281 the same day sellers dumped. Forward PE ~22x — low end of 4-year historical range. Strongest balance sheet in the AI power sector (D/E 0.66x). TMI/Microsoft nuclear PPA. 27 analysts avg PT $368. 35% below ATH. The overhang was a liquidity event not a thesis break.

307

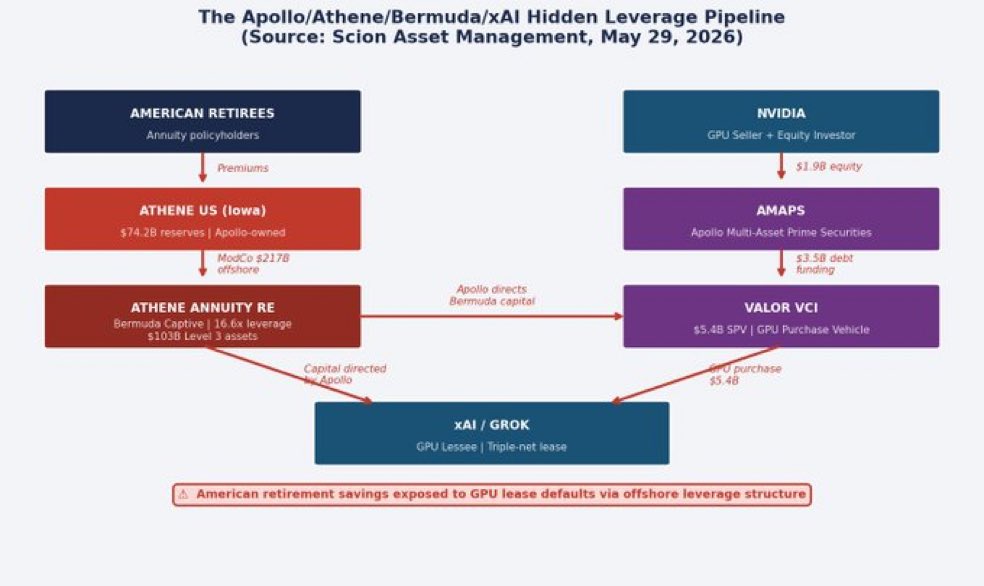

American retirees are unknowingly funding GPU leases for Elon Musk’s Grok. When xAI can’t pay, their annuities take the hit. This is the pipeline nobody on Wall Street is talking about publicly. 🧵

#AI #Investing #Stocks #WallStreet

1

126

Smart Money

Who’s positioning for the crash?

Buffett: $397B cash. Largest pile in Berkshire history.

Burry: 2027-dated puts on NVDA, QQQ, and semiconductors.

Alibaba Chairman Joe Tsai: “I see the beginning of some kind of bubble forming.”

Micron CEO: Sold $511-545 systematically on May 1.

These aren’t retail bears. They know something.

1

100